|

시장보고서

상품코드

2073350

인도네시아의 데이터센터 건설 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Indonesia Data Center Construction - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

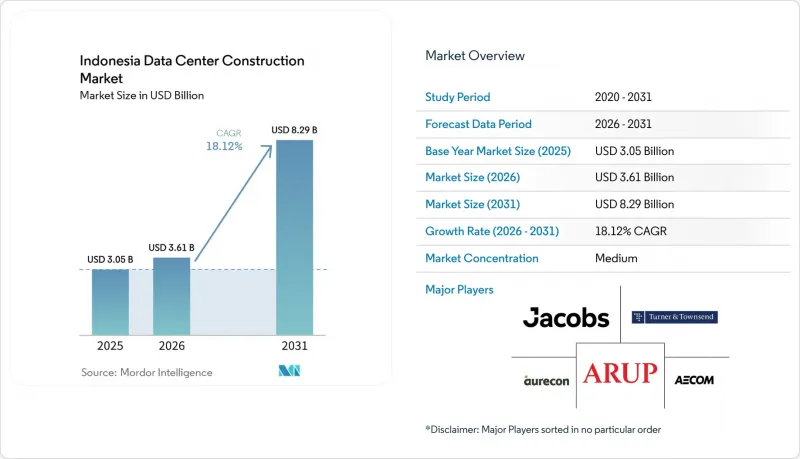

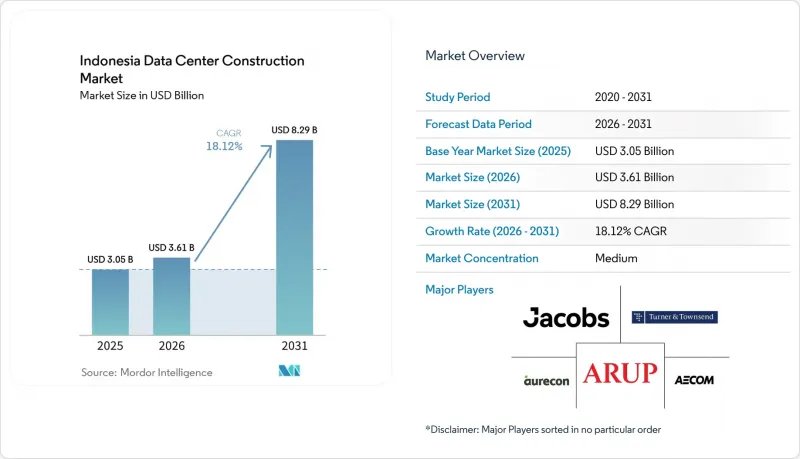

Mordor Intelligence에 의하면, 2026년 인도네시아의 데이터센터 건설 시장 규모는 36억 1,000만 달러에 달할 것으로 예상되고, 2025년 30억 5,000만 달러에서 확대해, 2031년에는 82억 9,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 18.12%를 나타낼 것으로 전망됩니다.

본 보고서는 티어 유형(Tier 1 및 2, Tier 3 및 Tier 4), 데이터센터 유형(코로케이션, 하이퍼스케일러(CSP) 자체 구축, 엔터프라이즈, 엣지), 인프라(전기 인프라, 기계 인프라)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

인도네시아의 데이터센터 건설 시장 동향 및 인사이트

클라우드 및 AI 주도형 하이퍼스케일 투자가 시설 수요를 가속화

하이퍼스케일 클라우드 기업들은 액체 냉각, 40-60kW급 랙, 그리고 캠퍼스당 50MW를 초과하는 연속적인 전력 블록이 필요한 AI 워크로드를 도입함으로써 인도네시아의 데이터센터 건설 시장을 재정의하고 있습니다. 텐센트의 5억 달러 투자, 엔비디아와 인도샛 오레두 허치슨이 공동으로 추진하는 2억 달러 규모의 GPU 센터, BDx의 500MW 재생에너지를 활용한 AI 캠퍼스 등은 인도네시아로 유입되는 자본의 규모를 여실히 보여주고 있습니다. AI에 최적화된 데이터센터는 하이퍼스케일 시설 전반에 걸쳐 고밀도 인프라 및 첨단 냉각 기술에 대한 수요를 높이고 있습니다. 침지 냉각 및 고밀도 전기 배스에 대한 수요가 증가함에 따라 현지 계약업체의 역량 한계에 다다르고 있어, 전 세계 엔지니어링 기업들이 국내 전문가들과 공동 팀을 구성하는 움직임이 나타나고 있습니다. 토지 소유자가 사전 승인을 받은 허가증이나 완공된 변전소를 제공하게 됨에 따라, 건설 일정은 2022년 평균 22개월에서 2025년에는 16-18개월로 단축되었습니다.

‘국립 디지털 인도네시아 로드맵 2030’이 공공 부문의 IT 부담을 가중시킵니다.

이 로드맵에서는 각 부처의 IT 워크로드를 4개의 국가 데이터센터(PDN)로 통합하도록 의무화하고 있습니다. 1억 6,468만 유로(1억 8,959만 달러)가 투입되는 주력 프로젝트인 치카란 PDN은 2만 5,000개의 프로세서 코어를 제공하며, 2024년 8월에 가동을 시작했습니다. 바탐과 누산타라에 3곳의 PDN 부지가 계획되어 있으며, 향후 5년 동안 Tier 4 규격 시설에 대한 안정적인 수요가 예상됩니다. 대통령령 제82/2023호에 따라 각 기관은 레거시 시설에서 이전해야 할 의무가 있으며, 이에 따라 보안 클라우드 구역, 제로 트러스트 네트워크, 사이버 복원력이 뛰어난 플랜트실에 관한 설계 및 건설 계약이 급증하고 있습니다. 이러한 확대는 2024년 5월에 시작된 공공 서비스의 새로운 원스톱 창구인 ‘“INA DIGITAL”의 출범도 뒷받침하고 있으며, 이 서비스 덕분에 부처 간 대역폭 요구량은 이전 예측치를 훨씬 웃도는 수준에 이르렀습니다.

전력 사용량 증가와 탄소세 부담

인도네시아의 탄소세 제도는 2022년에 시행되었으며, 각 부문의 상한선을 초과하는 배출량에 대해 과세가 이루어지고 있습니다. PLN의 발전 구성에서 석탄이 여전히 67%를 차지하고 있기 때문에 대규모 캠퍼스의 경우 재생에너지 전력구매계약(PPA)을 체결하거나 부지 내 태양광 발전 시설을 확보하지 않는 한, 상당한 비용 초과 위험에 직면하게 됩니다. 2060년까지 탄소중립을 달성하기 위한 PLN의 로드맵은 미래의 가격 불확실성을 가중시키고 있으며, 사업자들은 실시간 전력 모니터링, 폐열 재활용 및 수요 반응 프로그램의 도입이 요구되고 있습니다. EDGE2와 같은 선구적인 사업자들은 이미 탄소 중립에 드는 비용을 임차인에게 전가하고 있으며, 프리미엄 가격 책정의 선례를 만들고 있습니다.

부문별 분석

Tier 3 시설은 인도네시아의 데이터센터 건설 시장 규모의 50.62%를 차지하고 있으며, 이는 비용과 가용성 간의 균형이 잘 잡혀 있음을 반영합니다. NeutraDC와 같은 코로케이션 제공업체들은 Tier 3 인증을 활용하여, 99.982%의 가동률을 요구하면서도 설비 투자 제약을 고려하는 기업 임차인을 유치하기 위해 노력하고 있습니다. Tier 1 및 Tier 2 시설은 적절한 중복성을 갖추고, 허용 가능한 지연 시간에 민감한 에지 노드를 대상으로 계속해서 서비스를 제공합니다.

연평균 성장률(CAGR) 18.6%로 성장하고 있는 티어 4 시설은 AI 워크로드와 주권 클라우드 의무화로 인해 가동 중단에 대한 허용 범위가 제로가 되는 가운데, 인도네시아의 데이터센터 건설 시장의 양상을 완전히 바꿔놓고 있습니다. 자카르타 중심부에 위치한 DCI Indonesia의 Tier IV 엣지 시설은 제로 폴트 아키텍처로의 전환을 보여주는 것으로, 침지 냉각 및 구획화된 전원 경로의 도입으로 인해 프로젝트 비용은 Tier 3보다 25-30% 더 높습니다. STT GDC가 발표한 AI 클러스터는 미래를 내다본 설계로 Tier 4의 입지를 더욱 공고히할 것입니다.

콜로케이션은 인도네시아의 기업 기반이 세분화되어 있는 탓에, 2025년 매출의 56.72%를 계속 차지했습니다. Digital Edge사의 23MW 자카르타 거점과 같은 시설은 모듈식 홀을 통해 확장성을 제공하며, 기존 캐리어 호텔보다 이용률 향상을 가속화하는 다년 계약의 주요 임차인을 확보하고 있습니다.

자체 건설형 하이퍼스케일러는 연평균 성장률(CAGR) 19.5%로 성장을 지속하고, 있으며, 20헥타르 부지에 120MW 이상의 캠퍼스를 건설함으로써 인도네시아의 데이터센터 건설 시장을 확대되고 있습니다. EdgeConneX가 조달한 4억 380만 달러 규모의 지속가능성 연계형 대출은 사업자가 재생에너지를 활용한 건설 자금을 조달하기 위해 그린본드 구조를 어떻게 활용하고 있는지를 잘 보여줍니다. 하이퍼스케일러의 진출로 인해, 기존 코로케이션 사업자들은 도매형 스위트나 빌드-투-수트형 모델로 전환할 수밖에 없게 되었으며, 과거에는 명확했던 멀티테넌트 전략과 싱글테넌트 전략의 경계가 점차 모호해지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the indonesian data center construction market size in 2026 is estimated at USD 3.61 billion, growing from 2025 value of USD 3.05 billion with 2031 projections showing USD 8.29 billion, growing at 18.12% CAGR over 2026-2031.

This report is Segmented by Tier Type (Tier 1 and 2, Tier 3 and Tier 4), Data Center Type(Colocation, Self-Built Hyperscalers (CSPs), Enterprise, and Edge), Infrastructure (Electrical Infrastructure, Mechanical Infrastructure). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Data Center Construction Market Trends and Insights

Cloud and AI-Led Hyperscale Investments Accelerate Facility Demand

Hyperscale cloud firms are redefining the Indonesian data center construction market by introducing AI workloads that require liquid-cooling, 40-60 kW racks, and contiguous power blocks exceeding 50 MW per campus. Tencent's USD 500 million commitment, Nvidia's USD 200 million GPU center with Indosat Ooredoo Hutchison, and BDx's 500 MW renewable-powered AI campus exemplify the scale of capital flowing into. Indonesia (AI) optimised data center is increasing demand for high-density infrastructure and advanced cooling technologies across hyperscale facilities. The need for immersion cooling and high-density electrical buses is stretching local contractors' skill sets, prompting global engineering firms to form joint teams with domestic specialists. Construction schedules have tightened from an average 22 months in 2022 to 16-18 months in 2025 as land owners provide pre-approved permits and ready-built substations.

National Digital Indonesia Roadmap 2030 Spurs Public-Sector IT Loads

The Roadmap mandates the consolidation of ministerial IT workloads into four National Data Centers (PDN). The flagship Cikarang PDN, financed at EUR 164.68 million (USD 189.59 million), delivers 25,000 processor cores and is scheduled to begin in August 2024. Three additional PDN sites in Batam and Nusantara are in the pipeline, ensuring steady demand for Tier 4 builds over the next five years. Presidential Regulation 82/2023 requires agencies to migrate from legacy facilities, stimulating a surge of design-build contracts for secure cloud zones, zero-trust networks, and cyber-resilient plant rooms. The ramp-up has also catalysed INA DIGITAL, the new single window for public services that launched in May 2024, which now drives inter-ministerial bandwidth requirements well beyond earlier forecasts

Rising Power-Use and Carbon-Tax Exposure

Indonesia's carbon-tax regime took effect in 2022, applying levies on emissions that exceed sector caps. Because coal still supplies 67% of PLN's generation mix, large campuses risk material cost over-runs unless they secure renewable PPAs or on-site solar. PLN's roadmap to net-zero by 2060 adds future price uncertainty, driving operators toward real-time power monitoring, waste-heat reuse, and demand-response programmes. Early movers such as EDGE2 now pass carbon-neutral costs through to tenants, setting a precedent for premium pricing.

Other drivers and restraints analyzed in the detailed report include:

- New International Subsea Cables Landing in Jakarta and Batam Raise Latency Standards

- Edge Build-Outs in Surabaya, Medan and Makassar to Serve Tier-2 Cities

- Escalating Land Prices Around Jakarta CBD and Cikarang Industrial Parks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tier 3 facilities account for 50.62% of the Indonesia data center construction market size, reflecting their balanced cost-to-availability ratio. Colocation providers such as NeutraDC rely on Tier 3 certifications to court enterprise tenants that demand 99.982% uptime while staying mindful of capex constraints. Tier 1 and Tier 2 sites continue to serve latency-sensitive edge nodes where modest redundancy is acceptable.

Tier 4 builds, advancing at 18.6% CAGR, are reshaping the Indonesia data center construction market as AI workloads and sovereign-cloud mandates eliminate tolerance for downtime. DCI Indonesia's Tier IV edge facility in central Jakarta signals the march toward zero-fault architecture, with immersion cooling and compartmentalised power paths driving project costs 25-30% above Tier 3. STT GDC's announced AI clusters will further entrench Tier 4's position in future-ready designs.

Colocation maintains 56.72% of 2025 revenue thanks to Indonesia's fragmented enterprise base. Facilities such as Digital Edge's 23 MW Jakarta site offer scalability through modular halls, securing multi-year anchor tenants that raise the utilisation curve faster than legacy carrier-hotels.

Self-build hyperscalers are registering a 19.5% CAGR, swelling the Indonesia data center construction market through 120-MW-plus campuses on 20-hectare plots. EdgeConneX's USD 403.8 million sustainability-linked loan typifies how operators deploy green-bond structures to finance renewable-powered builds. The hyperscaler push is forcing colocation incumbents to pivot toward wholesale suites and build-to-suit models, blurring once-clear lines between multi-tenant and single-tenant strategies.

Complete Report Scope:

- By Tier Type

- Tier 1 and 2

- Tier 3

- Tier 4

- By Data Center Type

- Colocation

- Self-build Hyperscalers (CSPs)

- Enterprise and Edge

- By Infrastructure

- By Electrical Infrastructure

- Power Distribution Solution

- Power Distribution Solution

- Power Backup Solutions

- Power Backup Solutions

- Power Distribution Solution

- By Mechanical Infrastructure

- Cooling Systems

- Cooling Systems

- Racks and Cabinets

- Racks and Cabinets

- Servers and Storage

- Servers and Storage

- Other Mechanical Infrastructure

- Other Mechanical Infrastructure

- Cooling Systems

- General Construction

- Service - Design and Consulting, Integration, Support and Maintenance

- By Electrical Infrastructure

List of Companies Covered in this Report:

- Aurecon Group Pty Ltd

- PT AECOM Indonesia

- Arup Group

- Jacobs Engineering Group Inc.

- Turner and Townsend

- AWP Architects

- Aesler Group International

- PT Arkonin

- DSCO Group Pte Ltd

- Larsen and Toubro Ltd

- NTT Global Data Centers Indonesia

- Huawei Technologies

- Vertiv Group Corp.

- Schneider Electric SE

- ABB Ltd

- Legrand SA

- PT DCI Indonesia Tbk

- Princeton Digital Group

- Telkom Data Ekosistem (NeutraDC)

- BDx Indonesia

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-and-AI led hyperscale investments accelerate facility demand

- 4.2.2 National Digital Indonesia Roadmap 2030 spurs public-sector IT loads

- 4.2.3 New international subsea cables landing in Jakarta and Batam raise latency standards

- 4.2.4 Jakarta Bandung data-center corridor public-private zoning incentives

- 4.2.5 Corporate PPAs and green-tariff schemes open the door for renewable-powered campuses

- 4.2.6 Edge build-outs in Surabaya, Medan and Makassar to serve emerging Tier-2 cities

- 4.3 Market Restraints

- 4.3.1 Rising power-use and carbon-tax exposure

- 4.3.2 Escalating land prices around Jakarta CBD and Cikarang industrial parks

- 4.3.3 Shortage of specialised MEP-certified construction labour

- 4.3.4 Slow grid-upgrade cycle times at PLN substations delay energisation

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Key Data Center Statistics

- 4.8.1 Exhaustive Data Center Operators in Indonesia(in MW)

- 4.8.2 List of Major Upcoming Data Center Projects in Indonesia (2025-2030)

- 4.8.3 CAPEX and OPEX For Indonesia Data Center Construction

- 4.8.4 Data Center Power Capacity Absorption In MW, Selected Cities, Indonesia, 2023 and 2024

- 4.9 Artificial Intelligence (AI) Inclusion in Data Center Construction in Indonesia

- 4.10 Regulatory and Compliance Framework

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Tier Type

- 5.1.1 Tier 1 and 2

- 5.1.2 Tier 3

- 5.1.3 Tier 4

- 5.2 By Data Center Type

- 5.2.1 Colocation

- 5.2.2 Self-build Hyperscalers (CSPs)

- 5.2.3 Enterprise and Edge

- 5.3 By Infrastructure

- 5.3.1 By Electrical Infrastructure

- 5.3.1.1 Power Distribution Solution

- 5.3.1.1.1 Power Distribution Solution

- 5.3.1.2 Power Backup Solutions

- 5.3.1.2.1 Power Backup Solutions

- 5.3.1.1 Power Distribution Solution

- 5.3.2 By Mechanical Infrastructure

- 5.3.2.1 Cooling Systems

- 5.3.2.1.1 Cooling Systems

- 5.3.2.2 Racks and Cabinets

- 5.3.2.2.1 Racks and Cabinets

- 5.3.2.3 Servers and Storage

- 5.3.2.3.1 Servers and Storage

- 5.3.2.4 Other Mechanical Infrastructure

- 5.3.2.4.1 Other Mechanical Infrastructure

- 5.3.2.1 Cooling Systems

- 5.3.3 General Construction

- 5.3.4 Service - Design and Consulting, Integration, Support and Maintenance

- 5.3.1 By Electrical Infrastructure

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Data Center Infrastructure Investment Based on Megawatt (MW) Capacity, 2024 vs 2030

- 6.5 Data Center Construction Landscape (Key Vendors Listings)

- 6.6 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.6.1 Aurecon Group Pty Ltd

- 6.6.2 PT AECOM Indonesia

- 6.6.3 Arup Group

- 6.6.4 Jacobs Engineering Group Inc.

- 6.6.5 Turner and Townsend

- 6.6.6 AWP Architects

- 6.6.7 Aesler Group International

- 6.6.8 PT Arkonin

- 6.6.9 DSCO Group Pte Ltd

- 6.6.10 Larsen and Toubro Ltd

- 6.6.11 NTT Global Data Centers Indonesia

- 6.6.12 Huawei Technologies

- 6.6.13 Vertiv Group Corp.

- 6.6.14 Schneider Electric SE

- 6.6.15 ABB Ltd

- 6.6.16 Legrand SA

- 6.6.17 PT DCI Indonesia Tbk

- 6.6.18 Princeton Digital Group

- 6.6.19 Telkom Data Ekosistem (NeutraDC)

- 6.6.20 BDx Indonesia

- 6.7 List of Data Center Construction Companies

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment