|

시장보고서

상품코드

2044286

멸균 주사제 위탁 제조 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Sterile Injectable Contract Manufacturing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

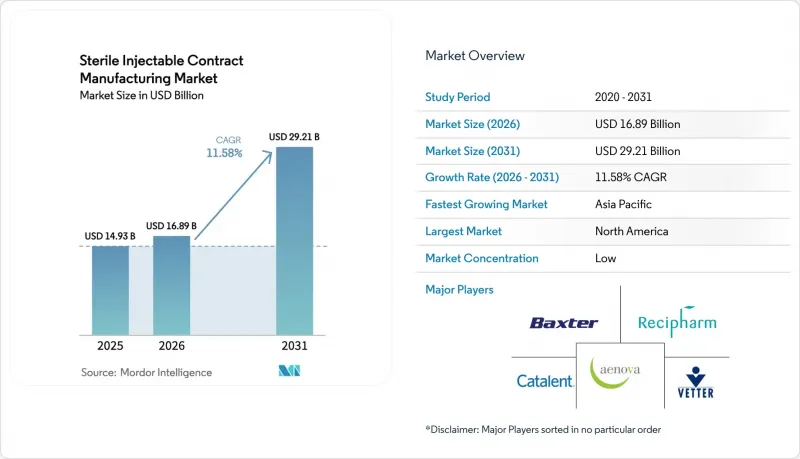

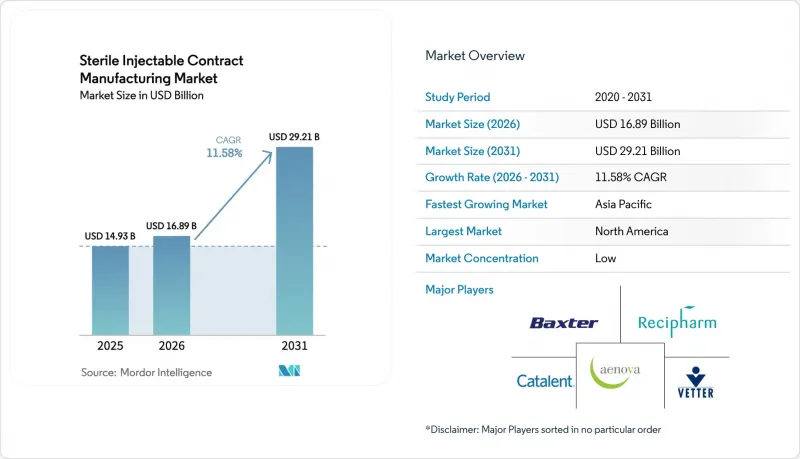

멸균 주사제 위탁 제조 시장 규모는 2025년에 149억 3,000만 달러, 2026년에 168억 9,000만 달러되어, 2031년까지 292억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 11.58%로 성장할 전망입니다.

이러한 상승세는 제약사들이 자산을 최소화한 공급망을 선호하는 경향, 바이오의약품 파이프라인의 확대, 그리고 이중 소싱을 제도화하는 의약품 부족 대책의 강화로 뒷받침되고 있습니다. 2024년 이후 발표된 생산능력 투자는 제약기업이 제품 소유권을 유지하면서 자본집약적인 멸균 제조 인프라를 외부에 위탁하고 있는 현실을 보여줍니다. 만성질환 치료용 프리필드 디바이스가 바이알을 대체하는 경향이 증가하고 있으며, 이에 따라 고속 주사기 충전 및 복합 제품 조립에 대한 수요가 증가하고 있습니다. 다가오는 특허 만료에 따른 바이오시밀러 출시는 더 많은 생산량과 복잡성을 추가할 것이며, 규제 대응 실적이 있는 CDMO는 장기적인 마스터 서비스 계약을 체결할 수 있습니다. 한편, 붕규산 유리 및 일회용 부품공급망 병목현상은 단기적으로 처리 능력의 확장을 억제하고 있습니다.

세계 멸균 주사제 위탁 제조 시장 동향 및 인사이트

바이오 의약품 파이프라인 확장으로 특수 멸균 생산 능력에 대한 수요 증가

FDA는 2024년 16건의 신규 생물학적 제제를 승인했으며, 이는 전년도 12건보다 증가한 수치입니다. 한편, EMA는 14개의 새로운 생물학적 제제를 승인하여 혁신의 꾸준한 모멘텀을 뒷받침하고 있습니다. 세포독성 항체 약물 복합체(ADC)는 전용 아이솔레이터 스위트가 필요하지만, 현재 상업적 규모로 이러한 설비를 제공할 수 있는 CDMO는 20개 미만입니다. 세포 및 유전자 치료는 자가 유래 배치가 일반적으로 100개 미만이기 때문에 복잡성이 더욱 증가하고 있으며, 공급자는 수요에 따라 구성 가능한 모듈식 클린룸과 일회용 바이오리액터를 도입해야 합니다. 캐터런트는 2025년 메릴랜드 주에 1억 5,000만 달러를 투자한 바이오 의약품 시설을 가동할 예정입니다. 이 시설은 4개의 독립적인 고활동성 스위트 룸을 갖추고 있으며, 주요 기업들 간의 설비투자(CAPEX) 경쟁이 치열해지고 있음을 보여줍니다.

설비투자 절감 및 시장 출시 기간 단축을 위한 아웃소싱 급증

화이자는 2024년 말 미국 내 노후화된 멸균 생산 공장 2곳을 폐쇄하고, 생산을 파트너사에 이관함으로써 연간 3억 달러의 운영비를 절감했습니다. 2025년 임상 2상 종양학 임상시험의 60% 이상이 자체 생산 능력을 갖추지 못한 가상 바이오텍 기업이 후원하고 있으며, GMP를 준수하는 공급에 있어 CDMO에 대한 의존도가 높아지고 있습니다. 현재 FDA의 '신기술 프로그램'에서 인증된 연속 멸균 제조 공정은 로트 릴리스 기간을 단축할 수 있지만, 전문적 노하우가 필요하기 때문에 많은 혁신 기업들이 계약 파트너로부터 조달하고 있습니다.

자본 집약적인 GMP 멸균 시설

신규 멸균공장 건설비용은 현재 2억 달러가 넘고, 자격인증에 3-5년이 소요되어 신규 진입을 막고, 중견업체들의 적극적인 확장을 제한하고 있습니다. PwC의 조사에 따르면, 2025년 ISO 5 클린룸의 비용은 평방미터당 15,000달러로, HVAC(공조 설비)와 검증 비용 상승으로 인해 2023년 대비 22% 증가할 것으로 예상했습니다. 유럽의 CDMO는 2024년 가스 가격 급등으로 광열비가 40% 급등하면서 프로젝트 ROI가 더욱 압박을 받았습니다. 모듈식 조립식 시설은 건설 기간을 18개월로 단축할 수 있지만, 재구성 관리와 관련된 규제 불확실성에 여전히 직면해 있습니다.

부문 분석

2025년에도 저분자 의약품은 62.83%의 매출 점유율을 유지했습니다. 그러나 바이오의약품 매출은 CAGR 14.69%로 확대될 것으로 예상되며, 이는 바이오의약품 멸균주사제 위탁 제조 시장 규모가 전체 서비스 시장보다 빠르게 확대될 것임을 의미합니다. 화이자 센터원은 바이오의약품이 파이프라인의 55%를 차지하고 있으며, 이는 2년 전의 38%에서 크게 증가한 수치라고 밝혔습니다. 아이솔레이터를 갖춘 세포독성 의약품 제조시설을 보유한 CDMO는 ADC(항체 약물 복합체) 프로젝트에서 프리미엄 가격을 책정하고 있습니다. 저분자 의약품 생산량은 식염수, 포도당, 마취제 라인에 여전히 필수적이지만, 동유럽공급 과잉으로 인해 2023년 이후 8%의 가격 하락이 예상되고 있습니다. 최근 FDA로부터 재택 사용을 승인받은 피하투여용 바이오의약품은 고점도 제제의 주사기 충전에 대한 투자를 촉진하고 있습니다. WuXi Biologics는 아일랜드의 ADC 생산 능력 확장에 2억 4,000만 달러를 투자했으며, 이는 스폰서들 수요 규모를 반영하고 있습니다.

지역별 분석

북미는 노스캐롤라, 뉴저지, 메릴랜드에 FDA 검사 시설이 밀집되어 있어 2025년 매출의 37.26%를 차지했습니다. 스폰서 기업들은 기술이전 협력에 있어 지리적 근접성을 중시하고 있으며, 높은 인건비는 프리미엄 가격으로 상쇄되고 있습니다. 그럼에도 불구하고 아시아태평양은 2031년까지 연평균 복합 성장률(CAGR) 16.04%로 성장을 견인할 것으로 예측됩니다. 중국의 '바이오 보안' 정책은 국내 충진 및 마무리를 장려하고 있으며, WuXi Biologics가 2억 달러를 투자한 우시 공장은 현지화의 급격한 증가를 상징하는 사례입니다. 인도는 WHO의 사전 인증을 활용하여 비용에 민감한 지역에 바이오시밀러를 수출하고 있으며, 이를 통해 국내 수요를 훨씬 능가하는 수요를 충족시키고 있습니다.

유럽의약품청(EMA)의 중앙집중식 심사 프로세스는 단일 인증 시설로 EU 전 회원국에 대응할 수 있기 때문에 지역 CDMO가 사업 규모를 확장할 수 있는 유연성을 제공합니다. 그러나 유럽의 치솟는 에너지 가격은 2024년까지 수익률을 압박하여 재생에너지 구매 계약에 대한 관심을 높였습니다. 중동 및 아프리카은 규모는 작지만, '사우디 비전 2030'이 의약품 제조의 40%를 국내 생산한다는 목표를 세우면서 그 중요성이 커지고 있으며, 여러 CDMO가 신규 프로젝트를 검토하고 있습니다.

남미에서는 2024년에 제정된 브라질의 간소화된 바이오시밀러 상호교환성 규정이 효과를 발휘하여 현지 시장 진출을 노리는 외국계 합작 투자기업을 끌어들이고 있습니다. 국내 조달 의무는 멸균 제조 영역의 자금 조달에 필수적인 생산량 확보를 가져오고, 이 영역에 진입하는 초기 단계 CDMO의 규제 리스크를 줄여줍니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSThe Sterile Injectable Contract Manufacturing Market size is projected to be USD 14.93 billion in 2025, USD 16.89 billion in 2026, and reach USD 29.21 billion by 2031, growing at a CAGR of 11.58% from 2026 to 2031.

The uptrend is anchored in drug-sponsor preference for asset-light supply chains, swelling biologics pipelines, and tighter drug-shortage rules that institutionalize dual sourcing. Capacity investments announced since 2024 illustrate how sponsors are outsourcing capital-intensive aseptic infrastructure while retaining product ownership. Prefilled devices for chronic therapies are increasingly displacing vials, thereby elevating demand for high-speed syringe filling and combination-product assembly. Biosimilar launches linked to looming patent cliffs add further volume and complexity, pulling CDMOs with proven regulatory credentials into long-term master service agreements. At the same time, supply-chain bottlenecks for borosilicate glass and single-use components temper near-term expansion of throughput.

Global Sterile Injectable Contract Manufacturing Market Trends and Insights

Biologics Pipeline Expansion Boosts Demand for Specialized Aseptic Capacity

The FDA cleared 16 novel biologics in 2024, up from 12 approvals the previous year, while the EMA approved 14 new biologicals, underscoring steady momentum in innovation. Cytotoxic antibody-drug conjugates require dedicated isolator suites, and fewer than 20 CDMOs presently offer such capacity at commercial scale. Cell and gene therapies add further complexity because autologous batches typically run below 100 units, prompting providers to adopt modular cleanrooms and single-use bioreactors that can be configured on demand. Catalent commissioned a USD 150 million biologics facility in Maryland in 2025, which features four independent high-potency suites, highlighting the capital expenditure (capex) race among top players.

Outsourcing Surge to Cut Cap-Ex & Accelerate Time-To-Market

Pfizer closed two legacy U.S. sterile plants in late 2024 and shifted output to partners, freeing USD 300 million in annual operating expense. More than 60% of Phase II oncology trials in 2025 were sponsored by virtual biotechs lacking internal manufacturing, increasing CDMO reliance for GMP supply. Continuous aseptic processing, now recognized under the FDA's Emerging Technology Program, can shorten lot-release times, yet it demands specialized know-how that most innovators source from contract partners.

Capital-Intensive GMP Sterile Facilities

Greenfield aseptic plants now exceed USD 200 million and require 3-5 years to qualify, deterring newcomers and limiting aggressive expansion among midsized providers. PwC measured ISO 5 cleanroom costs at USD 15,000 per square meter in 2025, up 22% from 2023, due to inflation in HVAC and validation. European CDMOs endured a 40% jump in utility bills during the 2024 gas-price spike, further squeezing project ROIs. Modular prefabs shrink timelines to 18 months but still face regulatory uncertainty about reconfiguration controls.

Other drivers and restraints analyzed in the detailed report include:

- Chronic-Disease Prevalence Growing Parenteral Volumes

- Patent Cliffs Spur Generic & Biosimilar Injectables

- Complex & Evolving Global Regulatory Compliance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Small molecules retained a 62.83% revenue share in 2025; however, biologics revenue is forecast to expand at a 14.69% CAGR, meaning that the Sterile Injectable Contract Manufacturing market size for biologics will accelerate faster than the broader service pool. Pfizer CentreOne confirmed that biologics represent 55% of pipeline deals, up sharply from 38% two years earlier. CDMOs with isolator-based cytotoxic suites enjoy premium pricing for ADC campaigns. Small-molecule volumes remain vital for saline, dextrose, and anesthetic lines, yet overcapacity in Eastern Europe has driven an 8% price decline since 2023. Subcutaneous biologics, recently cleared by the FDA for home use, are steering investment toward high-viscosity syringe filling. WuXi Biologics allocated USD 240 million to expand ADC capacity in Ireland, reflecting the scale of sponsor demand.

The Sterile Injectable Contract Manufacturing Market Report is Segmented by Molecule Type (Small Molecule, Large Molecule/Biologics), Service Stage (Pre-Clinical, Clinical, Commercial), Delivery Format (Vials, Prefilled Syringes, Cartridges, Ampoules & Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.26% of 2025 revenue thanks to dense clusters of FDA-inspected suites in North Carolina, New Jersey, and Maryland. Sponsors value proximity for tech-transfer collaboration, and premium pricing offsets higher labor costs. Nonetheless, Asia-Pacific is forecast to lead growth at a 16.04% CAGR through 2031. China's "bio-security" policy encourages domestic fill-finish, and WuXi Biologics' USD 200 million Wuxi plant exemplifies the surge in localization. India leverages the WHO prequalification to export biosimilars to cost-sensitive regions, thereby meeting demand well above its local needs.

The EMA centralized review process enables a single qualified site to serve all EU members, providing regional CDMOs with the flexibility to scale. High European energy prices, however, narrowed margins by 2024 and spurred interest in renewable power purchase agreements. Middle East & Africa, though tiny, is gaining relevance after Saudi Vision 2030 set a 40% local drug-manufacturing target, leading several CDMOs to scope greenfield projects.

South America benefits from Brazil's streamlined biosimilar interchangeability rules, established in 2024, which attract foreign joint ventures seeking entry into the local market. National content mandates provide volume commitments critical for financing sterile suites, and they reduce regulatory risk for early-stage CDMOs entering the region.

- Aenova Group

- Ajinomoto Bio-Pharma Services

- Baxter BioPharma Solutions

- Boehringer Ingelheim BioXcellence

- Bushu Pharmaceuticals

- Catalent

- Cipla

- Emergent Bio Solutions

- Fresenius

- Grand River Aseptic Manufacturing

- HALIX B.V.

- Jubilant HollisterStier

- LSNE Contract Manufacturing

- NextPharma Technologies

- Pfizer CentreOne

- Recipharm

- Seikagaku

- Symbiosis Pharmaceutical Services

- Unither Pharmaceuticals

- Vetter Pharma-Fertigung GmbH & Co. KG

- Wuxi Biologics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Biologics Pipeline Expansion Boosts Demand for Specialized Aseptic Capacity

- 4.2.2 Outsourcing Surge to Cut Cap-Ex & Accelerate Time-To-Market

- 4.2.3 Chronic-Disease Prevalence Growing Parenteral Volumes

- 4.2.4 Patent Cliffs Spur Generic & Biosimilar Injectables

- 4.2.5 Drug-Shortage Mitigation Rules Create Mandatory Dual-Sourcing

- 4.2.6 Modular Micro-Fill Isolators Enable Personalized Therapy Batches

- 4.3 Market Restraints

- 4.3.1 Capital-Intensive GMP Sterile Facilities

- 4.3.2 Complex & Evolving Global Regulatory Compliance

- 4.3.3 Supply-Chain Pinch on Pharma-Grade Borosilicate Glass & SUT

- 4.3.4 Long Lead Times for Isolator Equipment Causing Capacity Bottlenecks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Molecule Type

- 5.1.1 Small Molecule

- 5.1.2 Large Molecule / Biologics

- 5.2 By Service Stage

- 5.2.1 Pre-clinical Manufacturing

- 5.2.2 Clinical Manufacturing

- 5.2.3 Commercial Manufacturing

- 5.3 By Delivery Format

- 5.3.1 Vials

- 5.3.2 Prefilled Syringes

- 5.3.3 Cartridges

- 5.3.4 Ampoules & Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Aenova Group

- 6.3.2 Ajinomoto Bio-Pharma Services

- 6.3.3 Baxter BioPharma Solutions

- 6.3.4 Boehringer Ingelheim BioXcellence

- 6.3.5 Bushu Pharmaceuticals

- 6.3.6 Catalent Inc.

- 6.3.7 Cipla Ltd.

- 6.3.8 Emergent BioSolutions

- 6.3.9 Fresenius Kabi

- 6.3.10 Grand River Aseptic Manufacturing

- 6.3.11 HALIX B.V.

- 6.3.12 Jubilant HollisterStier

- 6.3.13 LSNE Contract Manufacturing

- 6.3.14 NextPharma Technologies

- 6.3.15 Pfizer CentreOne

- 6.3.16 Recipharm AB

- 6.3.17 Seikagaku Corporation

- 6.3.18 Symbiosis Pharmaceutical Services

- 6.3.19 Unither Pharmaceuticals

- 6.3.20 Vetter Pharma-Fertigung GmbH & Co. KG

- 6.3.21 WuXi Biologics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment