|

시장보고서

상품코드

2044288

유럽의 전자기기 제조 서비스 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Europe Electronic Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

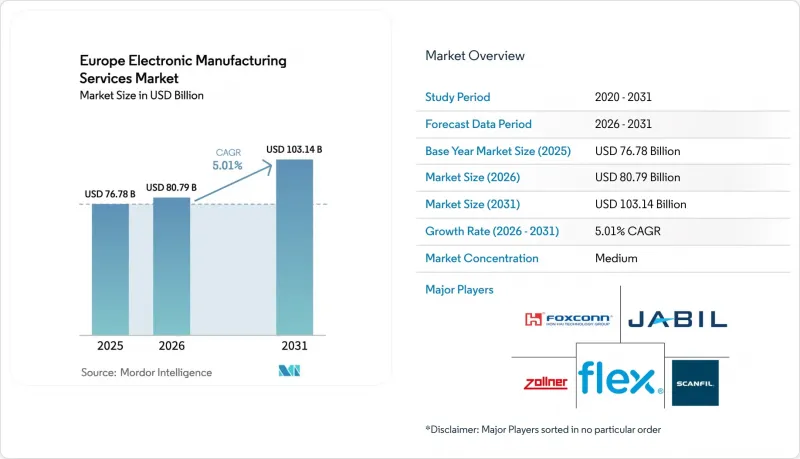

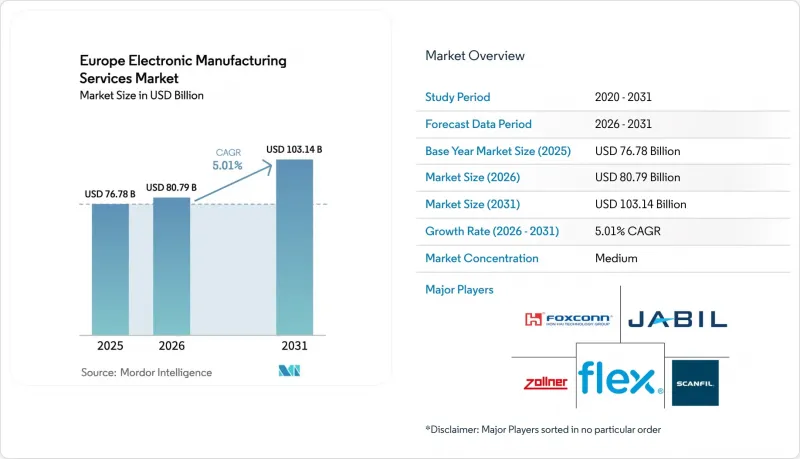

유럽의 전자기기 제조 서비스(EMS) 시장 규모는 2025년에 767억 8,000만 달러, 2026년에 807억 9,000만 달러가 되어, 2031년까지 1,031억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년까지 CAGR 5.01%로 성장할 전망입니다.

유럽 전자기기 제조 서비스 시장의 모멘텀은 공급망 투명성을 우선시하는 규제, 자동차, 산업, 의료 부문의 현지 생산 능력에 대한 수요 증가, 다품종 소량 생산 프로그램의 아시아에서 규제에 부합하는 유럽 공장으로의 지속적인 이전으로 인한 것입니다. ISO 14001을 준수하고 CSRD(Corporate Sustainability Reporting Directive)에 대한 대응을 증명할 수 있는 수탁 제조업체는 다년간의 프레임워크 계약을 체결하는 반면, 탄소 회계 시스템을 갖추지 못한 업체는 추적 가능한 저배출 어셈블리를 제공하는 경쟁업체에 밀려 수주를 잃게 됩니다. 경쟁사에게 수주를 빼앗기고 있습니다. 니어쇼어링을 통해 프로토타입 개발 주기도 8주에서 3주로 단축할 수 있습니다. 이는 설계 반복을 빠르게 하고, 운송비를 절감하여 높은 인건비를 상쇄하는 장점이 있습니다. 자동화, 협동로봇, AI를 활용한 광학 검사로 직접 인건비는 지속적으로 감소하고 있으며, 복잡한 조립품의 아시아 지역과의 비용 차이는 5년 전 40%에서 약 20%로 줄어들고 있습니다.

유럽 전자기기 제조 서비스 시장 동향과 인사이트

유럽 OEM의 전자제품 생산 아웃소싱 확대

OEM 업체들은 자체 생산 라인에서 소프트웨어 및 전동화 부문으로 자본을 이동하고 있으며, 복잡한 기판 실장 및 인클로저 조립을 이미 ISO 13485 및 IPC 표준을 충족하는 수탁 파트너에게 위탁하고 있습니다. 지멘스의 2025년 암베르크 PCB 사업 매각과 Bosch와 Zorner와의 협력 강화는 이러한 전환을 상징하는 사례이며, 이를 통해 제조업체는 표면 실장 라인과 리플로우 오븐에 묶여있던 자금을 확보할 수 있게 됩니다. 유럽의 아웃소싱 보급률은 2025년 38%에 달했지만 여전히 아시아에 미치지 못하고 있어 유럽 전자기기 제조 서비스 시장에는 더 많은 자체 공장을 아웃소싱으로 전환할 수 있는 여지가 있음을 시사합니다. 엔지니어링과 제조를 한 곳에서 수행할 수 있는 업체는 프로토타입에서 파일럿 생산으로 변경을 1주일 이내에 완료할 수 있으며, 이는 자체 공장에서는 거의 불가능한 사이클입니다. 이러한 추세는 컴플라이언스 및 변경 관리의 부담이 전문 EMS 파트너에게 유리하게 작용하는 의료 및 산업 프로그램에서 가장 두드러지게 나타납니다.

자동차 전장 수요 급증

각 배터리 전기차에는 기존 내연기관차 대비 3배에서 5배의 PCB 면적이 내장되어 있으며, 유럽 레벨3 자율주행 기능의 법적 승인에 따라 LiDAR, 레이더, 고성능 도메인 컨트롤러가 추가되었습니다. Volkswagen PowerCo와 Kontron의 BMS 공동 개발 및 48볼트 아키텍처의 광범위한 채택으로 실리콘 카바이드(SiC) 및 질화갈륨(GaN) 모듈에 대한 수요가 증가하고 있습니다. 자동차 등급의 열 사이클 하에서 플립칩과 와이어 본딩 조립 기술을 습득한 EMS 거점은 고수익률의 제품과 장기 계약을 체결하고 있습니다. Tier 1 공급업체들이 소프트웨어 정의 차량을 추진하면서 18개월마다 하드웨어를 개선하기 위해 EMS 파트너에게 의존하고 있습니다. 이러한 추세에 힘입어 2031년까지 유럽 전자기기 제조 서비스 시장에서 자동차 부문이 가장 빠르게 성장하는 부문이 될 것으로 예측됩니다.

아시아에 비해 높은 유럽의 인건비와 에너지 비용

독일의 풀로드 인건비는 시간당 평균 35유로(39.6달러)인 반면, 베트남은 4유로(4.5달러)입니다. 이 격차는 로봇 기술로 부분적으로만 메워지고 있습니다. 2025년 독일의 산업용 전력 요금은 1kWh당 0.18유로(0.20달러)로 중국 요금의 2배 이상이며, 웨이브 납땜 및 셀렉티브 솔더링 라인의 수익률을 압박하고 있습니다. 자동화로 인해 직접 노동시간은 25% 감소했지만, 로봇과 검사 카메라의 상각비로 인해 간접비용은 여전히 높은 수준에서 유지되고 있습니다. 배터리 규제 대상인 BMS 모듈 등 유럽에서 생산이 필수인 제품은 비싼 비용을 흡수할 수 있지만, 가격에 민감한 민수용 기기는 그렇지 못합니다. 이러한 불균형은 에너지 가격의 수렴과 보다 적극적인 자동화가 진행되기 전까지는 유럽 전자기기 제조 서비스 시장의 CAGR을 제한하고 있습니다.

부문 분석

2025년 기준 유럽 전자기기 제조 서비스 시장에서 PCB 조립 시장 규모는 매출의 41.22%를 차지했지만, OEM 업체들이 인클로저 통합, 케이블 하네스, 기능 테스트 벤치를 아웃소싱함에 따라 2031년까지 연평균 복합 성장률(CAGR) 6.11%를 나타낼 것으로 예측됩니다. 기록할 것으로 예측됩니다. 이 전환을 통해 OEM은 클린룸과 항온항습실에 묶여 있던 자금을 확보할 수 있으며, 컴플라이언스 감사에 투입되는 인력을 줄일 수 있습니다. EMS 제공업체들은 펌웨어 쓰기 및 인서킷 검증을 번들로 제공함으로써 추가 수익을 확보하고, 납기 지연에 대한 위약금 조항을 포함한 다년 계약으로 고객을 포섭하고 있습니다.

산업 및 의료용 프로그램이 이러한 급격한 증가를 주도하고 있습니다. 그 이유는 제품의 수명주기가 10년 이상에 달하고, 설계 변경 통지가 조립 공정의 깊숙한 곳까지 파급되는 경우가 많기 때문입니다. 독일과 스위스의 설계 센터 근처에 위치한 박스빌드 공장은 며칠 만에 설계 피드백 루프를 완료하고, 재작업이 필요한 서브 어셈블리의 항공 운송을 피함으로써 인건비 상승에 따른 영향을 줄일 수 있습니다. 유럽의 전자기기 제조 서비스 시장은 공급망 조정 소프트웨어의 통합으로 더욱 탄력을 받고 있습니다. 이 소프트웨어는 실시간 부품 재고 상황을 스케줄링에 반영하여 소량 생산의 분할 로트 키트화 및 병렬 엔지니어링을 가능하게 합니다. 그 결과, ODM 스타일의 엔지니어링 서비스도 동시에 확대되고 있으며, EMS 기업들은 규제 당국의 승인에 영향을 미칠 수 있는 재설계 주기 없이 제조성을 고려하여 기판 레이아웃을 미세 조정할 수 있게 되었습니다.

2025년 유럽 전자기기 제조 서비스 시장에서 위탁생산은 63.71%의 점유율을 차지했습니다. 이는 OEM이 부품을 소유하고 EMS 기업이 인건비를 청구하는 고착화된 위탁 모델을 반영한 것입니다. 그러나 CAGR 5.67%로 예측되는 하이브리드 계약과 턴키 계약은 EMS 벤더에게 부품 조달, 노후화, 추적성에 대한 책임을 부여함으로써 책임의 틀을 재구성하고 있습니다. 중소형 OEM이 이 모델을 채택하는 이유는 Arrow와 Avnet과 같은 유통업체의 대량 구매력을 활용할 수 있기 때문에 2024-2025년 동안 두드러졌던 공급 부족의 영향을 받지 않을 수 있기 때문입니다.

또한, 턴키 계약을 통해 EMS 기업은 OEM의 설계 변경 지시를 기다릴 필요 없이 즉시 핀 호환 대체품을 교체할 수 있어 생산 중단을 방지할 수 있습니다. 재무구조가 탄탄한 업체들은 6개월치 안전재고를 확보하고 있지만, 이는 틈새 시장 진입업체들이 접근하기 어려운 전략입니다. 그 결과 규모의 경제가 축적되어 설계, 조달, 조립을 단일 ERP 기반 내에 통합한 콘트론의 카텍 인수에서 볼 수 있듯이 산업 재편이 진행되고 있습니다. 따라서 유럽 EMS 시장에서는 중요한 의료용 자동차 프로젝트에서 적시 납기 기준을 유지하면서 재고 보유 비용을 흡수할 수 있는 사업자들 사이에 집중화가 진행되고 있습니다.

기타 혜택

- 엑셀 형태 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The Europe electronic manufacturing services market size is projected to be USD 76.78 billion in 2025, USD 80.79 billion in 2026, and reach USD 103.14 billion by 2031, growing at a CAGR of 5.01% from 2026 to 2031.

The momentum of the Europe electronics manufacturing services market stems from legislation that prioritizes supply-chain transparency, mounting demand for local capacity in automotive, industrial, and medical verticals, and the ongoing relocation of high-mix, low-volume programs from Asia to compliant European plants. Contract manufacturers that can prove ISO 14001 alignment and Corporate Sustainability Reporting Directive readiness are securing multi-year frameworks, while providers lacking carbon-accounting systems are losing bids to rivals offering traceable, low-emission assembly. Near-shoring also shortens prototype cycles from eight to three weeks, an advantage that offsets labor premiums through faster design iterations and lower freight expense. Automation, collaborative robotics, and AI-driven optical inspection continue to trim direct labor content, narrowing the cost delta with Asia to roughly 20% for complex assemblies, down from 40% five years earlier.

Europe Electronic Manufacturing Services Market Trends and Insights

Rising Outsourcing of Electronics Production by European OEMs

OEMs are channeling capital away from in-house lines toward software and electrification, pushing complex board population and box build into the hands of contract partners that already meet ISO 13485 and IPC standards. Siemens' 2025 divestiture of its Amberg PCB operation and Bosch's deeper collaboration with Zollner typify the transition, allowing manufacturers to release cash tied up in surface-mount lines and reflow ovens. Outsourcing penetration in Europe climbed to 38% in 2025 yet still trails Asia, implying runway for the Europe electronics manufacturing services market to convert additional captive plants. Providers able to co-locate engineering with manufacturing speed revisions from prototype to pilot in under a week, a cycle that captive plants rarely match. The trend is most pronounced in medical and industrial programs, where compliance and revision-control overhead favor specialist EMS partners.

Surge in Automotive Electronics Demand

Each battery electric vehicle embeds three to five times more PCB area than its combustion predecessor, and Europe's legal green-light for Level-3 autonomous functions is adding lidar, radar, and high-compute domain controllers. Volkswagen PowerCo's BMS co-development with Kontron and widespread adoption of 48-volt architectures increase silicon-carbide and gallium-nitride module demand. EMS sites that master flip-chip and wire-bond assembly under automotive-grade thermal cycling secure higher-margin content and long contracts. As Tier-1 suppliers push software-defined vehicles, they rely on EMS partners to iterate hardware every 18 months. This momentum positions automotive as the fastest advancing slice of the Europe electronic manufacturing services market through 2031.

Higher European Labor and Energy Costs vs. Asia

Fully loaded German labor averages EUR 35 per hour (USD 39.6) against EUR 4 in Vietnam (USD 4.5), a gulf only partly bridged by robotics. Industrial power in Germany cost EUR 0.18 per kWh (USD 0.20) during 2025, more than double Chinese rates, eroding margins on wave solder and selective-solder lines. Although automation trimmed direct labor minutes by 25%, amortization of robotics and inspection cameras keeps overhead high. Products that mandate European proximity, such as BMS modules subject to the Battery Regulation, survive the premium, but price-sensitive consumer gear does not. The imbalance caps the upper range of the Europe electronics manufacturing services market CAGR until energy-price convergence or more aggressive automation emerges.

Other drivers and restraints analyzed in the detailed report include:

- Near-Shoring Triggered by Supply-Chain Security Legislation

- CSRD-Driven Demand for Low-Carbon EMS Facilities

- Skilled-Labor Gap in Advanced SMT and Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Europe electronic manufacturing services market size for PCB assembly commanded 41.22% of revenue in 2025, yet electromechanical box build is posting a 6.11% CAGR through 2031 as OEMs outsource enclosure integration, cable harnessing, and functional test benches. The migration frees OEM cash otherwise tied up in clean rooms and climate-controlled chambers, simultaneously reducing headcount dedicated to compliance audits. EMS providers capture additional margin by bundling firmware flashing and in-circuit verification, locking clients into multi-year agreements with penalty clauses for schedule slippage.

Industrial and medical programs fuel the surge because product lifecycles run a decade or more, and engineering change notifications often cascade deep into assembly. Box-build plants located near design centers in Germany and Switzerland complete engineering feedback loops in days, diminishing the impact of labor premiums by avoiding air freight on reworked sub-assemblies. The Europe electronic manufacturing services market gains further momentum as providers embed supply-chain orchestration software that pulls real-time component availability into scheduling, allowing split-lot kitting and concurrent engineering on low-volume runs. In turn, ODM-style engineering services grow alongside, enabling EMS firms to tweak board layouts for manufacturability without incurring redesign cycles that jeopardize regulatory approvals.

Contract manufacturing held a 63.71% share of the Europe electronic manufacturing services market in 2025, reflecting entrenched consignment models where OEMs own parts and EMS firms charge labor fees. However, hybrid and turnkey contracts, projected at a 5.67% CAGR, are resetting liability frameworks by making EMS vendors responsible for component sourcing, obsolescence, and traceability. Smaller OEMs embrace the model because it taps the bulk-buying leverage of distributors like Arrow and Avnet, thereby insulating them from allocation shortages that defined 2024-2025.

Turnkey deals also empower EMS houses to swap pin-compatible alternates instantly, bypassing OEM engineering change orders and preventing production stops. Providers with deep balance sheets underwrite six months of safety stock, a strategy out of reach for niche players. Consequently, scale advantages accumulate, prompting consolidation as evidenced by Kontron's integration of KATEK that merged design, procurement, and assembly inside a single ERP backbone. The Europe EMS market therefore witnesses a progressive concentration among operators capable of absorbing inventory carrying costs while maintaining just-in-time delivery metrics for critical medical and automotive projects.

The Europe Electronic Manufacturing Services Market Report is Segmented by Service Type (Engineering Services, and More), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), and More), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), and More), End-User (Industrial, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Foxconn Technology Group

- Flex Ltd.

- Jabil Inc.

- Zollner Elektronik AG

- GPV Group

- Scanfil Plc

- Videoton Holding

- Kontron AG

- Kitron ASA

- Cicor Group

- HANZA AB

- LACROIX Electronics

- NOTE AB

- Neways Electronics

- BMK Group

- Melecs EWS

- Variosystems AG

- TT Electronics Plc

- INCAP Oy

- Norautron AS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Outsourcing of Electronics Production by European OEMs

- 4.2.2 Surge in Automotive Electronics Demand (EVs, ADAS)

- 4.2.3 Growth of High-Mix, Low-Volume Industrial and Medical Devices

- 4.2.4 EU Battery-Booster Incentives for Local BMS and Power-Electronics

- 4.2.5 Near-shoring Triggered by Supply-Chain Security Legislation

- 4.2.6 CSRD-Driven Demand for Low-Carbon EMS Facilities

- 4.3 Market Restraints

- 4.3.1 Higher European Labour and Energy Costs vs. Asia

- 4.3.2 Ongoing Component Shortages and Inventory Risk

- 4.3.3 Skilled-Labour Gap in Advanced SMT and Automation

- 4.3.4 Fragmented EU Compliance Burden for Smaller EMS Firms

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Electronic Manufacturing Services

- 5.1.1.1 PCB Assembly

- 5.1.1.2 Electromechanical Assembly/Box Build

- 5.1.1.3 Prototyping

- 5.1.1.4 Other Electronic Manufacturing Services

- 5.1.2 Engineering Services

- 5.1.3 Test and Development Implementation Services

- 5.1.4 Logistics Services

- 5.1.5 Other Service Types

- 5.1.1 Electronic Manufacturing Services

- 5.2 By Business Model

- 5.2.1 Contract Manufacturing (CM)

- 5.2.2 Original Design Manufacturing (ODM)

- 5.2.3 Hybrid / Turnkey / Other Business Models

- 5.3 By Manufacturing Process

- 5.3.1 Surface Mount Technology (SMT)

- 5.3.2 Through-Hole Technology (THT)

- 5.3.3 Advanced Packaging / Hybrid Processes

- 5.4 By End-user

- 5.4.1 Mobile Devices (Smartphones and Tablets)

- 5.4.2 Consumer Electronics

- 5.4.3 Computer (PCs/Desktop/Laptops)

- 5.4.4 Industrial

- 5.4.5 Automotive

- 5.4.6 Communication

- 5.4.7 Lighting

- 5.4.8 Medical

- 5.4.9 Other End-users

- 5.5 By Geography

- 5.5.1 Europe

- 5.5.1.1 Germany

- 5.5.1.2 United Kingdom

- 5.5.1.3 Rest of Europe

- 5.5.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Foxconn Technology Group

- 6.4.2 Flex Ltd.

- 6.4.3 Jabil Inc.

- 6.4.4 Zollner Elektronik AG

- 6.4.5 GPV Group

- 6.4.6 Scanfil Plc

- 6.4.7 Videoton Holding

- 6.4.8 Kontron AG

- 6.4.9 Kitron ASA

- 6.4.10 Cicor Group

- 6.4.11 HANZA AB

- 6.4.12 LACROIX Electronics

- 6.4.13 NOTE AB

- 6.4.14 Neways Electronics

- 6.4.15 BMK Group

- 6.4.16 Melecs EWS

- 6.4.17 Variosystems AG

- 6.4.18 TT Electronics Plc

- 6.4.19 INCAP Oy

- 6.4.20 Norautron AS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment