|

시장보고서

상품코드

2044274

북미의 데이터센터 건설 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

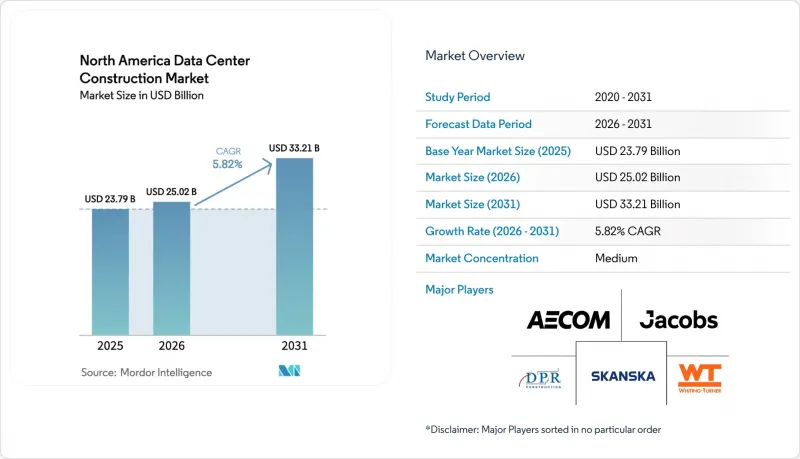

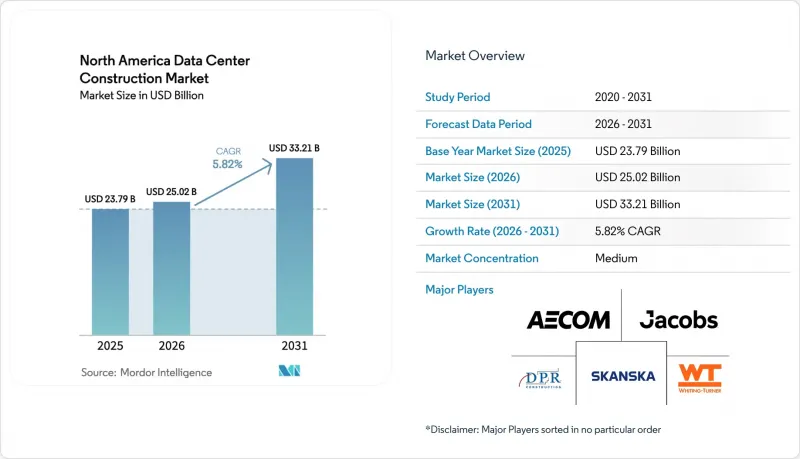

북미의 데이터센터 건설 시장 규모는 2025년에 237억 9,000만 달러, 2026년에 250억 2,000만 달러되어, 2031년까지 332억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 5.82%로 성장할 전망입니다.

클라우드 및 생성형 AI 워크로드 증가는 100kW 이상의 랙 밀도를 지원할 수 있는 하이퍼스케일 지원 캠퍼스에 대한 투자를 촉진하고 있습니다. 한편, 풍력 및 태양광 자원에 대한 근접성은 라이프사이클의 전력비용을 절감하고, 넷제로(Net Zero) 약속에도 부합합니다. 현재 변압기 리드타임이 2년이나 걸리면서 조기 조달 전략이 요구되고 있으며, 건설업체들은 숙련공 부족을 보완하기 위해 조립식 전기 및 냉각 모듈로 눈을 돌리고 있습니다. 경쟁 우위는 특히 대기 기간이 이미 18개월을 넘어선 버지니아, 텍사스, 애리조나 주에서 계통연계 대기자 명단보다 먼저 전력망에 접속할 수 있느냐에 달려있습니다. 지속가능성에 대한 규제 요건도 입지 선정에 변화를 가져오고 있으며, 기존 송전선로와 즉시 체결 가능한 재생에너지 전력구매계약(PPA)을 결합할 수 있기 때문에 폐지된 석탄화력발전소 부지가 선호되고 있습니다.

북미 데이터센터 건설 시장 동향 및 인사이트

클라우드 애플리케이션, AI, 빅데이터 보급 확대

16,000개 이상의 엔비디아 H100 GPU가 탑재된 트레이닝 클러스터는 현재 랙당 20-100kW의 전력을 소비하고 있으며, 이는 기존 기업용 데이터센터에서 볼 수 있는 5-10kW를 크게 상회하는 수준입니다. 마이크로소프트의 1,000억 달러 규모의 '스타게이트(Stargate)' 프로젝트는 부지 내에 변전소를 갖추고 칩 수준에서 서버 열의 80%를 제거할 수 있는 액체 냉각 시스템을 갖춘 전용 캠퍼스로의 전환을 강조합니다. 코로케이션 시설 소유주들은 고밀도화를 위한 리노베이션을 진행하고 있지만, 많은 Tier 3 쉘(미완성 데이터센터 시설)은 추가 바닥 하중을 감당할 수 없어 전력 공급이 풍부한 지역에 신규 건설이 촉진되고 있습니다. AI 중심의 성장은 설계 기준도 바꾸고 있으며, 이중화된 중전압 전원 공급 장치와 800V DC 백본을 우선시하고 있습니다. 그 결과, 건설비용이 구조적으로 증가하여 북미 데이터센터 건설 시장은 향후 몇 년 동안 지속적으로 확대될 것으로 예측됩니다.

하이퍼스케일 데이터센터 구축 확대

컴퍼스 데이터센터, 센터스퀘어, 파워하우스는 2026년까지 총 4.8GW 이상의 계획 용량을 발표했습니다. 이는 토지 임베디드부터 시운전까지 전 과정에서 자급자족을 보장하는 수 기가 와트 규모의 캠퍼스에 베팅한 것입니다. 이들 사업자들은 미국 에너지부가 지적한 공급망 병목현상을 피하기 위해 대형 변압기를 2년 전에 앞당겨 발주하고 있습니다. 부지조성, MEP(기계, 전기, 배관) 공사, 설비 설치를 단일 계약으로 통합하는 프로젝트 딜리버리 방식으로 공사기간을 최대 12개월 단축하고 있습니다. 또한, 하이퍼스케일러의 진출은 같은 지역에 광섬유 사업자와 재생에너지 개발업체를 유치하여 장기적인 수요를 강화하는 지역 생태계를 활성화하고 있습니다. 이러한 자본 집약적 특성이 북미 데이터센터 건설 시장의 주요 원동력이 되고 있습니다.

치솟는 전력 및 부동산 비용

라우돈 카운티의 우량 토지는 2025년 에이커당 100만 달러를 돌파할 것으로 예상되며, ERCOT의 도매 전력 가격은 평균 8.2센트/kWh로 전년 대비 34% 상승했습니다. PJM의 계통연계 대기자 명단은 현재 200GW를 넘어섰으며, 개발자들은 최대 36개월을 기다려야 하는 상황입니다. 보유비용 상승으로 인해 2024년 이전에 체결된 고정가격 임대계약에 묶여 있는 코로케이션 사업의 수익률이 압박을 받고 있습니다. 많은 건설업체들이 2차 시장으로 이동하고 있지만, 이들 지역에서는 광섬유 회선의 밀도가 낮은 경우가 많아 토지 및 전력 비용 절감분을 상쇄하는 경우가 많습니다. 이러한 단기적 압박은 본래 견조했던 북미 데이터센터 건설 시장의 성장 전망을 둔화시키고 있습니다.

부문 분석

금융 서비스 및 클라우드 대기업들이 99.995%의 가용성을 요구하는 가운데, Tier 4는 예측 기간 동안 CAGR 6.42%를 나타낼 것으로 예측됩니다. 한편, Tier 3는 2025년에도 북미 데이터센터 구축 시장 점유율의 41.64%를 차지하며, EC 및 SaaS 테넌트를 위한 가동시간과 예산의 균형을 유지하며 여전히 선도적인 지위를 유지할 것으로 보입니다. 리튬 이온 UPS 모듈은 설치 면적을 40% 감소시켜 Tier 3 사업자가 평방피트당 더 많은 수익 랙을 확보할 수 있게 해줍니다. 한편, Tier 4 프로젝트는 회전식 UPS와 이중 전원 공급 장치를 채택하여 토지 요구 사항을 증가시켜 Tier 3과의 비용 차이를 줄입니다. 더 높은 계층으로의 전환은 프로젝트의 평균 가치를 높이는 기술적 복잡성을 수반하며, 계약업체가 진입할 수 있는 북미 데이터센터 건설 시장 규모를 확대할 것입니다.

예측 기간 동안 은행 및 의료 분야의 컴플라이언스 규제로 인해 Tier 4의 성장률은 전체 시장의 CAGR을 계속 상회할 것이며, 지연에 민감한 서비스를 위한 엣지 지향적인 Tier 1-2 사이트가 계속 존재할 것입니다. 지속적인 구성 변경으로 인해 발전기, ATS(자동 전송 스위치), 배전반 공급업체들은 여러 중복화 체계에 대응하는 제품 라인의 확장을 요구받고 있습니다. 그 결과, 북미 데이터센터 건설 업계는 내결함성(fault tolerant) 신규 건설부터 모듈형 Tier 2 엣지 포드에 이르기까지 서비스 스택을 다양화할 준비가 되어 있습니다.

2025년에는 10-50MW 규모의 대형 시설이 54.43%의 점유율을 차지했지만, 100MW 이상 사이트는 CAGR 6.76%로 확대되고 있습니다. 단일 하이퍼스케일 캠퍼스는 200에이커의 면적을 차지하며, 카운티의 구역 설정 패턴을 변경하고 변압기 공급을 3년 동안 확보해야 하는 독립적인 변전소를 필요로 합니다. 이러한 메가 프로젝트를 대상으로 한 북미 데이터센터 건설 시장 규모는 기존의 기업 예산을 훨씬 상회하며, 세계 EPC 컨소시엄을 끌어들이고 있습니다. 그러나 특히 도심의 부동산 사정으로 인해 확장이 제한되는 지역에서는 5G 엣지 및 재해복구 역할을 담당하는 소규모(5MW 미만) 시설의 건설이 여전히 필수적입니다.

하이퍼스케일의 성장에 따라 사업자들이 디젤 대안을 모색하는 가운데, 용융염과 수소 대응 백업 시스템이 주목받고 있습니다. 동시에 모듈형 공급업체들은 10MW까지 쌓을 수 있는 2MW 블록을 표준화하고 있으며, 이를 통해 중견기업도 대규모 토지를 구매하지 않고도 경쟁할 수 있도록 하고 있습니다. 이러한 양극화된 수요 패턴은 북미 데이터센터 건설 시장 전체에 균형 잡힌 비즈니스 기회를 보장하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.11The North America data center construction market size is projected to be USD 23.79 billion in 2025, USD 25.02 billion in 2026, and reach USD 33.21 billion by 2031, growing at a CAGR of 5.82% from 2026 to 2031.

Rising cloud and generative-AI workloads are steering capital toward hyperscale-ready campuses that can support 100+ kW rack densities, while proximity to wind and solar resources lowers lifecycle power costs and aligns with net-zero pledges. Transformer lead times that now stretch to two years are prompting early procurement strategies, and contractors are turning to prefabricated electrical and cooling modules to offset skilled-labor shortages. Competitive advantage hinges on locking in grid access ahead of interconnection queues, especially in Virginia, Texas, and Arizona, where wait times already exceed 18 months. Sustainability mandates are further reshaping site selection, with decommissioned coal sites gaining favor because they pair existing transmission lines with ready-to-sign renewable power purchase agreements.

North America Data Center Construction Market Trends and Insights

Growing Cloud Applications, AI and Big Data Adoption

Training clusters that embed 16,000-plus Nvidia H100 GPUs now draw 20-100 kW per rack, vastly outstripping the 5-10 kW seen in legacy enterprise rooms. Microsoft's USD 100 billion Stargate project underscores a swing toward purpose-built campuses with on-site substations and liquid cooling that removes 80% of server heat at the chip. Colocation landlords are retrofitting for higher densities, yet many Tier 3 shells cannot accommodate the additional floor loading, spurring greenfield builds in power-rich regions. AI-centric growth also shifts design norms, prioritizing redundant medium-voltage feeds and 800-V DC backbones. The net result is a structural uplift in construction spending that keeps the North America data center construction market on a multi-year expansion path.

Rising Hyperscale Data Center Roll-Outs

Compass Datacenters, Centersquare, and PowerHouse collectively unveiled more than 4.8 GW of planned capacity in 2026, banking on multi-gigawatt campuses that ensure self-sufficiency from land purchase through commissioning. These operators are pre-ordering large transformers two years ahead to dodge supply chain bottlenecks flagged by the U.S. Department of Energy. Integrated project delivery combining site prep, MEP build, and equipment installation under one contract is trimming schedules by up to 12 months. Hyperscaler presence also pulls fiber and renewable developers into the same zip codes, catalyzing local ecosystems that reinforce long-term demand. Such capital intensity is a key driver of the North America data center construction market.

Escalating Power and Real-Estate Costs

Prime land in Loudoun County surpassed USD 1 million per acre in 2025 while wholesale power prices in ERCOT averaged 8.2 ¢/kWh, up 34% year-over-year. Lengthy PJM interconnection queues now top 200 GW, forcing developers to wait as long as 36 months before tapping the grid. Higher carrying costs erode colocation margins locked into fixed-price leases inked before 2024. Many builders are shifting toward secondary markets, but these areas often lack dense fiber routes, offsetting the savings in land and electricity. The near-term squeeze tempers the otherwise solid growth profile of the North America data center construction market.

Other drivers and restraints analyzed in the detailed report include:

- Edge-Computing Demand Near 5G Hubs

- Corporate Sustainability and Net-Zero Mandates

- Skilled Electrical and Mechanical Labor Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tier 4 is expected to grow at a CAGR of 6.42% during the forecast period, as financial services and cloud giants demanded 99.995% availability. Tier 3 still led in 2025 with 41.64% of the North America data center construction market share, balancing uptime and budget for e-commerce and SaaS tenants. Lithium-ion UPS modules now cut footprint 40%, letting Tier 3 operators squeeze more revenue racks per square foot. Tier 4 projects, meanwhile, adopt rotary UPS and dual utility feeds, which increase land requirements but narrow the cost premium over Tier 3. The move toward higher tiers injects engineering complexity that raises average project value, expanding the North America data center construction market pool available to contractors.

Across the forecast horizon, banking and healthcare compliance rules will keep Tier 4 growth above the headline CAGR, while edge-oriented Tier 1-2 sites persist for latency-sensitive services. The ongoing mix shift encourages vendors of generators, ATS, and switchgear to broaden product lines for multiple redundancy schemes. Consequently, the North America data center construction industry is poised to diversify its service stack, from fault-tolerant new builds to modular Tier 2 edge pods.

Large facilities between 10 and 50 MW secured 54.43% share in 2025; however, sites exceeding 100 MW are scaling at a 6.76% CAGR. A single hyperscale campus can absorb 200 acres, altering county zoning patterns and requiring separate substations that lock up three years of transformer supply. The North America data center construction market size for these mega-projects dwarfs traditional enterprise budgets, attracting global EPC consortia. Yet small (sub-5 MW) builds remain vital for 5G edge and disaster-recovery roles, especially where urban real estate limits expansion.

Hyperscale growth is spurring molten-salt and hydrogen-ready backup systems as operators hunt for diesel alternatives. Simultaneously, modular suppliers are standardizing 2-MW blocks that stack to 10 MW, allowing medium-size entrants to compete without buying vast tracts of land. This bimodal demand pattern ensures balanced opportunity across the North America data center construction market.

The North America Data Center Construction Market Report is Segmented by Tier Type (Tier 1, Tier 2, Tier 3, and Tier 4), Data Center Type (Colocation, Hyperscalers/Cloud Service Providers, and Enterprise and Edge Data Center), Infrastructure (Electrical Infrastructure, General Construction, and More), Data Center Size (Small, Medium, Large, and Hyperscale), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- AECOM

- Whiting-Turner Contracting Company

- Turner Construction Company

- Jacobs Solutions Inc.

- DPR Construction Inc.

- Skanska USA

- Balfour Beatty US

- Hensel Phelps

- McCarthy Building Companies Inc.

- Gilbane Building Company

- Brasfield and Gorrie LLC

- Holder Construction

- Mortenson Construction

- Fluor Corporation

- Clark Construction Group

- Walsh Construction

- JE Dunn Construction

- Webcor Builders

- Kiewit Corporation

- Layton Construction

- Compass Datacenters

- STACK Infrastructure

- Digital Realty

- Equinix Inc.

- CyrusOne Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Growing Cloud Applications, AI and Big Data Adoption

- 4.3.2 Rising Hyperscale Data Center Roll-Outs

- 4.3.3 Edge-Computing Demand Near 5G Hubs

- 4.3.4 Corporate Sustainability and Net-Zero Mandates

- 4.3.5 Surplus Grid Capacity in Decommissioned Coal Plant Sites

- 4.3.6 AI-Specific GPU Supply-Chain Clustering Near US Gulf Ports

- 4.4 Market Restraints

- 4.4.1 Escalating Power and Real-Estate Costs

- 4.4.2 Skilled Electrical and Mechanical Labor Shortage

- 4.4.3 Multi-Year Lead Times for Large Power Transformers

- 4.4.4 Community Opposition to High-Water-Use Cooling Systems in Arid States

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Key Data Center Statistics

- 4.9.1 Exhaustive Data Center Operators in North America (in MW)

- 4.9.2 List of Major Upcoming Data Center Projects in North America

- 4.9.3 CAPEX and OPEX For North America Data Center Construction

- 4.9.4 Data Center Power Capacity Absorption In MW, North America, 2023 and 2024

- 4.10 Artificial Intelligence (AI) Inclusion in Data Center Construction in North America

- 4.11 Regulatory and Compliance Framework

- 4.12 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Tier Type

- 5.1.1 Tier 1 and 2

- 5.1.2 Tier 3

- 5.1.3 Tier 4

- 5.2 By Data Center Size

- 5.2.1 Small

- 5.2.2 Medium

- 5.2.3 Large

- 5.2.4 Hyperscale

- 5.3 By Data Center Type

- 5.3.1 Colocation Data Center

- 5.3.2 Hyperscalers/Cloud Service Provider (CSPs)

- 5.3.3 Enterprise and Edge Data Center

- 5.4 By Infrastructure

- 5.4.1 Electrical Infrastructure

- 5.4.1.1 Power Distribution Solution

- 5.4.1.2 Power Backup Solutions

- 5.4.2 Mechanical Infrastructure

- 5.4.2.1 Cooling Systems

- 5.4.2.2 Racks and Cabinets

- 5.4.2.3 Servers and Storage

- 5.4.2.4 Other Mechanical Infrastructure

- 5.4.3 General Construction

- 5.4.4 Services - Design and Consulting, Integration, Support and Maintenance

- 5.4.1 Electrical Infrastructure

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Data Center Infrastructure Investment Based on Megawatt (MW) Capacity, 2024 vs 2030

- 6.5 Data Center Construction Landscape (Key Vendors Listings)

- 6.6 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, Recent Developments)

- 6.6.1 AECOM

- 6.6.2 Whiting-Turner Contracting Company

- 6.6.3 Turner Construction Company

- 6.6.4 Jacobs Solutions Inc.

- 6.6.5 DPR Construction Inc.

- 6.6.6 Skanska USA

- 6.6.7 Balfour Beatty US

- 6.6.8 Hensel Phelps

- 6.6.9 McCarthy Building Companies Inc.

- 6.6.10 Gilbane Building Company

- 6.6.11 Brasfield and Gorrie LLC

- 6.6.12 Holder Construction

- 6.6.13 Mortenson Construction

- 6.6.14 Fluor Corporation

- 6.6.15 Clark Construction Group

- 6.6.16 Walsh Construction

- 6.6.17 JE Dunn Construction

- 6.6.18 Webcor Builders

- 6.6.19 Kiewit Corporation

- 6.6.20 Layton Construction

- 6.6.21 Compass Datacenters

- 6.6.22 STACK Infrastructure

- 6.6.23 Digital Realty

- 6.6.24 Equinix Inc.

- 6.6.25 CyrusOne Inc.

- 6.7 List of Data Center Construction Companies

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment