|

시장보고서

상품코드

2044214

클라우드 POS 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Cloud Point Of Sale (PoS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

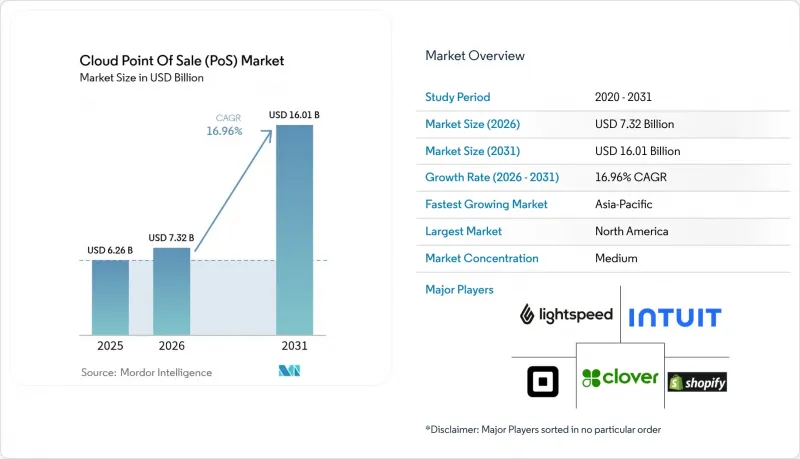

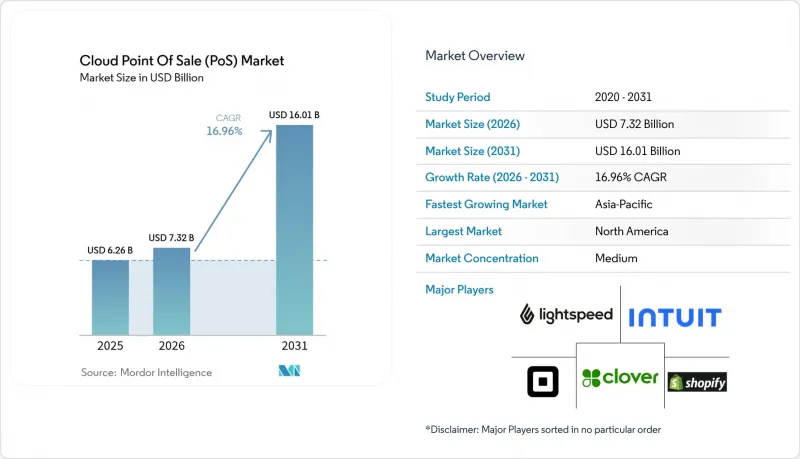

2026년 클라우드 POS 시장 규모는 73억 2,000만 달러로 추정되고 있으며 2025년 62억 6,000만 달러에서 성장하여 2031년에는 160억 1,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 16.96%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

스마트폰 사용 확대, 원활한 디지털 결제 경험, 실시간 데이터 가시성 확보가 지속적으로 도입에 힘을 실어주고 있습니다. 소매업체들은 계산대 대기줄을 없애기 위해 기존의 고정식 계산대에서 모바일 단말기로 전환하고 있으며, 호스피탈리티 산업 사업자들은 주문, 결제, 로열티 프로그램을 통합하는 플랫폼에 의존하고 있습니다. 정부는 현금 취급에 대한 규제를 강화하고 전자거래를 장려하고 있으며, 이는 사업자들을 클라우드 솔루션으로 더욱 밀어붙이고 있습니다. 공급업체들은 이에 대응하여 거래 로그를 예측적 인사이트으로 전환하는 인공지능(AI)을 통합하여 사업자가 재고 소진을 줄이고, 오퍼를 개인화하며, 수익률을 향상시킬 수 있도록 지원하고 있습니다.

세계 클라우드 POS 시장 동향 및 인사이트

현금 없는 결제의 기세

2025년까지 매장 결제 중 현금 결제는 10%에 불과할 것으로 예상되며, 이러한 전환점으로 인해 사업자들은 카드, 모바일 월렛, 계좌 간 결제를 받아들일 수밖에 없는 상황에 처해 있습니다. 클라우드 PoS 플랫폼을 이용하면 사업자는 하드웨어를 교체하지 않고도 하룻밤 사이에 새로운 결제 수단을 추가할 수 있기 때문에 미래지향적인 결제 수락의 표준 선택이 되고 있습니다. 이러한 변화는 비접촉식 카드가 주류인 북미와 규제 당국이 현금 사용 한도를 제한하고 있는 유럽에서 특히 두드러집니다. 생체인식도 도입되고 있으며, 얼굴인증이나 지문인식을 통한 결제가 가능해져 신뢰성과 속도가 향상되고 있습니다. 이용이 확대됨에 따라 아쿠아월러는 디지털 거래의 교환 수수료를 인하하여 클라우드 POS 시장의 잠재적 규모를 확대되고 있습니다.

모바일 퍼스트형 커머스 확산

모바일 커머스는 2025년 7,280억 달러를 넘어 미국 소매 전자상거래 매출의 거의 절반을 차지했습니다. 이러한 거래량에는 쇼룸의 한 구석, 매장 앞 공간, 또는 배송용 밴을 결제 포인트로 전환하는 모바일 POS 하드웨어가 필요합니다. 2024년 442억 6,000만 달러 규모로 평가된 mPOS 부문은 2029년까지 805억 8,000만 달러에 달할 것으로 예측됩니다. 아시아태평양의 소매업체들은 고정형 단말기를 넘어 클라우드 백엔드와 원활하게 연동되는 QR 코드와 NFC를 통한 스마트폰 결제를 자주 활용하고 있습니다. 소매업체들은 현재 mPOS를 고객 경험 향상, 대기 시간 단축, 무한한 상품 검색 기능 제공, 신속한 판매를 위한 개인화된 프로모션을 촉진하는 수단으로 인식하고 있습니다. 이러한 요인들이 복합적으로 작용하여 클라우드 POS 시장을 확대하는 동시에 기존 계산대의 모습을 변화시키고 있습니다.

데이터 보안 및 컴플라이언스 이슈

최근 이슈가 되고 있는 정보 유출 사건과 PCI DSS 위반으로 인한 벌금 등으로 인해 많은 기업들이 완전한 클라우드 전환에 나서지 못하고 있습니다. 레거시 On-Premise 서버를 운영하는 대형 체인은 최신 POS 제품군이 전송 및 저장 데이터를 암호화하고 있음에도 불구하고, 데이터 거주지에 대한 위험을 우려하고 있습니다. 벤더들은 토큰화, 제로 트러스트 아키텍처, 전담 컴플라이언스 팀을 제안하고 있지만, 인식의 격차는 여전히 남아있습니다. 고객 데이터의 기밀성이 높은 제약 및 고급 제품 산업의 소매업체들은 하이브리드 구축을 강력하게 요구하는 경우가 많으며, 그 결과 클라우드 POS 시장에서 퍼블릭 클라우드 구성의 단기적인 성장이 둔화되고 있습니다.

부문 분석

소프트웨어 부문은 2025년 클라우드 POS 시장 점유율의 59.40%를 차지했으며, 거래 엔진 및 분석 허브로서의 역할을 강조하고 있습니다. 정기적인 업그레이드, 실시간 패치 적용, 원격 기능 활성화로 하드웨어 업데이트 없이도 지속적인 가치를 창출할 수 있습니다. 도입에서 관리형 분석에 이르는 서비스는 CAGR 20.95%로 확대되고 있으며, 이는 컨설팅 및 아웃소싱 전문가를 위한 클라우드 POS 시장 규모를 확대할 것입니다.

최신 제품군은 재고 관리, 직원 스케줄링, CRM을 통합된 인터페이스로 통합하여 POS 소프트웨어를 일상 업무의 사령탑으로 재정의하고 있습니다. 사내 IT 인력이 없는 소매업체들은 도입, 맞춤형 워크플로우, 온콜 지원을 위해 서비스 통합업체에 의뢰하고 있습니다. 옴니채널을 지향하는 소매업체가 늘어남에 따라 라스트마일 배송 네트워크 및 ERP 시스템과의 맞춤형 통합에 대한 수요가 증가하여 서비스 부문의 성장을 가속하고 클라우드 POS 시장을 더욱 확대시키고 있습니다.

모바일 POS 솔루션은 2025년 매출의 57.20%를 차지했으며, 2031년까지 22.84%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측되어 이 선두를 유지할 것으로 보입니다. 소매업체들은 매장 내, 팝업스토어, 도로변 픽업 등에 태블릿과 핸드헬드 단말기를 도입하여 클라우드 POS 시장의 성장세를 뒷받침하는 유연성을 입증하고 있습니다. 고정형 단말기는 여전히 처리 능력이 높은 식료품 계산대에서는 필수적이지만, 현재는 많은 단말기가 클라우드에 연결된 노드 역할을 하며 중앙 집중식 분석을 활용하고 있습니다.

하드웨어의 발전(내충격성 케이스, 배터리 수명 연장, 클라우드 네이티브 OS 업데이트 등)으로 인해 모바일 단말기는 엔터프라이즈급 성능을 구현하고 있습니다. 조사 대상 소매업체 경영진의 절반은 서비스 수준 향상을 위해 mPOS를 도입할 계획인 것으로 나타났습니다. 접객업의 경우, 테이블 사이드 주문으로 인해 고객 회전율이 빨라지는 동시에 팁율도 향상되고 있습니다. 이러한 직접적인 ROI의 증거를 통해 모바일 단말기는 '있으면 편리한 것'에서 클라우드 POS 시장의 핵심 축으로 자리매김하고 있습니다.

클라우드 POS 시장은 구성요소(소프트웨어, 서비스), POS 유형(고정형 POS, 모바일/mPOS), 배포 모델(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 조직 규모(중소기업(SME), 대기업), 최종 사용자 산업(소매, 소비재, 숙박/레스토랑, 기타), 지역별로 세분화되어 있습니다. 소비재, 호텔/레스토랑, 기타), 지역별로 시장 세분화되어 있습니다. 시장 예측은 금액(USD) 기준으로 제시됩니다.

지역별 분석

북미는 기술에 정통한 소비자와 벤더의 집중을 바탕으로 2025년 매출의 34.70%를 차지하며 시장을 주도했습니다. '토스트'를 운영하는 미국의 레스토랑 체인 등은 주문, 결제, 로열티 프로그램을 하나의 플랫폼으로 통합하여 눈에 띄는 실적 향상을 이루었습니다. 토큰화 및 비접촉식 거래에 대한 명확한 기준도 플랫폼 도입을 가속화하고 클라우드 POS 시장 전체에 청사진을 제시했습니다.

아시아태평양이 가장 빠르게 성장하고 있으며, 2031년 CAGR은 19.92%로 예측됩니다. 중국의 Alipay와 WeChat Pay의 생태계는 가맹점에 네이티브 통합을 촉진하고 있으며, 일본에서는 셀프 체크아웃 키오스크를 통해 인력 부족을 보완하고 있습니다. 인도의 중소기업 디지털화 지원책은 지역 벤더들에게 새로운 발판이 되고 있으며, 2선 도시에서의 mPOS 활용을 확대시키고 있습니다. 통신 인프라의 업그레이드로 대역폭 격차가 줄어들면서 이 지역의 크로스보더 EC는 다국어, 다통화 지원 솔루션에 대한 클라우드 POS 시장 규모를 확대할 것으로 보입니다.

유럽에서는 시장이 성숙해졌지만, 규제 중심 수요를 볼 수 있습니다. 독일의 'Kassensicherungsverordnung', 오스트리아의 'RKSV'와 같은 규정은 안전한 회계 메모리와 변조 방지 로그를 의무화하고 있습니다. 많은 가맹점이 원격으로 컴플라이언스 업데이트를 제공하는 인증된 클라우드 스택을 선택하고 있으며, 이는 클라우드 POS 시장을 활성화하고 있습니다. 라틴아메리카, 중동 및 아프리카는 아직 개발 단계에 있지만, 미래 가능성이 높습니다. 무선 통신 영역의 개선과 정부의 핀테크 로드맵에 따라, 특히 오프라인 우선의 하이브리드 아키텍처를 통해 두 자릿수 성장이 예상됩니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02Cloud point of sale market size in 2026 is estimated at USD 7.32 billion, growing from 2025 value of USD 6.26 billion with 2031 projections showing USD 16.01 billion, growing at 16.96% CAGR over 2026-2031.

Greater smartphone usage, seamless digital payment experiences, and real-time data visibility continue to propel adoption. Retailers are swapping static tills for mobile terminals to remove checkout queues, while hospitality operators rely on unified platforms to blend ordering, payments, and loyalty programs. Governments are tightening rules on cash handling and encouraging electronic transactions, which further nudges merchants toward cloud solutions. Vendors are responding by embedding artificial intelligence that transforms transaction logs into predictive insights, helping operators trim stockouts, personalize offers, and boost margins.

Global Cloud Point Of Sale (PoS) Market Trends and Insights

Cashless-transaction momentum

Only 10% of in-store payments are expected to remain cash-based by 2025, a tipping point that forces merchants to accept cards, mobile wallets, and account-to-account payments. Cloud PoS platforms let operators add new tenders overnight without swapping hardware, making them the default choice for future-proofing payment acceptance. The shift is most visible in North America, where contactless cards dominate, and in Europe, where regulators restrict cash thresholds. Biometric authentication is joining the mix, allowing face or fingerprint-verified payments that boost trust and speed. As usage grows, acquirers lower interchange fees for digital transactions, widening the total addressable cloud point of sale market.

Mobile-first commerce adoption

Mobile commerce will surpass USD 728 billion in 2025, accounting for nearly half of U.S. retail e-commerce sales. Such volumes demand mobile PoS hardware that turns any showroom corner, curbside location, or delivery van into a checkout point. The mPOS segment, valued at USD 44.26 billion in 2024, is projected to reach USD 80.58 billion by 2029. Asia-Pacific retailers frequently leapfrog fixed terminals and rely on QR or NFC phone payments that integrate seamlessly with cloud back ends. Retailers now view mPOS as a customer-experience lever-line-busting, delivering endless-aisle lookups, and facilitating personalised promotions that close sales faster. These factors collectively expand the cloud point of sale market while altering the traditional checkout footprint.

Data-security and compliance gaps

High-profile breaches and PCI DSS penalties keep many enterprises on the fence about full cloud migration. Larger chains running legacy on-premise servers fear data residency risks even though modern PoS suites encrypt data in motion and at rest. Vendors counter with tokenisation, zero-trust architectures, and dedicated compliance teams, yet the perception gap lingers. Retailers in pharmaceuticals or luxury goods, where customer data sensitivity runs high, often insist on hybrid deployments, dampening near-term growth for public-cloud configurations within the cloud point of sale market.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel analytics demand

- Regulatory push for e-payments

- Bandwidth reliability in emerging markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The software segment captured 59.40% of the cloud point of sale market share in 2025, underscoring its role as the transaction engine and analytics hub. Recurring upgrades, real-time patches, and remote feature activation create sustained value without hardware refresh. Services, from implementation to managed analytics, are on a 20.95% CAGR climb that will enlarge the cloud point of sale market size for advisory and outsourcing specialists.

Modern suites bundle inventory control, staff scheduling, and CRM within a unified interface, reframing PoS software as the command centre for daily operations. Merchants lacking in-house IT staff turn to service integrators for deployment, custom workflows, and on-call support. As more retailers push omnichannel ambitions, demand for tailored integrations with last-mile delivery networks and ERP systems bolsters the services uptick, further expanding the cloud point of sale market.

Mobile PoS solutions held 57.20% of 2025 revenue, a lead they will likely maintain thanks to a projected 22.84% CAGR through 2031. Retailers deploy tablet or handheld devices on shop floors, at pop-ups, and for curbside pick-ups, proving the flexibility that underpins cloud point of sale market momentum. Fixed terminals remain vital in high-throughput grocery lanes, but many now operate as cloud-linked nodes to harness centralised analytics.

Hardware advances-ruggedised casings, extended battery cycles, and cloud-native OS updates-make mobile units enterprise-grade. Half of surveyed retail executives plan mPOS rollouts to heighten service levels. In hospitality, tableside ordering accelerates meal turns while boosting gratuity rates. Such first-hand ROI evidence elevates mobile devices from a nice-to-have to a core pillar of the cloud point of sale market.

Cloud PoS Market is Segmented by Component (Software, Services), Pos Type (Fixed PoS, Mobile / MPoS), Deployment Model (Public Cloud, Private Cloud, Hybrid Cloud), Organization Size (Small and Medium Enterprises (SMEs), Large Enterprises), End-User Industry (Retail and Consumer Goods, Hospitality and Restaurants, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 34.70% of 2025 sales, fueled by tech-savvy consumers and vendor concentration. U.S. restaurant chains such as those running Toast saw notable performance gains after integrating ordering, payments, and loyalty on a single stack. Clear standards around tokenisation and contactless transactions also fast-tracked platform rollouts, setting a blueprint for the wider cloud point of sale market.

Asia-Pacific is the fastest climber, projected at 19.92% CAGR to 2031. China's Alipay and WeChat Pay ecosystems push merchants toward native integrations, while Japan offsets labour shortages with self-checkout kiosks. India's digitisation incentives for SMEs unlock new footholds for regional vendors, amplifying mPOS use in tier-2 towns. As telecom upgrades narrow bandwidth gaps, cross-border commerce in the region will enlarge the cloud point of sale market size for multilingual, multi-currency suites.

Europe commands mature but regulation-driven demand. Mandates such as Germany's Kassensicherungsverordnung and Austria's RKSV require secure fiscal memory and tamper-proof logs. Many merchants opt for certified cloud stacks that deliver compliance updates remotely, buoying the cloud point of sale market. Latin America, the Middle East, and Africa remain nascent yet promising: improving wireless coverage and government fintech roadmaps should unlock double-digit growth, especially through hybrid offline-first architectures.

- Block, Inc. (Square)

- Shopify Inc.

- Intuit Inc.

- Lightspeed Commerce Inc.

- Clover Network Inc. (Fiserv)

- NCR Voyix Corp.

- Oracle Corp. (Micros)

- Toast Inc.

- PAR Technology Corp.

- Toshiba Global Commerce Solutions

- Verifone, Inc.

- Ingenico (Worldline SA)

- PAX Global Technology Ltd.

- SumUp Payments Ltd.

- Adyen N.V.

- Revel Systems Inc.

- Cegid Group

- HP Inc.

- Dell Technologies Inc.

- NEC Corp.

- Panasonic Corp.

- Samsung Electronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cashless-transaction momentum

- 4.2.2 Mobile-first commerce adoption

- 4.2.3 Omnichannel analytics demand

- 4.2.4 Regulatory push for e-payments

- 4.2.5 AI-driven inventory optimization tools

- 4.2.6 SaaS revenue-share pricing models

- 4.3 Market Restraints

- 4.3.1 Data-security and compliance gaps

- 4.3.2 Bandwidth reliability in emerging markets

- 4.3.3 Fragmented cross-border payment rules

- 4.3.4 Rising cyber-insurance premiums

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By PoS Type

- 5.2.1 Fixed PoS

- 5.2.2 Mobile / mPoS

- 5.3 By Deployment Model

- 5.3.1 Public Cloud

- 5.3.2 Private Cloud

- 5.3.3 Hybrid Cloud

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By End-user Industry

- 5.5.1 Retail and Consumer Goods

- 5.5.2 Hospitality and Restaurants

- 5.5.3 Healthcare

- 5.5.4 Entertainment and Leisure

- 5.5.5 Transportation and Logistics

- 5.5.6 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level overview, Market-level overview, Core segments, Financials as available, Strategic information, Market rank/share, Products and Services, Recent developments)

- 6.4.1 Block, Inc. (Square)

- 6.4.2 Shopify Inc.

- 6.4.3 Intuit Inc.

- 6.4.4 Lightspeed Commerce Inc.

- 6.4.5 Clover Network Inc. (Fiserv)

- 6.4.6 NCR Voyix Corp.

- 6.4.7 Oracle Corp. (Micros)

- 6.4.8 Toast Inc.

- 6.4.9 PAR Technology Corp.

- 6.4.10 Toshiba Global Commerce Solutions

- 6.4.11 Verifone, Inc.

- 6.4.12 Ingenico (Worldline SA)

- 6.4.13 PAX Global Technology Ltd.

- 6.4.14 SumUp Payments Ltd.

- 6.4.15 Adyen N.V.

- 6.4.16 Revel Systems Inc.

- 6.4.17 Cegid Group

- 6.4.18 HP Inc.

- 6.4.19 Dell Technologies Inc.

- 6.4.20 NEC Corp.

- 6.4.21 Panasonic Corp.

- 6.4.22 Samsung Electronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment