|

시장보고서

상품코드

2044261

유럽의 아크릴 접착제 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Europe Acrylic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

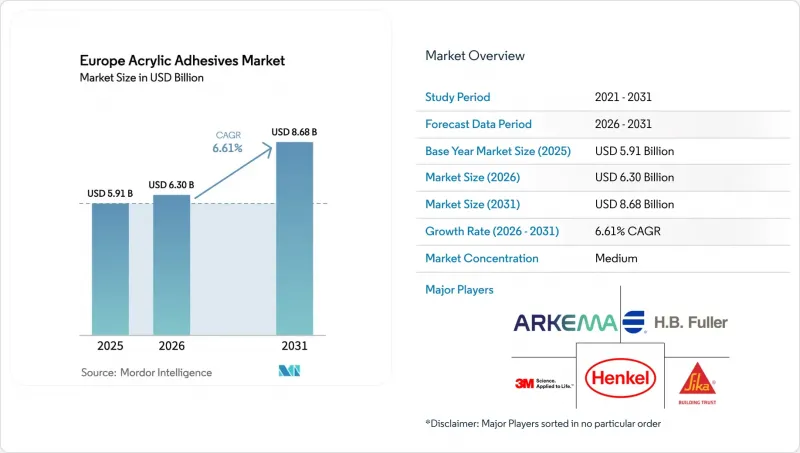

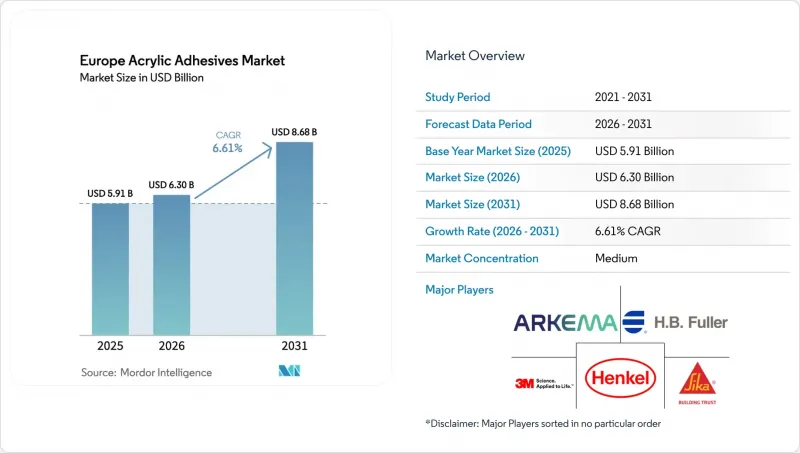

유럽의 아크릴 접착제 시장 규모는 2025년 59억 1,000만 달러에서 2026년에는 63억 달러로 확대되어 2031년까지 86억 8,000만 달러에 이를 것으로 예상되고 있으며 2026-2031년까지 CAGR 6.61%로 성장할 전망입니다.

제품 수요는 전자상거래용 포장, 자동차 경량화, 개조 공사에 대한 인센티브의 혜택을 받고 있으며, 이러한 요소들이 결합되어 판매량을 늘리고 평균 판매 가격을 향상시키고 있습니다. 휘발성 유기화합물(VOC) 기준치를 강화하는 규제 변경으로 인해 저 VOC 수성 화학제품으로의 전환이 가속화되고 있으며, 공급업체들은 규정을 준수하는 모노머와 유화제를 확보하기 위해 공급망을 재구성해야 하는 상황에 처해 있습니다. 메틸 메타크릴레이트, 부틸 아크릴레이트와 같은 원료의 후방 연계성을 가진 통합 제조업체는 원가 우위를 유지하는 반면, 중견 컨버터는 틈새 기판용 맞춤형 배합을 통해 물량을 늘리고 있습니다. 바이어들이 납기 준수와 규제 관련 서류를 확보하기 위해 공급업체 기반을 통합하는 가운데, 제품 포트폴리오의 간소화, 기술 서비스 지원, 신속한 생산 능력 확대는 여전히 결정적인 경쟁 요소로 작용하고 있습니다.

유럽 아크릴 접착제 시장 동향과 인사이트

유럽 연합(EU)의 VOC 규제에 따른 수성 아크릴로의 전환

2025년 말 발표되고 2026년 중반에 발효되는 EU의 VOC 상한선 개정에 따라, 배합 제조업체는 모든 용매 기반 SKU(재고 관리 단위)에 대한 감사를 실시하고, 규정을 준수하는 수성 등급의 파일럿 생산을 가속화하고, 새로운 원료 공급망 인증을 획득해야 합니다. 인증을 획득해야 합니다. 제3자 수명주기 평가(LCA)를 공개한 선행 기업들은 저배출 제품을 더 높게 평가하는 공공 입찰이나 접객 산업 개조 공사에서 우대 점수를 획득하고 있습니다. 에멀젼계 제품은 개방 시간이 길고 유변학적 특성도 변화하기 때문에 시공자에게 재교육이 필요하지만, 무취에 가까운 특성으로 실내공기 재사용까지의 대기시간을 단축할 수 있습니다. 포장 제조업체들은 이미 생산성과 규제 준수라는 두 가지 목표를 모두 충족하는 하이브리드 아크릴 UV 에멀젼 화학 성분을 검사하고 있습니다. 전반적으로, 이 법규의 추진으로 유럽 아크릴 접착제 시장 예측 CAGR은 1.8 포인트 상승할 것으로 예측됩니다.

전자상거래 포장의 급격한 성장이 PSA 수요를 견인합니다.

온라인 소매로의 전환은 골판지, 폴리에틸렌, 금속 증착 기판에서 일관된 접착력을 발휘하는 감압성 아크릴 에멀젼을 필요로 하는 골판지 라벨, 연질 필름, 재밀봉 가능한 파우치에 대한 수요를 증가시키고 있습니다. RFID 태그 및 스마트 라벨용 센서에서는 다온도 영역의 물류 사이클을 통해 안정성을 유지하는 저전이성 아크릴이 점점 더 많이 지정되고 있습니다. 브랜드 소유자는 EU의 순환 경제 지침에 따라 섬유 간 재활용을 촉진하고 탈묵 공정을 줄이는 수성 등급을 선호합니다. 유럽의 컨버터는 차세대 에멀젼 PSA로 전환한 후 라인 속도가 최대 12% 향상되었으며, 이는 유럽 아크릴 접착제 시장의 전체 성장률을 1.5% 끌어올리는 요인이 되었다고 보고하고 있습니다.

아크릴 모노머 가격 변동

크래커의 정기보수 및 아세톤 현물시장에서공급 부족은 과거 메틸 메타크릴레이트 가격의 분기별 두 자릿수 변동폭을 유발한 바 있습니다. 2025년 하반기 공급과잉으로 인해 시장은 안정세를 보였으나, 구매자들은 여전히 경계심을 갖고 있으며, 배합 기반 계약과 완전 통합 공급업체로부터의 이중 소싱으로 전환하고 있습니다. 원료 가격의 ±10% 변동은 배합 제조업체의 이윤율을 압박하고 재량 투자를 지연시켜 단기적으로 유럽 아크릴 접착제 시장의 성장 잠재력을 0.8% 낮추었습니다.

부문 분석

2025년, 포장 부문은 유럽 아크릴 접착제 시장 점유율의 59.56%를 차지했습니다. 이는 소포 취급량 증가와 사상 최고 가동률로 가동 중인 연질 필름 라미네이팅 라인에 힘입은 결과입니다. 브랜드 소유자가 고투명 아크릴 에멀젼에 의존하는 단일 재료 구조로 전환함에 따라 이 부문은 2031년까지 선두를 유지할 것으로 예측됩니다. 2024년 말 Arkema가 Dow의 연포장용 접착제 사업을 인수함에 따라 Bostik의 유럽 사업 기반이 즉시 확장되고 고기능성 수지에 대한 후방 통합이 보장되었습니다. 의료용 포장 및 의약품 블리스터 라벨은 기본 수요를 더욱 뒷받침하고 있으며, 예측 기간 동안 유럽 아크릴 접착제 시장의 포장 부문 규모는 꾸준히 확대될 것으로 예측됩니다.

자동차 부문은 시장 규모 비중은 작지만 배터리 모듈 조립, 경량화, 경량화, 전기화에 대한 투자를 배경으로 CAGR 6.72%로 가장 빠르게 성장할 것으로 예측됩니다. 차량 플랫폼에서는 항속거리를 늘리기 위해 적극적인 경량화가 진행되고 있으며, OEM(자동차 제조업체)은 열팽창 차이를 견딜 수 있는 혼합 금속 접합부에 아크릴 테이프의 채택을 검증하고 있습니다. 독일 자동차 제조업체가 체결한 전략적 조달 계약은 다년간의 생산 능력을 확보하여 모빌리티 밸류체인에서 유럽 아크릴 접착제 시장의 명확한 성장 경로를 만들어냈습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Europe Acrylic Adhesives Market size is expected to increase from USD 5.91 billion in 2025 to USD 6.30 billion in 2026 and reach USD 8.68 billion by 2031, growing at a CAGR of 6.61% over 2026-2031. Product demand benefits from e-commerce packaging, vehicle lightweighting, and retrofit construction incentives that collectively lift volumes and improve average selling prices. Regulatory changes that tighten volatile-organic-compound (VOC) thresholds accelerate the switch to low-VOC water-borne chemistries, prompting suppliers to re-engineer supply chains for compliant monomers and emulsifiers. Integrated producers with backward linkages into methyl-methacrylate and butyl-acrylate feedstocks retain a cost edge, while mid-tier converters win volume with tailored formulations for niche substrates. Portfolio rationalization, technical-service support, and rapid scale-up capacity remain decisive competitive factors as buyers consolidate supplier bases to secure on-time deliveries and regulatory documentation.

Europe Acrylic Adhesives Market Trends and Insights

Shift Toward Water-Borne Acrylics Under European Union VOC Limits

Revised EU VOC ceilings, announced late 2025 and effective mid-2026, compel formulators to audit every solvent-borne stock-keeping unit, accelerate pilot runs of compliant water-borne grades, and certify new raw-material supply chains. Early movers that publish third-party life-cycle assessments secure preferential scores in public tenders and hospitality refurbishments that weight low-emission products higher. Installers need retraining because emulsion systems exhibit longer open time and altered rheology, yet their near-zero odor profile reduces indoor-air re-occupancy delays. Packaging groups have already trialed hybrid acrylic UV-emulsion chemistries that meet both productivity and compliance targets. Collectively, the legislative push adds a visible 1.8 percentage-point uplift to the forecast CAGR of the Europe Acrylic Adhesives market.

E-Commerce Packaging Boom Driving PSA Demand

Online retail migration propels demand for corrugated labels, flexible films, and resealable pouches that rely on pressure-sensitive acrylic emulsions for consistent tack across cardboard, polyethylene, and metallized substrates. RFID tags and smart-label sensors increasingly specify low-migration acrylics that remain stable through multi-temperature logistics cycles. Brand owners favor water-borne grades that facilitate fiber-to-fiber recycling and reduce de-inking steps, aligning with EU circular-economy directives. European converters report line-speed gains of up to 12% after switching to next-generation emulsion PSAs, supporting a 1.5 percentage-point boost to overall growth in the Europe Acrylic Adhesives market.

Acrylic-Monomer Price Volatility

Scheduled cracker turnarounds and spot acetone tightness have historically triggered double-digit quarterly swings in methyl-methacrylate pricing. Although late-2025 oversupply cooled quotations, buyers remain wary and shift toward formula-based contracts or dual sourcing from fully integrated suppliers. Feedstock swings of +-10% compress formulators' margins, delaying discretionary investments and shaving 0.8 percentage-points off the Europe acrylic adhesives market growth potential in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting and Mixed-Material Bonding

- EU Renovation Wave Spurring Facade-Insulation Adhesives

- VOC-Compliance Costs for Solvent Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packaging accounted for 59.56% of the Europe Acrylic Adhesives market share in 2025, supported by escalating parcel volumes and flexible-film lamination lines running at record utilization. The segment is expected to retain leadership through 2031 as brand owners migrate to mono-material structures that rely on high-clarity acrylic emulsions. Arkema's late-2024 acquisition of Dow's flexible-packaging adhesive assets immediately lifted Bostik's European footprint and secured backward integration into performance resins. Medical packaging and pharmaceutical blister labels further reinforce baseline demand, ensuring the Europe Acrylic Adhesives market size for packaging expands steadily across the forecast years.

Automotive, while contributing a smaller base, is forecast to grow fastest at 6.72% CAGR on the back of battery module assembly, lightweight body-in-white bonding, and electromobility investments. Vehicle platforms aggressively cut weight to extend driving range, and OEMs (Original Equipment Manufacturers) validate acrylic tapes for mixed-metal joints that tolerate differential thermal expansion. Strategic sourcing arrangements signed by German automakers secure multi-year capacity reservations, creating a visible growth pipeline for the Europe acrylic adhesives market within the mobility value chain.

The Europe Acrylic Adhesives Market Report is Segmented by End-User Industry (Aerospace, Automotive, Building and Construction, Footwear and Leather, Healthcare, Packaging, and More), Technology (Reactive, Solvent-Borne, UV-Cured Adhesives, and Water-Borne), and Country (Australia, China, India, Indonesia, Malaysia, Singapore, South Korea, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corporation

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- MAPEI S.p.A.

- Sika AG

- Soudal Holding N.V.

- BASF

- Dymax Corporation

- ITW Performance Polymers

- PARKER HANNIFIN CORP

- Lohmann

- Hoenle AG

- Parson Adhesives, Inc.

- Novatech International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift toward water-borne acrylics under European Union VOC limits

- 4.2.2 E-commerce packaging boom driving PSA demand

- 4.2.3 Automotive lightweighting and mixed-material bonding

- 4.2.4 European Union "Renovation Wave" spurring facade-insulation adhesives

- 4.2.5 Wind-turbine blade refurbishment using structural acrylics

- 4.3 Market Restraints

- 4.3.1 Acrylic-monomer price volatility

- 4.3.2 VOC-compliance costs for solvent systems

- 4.3.3 Bio-based polyurethane dispersions cannibalising share

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Distribution Channel Analysis

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-user Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Footwear and Leather

- 5.1.5 Healthcare

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 By Technology

- 5.2.1 Reactive

- 5.2.2 Solvent-borne

- 5.2.3 UV-cured

- 5.2.4 Water-borne

- 5.3 By Country

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Huntsman International LLC

- 6.4.8 MAPEI S.p.A.

- 6.4.9 Sika AG

- 6.4.10 Soudal Holding N.V.

- 6.4.11 BASF

- 6.4.12 Dymax Corporation

- 6.4.13 ITW Performance Polymers

- 6.4.14 PARKER HANNIFIN CORP

- 6.4.15 Lohmann

- 6.4.16 Hoenle AG

- 6.4.17 Parson Adhesives, Inc.

- 6.4.18 Novatech International

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment