|

시장보고서

상품코드

2061504

아시아태평양의 의학 임상 영양 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Asia-Pacific Medical Clinical Nutrition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

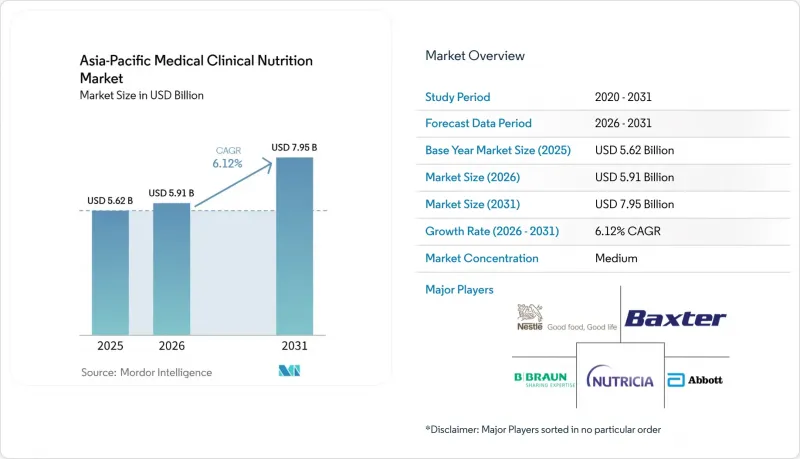

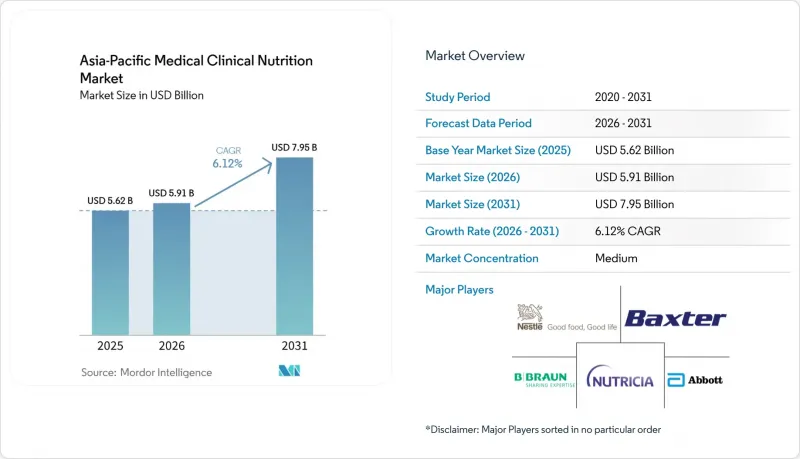

Mordor Intelligence에 의하면, 아시아태평양의 의학 임상 영양 시장 규모는 2025년에 56억 2,000만 달러로 평가되었습니다. 2026년 59억 1,000만 달러에서 2031년까지 79억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.12%를 나타낼 전망입니다.

본 보고서에서는 해당 산업을 투여 경로(경구·경장, 비경구), 용도(영양실조, 대사 장애 등), 연령대(소아, 성인, 고령자), 유통 채널(병원 약국, 소매 약국 등) 및 국가(중국, 일본, 인도 등)별로 분류하고 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 의학 임상 영양 시장 동향과 고찰

대사성 질환 및 만성 질환의 유병률 증가

당뇨병, 신부전, 대사증후군으로 입원한 환자 수는 증가하고 있으며, 해당 지역의 당뇨병 환자 수는 2021년 2억 9,580만 명에서 2045년까지 4억 1,170만 명에 달할 것으로 예측됩니다. 현재 많은 환자가 젊은 연령대에서 발병하고 있으며, 의료용 영양제에 대한 평생 의존 기간이 길어지고 있습니다. 싱가포르가 2024년에 시작한 만성 질환 대책에서는 연속 혈당 모니터링과 영양사가 주도하는 상담을 결합한 노력을 통해 이미 치료 순응도가 개선된 것으로 나타났습니다. 한국에서도 아미노산 정맥주사액이 필요한 대사증후군으로 인한 입원이 마찬가지로 증가하고 있는 것으로 보고되고 있습니다. 그 결과, 분지쇄 아미노산, 오메가-3 지방산, 식이섬유 혼합물을 강화한 영양제가 중환자실에서 기존의 폴리머 계열 제품을 점차 대체하고 있습니다. 예방적 대사 영양 관리 프로토콜을 도입한 병원에서는 입원 일수 단축 및 재입원 비용 절감이 보고되고 있으며, 이에 따라 전문 제품에 대한 보험사의 지원이 강화되고 있습니다.

고령화의 진행

동남아시아에서는 60세 이상 주민의 비율이 2050년까지 22.9%로 두 배로 늘어날 전망입니다. 근감소증, 연하 장애, 다약제 병용으로 인해 고단백·식감 조절형 포뮬러에 대한 수요가 증가하고 있습니다. 일본의 2024년 요양 개혁에서는 상온 보관이 가능한 재택 장내 영양 요법에 대한 자금 지원이 이루어지고 있으며, 이에 따라 지방 현에서 수요가 증가하고 있습니다. 11개국이 ‘건강한 고령화에 관한 콜롬보 선언’에 서명하고, 1차 의료 현장에서 정기적인 영양 검진을 실시하기로 약속했습니다. 중국의 최신 지침에 따르면, 허약한 고령자의 단백질 섭취량을 기존의 1.0g에서 1.2-1.5g/kg으로 늘릴 것을 권장하고 있으며, 이에 따라 1인당 영양제 소비량이 증가하고 있습니다.

아시아태평양의 제각각인 상환 제도

지방 정부의 재택 장내 영양 공급에 대한 지원은 고작 40%에 그치고 있습니다. 본인 부담에 의존할 수밖에 없는 상황이라, 간병인은 믹서로 갈아 만든 식사를 준비할 수밖에 없어 미생물 오염의 위험이 발생하고 있습니다. 태국은 2024년에 상환 한도를 폐지했으나, 여전히 일반 영양제의 비용 중 60%만 보장하고 있으며, 특정 질환용 프리미엄 제품은 보장 대상에서 제외되어 있습니다. 인도의 주요 건강보험 제도에서는 경장영양 및 정맥영양 항목이 보장 대상에서 제외되어 있으며, 그 보급은 연소득 5,000달러 이상의 도시 지역 가구에 한정되어 있습니다. 따라서 각 제조업체는 이중 제품 포트폴리오를 전개하고 있으며, 현금 시장용으로는 1회분당 2달러 미만의 가성비를 중시한 제품 라인을 출시하는 한편, 일본이나 호주의 보험 적용 제도를 대상으로는 프리미엄 면역 영양 제품을 공급하고 있습니다.

부문별 분석

2025년, 아시아태평양의 의학 임상 영양 시장에서 경구 및 경장 영양이 89.52%의 점유율을 차지했습니다. 이는 합리적인 가격과 기능적인 위장관과의 적합성을 반영한 것입니다. 그럼에도 불구하고, 중환자실(ICU) 입원 환자 증가와 오염률을 0.1%로 낮추는 자동 조제 시스템의 보급에 힘입어, 정맥영양제는 연평균 성장률(CAGR) 7.36%로 성장을 지속하고, 있습니다. 2024년 중국에서 시행된 의료기기 승인 제도 개혁에 따라, 국내산 3실 백이 기존보다 1년 빨리 병원에 공급되게 되어 수입 의존도가 낮아졌습니다. 일본과 한국의 병원에서는 수동 조제 방식에서 48시간 이내에 배송되는 프리믹스식 다실 백으로의 전환이 진행되고 있으며, 이를 통해 약제 부서의 업무 부담과 폐기물이 줄어들고 있습니다. 장내 영양 분야의 혁신은 계속되고 있으며, 연하 장애가 있는 고령자의 흡인 위험을 줄여주는 점도 증진된 ‘젤리’ 유형 제품이 등장한 반면, 경구용 면역 영양제는 수술 후 입원 기간을 2.5일 단축시키고 있습니다.

2025년에는 영양실조 관련 제품이 매출의 14.72%를 차지했으나, 암 입원 환자의 40-80%가 영양 결핍 상태에 있는 만큼, 암 환자용 영양제는 연평균 성장률(CAGR) 7.69%로 성장하고 있습니다. 중국 전역에서 실시된 조사에 따르면, 영양실조 상태에 있는 암 환자 중 적절한 치료를 받은 비율은 고작 38%에 그쳐, 치료에 있어 큰 격차가 드러났습니다. 일본에서는 2025년에 3종의 새로운 수술 전후 면역 영양 제품이 승인됨에 따라, 지역 전체에서 전문 제품의 출시가 가속화되고 있습니다. 염증성 장 질환, 만성 신장 질환, 간 질환을 대상으로 한 제제는 꾸준한 수요를 창출하고 있는 반면, 장외영양 단독 요법은 2025년 소아 크론병 코호트에서 60%의 관해율을 달성했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the asia-Pacific medical clinical nutrition market size was valued at USD 5.62 billion in 2025 and is estimated to grow from USD 5.91 billion in 2026 to reach USD 7.95 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031).

This report Segments the Industry Into Route of Administration (Oral and Enteral, Parenteral), Application (Malnutrition, Metabolic Disorders, and More), Age Group (Pediatric, Adult, and Geriatric), Distribution Channel (Hospitals Pharmacies, Retail Pharmacies, and More), and Country (China, Japan, India, and More). Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Medical Clinical Nutrition Market Trends and Insights

Rising Prevalence of Metabolic and Chronic Diseases

Hospital caseloads of diabetes, renal failure, and metabolic syndrome are swelling, with regional diabetes prevalence projected to rise from 295.8 million in 2021 to 411.7 million by 2045. Many patients now present at younger ages, lengthening lifetime dependence on medical nutrition. Singapore's 2024 chronic disease initiative, which combines continuous glucose monitoring with dietitian-led counseling, is already showing improvements in adherence metrics. South Korea has documented a parallel uptick in metabolic syndrome admissions requiring intravenous amino acid solutions. Formulas fortified with branched-chain amino acids, omega-3 fatty acids, and fiber blends are therefore displacing standard polymeric products in critical-care wards. Hospitals that integrate proactive metabolic-nutrition pathways report shorter stays and lower readmission bills, reinforcing payer support for specialized products.

Expanding Geriatric Population

The share of residents aged 60 plus is on track to double to 22.9% by 2050 in Southeast Asia. Sarcopenia, dysphagia, and polypharmacy are boosting the need for hyper-protein, texture-modified formulas. Japan's 2024 long-term care reforms fund home enteral regimens that can be stored at room temperature, thereby increasing demand in rural prefectures. Eleven nations endorsed the Colombo Declaration on Healthy Ageing, pledging routine nutrition screening in primary care. Updated Chinese guidelines now recommend 1.2-1.5 g of protein per kilogram for frail seniors, up from 1.0 g, which raises per-capita formula volumes.

Inconsistent Reimbursement Across APAC

Only 40% of regional governments fund home enteral nutrition. Cash-pay reliance forces caregivers to prepare blenderized feeds that risk microbial contamination. Thailand lifted reimbursement caps in 2024, yet still covers just 60% of standard-formula costs, excluding premium disease-specific variants. India's flagship health insurance plan omits the enteral and parenteral categories, limiting its penetration to urban households with annual incomes above USD 5,000. Manufacturers, therefore, run dual portfolios, releasing value-engineered lines priced below USD 2 per serving for cash markets while reserving premium immunonutrition for reimbursed systems in Japan and Australia.

Other drivers and restraints analyzed in the detailed report include:

- Growing Healthcare Spending and Middle-Income Expansion

- Home-Based Nutrition Uptake Via Smart Pumps and Telehealth

- Low Inventory Appetite in Hospital Pharmacies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oral and Enteral held 89.52% of Asia-Pacific medical clinical nutrition market share in 2025, reflecting affordability and compatibility with functional gastrointestinal tracts. Nevertheless, parenteral formulations are posting a 7.36% CAGR due to rising ICU admissions and the broader use of automated compounding, which reduces contamination to 0.1%. China's 2024 device-approval reforms enabled domestic three-chamber bags to reach hospitals a year faster than before, reducing reliance on imports. Hospitals across Japan and South Korea are transitioning from manual mixing to premixed multi-chamber bags, which are delivered within 48 hours, thereby decreasing pharmacy labor and waste. Enteral innovation continues, with thickened "jelly" formats mitigating aspiration risk in dysphagic elders while oral immunonutrition shortens surgical stays by 2.5 days.

Malnutrition held 14.72 % revenue share in 2025, yet oncology formulas are expanding at 7.69% CAGR as 40%-80% of cancer inpatients present undernourished. China's nationwide audit revealed only 38% of malnourished oncology patients received dedicated intervention, underscoring a sizeable treatment gap. Japan cleared three new perioperative immunonutrition products in 2025, accelerating specialty launches across the region. Formulas targeting inflammatory bowel disease, chronic kidney disease, and liver disorders continue to generate stable demand, while exclusive enteral nutrition achieved a 60% remission rate in pediatric Crohn's cohorts in 2025.

List of Companies Covered in this Report:

- Abbott Laboratories

- Ajinomoto

- B. Braun

- Baxter

- Beckton Dickinson

- Boston Scientific

- Cardinal Health

- Danone

- DSM-Firmenich

- Fresenius

- Hero Nutritionals

- JW Pharmaceutical

- Kate Farms

- Kelun Pharma

- Meiji Holdings

- Nestle Health Science

- Otsuka

- Perrigo

- Reckitt/Mead Johnson

- Vifor Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Metabolic & Chronic Diseases

- 4.2.2 Expanding Geriatric Population

- 4.2.3 Growing Healthcare Spending & Middle Class

- 4.2.4 Home-Based Nutrition Uptake Via Smart Pumps & Telehealth

- 4.2.5 nHEOR Evidence Shaping Reimbursement

- 4.2.6 Regionalization of Premixed PN Manufacturing

- 4.3 Market Restraints

- 4.3.1 Inconsistent Reimbursement Across APAC

- 4.3.2 Low Inventory Appetite in Hospital Pharmacies

- 4.3.3 Counterfeit Products in Emerging ASEAN Markets

- 4.3.4 Shortage of Precision-Nutrition Dietitians

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Route of Administration

- 5.1.1 Oral & Enteral

- 5.1.2 Parenteral

- 5.2 By Application

- 5.2.1 Malnutrition

- 5.2.2 Metabolic Disorders

- 5.2.3 Gastrointestinal Diseases

- 5.2.4 Neurological Diseases

- 5.2.5 Cancer

- 5.2.6 Other Diseases

- 5.3 By Age Group

- 5.3.1 Pediatric

- 5.3.2 Adult

- 5.3.3 Geriatric

- 5.4 By Distribution Channel

- 5.4.1 Hospitals Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Channel

- 5.4.4 Others

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Ajinomoto

- 6.3.3 B. Braun SE

- 6.3.4 Baxter

- 6.3.5 Becton Dickinson

- 6.3.6 Boston Scientific

- 6.3.7 Cardinal Health

- 6.3.8 Danone Nutricia

- 6.3.9 DSM-Firmenich

- 6.3.10 Fresenius Kabi

- 6.3.11 Hero Nutritionals

- 6.3.12 JW Pharmaceutical

- 6.3.13 Kate Farms

- 6.3.14 Kelun Pharma

- 6.3.15 Meiji Holdings

- 6.3.16 Nestle Health Science

- 6.3.17 Otsuka Pharmaceutical

- 6.3.18 Perrigo

- 6.3.19 Reckitt/Mead Johnson

- 6.3.20 Vifor Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment