|

시장보고서

상품코드

2044287

지속가능 전자상거래 포장 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Sustainable E-Commerce Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

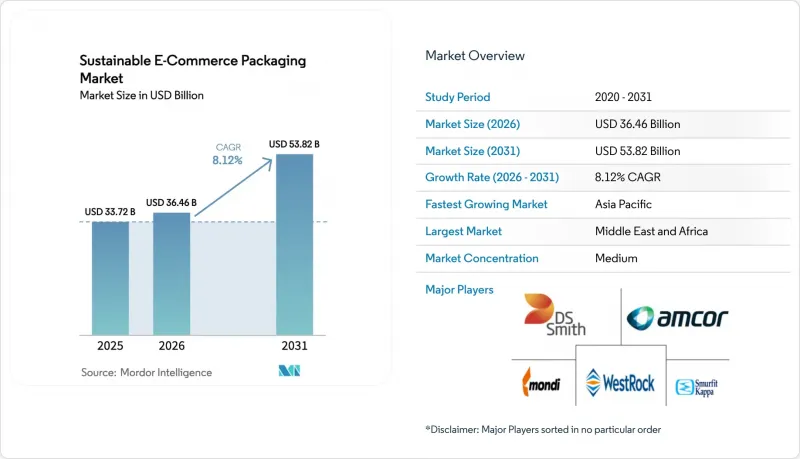

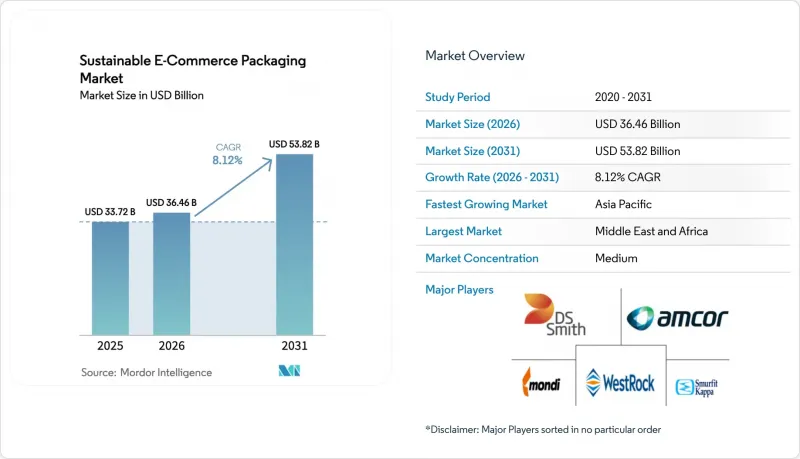

지속가능 전자상거래 포장 시장 규모는 2025년에 337억 2,000만 달러, 2026년에 364억 6,000만 달러가 되어, 2031년까지 538억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년까지 CAGR 8.12%로 성장할 전망입니다.

일회용 플라스틱에 대한 규제 압력 증가, 온라인 주문량 급증, 저탄소 소재에 대한 소비자의 뚜렷한 선호도가 라스트마일 배송에서 지속 가능한 솔루션에 대한 수요를 가속화하고 있습니다. 부피 중량 요금을 절감하는 형태 최적화 기술과 확대되는 순환경제 비즈니스 모델이 맞물려 얼리어답터를 넘어 도입이 확산되고 있습니다. 섬유계 소재를 취급하는 주요 기업 간의 통합으로 세계 규모와 R&D 예산이 확대되고 있는 가운데, AI를 활용한 적정 사이즈 선정 시스템은 측정 가능한 비용 절감을 실현하여 브랜드 소유자의 투자 회수 근거를 공고히 하고 있습니다.

세계 지속가능 전자상거래 포장 시장 동향과 인사이트

재활용 가능하고 친환경적인 소재에 대한 소비자 선호도 변화

진정한 환경보호에 대한 노력을 입증한 브랜드는 현재 가격 프리미엄과 더 깊은 충성도를 확보하고 있습니다. 뷰티 및 퍼스널케어 브랜드에 따르면, 쇼핑객의 61%가 친환경 브랜드를 적극적으로 찾고 있으며, 이로 인해 사용 후 재활용 소재(PCR)로 전환하여 버진 수지 대체품에 비해 40% 이상의 탄소 발자국 감소를 달성했다고 보고했습니다. 따라서 PCR의 채택은 수익의 회복력과 평판 가치를 모두 높이고 있습니다. 소매업체들은 PCR 재료 사용 의무를 개인 브랜드 제품에도 확대하고 있으며, 재활용 가능성은 여러 온라인 카테고리에서 최소한의 진입 요건이 되고 있습니다. 정부도 2025년 유럽연합(EU)에서 시행되는 재활용 소재 함유량 의무화 기준을 통해 이러한 추세를 부추기고 있으며, 대응 가능한 소재에 대한 기초적인 수요를 높이고 있습니다. 이에 따른 파급 효과로 차세대 섬유 회수 시스템에 대한 투자가 가속화되고, 고품질 공급원이 확대되고, 비용 프리미엄이 낮아지고 있습니다. 전환량이 증가하는 가운데, 초기 도입 기업들은 다년간의 PCR 원료 공급 계약을 체결하여 수익률을 확보하고 있습니다.

전자상거래 주문량 및 라스트마일 배송의 폭발적인 성장세

온라인 소비가 오프라인 소매를 넘어섰고, 모든 카테고리에서 보호 포장에 대한 수요가 증가하고 있습니다. 랑팩은 2024년 3분기 완충재 취급량이 14.7% 증가했고, 순매출액은 11.4% 증가한 9,220만 달러를 기록했습니다. 아마존의 96.7% 재펄프화 가능한 종이 완충재 우편 봉투는 섬유 기반 솔루션이 낙하 검사 기준을 충족하고 가정용 쓰레기 수거 시스템에 통합될 수 있음을 입증했습니다. 이에 따라 전자상거래 업체들은 플라스틱에서 종이로의 전환을 가속화하고 있으며, 비용 효율성과 지속가능성 측면에서 이점을 누리고 있습니다. 처리량에 연동된 규모의 경제로 인해 자동 이송 하에서 천공에 견딜 수 있는 고강도 경량 용지의 가격 경쟁이 더욱 치열해지고 있습니다. 이러한 추세는 주류 재활용 공정에 대응하는 방습 코팅에 대한 수요를 증가시키고, 가공업체와 화학물질 공급업체 간의 공동 연구개발을 촉진하고 있습니다. 출하 빈도가 구조적으로 높은 수준으로 정상화되는 가운데, 대규모 생산 체제에서도 일관된 품질을 보장하는 포장 공급업체가 우선 공급업체로 자리매김하고 있습니다.

공급망 변동성 및 섬유 및 폴리머 원료 비용 변동성

컨테이너 보드 가격은 온라인 수요 급증과 에너지 비용 상승에 힘입어 2024년 이후 두 자릿수 상승률을 기록하며 컨버터 수익률을 압박하고 있습니다. 바이오 수지공급이 더욱 타이트해지면서 농산물 가격의 변동이 PLA와 PHA의 비용 구조에 영향을 미치고 있습니다. 대규모 통합형 생산자들은 자체 소유의 산림 자산과 다년간의 구매자 측 계약을 통해 리스크를 완화하고 있지만, 소규모 컨버터들은 운전자금 수요의 팽창으로 유동성 리스크에 직면해 있습니다. 현물 가격의 불안정성은 브랜드 소유주에게 선물 가격 책정을 복잡하게 만들고, 계약 갱신 지연과 새로운 형태 개발의 둔화를 초래하고 있습니다. 따라서 가격의 불확실성이 높아지는 가운데, 생산능력 증설로 원자재 부족이 완화될 때까지 헤지 전략을 지속할 수 있는 기존 유력 업체들이 일시적으로 유리한 위치에 있습니다.

부문 분석

종이 및 판지는 광범위한 재활용 가능성, 비용 우위, 견고한 공급망 덕분에 2025년 지속 가능한 전자상거래 포장 시장에서 47.02%의 점유율을 차지했습니다. 바이오플라스틱은 사탕수수 유래 PE, 나무 껍질 기반 필름, 조류 코팅이 성숙함에 따라 2031년까지 9.78%의 가장 높은 CAGR을 나타낼 것으로 예측됩니다. 바이오플라스틱을 이용한 지속 가능한 전자상거래 포장 시장 규모는 식품 및 퍼스널케어 제품의 높은 차단 성능에 대한 수요 증가를 반영하여 2031년까지 9억 3,200만 달러에 달할 것으로 예측됩니다. 섬유업체들은 재펄프화 검사를 통과하는 내수성 분산액을 추가하여 점유율을 지키기 위해 노력하고 있으며, 석유화학 산업의 기존 기업들은 단일 소재의 재활용 제품의 유용성을 유지하기 위해 화학적 재활용의 백루프에 투자하고 있습니다. 단백질 기반 필름에 대한 벤처 자금의 유입은 원료 선택의 폭이 넓어지고 있음을 의미하며, 이로 인해 기존 등급과의 가격 차이가 줄어들 것으로 예측됩니다.

크래프트 라이너 보드와 PLA의 비용 차이는 2025년 20% 이하로 줄어들고, 고투명 창이 필요 없는 우편 봉투의 대체가 가속화되고 있습니다. 탄소중립을 약속하는 브랜드는 인증된 퇴비화 필름이 산업용 퇴비화와 결합하여 저배출을 위한 선택이 될 수 있음을 보여주는 수명주기 분석 데이터에 의존하고 있습니다. 따라서 기업의 조달 부서는 기술 및 규제 리스크를 헤지하기 위해 기존 섬유 소재와 신흥 바이오 폴리머에 대한 조달 물량을 분산하여 조달하고 있습니다. 단일 조달 계약 내에서 두 기재를 결합할 수 있는 공급업체는 협상에서 우위를 점할 수 있으며, 경기 사이클을 통해 안정적인 공급량을 확보할 수 있습니다.

2025년 골판지 상자는 다용도성, 적재 강도, 성숙한 재활용 시스템을 배경으로 지속 가능한 전자상거래 포장 시장의 72.10%를 차지하며 압도적인 점유율을 유지했습니다. 한편, AI를 활용한 카톤화 시스템을 통해 완충재가 필요 없는 우편물 및 봉투는 9.41%의 연평균 복합 성장률(CAGR)을 보이고 있습니다. 소매업체들이 깨지기 쉬운 상품의 낙하 테스트를 통과하는 종이 완충재를 채택함에 따라 우편물용 지속 가능한 전자상거래 포장 시장 규모는 2031년 85억 5,000만 달러에 달할 것으로 예측됩니다. 슬림한 형태는 컨베이어의 처리 능력을 향상시키고 트레일러의 적재 공간 낭비를 줄여 배송 허브에 이점을 제공합니다.

소매업체는 형태 다양화와 SKU 수준의 예측 분석을 결합하여 보호 성능을 저하시키지 않으면서도 실현 가능한 최소 외부 포장 크기를 선택할 수 있도록 하고 있습니다. 구독형 EC 브랜드는 마케팅 매체로도 활용할 수 있는 인쇄된 메일러를 선호하고 있으며, 소량 생산을 경제적으로 처리할 수 있는 디지털 인쇄 라인의 도입이 가속화되고 있습니다. 대형 가전제품 주문은 여전히 박스가 중심이지만, 현재 박스 디자인에는 역물류의 워크플로우에 맞추어 떼어내어 붙이는 방식의 밀봉과 천공된 반송용 스트립이 내장되어 있습니다. 폼 인서트는 성형 펄프 구조를 대체하여 석유 원료 사용량을 줄이고 가정에서의 재활용성을 향상시켰습니다.

지역별 분석

2025년, 아시아태평양은 지속 가능한 전자상거래 포장 시장의 42.35%를 차지했습니다. 이는 중국의 방대한 소포 취급량과 인도의 두 자릿수 성장을 지속하고 있는 전자상거래 소매 시장에 힘입은 것입니다. 중국에서는 일부 지방 정부가 세금 환급을 재활용 재료 함량 기준과 연계하여 수출 지향적 판매 업체에서 PCR 라이너 보드에 대한 수요를 촉진하고 있습니다. 일본의 가공업체들은 NFC 태그를 통합한 스마트 라벨 기술을 선도적으로 개발하여 진위 확인 및 콜드체인 알림을 가능하게 합니다. 동남아시아의 풀필먼트 허브에서는 각국의 플라스틱 폐기물 대책 로드맵에 따라 EPS를 대체할 수 있는 종이 단열 포장을 채택하고 있습니다. 아시아태평양의 지속 가능한 전자상거래 포장 시장 규모는 섬유 및 바이오 수지 원료의 현지 생산을 반영하여 2031년까지 236억 달러 이상에 달할 것으로 예측됩니다.

중동 및 아프리카는 걸프 지역의 옴니채널 전략과 아프리카의 모바일 커머스의 급격한 성장에 힘입어 9.66%의 가장 높은 CAGR을 기록했습니다. 사우디 소비자 조사에서 친환경 포장에 대해 최대 12%의 할증료를 지불할 의향이 있는 것으로 나타났으며, 이는 고처리 용량의 골판지 제조기를 도입하는 현지 가공업체들의 수입 대체를 촉진하고 있습니다. 아랍에미리트는 2026년까지 전자상거래 외부 포장재의 100% 재활용을 의무화하고 있어 경량 크래프트 소재의 우편물 포장재에 대한 관심이 높아지고 있습니다. 남아공은 비교적 잘 갖춰진 회수 인프라를 활용하여 섬유 기반 단열 라이너의 문전수거를 시험적으로 도입하여 사하라 이남 지역 수출의 거점으로 자리매김하고 있습니다. 케냐와 르완다의 물류 자유무역지대는 동아프리카의 국경 간 무역을 지원하는 자동화 우편물 생산라인에 대한 투자를 유치하고 있습니다.

북미와 유럽은 여전히 성숙한 시장이지만, 확대되는 생산자책임제도와 플라스틱세 도입을 통해 세계 표준을 형성하는 영향력 있는 시장으로 남아있습니다. 유럽 연합(EU)의 "포장 및 포장 폐기물 규정"은 2030년까지 모든 EC용 포장재를 재사용 또는 재활용할 수 있도록 의무화하고 있으며, 섬유 전문 제조업체들 사이에서 디자인 개선이 빠르게 진행되고 있습니다. 미국 브랜드 소유주들은 2027년까지 최소 8개 주에서 EPR(확대된 생산자 책임)이 전국적으로 통과될 것으로 예상하고 있으며, 총비용 모델에 요금 체계를 통합하고 있습니다. 이들 지역에서는 섬유 기반 능동형 온도 관리 배송 컨테이너, 블록체인 검증 시스템에 정보를 제공하는 클라우드 연결형 추적 및 추적 라벨 등 고도로 복잡한 솔루션의 검사 운영이 계속되고 있습니다. 이를 통해 얻은 지식은 급성장하는 신흥 시장에 반영되어 검증된 순환경제 프레임워크에 대한 전 세계의 수렴을 가속화하고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 동향

JHS 26.06.02The Sustainable E-Commerce Packaging Market size is projected to be USD 33.72 billion in 2025, USD 36.46 billion in 2026, and reach USD 53.82 billion by 2031, growing at a CAGR of 8.12% from 2026 to 2031.

Rising regulatory pressure on single-use plastics, surging online order volumes, and clear consumer preference for low-carbon materials are accelerating demand for sustainable solutions across last-mile delivery. Format optimization technologies that reduce dimensional weight fees, alongside expanding circular-economy business models, are broadening adoption beyond early movers. Consolidation among leading fiber-based players is improving global scale and R&D budgets, while AI-enabled right-sizing systems deliver measurable cost savings that reinforce payback arguments for brand owners.

Global Sustainable E-Commerce Packaging Market Trends and Insights

Shift in consumer preference toward recyclable and eco-friendly materials

Brands that prove real environmental commitment now secure price premiums and deeper loyalty. Beauty and personal-care labels report that 61% of shoppers actively seek eco-aligned brands, prompting conversions to post-consumer-recycled (PCR) substrates and achieving carbon-footprint cuts of more than 40% versus virgin resin alternatives. PCR uptake therefore builds both revenue resilience and reputational equity. Retailers are extending PCR mandates to private-label ranges, making recyclability a minimum entry requirement across multiple online categories. Governments reinforce the trend via mandatory recycled-content thresholds that take effect in the European Union in 2025, raising baseline demand for compatible materials. The resulting pull-through effect speeds investment in next-generation fiber recovery systems, widening quality supply and lowering cost premiums. As conversion volumes climb, early adopters protect margin by locking multiyear PCR feedstock agreements.

Explosive growth in e-commerce order volumes and last-mile deliveries

Online spending outpaces store-based retail, lifting protective-packaging requirements across categories. Ranpak logged a 14.7% rise in void-fill volumes in Q3 2024, with net sales up 11.4% to USD 92.2 million . Amazon's 96.7%-repulpable paper-padded mailer proves that fiber-based solutions can meet drop-test criteria and integrate into curbside streams. E-retailers subsequently accelerate plastic-to-paper shifts, capturing both cost efficiencies and sustainability gains. Volume-linked economies of scale widen price competitiveness for high-strength lightweight papers that resist puncture under automated handling. The trend raises demand for moisture-barrier coatings compatible with mainstream recycling processes, stimulating joint R&D between converters and chemical suppliers. As shipment frequency normalizes at a structurally higher base, packaging suppliers that guarantee consistent quality at scale consolidate preferred-supplier status.

Supply-chain volatility and fluctuating fiber / polymer input costs

Containerboard prices have posted double-digit jumps since 2024, propelled by surging online demand and energy-cost spikes, straining converters' margins. Bio-based resin supply is even tighter, with agricultural-commodity price swings feeding through to PLA and PHA cost structures. Large integrated producers mitigate exposure through captive forestry assets or multiyear buy-side contracts, but small converters face liquidity risk as working-capital needs inflate. Spot-price instability complicates forward-pricing for brand owners, delaying contract renewals and slowing new-format rollouts. Heightened price uncertainty therefore temporarily favors established incumbents that can underwrite hedging strategies until capacity additions ease feedstock tension.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven smart-box right-sizing systems reducing dimensional-weight fees

- Reusable packaging-as-a-service models gaining retailer adoption

- Barrier-property limitations of certain bio-based films and coatings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paper and paperboard accounted for 47.02% of the sustainable e-commerce packaging market in 2025 thanks to broad recyclability, cost advantages, and robust supply chains. Bioplastics register the fastest 9.78% CAGR to 2031 as sugarcane-derived PE, bark-based films, and algae coatings mature. The sustainable e-commerce packaging market size for bioplastics is projected to reach USD 9.32 billion by 2031, reflecting increased demand for higher barrier performance next to food and personal-care items. Fiber producers safeguard share by adding water-resistant dispersions that pass repulpability tests, while petrochemical incumbents invest in chemical-recycling back-loops to prolong the relevance of mono-material recyclables. Venture funding in protein-based films signals widening raw-material options poised to narrow price gaps with incumbent grades.

Cost differentials between kraft linerboard and PLA narrowed to under 20% in 2025, accelerating substitution in mailers that do not require high-clarity windows. Brands targeting carbon-neutral pledges lean on lifecycle-analysis data that position certified compostable films as a lower-emission choice when paired with industrial-compost access. Industrial procurement teams therefore split volumes across both fibers and emerging biopolymers to hedge technical and regulatory risk. Suppliers that can bundle both substrates within a single sourcing contract gain negotiating leverage and lock in throughput across economic cycles.

Corrugated boxes dominated at 72.10% of the sustainable e-commerce packaging market in 2025 on versatility, stacking strength, and a mature recycling stream. Mailers and envelopes, however, show a 9.41% CAGR on the strength of AI-assisted cartonization systems that eliminate void fill. The sustainable e-commerce packaging market size for mailers is forecast to hit USD 8.55 billion in 2031 as retailers deploy paper padded designs that meet fragile-item drop tests. Slim form factors benefit parcel hubs by lifting conveyor throughput and curbing trailer cube waste.

Retailers pair format diversification with SKU-level predictive analytics, ensuring the smallest feasible exterior is selected without compromising protective performance. Subscription-commerce brands prefer printed mailers that double as marketing real estate, accelerating adoption of digital-print lines that handle shorter runs economically. Boxes stay central for large consumer-electronics orders, yet box designs now integrate peel-and-seal closures and perforated returns strips to fit reverse-logistics workflows. Foam-in-place inserts give way to molded-pulp structures , cutting petroleum inputs and improving curbside recyclability.

The Sustainable E-Commerce Packaging Market Report is Segmented by Material Type (Plastic, Paper and Paperboard, Metal, Bioplastics), Packaging Format (Corrugated Boxes, Mailers and Envelopes, and More), End-User Industry (Fashion and Apparel, Consumer Electronics, and More), Sustainable Attribute (Recyclable, Compostable, Reusable, Biodegradable), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 42.35% of the sustainable e-commerce packaging market in 2025, buoyed by China's giant parcel volumes and India's double-digit e-retail expansion. Several provincial governments in China have tied tax rebates to recycled-content thresholds, boosting demand for PCR linerboard among export-oriented sellers. Japanese converters pioneer smart-label technologies that integrate NFC tags, enabling authenticity checks and cold-chain alerts. Southeast Asian fulfillment hubs adopt paper-based insulated shippers to replace EPS, aligning with national plastic-waste roadmaps. The sustainable e-commerce packaging market size in Asia-Pacific is projected to surpass USD 23.6 billion by 2031, reflecting localized production of both fiber and bio-resin inputs.

Middle East and Africa posts the fastest 9.66% CAGR, lifted by Gulf-region omnichannel initiatives and Africa's mobile-commerce surge. Saudi consumer surveys show willingness to pay up to 12% premiums for eco-friendly packaging, stimulating import substitution by regional converters installing high-throughput corrugators. The United Arab Emirates mandates 100% recyclability for e-commerce outer packs by 2026, propelling interest in lightweight kraft mailers. South Africa leverages comparatively robust collection infrastructure to pilot curbside separation of fiber-based insulated liners, positioning itself as a launchpad for sub-Saharan regional exports. Logistic free-zones in Kenya and Rwanda attract investment in automated mailer production lines that serve East-African cross-border trade.

North America and Europe remain mature but influential markets, shaping global standards through extended producer responsibility rules and plastic-tax rollouts. The European Union's Packaging and Packaging Waste Regulation requires all e-commerce packs to be reusable or recyclable by 2030, spurring rapid design iterations among fiber specialists. United States brand owners anticipate nationwide EPR passage in at least eight additional states by 2027, integrating fee schedules into total-cost models. These regions continue to pilot high-complexity solutions such as fiber-based active-temperature shippers and cloud-connected track-and-trace labels that feed blockchain verification systems. Lessons learned feed into fast-growing emerging markets, accelerating global convergence toward proven circular-economy frameworks.

- Amcor PLC

- Smurfit Kappa Group PLC

- WestRock Company

- DS Smith PLC

- Sealed Air Corporation

- Mondi PLC

- International Paper Company

- Packman Packaging Private Limited

- Pinnacle Packing Industries LLC

- H.B. Fuller Company

- Ranpak Holdings Corporation

- Pregis LLC

- Stora Enso Oyj

- UPM-Kymmene Corporation

- EcoEnclose LLC

- Krones AG

- Sonoco Products Company

- AptarGroup Inc.

- Huhtamaki Oyj

- Veritiv Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift in consumer preference toward recyclable and eco-friendly materials

- 4.2.2 Explosive growth in e-commerce order volumes and last-mile deliveries

- 4.2.3 Global regulatory bans and eco-taxes on single-use plastics

- 4.2.4 AI-driven smart box right-sizing systems reducing dimensional-weight fees

- 4.2.5 Reusable packaging-as-a-service (PaaS) models gaining retailer adoption

- 4.2.6 Scope-3 carbon reporting forcing brands to demand low-carbon packaging

- 4.3 Market Restraints

- 4.3.1 Supply-chain volatility and fluctuating fiber / polymer input costs

- 4.3.2 Barrier-property limitations of certain bio-based films and coatings

- 4.3.3 Cyber-security risks in connected / track-and-trace packaging data

- 4.3.4 Recycling-infrastructure gaps for multi-layer flexible mailers

- 4.4 Value / Supply-Chain Analysis

- 4.5 Evaluation of Critical Regulatory Framework

- 4.6 Impact Assessment of Key Stakeholders

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Consumers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macro-economic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic

- 5.1.2 Paper and Paperboard

- 5.1.3 Metal

- 5.1.4 Bioplastics

- 5.2 By Packaging Format

- 5.2.1 Corrugated Boxes

- 5.2.2 Mailers and Envelopes

- 5.2.3 Pouches and Bags

- 5.2.4 Protective/Insulative Solutions

- 5.3 By End-User Industry

- 5.3.1 Fashion and Apparel

- 5.3.2 Consumer Electronics

- 5.3.3 Food and Beverage

- 5.3.4 Pharmaceuticals

- 5.3.5 Personal Care and Cosmetics

- 5.4 By Sustainable Attribute

- 5.4.1 Recyclable

- 5.4.2 Compostable

- 5.4.3 Reusable

- 5.4.4 Biodegradable

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Smurfit Kappa Group PLC

- 6.4.3 WestRock Company

- 6.4.4 DS Smith PLC

- 6.4.5 Sealed Air Corporation

- 6.4.6 Mondi PLC

- 6.4.7 International Paper Company

- 6.4.8 Packman Packaging Private Limited

- 6.4.9 Pinnacle Packing Industries LLC

- 6.4.10 H.B. Fuller Company

- 6.4.11 Ranpak Holdings Corporation

- 6.4.12 Pregis LLC

- 6.4.13 Stora Enso Oyj

- 6.4.14 UPM-Kymmene Corporation

- 6.4.15 EcoEnclose LLC

- 6.4.16 Krones AG

- 6.4.17 Sonoco Products Company

- 6.4.18 AptarGroup Inc.

- 6.4.19 Huhtamaki Oyj

- 6.4.20 Veritiv Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-need Assessment