|

시장보고서

상품코드

2060418

유럽의 용사 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Europe Thermal Spray - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

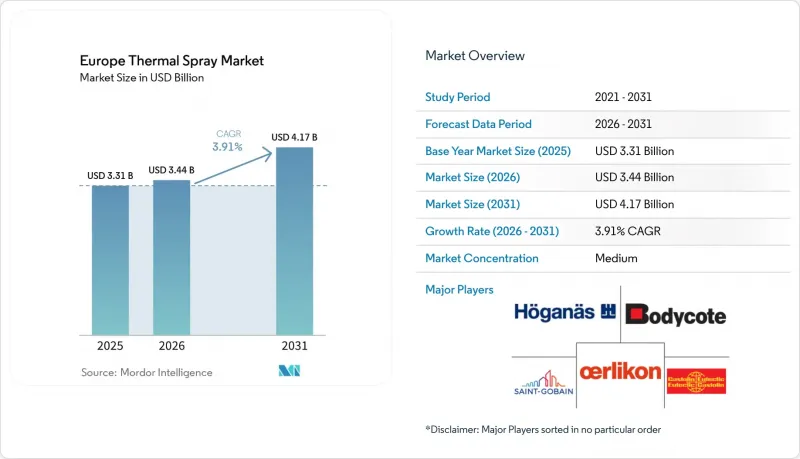

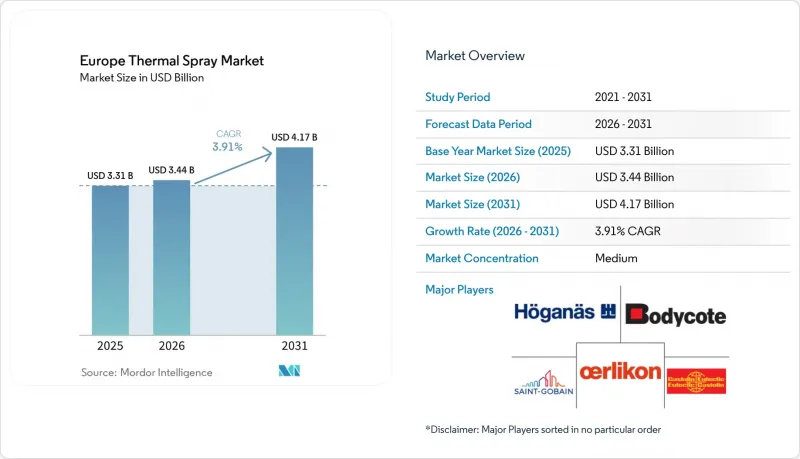

Mordor Intelligence에 의하면, 유럽의 용사 시장 규모는 2025년에 33억 1,000만 달러로 평가되었습니다. 2026년 34억 4,000만 달러에서 2031년까지 41억 7,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 3.91%를 나타낼 전망입니다.

본 보고서는 제품 유형(코팅, 소재, 장비), 공정 유형(연소식·전기 에너지식), 최종 사용자 산업(항공우주, 산업용 가스 터빈, 자동차, 전자기기, 석유 및 가스, 의료기기, 에너지 및 전력, 제철, 섬유, 인쇄·제지), 지역(독일, 영국, 프랑스, 이탈리아 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

유럽의 용사 시장 동향과 인사이트

임플란트용 의료용 등급 Ti·HA 코팅

2030년까지 유럽의 65세 이상 인구가 전체 인구의 3분의 1에 육박할 것으로 예상되는 가운데, 정형외과 및 치과 임플란트 제조업체들은 플라즈마 분사 방식을 이용한 티타늄(Ti) 및 하이드록시아파타이트(HA) 코팅의 적용을 확대되고 있습니다. 이러한 기술 발전 덕분에 회복 기간이 현저히 단축되었으며, 재수술의 필요성도 줄어들고 있습니다. 서스펜션 플라즈마 분사 기술의 발전으로, 현재는 서브미크론 크기의 HA 분말을 정교하게 처리할 수 있게 되었습니다. 이 분말은 천연 골광물과 매우 유사하며, 엄격한 ISO 13779-2 인증 기준을 준수합니다. 임플란트의 내구성과 병원 진료비 지불을 연계하는 제도 개혁으로 인해 수요는 증가하고 있지만, 우려되는 동향도 나타나고 있습니다. 티타늄 분말의 절반 이상이 여전히 북미의 단 두 곳공급업체로부터 조달되고 있어, 공급 측면의 취약성을 가중시키고 있습니다.

터빈 및 보일러에 대한 EU의 탈탄소화 의무

EU의 ‘청정 산업 협정’에 따라, 사업자들은 2030년까지 배출량을 대폭 감축해야 합니다. 이에 대응하기 위해 사업자는 터빈에 가돌리늄 및 란탄-지르코네이트 계열의 열차단 코팅(TBC)을 사후 적용하고 있습니다. 이들은 일정량의 수소 혼합 가스를 견딜 수 있도록 설계되었습니다. 네덜란드의 복합 사이클 발전소에서 실시된 초기 시험 결과, 내구성이 현저히 향상된 것으로 밝혀졌습니다. 또한, 보일러의 고효율화를 중시하는 ‘건축물의 에너지 성능에 관한 지침’에 따라 MCrAlY 본드 코팅의 교체 주기가 단축되고 있습니다.

로봇 통합형 스프레이 셀에 대한 고액의 설비 투자(CAPEX)

소규모 공장의 경우, 충분한 매출로 비용을 분산시킬 수 없기 때문에 자동화 셀이 감당하기 어려울 정도로 비싸다고 느끼는 경우가 종종 있습니다. 리스는 막대한 초기 비용(설비 투자 : CAPEX)을 부담이 덜한 지속적인 비용(운영비 : OPEX)으로 전환하는 해결책이 됩니다. 그러나 이러한 편의성에는 대가가 따릅니다. 사용자는 고가의 소모품에 얽매이게 되고, 이로 인해 이익률이 압박받기 때문입니다. 재무적 위험에 더해, 콜드 스프레이 시스템에서 새로운 HVAF 기술로의 전환이 불과 수년이라는 짧은 기간 내에 이루어짐에 따라, 급속한 노후화 위험이 더욱 높아지고 있습니다.

부문별 분석

2025년, 유럽의 용사 시장에서 코팅이 주류를 차지하며 77.13%라는 압도적인 점유율을 확보했습니다. 이러한 우위는 코팅이 소모품이라는 특성과 항공우주 분야의 정기적인 정비 주기를 여실히 보여주고 있습니다. 한편, 기기 부문은 상승세를 보이고 있으며, 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 3.95%의 성장이 예상됩니다. 이러한 예상되는 성장은 각 OEM 업체들이 스프레이 셀의 디지털화와 실시간 진단 기능 통합을 추진하고 있기 때문입니다. 유럽의 용사 시장에서 장비 부문은 엘리콘(Elicon)사의 예측 유지보수 모듈로부터 혜택을 볼 것으로 예측됩니다. 이러한 첨단 모듈은 예비 부품의 자동 발주를 촉진할 뿐만 아니라, 애프터마켓 수익 확대에도 기여합니다. 코팅과 장비의 중간에 위치한 소재 분야는 호가나스사가 최근 ‘Amperit 678’ 및 ‘685’를 도입한 것도 한 요인이 되어 성장세를 보이고 있습니다. 이러한 신소재는 REACH 규정에 따라 추진되고 있는 니켈 및 코발트 사용 감축을 위한 업계의 전환과 부합합니다.

유럽의 용사 부문의 가격 동향에서는 뚜렷한 격차가 나타납니다. 항공우주용 TBC 분말은 고가에 거래되는 반면, 산업용 텅스텐 카바이드 등급의 가격은 비교적 저렴한 임베디드니다. 또한, 집진 시스템과 중량식 피더는 단순한 보조 도구에서 규정 준수에 필수적인 장치로 발전했습니다. 이러한 변화는 주로 서브마이크론 입자의 포집을 중시하는 ISO 45001의 시행에 기인한 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the europe thermal spray market size was valued at USD 3.31 billion in 2025 and is estimated to grow from USD 3.44 billion in 2026 to reach USD 4.17 billion by 2031, at a CAGR of 3.91% during the forecast period (2026-2031).

This report is Segmented by Product Type (Coatings, Materials, and Equipment), Process Type (Combustion and Electric Energy), End-User Industry (Aerospace, Industrial Gas Turbines, Automotive, Electronics, Oil and Gas, Medical Devices, Energy and Power, Steel Making, Textile, and Printing and Paper), and Geography (Germany, UK, France, Italy, and More). Market Forecasts are Provided in Value (USD).

Europe Thermal Spray Market Trends and Insights

Medical-Grade Ti and HA Coatings for Implants

With Europe's over-65 population set to reach nearly one-third by 2030, orthopedic and dental implant manufacturers are increasingly adopting plasma-sprayed titanium and hydroxyapatite layers. These advancements are notably shortening healing times and diminishing the necessity for revision surgeries. The evolution of suspension plasma spray now adeptly handles sub-micron HA powders, closely resembling natural bone minerals and adhering to the rigorous ISO 13779-2 certification standards. While reforms tying hospital payments to implant longevity have increased demand, a worrisome trend surfaces: over half of titanium powder is still procured from merely two North American suppliers, amplifying supply vulnerabilities.

EU Decarbonization Mandates for Turbines and Boilers

Operators, under the EU Clean Industrial Deal, face a 2030 deadline for significant emissions reductions. In response, they are retrofitting turbines with gadolinium- and lanthanum-zirconate thermal barrier coatings (TBCs), which are designed to withstand specific volumes of hydrogen blends. Early tests in Dutch combined-cycle plants have highlighted notable durability enhancements. Furthermore, the Energy Performance of Buildings Directive, which emphasizes high boiler efficiency, is accelerating the replacement cycle for MCrAlY bond coats.

High CAPEX of Robot-Integrated Spray Cells

Small shops often find automated cells prohibitively expensive, as they are unable to distribute the costs over sufficient sales. Leasing offers a solution, converting a significant upfront cost (capital expenditure - CAPEX) into a more digestible ongoing expense (operational expenditure - OPEX). However, this convenience comes at a price, as users become tethered to costly consumables, which squeeze their profit margins. Adding to the financial stakes, the swift transition from cold-spray systems to the newer HVAF technology, just a few years apart, amplifies the risks of rapid obsolescence.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of HVOF Ceramic Coatings for EV Rotors

- Surging Demand for Wear-Resistant Coatings in Wind-Turbine Rebuilds

- Supply Tightness of YSZ and Rare-Earth Oxides

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, coatings took center stage in the European thermal spray market, securing a dominant 77.13% share. This dominance highlights the consumable nature of coatings and the aerospace sector's regular overhaul cycles. Meanwhile, the equipment segment is on an upward trajectory, with projections indicating a 3.95% CAGR growth during the forecast period of 2026-2031. This anticipated growth is fueled by OEMs' initiatives to digitize spray cells and integrate real-time diagnostics. The equipment segment of Europe's thermal spray market is set to benefit from Oerlikon's predictive-maintenance modules. These advanced modules not only trigger automatic spare-part orders but also boost aftermarket revenue. Positioned between coatings and equipment, materials are gaining momentum, thanks in part to Hoganas' recent introductions of Amperit 678 and 685. These new materials resonate with the industry's pivot towards reducing nickel and cobalt, a shift driven by REACH mandates.

Price dynamics in the European thermal spray sector showcase a clear disparity. Aerospace TBC powders fetch premium prices, while industrial tungsten-carbide grades are priced more modestly. Additionally, dust-collection systems and gravimetric feeders have evolved from secondary tools to vital compliance instruments. This transformation is primarily attributed to ISO 45001 enforcement, which emphasizes the capture of sub-micron particulates.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Medical-grade Ti and HA coatings for implants

- 4.2.2 EU decarbonisation mandates for turbines and boilers

- 4.2.3 Rapid uptake of HVOF ceramic coatings for EV rotors

- 4.2.4 AI-optimised spray-path algorithms cut scrap

- 4.2.5 Surging demand for wear-resistant coatings in European Union wind-turbine rebuilds

- 4.3 Market Restraints

- 4.3.1 High CAPEX of robot-integrated spray cells

- 4.3.2 Supply tightness of YSZ and rare-earth oxides

- 4.3.3 ESG-driven phase-out of methane fuel in spray booths

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Coatings

- 5.1.2 Materials

- 5.1.2.1 Coating Materials

- 5.1.2.1.1 Powders

- 5.1.2.1.1.1 Ceramics

- 5.1.2.1.1.2 Metals

- 5.1.2.1.1.3 Polymer

- 5.1.2.1.1.4 Other Coating Materials

- 5.1.2.1.1 Powders

- 5.1.2.2 Wires/Rods

- 5.1.2.3 Other Materials

- 5.1.2.1 Coating Materials

- 5.1.3 Thermal-Spray Equipment

- 5.1.3.1 Thermal Spray Coating System

- 5.1.3.2 Dust Collection Equipment

- 5.1.3.3 Spray Gun and Nozzle

- 5.1.3.4 Feeder Equipment

- 5.1.3.5 Spare Parts

- 5.1.3.6 Noise-reducing Enclosure

- 5.1.3.7 Other Thermal Spray Equipment

- 5.2 By Process Type

- 5.2.1 Combustion

- 5.2.2 Electric Energy

- 5.3 By End-user Industry

- 5.3.1 Aerospace

- 5.3.2 Industrial Gas Turbines

- 5.3.3 Automotive

- 5.3.4 Electronics

- 5.3.5 Oil and Gas

- 5.3.6 Medical Devices

- 5.3.7 Energy and Power

- 5.3.8 Steel Making

- 5.3.9 Textile

- 5.3.10 Printing and Paper

- 5.4 By Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 NORDICS Countries

- 5.4.7 Russia

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Thermal Spray Powder Companies

- 6.4.1.1 Air Products and Chemicals, Inc.

- 6.4.1.2 AMETEK

- 6.4.1.3 C&M Technologies GmbH

- 6.4.1.4 CASTOLIN EUTECTIC

- 6.4.1.5 CRS Holdings Inc.

- 6.4.1.6 Diffusion Engineers Limited

- 6.4.1.7 Fujimi Corporation

- 6.4.1.8 Global Tungsten & Powders

- 6.4.1.9 H.C. Starck

- 6.4.1.10 HAI Inc

- 6.4.1.11 Hoganas AB

- 6.4.1.12 Kennametl Stellite

- 6.4.1.13 Linde plc

- 6.4.1.14 Metallisation Limited

- 6.4.1.15 OC Oerlikon Management AG

- 6.4.1.16 Saint-Gobain

- 6.4.1.17 Sandvik AB

- 6.4.1.18 The Fisher Barton Group

- 6.4.1.19 Treibacher Industrie AG

- 6.4.2 Thermal Spray Coating Companies

- 6.4.2.1 APS Materials, Inc.

- 6.4.2.2 ARC International

- 6.4.2.3 Bodycote

- 6.4.2.4 CASTOLIN EUTECTIC

- 6.4.2.5 Chromalloy Gas Turbine LLC

- 6.4.2.6 Fujimi Corporation

- 6.4.2.7 Kennametl Stellite

- 6.4.2.8 Linde plc

- 6.4.2.9 Metallisation Limited

- 6.4.2.10 OC Oerlikon Management AG

- 6.4.2.11 Pamarco

- 6.4.2.12 Surface Dynamics

- 6.4.2.13 The Fisher Barton Group

- 6.4.3 Thermal Spray Equipment Companies

- 6.4.3.1 Air Products and Chemicals, Inc.

- 6.4.3.2 Camfil Air Pollution Control

- 6.4.3.3 CASTOLIN EUTECTIC

- 6.4.3.4 Donaldson Company Inc.

- 6.4.3.5 Flame Spray Technologies BV

- 6.4.3.6 GTV-wear GmbH

- 6.4.3.7 HAI Inc

- 6.4.3.8 Kennametl Stellite

- 6.4.3.9 Kurt J. Lesker Company

- 6.4.3.10 Linde plc

- 6.4.3.11 Metallisation Limited

- 6.4.3.12 OC Oerlikon Management AG

- 6.4.3.13 Saint-Gobain

- 6.4.3.14 The Lincoln Electric Company

- 6.4.1 Thermal Spray Powder Companies

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment