|

시장보고서

상품코드

2044259

아시아태평양의 에폭시 접착제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Epoxy Adhesive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

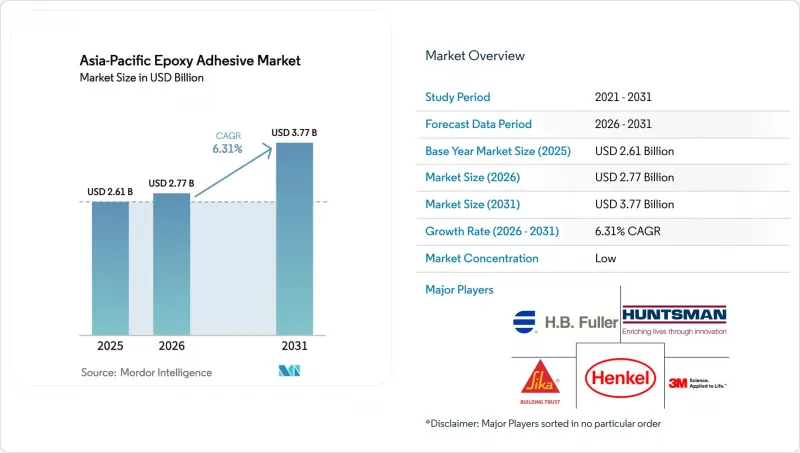

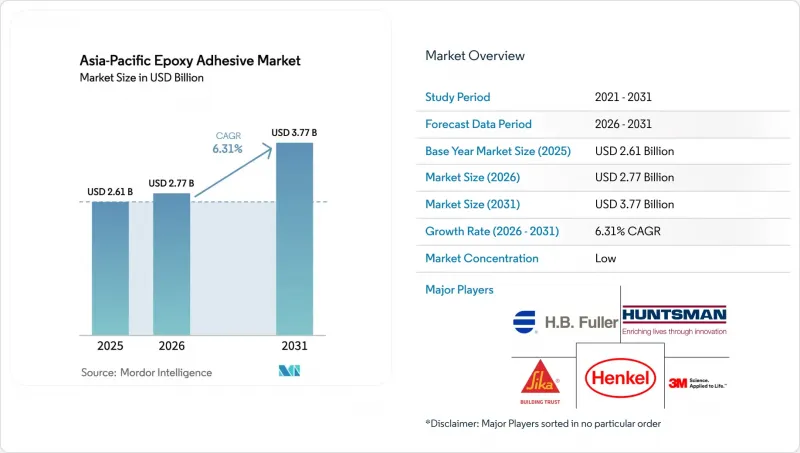

아시아태평양의 에폭시 접착제 시장 규모는 2025년 26억 1,000만 달러에서 2026년에는 27억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 6.31%로 성장을 지속하여, 2031년에는 37억 7,000만 달러에 이를 것으로 예측됩니다.

운송 장비의 꾸준한 전동화, 반도체 패키징에 대한 투자 확대, 사상 최고 수준의 도시 인프라 지출이 결합되어 아시아태평양 전체에서 구조용 접착제에 대한 수요가 증가하고 있으며, 이로 인해 아시아태평양의 에폭시 접착제 시장은 세계 평균을 상회하는 성장을 보일 것으로 예측됩니다. 자동차 제조업체들이 용접 대신 경량 복합재 접착을 채택하는 가운데, 2액형 반응성 제품은 가격 결정력을 계속 유지하고 있습니다. 한편, 엄격한 실내 공기질 규제로 인해 건설 프로젝트에서는 상온에 가까운 온도에서 경화되는 저 VOC 경화제로의 전환이 진행되고 있습니다. 주요 화학업체들은 전기자동차 배터리, 포토닉스 칩렛, 고층 빌딩 파사드 패널용 배합 개발 주기를 단축하기 위해 지역 연구소의 규모를 확대하고 있으며, 이러한 변화로 인해 현지 용도 엔지니어링에 강점을 가진 기업에게 경쟁 우위가 기울어지고 있습니다. 기울어지고 있습니다.

아시아태평양의 에폭시 접착제 시장 동향과 인사이트

급증하는 전기차 및 자동차 경량화 생산량 증가

아시아태평양에서는 전기자동차(EV) 제조 공장에서 배터리 모듈, 셀 투 팩(CTP) 시스템, 알루미늄 복합재 차체 패널 등 다양한 부품에 대한 접착제 솔루션의 채택이 확대되고 있습니다. 이러한 추세는 특히 자동차 제조업체들이 차량 총중량을 15-20% 줄이는 것을 목표로 하고 있기 때문에 이 지역의 에폭시 접착제 시장을 촉진하고 있습니다. BYD, 현대자동차, LG 에너지 솔루션 등 업계 대기업의 대규모 투자가 수 기가 와트시급 배터리용량 확대를 견인하고 있습니다. 이 배터리에는 높은 열전도율과 빠른 초기 강도로 알려진 틈새 충전용 에폭시가 채택되어 있습니다. 또한, 실온에서 최대 6개월까지 보관할 수 있는 새로운 실버 페이스트 에폭시는 실리콘 카바이드 파워 모듈 제조에 혁명을 불러일으키고 있습니다. 이 혁신 기술은 기존의 소결 공정을 생략함으로써 인버터 생산 효율을 높일 뿐만 아니라 에너지 소비를 최대 40%까지 절감할 수 있습니다.

빠른 인프라 구축과 고층 건축

2025년 아시아태평양 각국 정부는 건설 분야에 5조 달러 이상을 투자했습니다. 이러한 도시화의 급격한 확대로 인해 파사드용 유리, 앵커용 그라우트, 보수용 모르타르 등 수요가 증가했는데, 이들 모두 고강도 에폭시 수지에 의존하고 있습니다. 또한, 5℃에서 10℃ 범위에서 경화 가능한 신개발 저온 경화제가 겨울철 콘크리트 타설에 혁명을 일으키고 있습니다. 이 혁신 기술은 중국 북부의 건설 현장과 인도의 고산지대 철도 프로젝트에서 특히 유용하며, 고가의 난방 담요를 사용하지 않아도 됩니다.

비스페놀 A 및 에피클로로히드린 원료의 가격 변동성

장기 수지 계약이 없는 중견 컴파운드 제조업체는 분기별 가격 변동폭이 20%를 초과하여 수익률 압박에 직면해 있습니다. 이러한 제약을 극복하기 위해 동남아시아의 일부 가공업체들은 바이오 에폭시 수지로의 전환을 추진하고 있습니다. 로진이나 카르다놀을 원료로 하는 이들 에폭시 수지는 가격이 30% 정도 비싼 편이며, 230°C 이상의 유리 전이 온도를 자랑합니다.

부문 분석

전자기기 및 반도체 응용 분야는 CAGR 6.58%의 속도로 성장하고 있습니다. 신주쿠와 크림을 포함한 각 지역에 파워 디바이스 및 광모듈 제조 공장이 생겨나면서 이 부문은 자동차 부문을 능가하고 있습니다. 그러나 자동차 부문은 여전히 가장 큰 기여를 하는 분야로 23.18%의 점유율을 차지하고 있습니다. 아시아태평양의 에폭시 접착제 시장은 자동차 차체 구조, 배터리 팩, 파워트레인에 대한 적용을 중심으로 지속적으로 성장하고 있습니다.

고주파 질화갈륨 및 실리콘 카바이드 디바이스 분야는 체적 열전도율이 150 W/m-K를 초과하는 은 충전 에폭시 수지에 대한 수요를 주도하고 있습니다. 이러한 추세에 따라 화학물질 공급업체와 기판 제조업체 간의 연구개발(R&:D) 협력이 강화되고 있습니다. 또한, 건설, 에너지, 선박 부문은 전반적으로 안정적인 수요를 유지하고 있습니다. 인프라에 대한 정부 투자는 교량, 풍력 발전용 블레이드, 선체 개조 등의 프로젝트에 중점을 두고 있으며, 모두 고탄성 접착이 필요한 프로젝트입니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The Asia-Pacific epoxy adhesives market size is expected to grow from USD 2.61 billion in 2025 to USD 2.77 billion in 2026 and is forecast to reach USD 3.77 billion by 2031 at 6.31% CAGR over 2026-2031. Steady electrification of transport, an upturn in semiconductor packaging investments, and record urban infrastructure spending are converging to lift structural bonding demand across the region, allowing the Asia-Pacific epoxy adhesives market to outpace global averages. Two-component reactive systems continue to command pricing power as vehicle makers replace welding with lightweight composite bonding, while stringent indoor-air-quality rules are steering construction projects toward low-VOC hardeners that cure at near-ambient temperatures. Major chemical suppliers are scaling regional laboratories to shorten formulation cycles for electric-vehicle batteries, photonics chiplets, and high-rise facade panels, a shift that tilts competitive advantage toward firms with local application-engineering depth.

Asia-Pacific Epoxy Adhesive Market Trends and Insights

Surging EV And Lightweight Automotive Output

In the Asia-Pacific region, electric vehicle plants are increasingly turning to adhesive solutions for various components, including battery modules, cell-to-pack systems, and aluminum-composite body panels. This trend is bolstering the region's epoxy adhesives market, especially as original-equipment manufacturers aim to reduce curb weight by 15-20%. Major investments from industry giants like BYD, Hyundai, and LG Energy Solution are driving a multi-gigawatt-hour battery capacity. These batteries rely on gap-filling epoxies known for their high thermal conductivity and rapid green strength. Additionally, a newly commercialized silver-paste epoxy, which can be stored at room temperature for up to six months, is revolutionizing the production of silicon-carbide power modules. By eliminating the traditional sintering steps, this innovation not only streamlines inverter production but also reduces energy consumption by as much as 40%.

Rapid Infrastructure And High-Rise Construction

In 2025, governments across the Asia-Pacific region invested over USD 5 trillion in construction. This surge in urbanization heightened the demand for products like facade glazing, anchor grouts, and repair mortars, all of which depend on high-toughness epoxies. Additionally, a newly introduced low-temperature hardener, capable of curing between 5 °C and 10 °C, is revolutionizing winter concreting. This innovation is particularly beneficial for northern China's construction and India's high-altitude rail projects, eliminating the need for expensive heating blankets.

Volatility In Bisphenol A And Epichlorohydrin Feedstocks

Mid-tier mixers, lacking long-term resin contracts, face margin compression due to quarterly price swings exceeding 20%. As a restraint, several processors in Southeast Asia are turning to bio-based epoxies. These epoxies, sourced from rosin and cardanol, boast glass-transition temperatures surpassing 230 °C, albeit at a 30% price premium.

Other drivers and restraints analyzed in the detailed report include:

- Expansion Of Electronics And Semiconductor Assembly

- Anti-Dumping Tariffs Spurring Backward Integration

- Stringent VOC And Indoor-Air-Quality Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electronics and semiconductor applications are expanding at a rate of 6.58% CAGR. This segment is surpassing the automotive sector as fabs for power devices and photonic modules emerge across regions, including Hsinchu and Kulim. The automotive sector, however, remains the largest contributor, holding a 23.18% share. The Asia-Pacific epoxy adhesives market within this segment continues to grow, driven by applications in vehicle structures, battery packs, and powertrains.

The high-frequency gallium-nitride and silicon-carbide devices segment is fueling demand for silver-filled epoxies with bulk thermal conductivity exceeding 150 W/m-K. This trend is strengthening R&D collaborations between chemical suppliers and substrate manufacturers. Additionally, the construction, energy, and marine segments collectively maintain steady demand. Government investments in infrastructure are focusing on projects such as bridges, wind blades, and hull refurbishments, all of which require high-modulus bonding.

The Asia-Pacific Epoxy Adhesives Market Report is Segmented by End-User Industry (Aerospace and Defense, Automotive, Electrical and Electronics, Construction, Other End-User Industries), Technology (Reactive, Solvent-Borne, UV-Cured, Water-Borne), and Geography (Australia, China, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Thailand, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- artience Co., Ltd.

- Avery Dennison Corporation

- BASF

- Dow Inc.

- Dymax Corporation

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hubei Huitian New Materials Co., Ltd.

- Huntsman Corporation

- ITW Performance Polymers

- Jowat SE

- Kangda New Materials (Group) Co., Ltd.

- NANPAO RESINS CHEMICAL GROUP

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in EV and lightweight automotive manufacturing

- 4.2.2 Rapid infrastructure and high-rise construction spending

- 4.2.3 Expansion of electronics and semiconductor assembly

- 4.2.4 Domestic aircraft programs adopt localized qualifications

- 4.2.5 Anti-dumping tariffs spurring backward integration

- 4.3 Market Restraints

- 4.3.1 Volatile BPA and ECH feedstock prices

- 4.3.2 Stringent VOC and IAQ regulations on solvent systems

- 4.3.3 Performance gap and cost premium of water-borne epoxies

- 4.4 Value Chain Analysis

- 4.5 Distribution Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Distribution Channel Analysis

5 Market Size & Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Aerospace and Defense

- 5.1.2 Automotive

- 5.1.3 Marine

- 5.1.4 Electrical and Electronics

- 5.1.5 Construction

- 5.1.6 Energy and Power

- 5.1.7 Other End-User Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-Cured

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 Australia

- 5.3.2 China

- 5.3.3 India

- 5.3.4 Indonesia

- 5.3.5 Japan

- 5.3.6 Malaysia

- 5.3.7 Singapore

- 5.3.8 South Korea

- 5.3.9 Thailand

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 artience Co., Ltd.

- 6.4.4 Avery Dennison Corporation

- 6.4.5 BASF

- 6.4.6 Dow Inc.

- 6.4.7 Dymax Corporation

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hubei Huitian New Materials Co., Ltd.

- 6.4.11 Huntsman Corporation

- 6.4.12 ITW Performance Polymers

- 6.4.13 Jowat SE

- 6.4.14 Kangda New Materials (Group) Co., Ltd.

- 6.4.15 NANPAO RESINS CHEMICAL GROUP

- 6.4.16 Permabond LLC

- 6.4.17 Pidilite Industries Ltd.

- 6.4.18 Sika AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment