|

시장보고서

상품코드

2060415

털세포 백혈병 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Hairy Cell Leukemia - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

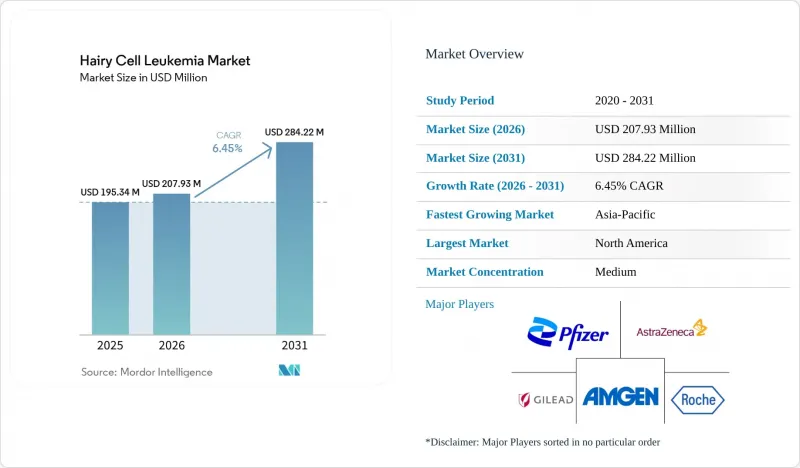

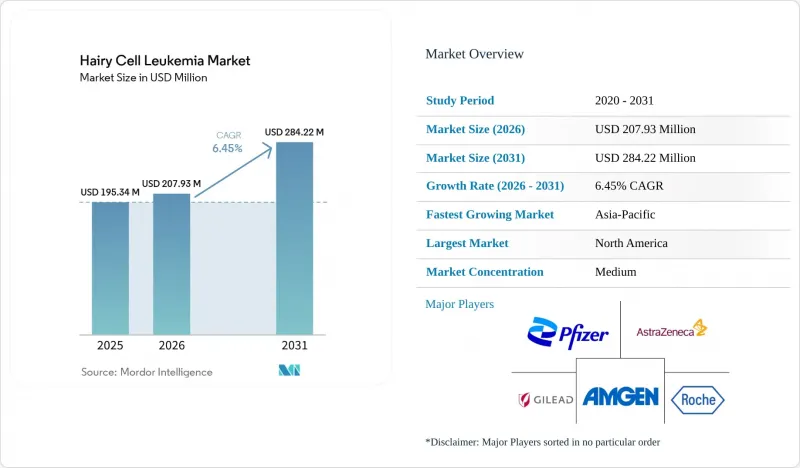

Mordor Intelligence에 의하면, 털세포 백혈병 시장 규모는 2025년에 1억 9,534만 달러로 평가되었습니다. 2026년 2억 793만 달러에서 2031년까지 2억 8,422만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.45%를 나타낼 전망입니다.

본 보고서는 제품 유형(진단제 유형별, 치료제 유형별), 투여 경로(경구, 정맥 내, 피하), 치료 설정(1차 선택, 재발·난치성), 최종 사용자(병원, 전문 암 센터 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 털세포 백혈병 시장 동향 및 인사이트

MRD에 기반한 재치료가 점차 보편화되고 있습니다.

0.01% 미만의 BRAF V600E 알레르 빈도를 검출할 수 있는 골수 MRD 검사는 구제 치료의 시행 시기를 결정하는 데 있어 점점 더 중요한 역할을 하고 있습니다. 이러한 발전 덕분에 범혈구감소증 환자의 감염 관련 합병증이 줄어들었고, 치료 비용도 절감되고 있습니다. 메모리얼 슬론 케터링 암 센터의 2상 임상시험 프로토콜이 6개월 시점의 MRD 평가를 필수 요건으로 규정함에 따라, 이러한 추세가 가속화되고 있습니다. 표적 치료를 통한 조기 개입으로 입원 횟수가 최소화되고 있습니다. 그러나 MRD의 기준치가 표준화되어 있지 않아, 보험사 측의 요건과의 일관성 측면에서 문제가 발생하고 있습니다. 2025년 하반기에 발표된 지침 초안은 평가 지표의 표준화에 기여할 가능성이 있지만, 보험 급여 여부는 여전히 각국의 의료기술평가 결과에 따라 결정될 것입니다.

BRAF V600E 돌연변이에 대한 동반 진단이 주목받고 있습니다.

전형적인 사례의 95% 이상이 BRAF V600E 돌연변이와 관련되어 있으므로, 베무라페닙을 처방하기 전에 이 돌연변이를 확인하는 것이 필수적입니다. 고처리량 유동 분석법 개발을 위한 최근의 제휴 사례에서 알 수 있듯이, 업계는 다중 검사와 임상 현장에서 즉시 활용 가능한 검사로 전환되고 있습니다. 이러한 진단약의 분류가 클래스 III에서 클래스 II로 변경되는 등 규제상의 변경으로 인해, 시장 출시까지의 기간이 단축될 것으로 예측됩니다. 그러나 분석적 타당성 확인 요건이 강화됨에 따라 개발 비용이 증가할 가능성이 있습니다. 유럽에서는 IVDR(체외진단용 의료기기 규정)의 시행이 2029년까지 연기됨에 따라 양극화된 시장이 형성되고 있습니다. 미국에서는 검사실이 MRD(미세 잔류 병변) 플랫폼 개발을 추진하는 한편, 유럽의 많은 기관에서는 규정을 준수하는 키트가 출시되기를 기다리고 있는 상황입니다.

환자 수가 적어 발생하는 임상시험의 경제적 제약

세계 환자 수가 불과 1만 5,000-2만 명에 불과하기 때문에 피험자 80명 규모의 2상 임상시험조차 피험자 모집에 3년이 소요됩니다. 여러 기관에서 진행되는 활성화 비용과 중앙 집중식으로 관리되는 MRD 검사 때문에 환자 1인당 비용은 4만 5,000달러를 초과하며, 이는 일반적인 종양학 임상시험 비용의 2배에 달할 전망입니다. 규제 당국은 단일군 설계를 허용하고 있지만, 유럽의 보험사들이 무작위 대조군이 없는 데이터를 종종 기각하기 때문에 시장 진출까지의 기간이 지연되고 있습니다.

부문별 분석

2025년에는 치료제가 매출의 62.34%를 차지했으며, 털세포 백혈병 시장이 클라드리빈, 펜토스타틴, 리툭시맙 및 새롭게 등장한 BRAF 억제제 요법에 의존하고 있음이 드러났습니다. MRD 검사가 표준화됨에 따라 진단약 시장은 연평균 성장률(CAGR) 7.79%로 확대되고 있으며, 4색 유세포 분석 패널에서 민감도 임계값 0.01%의 고매개변수 분광 세포 계수법으로 진화하고 있습니다. 털세포 백혈병 분야의 첨단 진단제 시장은 의약품 매출보다 더 빠르게 성장하고 있지만, 그 기반은 더 작은 규모에서 시작되었습니다.

스펙트럼 분석기와 차세대 염기서열 분석법을 결합함으로써, BRAF V600E 돌연변이를 알레르 특이적 PCR을 통해 돌연변이 알레르 빈도 0.001%의 민감도로 확인할 수 있게 되어, 임상의는 구제 요법의 시작 시기를 정확하게 판단할 수 있게 됩니다. 그러나 이 워크플로우의 도입 현황은 국가마다 차이가 있었으며, 2025년 시점에서 EU 회원국 28개국 중 분자 검사에 대해 보험 적용을 시행하고 있는 국가는 11개국에 불과했습니다. 그럼에도 불구하고, 이러한 격차를 해소하기 위해 중앙 검사실은 규모를 확대되고 있습니다. MRD에 관한 통일 지침의 제정이 코앞으로 다가온 가운데, 진단 기술은 모발세포 백혈병의 향후 시장 점유율을 결정하는 데 중요한 역할을 할 것으로 보입니다.

2025년에는 지역 의료 현장에서 널리 보급된 클라드리빈 및 리툭시맙의 확립된 프로토콜에 힘입어, 정맥 내 투여가 지출의 51.43%를 차지했습니다. 그러나 경구용 베무라페닙은 연평균 성장률(CAGR) 7.96%를 나타낼 것으로 예측되며, 털세포 백혈병 시장에서 경구용 제제 부문의 점유율을 점차 높여갈 것으로 보입니다. 클라드리빈의 2시간 정맥 주입은 5일간의 지속 정맥 주입에 비해 호중구 감소증의 위험을 낮출 뿐만 아니라, 수익성이 더 높은 생물학적 제제를 위한 주입 의자의 가동률을 최적화함으로써 미국 내 정맥 주입 과정의 혁신을 가속화하고 있습니다.

유럽에서는 더 장기간의 정맥 주사 투여를 권장하는 보험 급여 코드의 영향으로 도입이 지연되고 있지만, 입원 기간 단축을 요구하는 압력은 커지고 있습니다. 2025년에는 투여 경로의 8%를 차지하는 피하 투여용 리툭시맙이, 병원들이 점적 의자의 가동 효율 향상을 목표로 하는 가운데 증가했습니다. 경구 요법이 정맥 내 투여의 우월성에 도전하고 있는 상황이지만, 릿룩시맙 병용 요법에 대한 지속적인 수요로 인해 당분간은 정맥 내 투여의 확고한 입지가 유지될 것으로 보입니다.

지역별 분석

2025년, 북미는 매출의 39.34%를 차지했습니다. 이는 클라드리빈, 리툭시맙, 그리고 NCCN에 등재된 비승인 용도의 베무라페닙에 대한 메디케어의 보험 지급이 주도한 결과입니다. 이러한 요인들이 복합적으로 작용하여 해당 지역의 모발세포 백혈병 시장을 지탱하고 있습니다. 미국은 학술 기관의 강력한 입지뿐만 아니라, 2025년부터 FDA가 시행하는 희귀질환 치료제 수수료 면제 혜택까지 누리고 있으며, 이는 소규모 후원사들에게 큰 도움이 됩니다. 한편, 캐나다는 캐나다 보건부가 명확한 적응증을 요구하고 있기 때문에 미국보다 12-18개월 뒤처져 있습니다. 또한, 주 정부의 처방약 목록에 따라 비용 대비 효과 심사가 완료될 때까지 접근이 제한됩니다.

유럽의 32%라는 시장 점유율은 지역 간 격차를 반영하고 있습니다. 독일은 180일간의 희귀질환 의약품 자동 보험급여 규정을 마련하고 있으며, 이 지역의 매출의 28%를 차지하고 있습니다. 반면, 중동부 유럽에서는 국내 승인 절차에 24개월이 넘는 지연이 발생하고 있습니다. 2025년 EU 공동 임상 평가는 증거 기준의 표준화를 목표로 하고 있지만, 가격 및 수량 계약 협상은 여전히 각국의 관할 하에 있습니다. 털세포 백혈병 시장은 안정적인 성장 잠재력을 보이고 있으나, 폴란드와 불가리아에서 MRD(미세 잔류 병변) 치료에 대한 보험 급여 지연이 단기적인 성장을 저해할 가능성이 있습니다.

아시아태평양은 연평균 성장률(CAGR) 8.25%로 성장을 지속하고, 있으며, 2026년 3월 한국의 혈액학 분야 보험 적용 확대와 표적 치료에 대한 긍정적인 태도를 보여주는 2025년 중국 국가기본의약품목록(NRDL)의 개정이 성장의 원동력이 되고 있습니다. 일본에서 확립된 희귀질환 치료제(희귀의약품) 체계는 환자들이 더 신속하게 치료제를 이용할 수 있도록 하고 있습니다. 그러나 전문적인 혈액병리학 인프라가 부족한 소규모 아세안 국가들이 이 지역의 전체 평균치를 끌어내리고 있습니다. 그럼에도 불구하고, 결제 기관의 지속적인 현대화는 2031년까지의 모발세포 백혈병 시장에서 꾸준한 성장세를 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the hairy cell leukemia market size was valued at USD 195.34 million in 2025 and is estimated to grow from USD 207.93 million in 2026 to reach USD 284.22 million by 2031, at a CAGR of 6.45% during the forecast period (2026-2031).

This report is Segmented by Product Type (Diagnostic and Therapy Type), Route of Administration (Oral, Intravenous, Subcutaneous), Treatment Setting (First-Line, Relapsed/Refractory), End User (Hospitals, Specialty Cancer Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

Global Hairy Cell Leukemia Market Trends and Insights

MRD-Guided Retreatment Gains Traction

Bone-marrow MRD assays, capable of detecting BRAF V600E allele frequencies below 0.01%, are increasingly influencing the timing of salvage treatments. This advancement is reducing infection-related complications and lowering costs for pancytopenic patients. The adoption of Memorial Sloan Kettering's Phase 2 protocol, which requires MRD assessment at six months, has accelerated this trend. Early intervention with targeted therapies is minimizing hospitalizations. However, the absence of standardized MRD cut-offs presents challenges in aligning with payer requirements. Draft guidance expected in late 2025 may help standardize endpoints, but reimbursement will remain contingent on national health-technology assessments.

Companion Diagnostics for BRAF V600E Mutation Take Center Stage

With over 95% of classic cases linked to the BRAF V600E mutation, confirming this alteration is essential before prescribing vemurafenib. The industry is shifting toward multiplex, clinic-ready testing, as demonstrated by recent partnerships to develop high-throughput flow assays. Regulatory changes, such as the reclassification of these diagnostics from Class III to Class II, are expected to shorten pre-market timelines. However, stricter analytical validation requirements are likely to increase development costs. In Europe, delays in IVDR enforcement until 2029 are creating a two-speed market, where U.S. laboratories are advancing MRD platforms while many European facilities await regulatory-compliant kits.

Small Patient Pool Limits Trial Economics

With a global prevalence of only 15,000 to 20,000 cases, even 80-patient Phase 2 studies require three years for enrollment. Per-patient costs exceed USD 45,000, double that of standard oncology trials, due to multi-center activation fees and centralized MRD testing. While regulators permit single-arm designs, European payers often reject data without randomized comparators, delaying market access timelines.

Other drivers and restraints analyzed in the detailed report include:

- Ageing Male Demographic Sees Rising Incidence

- Outpatient IV Push Formulations on the Rise

- High Relapse Rates With Purine-Analog Re-Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, therapy-type products accounted for 62.34% of the revenue, highlighting the Hairy cell leukemia market's reliance on cladribine, pentostatin, rituximab, and emerging BRAF-inhibitor regimens. As MRD testing becomes standard, diagnostics are growing at a 7.79% CAGR, evolving from four-color flow panels to high-parameter spectral cytometry with a 0.01% sensitivity threshold. While the market for advanced diagnostics in Hairy cell leukemia is expanding more rapidly than drug revenue, it is starting from a smaller base.

Spectral instruments, combined with next-generation sequencing, allow for allele-specific PCR confirmation of BRAF V600E at a 0.001% variant-allele frequency, enabling clinicians to time salvage therapy accurately. However, the adoption of this workflow is inconsistent; by 2025, only 11 out of 28 EU countries reimbursed molecular tests. Yet, centralized reference labs are growing to bridge this gap. With unified MRD guidance on the horizon, diagnostics are poised to play a significant role in shaping the future market share of Hairy cell leukemia.

In 2025, intravenous delivery accounted for 51.43% of spending, supported by established cladribine and rituximab protocols prevalent in community practice. However, oral vemurafenib is projected to expand at a 7.96% CAGR, gradually increasing the oral segment's share in the Hairy cell leukemia market. A two-hour IV push of cladribine reduces neutropenia risk compared to a five-day continuous infusion, also optimizing infusion chair usage for more profitable biologics, thus accelerating IV process innovation in the U.S.

While European adoption lags due to reimbursement codes favoring longer infusions, there is growing pressure to reduce inpatient stays. Subcutaneous rituximab, making up 8% of administration routes in 2025, could see an uptick as hospitals aim for better chair-time efficiency. Although oral therapies are challenging the IV's dominance, the ongoing need for combination rituximab infusions ensures IV's stronghold for the foreseeable future.

Geography Analysis

In 2025, North America accounted for 39.34% of the revenue, driven by Medicare's reimbursement for cladribine, rituximab, and the NCCN-listed off-label vemurafenib. These factors collectively support the Hairy Cell Leukemia market in the region. The U.S. benefits from a strong presence of academic institutions and the 2025 FDA orphan-drug fee waiver, which provides significant support to smaller sponsors. Meanwhile, Canada lags 12-18 months behind the U.S. due to Health Canada's requirement for explicit indications. Additionally, provincial formularies restrict access until cost-effectiveness reviews are completed.

Europe's 32% market share reflects regional disparities. Germany, with its 180-day automatic orphan-drug reimbursement rule, secures 28% of the region's sales. In contrast, Central and Eastern Europe face delays exceeding 24 months for national approvals. While the 2025 EU Joint Clinical Assessment aims to standardize evidentiary benchmarks, the negotiation of price-volume agreements remains under state jurisdiction. Although the Hairy Cell Leukemia market demonstrates stable potential, delayed MRD reimbursements in Poland and Bulgaria could hinder short-term growth.

Asia-Pacific, with an 8.25% CAGR, is fueled by South Korea's hematology reimbursement expansion in March 2026 and China's 2025 NRDL update, which signals a favorable stance towards targeted therapies. Japan's established orphan-drug framework facilitates quicker access. However, smaller ASEAN countries, lacking specialized hematopathology infrastructure, dampen the region's overall averages. Despite this, ongoing modernization among payers indicates a consistent growth trajectory for the Hairy Cell Leukemia market through 2031.

- Abbvie

- Adaptive Biotechnologies Corp.

- ADC Therapeutics

- Amgen

- AstraZeneca

- BeiGene

- Bristol-Myers Squibb

- Roche

- Genmab

- Gilead Sciences

- Innate Pharma SA

- Johnson & Johnson

- Merck

- Merck

- Novartis

- Pfizer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Burden of Leukemia Cases & Higher Diagnosis Rates

- 4.2.2 Rising Geriatric Population

- 4.2.3 Rapid Uptake of Next-Generation Targeted Therapies

- 4.2.4 MRD-Guided Retreatment Algorithms

- 4.2.5 Home-Based Sub-Cutaneous Cladribine Protocols

- 4.2.6 Support of Regulatory Authorities

- 4.3 Market Restraints

- 4.3.1 Limited Awareness & Specialist Access in Rural Areas

- 4.3.2 High Cost of Novel Targeted Agents

- 4.3.3 Orphan-Drug Exclusivity Expiries Post-2028

- 4.3.4 Severe Immunosuppression & Infection Risk with Purine Analogues

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Therapy Type

- 5.1.1 Chemotherapy (purine analogues)

- 5.1.2 Targeted Therapy (BRAF, BTK, MEK inhibitors)

- 5.1.3 Immunotherapy (mAbs, immunotoxins)

- 5.1.4 Others (interferon-a, splenectomy)

- 5.2 By Patient Type

- 5.2.1 Classic HCL (cHCL)

- 5.2.2 Variant HCL (HCL-V)

- 5.2.3 SDRPL & other HCL-like disorders

- 5.3 By Route of Administration

- 5.3.1 Intravenous Infusion

- 5.3.2 Sub-cutaneous Injection

- 5.3.3 Oral

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Adaptive Biotechnologies Corp.

- 6.3.3 ADC Therapeutics SA

- 6.3.4 Amgen Inc.

- 6.3.5 AstraZeneca plc

- 6.3.6 BeiGene Ltd

- 6.3.7 Bristol-Myers Squibb Co.

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 Genmab A/S

- 6.3.10 Gilead Sciences Inc.

- 6.3.11 Innate Pharma SA

- 6.3.12 Johnson & Johnson (Janssen)

- 6.3.13 Merck & Co., Inc.

- 6.3.14 Merck KGaA

- 6.3.15 Novartis AG

- 6.3.16 Pfizer Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment