|

시장보고서

상품코드

2061511

남미의 C암 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America C-Arms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

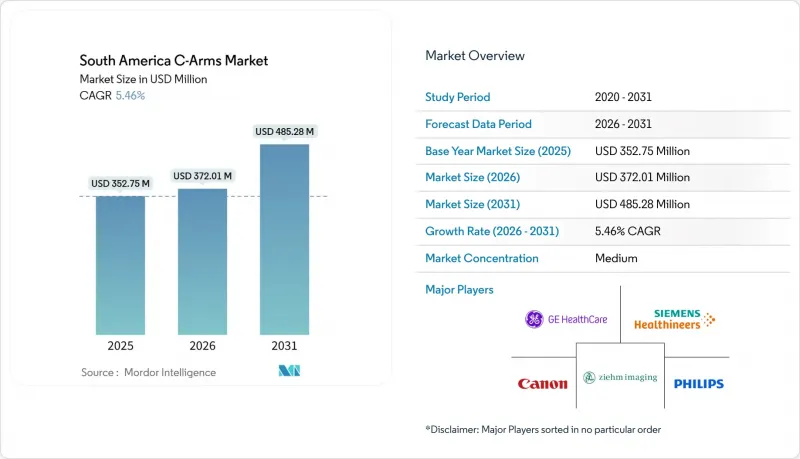

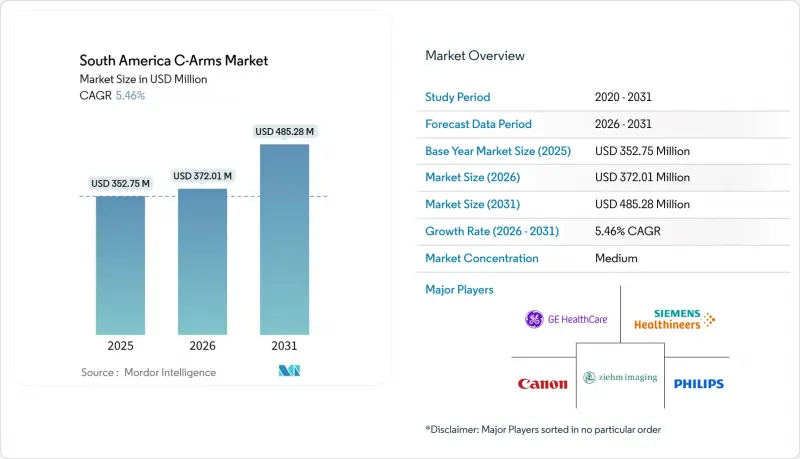

Mordor Intelligence에 의하면, 남미의 C암 시장 규모는 2025년 3억 5,275만 달러로 평가되었고, 2026년에는 3억 7,201만 달러로 추정되고, 2031년까지 4억 8,528만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 5.46%로 성장할 전망입니다.

본 보고서는 기기 유형별(고정식 C암, 이동식 C암), 검출기 기술별(이미지 인텐시파이어, 플랫 패널), 용도별(심장학, 소화기학, 신경학, 정형외과 및 외상, 기타), 최종 사용자별(병원, 외래수술센터(ASC), 전문 클리닉), 지역(브라질, 아르헨티나, 칠레, 콜롬비아, 페루, 기타 남미)에 따라 분류되어 있습니다. 시장 전망은 금액(달러)으로 제시되어 있습니다.

남미 C암 시장 동향과 인사이트

고령화의 진행과 만성 질환으로 인한 부담 증가

콜롬비아에서는 2050년까지 연간 3만 9,270건의 인공관절 치환술이 시행될 것으로 예상되며, 이는 52.7%의 급증에 해당하므로 수술 중 영상 진단 주기의 확대가 필요하게 됩니다. 브라질에서는 2008-2023년 20만 2,940건의 외상성 절단 사례가 기록되었으며, 연간 5,487만 달러의 보상 비용이 발생하고 있어, 고처리량 시스템에 대한 지속적인 설비 투자를 촉진하고 있습니다. 2000-2023년 브라질에서는 60세 이상 인구가 8.7%에서 15.6%로 크게 증가했습니다. 이러한 인구 구조의 변화로 인해 정형외과, 혈관 치료, 종양학 분야에서 영상 유도 시술에 대한 수요가 증가하고 있습니다. 비슷한 고령화 추세와 만성 질환 유병률을 보이는 아르헨티나와 칠레에서도 스텐트 삽입술, 척추체 성형술, 종양 절제술에 있어 투시 검사의 이용이 증가하고 있습니다. 브라질의 대도시권에 위치한 공공 영상진단 시설의 가동률은 70-80%에 달하고 있으며, 그 결과 대기 시간이 길어지면서 보험 가입 환자들은 휴대용 C암을 갖춘 민간 클리닉에서 진료를 받기를 원하고 있습니다. 병상 부족 문제를 해소하고 구식 시스템을 현대화하기 위해 상파울루주와 미나스제라이스주 당국은 외래수술센터(ASC)에 공동으로 투자하고 있습니다. 예산상의 제약이 있음에도 불구하고, 인구 통계학적 수요와 기술적 역량 간의 이러한 불일치가 의료기기에 대한 수요를 지속적으로 뒷받침하고 있습니다.

저침습 및 영상 유도 수술의 보급

보고타에 위치한 지역 연수 거점이 외과 의사들의 숙련도 향상에 기여하고 있어, 남미 전역에서 최소 침습 척추 수술이 확대되고 있습니다. 브라질에서는 영상 유도 장비를 활용한 골고정형 인공와우 수술에서 합병증 발생률이 49% 감소했으며, 수술 시간도 절반으로 단축되었습니다. 로봇 보조 흉부 수술 프로그램에서는 현재 상파울루와 리우데자네이루에 집중된 41대의 다빈치 시스템이 가동 중이며, 이는 로봇 수술과 연동되는 실시간 투시 장치에 대한 병원 측 수요가 있음을 입증하고 있습니다. 수술이 외래 환경으로 전환됨에 따라, 남미의 C암 시장에서는 하이브리드 수술실에 쉽게 설치할 수 있는 콤팩트하고 기동성이 뛰어난 플랫폼이 주목받고 있습니다. 이를 통해 영구적인 인프라 변경 없이 워크플로의 연속성을 보장할 수 있습니다.

높은 도입 및 유지 비용

브라질에서는 수입 의료기기에 20-60%의 관세가 부과되고 있으며, 2024년에 60일간의 납부 유예 기간이 도입된 이후에도 3차 의료기관의 설비 투자 예산은 증가하고 있습니다. 아르헨티나 페소화 가치 하락으로 인한 가격 불확실성이 커지면서, 의료기관들은 선택적인 영상진단 장비 업그레이드보다는 필수 소모품 구매를 우선시할 수밖에 없는 상황입니다. 평면 패널식 C암의 가격은 5만 달러에서 17만 5,000달러에 달하며, 환자 수를 보장할 수 없는 소규모 클리닉에게는 진입 장벽이 되고 있습니다. 칠레에서는 민간 보험 가입자의 정형외과 수술 비율이 공적 보험 가입자의 2.8배에 달하는 등, 의료 접근성 격차가 여전히 존재하여 경제적 격차가 뚜렷이 드러나고 있습니다.

부문별 분석

2025년, 남미 C암 시장의 67.91%를 고정식 시스템이 차지했습니다. 이는 천장 설치로 인한 안정성과 대형 검출기가 필요한 가동률이 높은 외상 센터의 요구에 부응한 것입니다. 그러나 외래 진료 부문에서는 다직종 수술 체계에서 기동성이 중요시되므로, 이동식 플랫폼의 연평균 성장률(CAGR)이 5.82%로 고정식 플랫폼을 상회할 것으로 예측됩니다. 2024년에 출시된 지멘스 헬스인이어스의 자율형 CIARTIC Move는 포지셔닝 설정 시간을 절반으로 단축함으로써, 인력 부족을 겪고 있는 시설에서 이동형 혁신 기술이 지지를 받는 이유를 입증하고 있습니다.

모바일 기기에 콘빔 CT를 도입함으로써 고정식 투시 장치와의 기능 격차가 줄어들었고, 응급도가 낮은 의료 기관에서도 고도의 외상 및 척추 치료 워크플로우를 수행할 수 있게 되었습니다. 브라질과 아르헨티나에서 개조 편의성을 고려한 규제가 정착됨에 따라, 외래 진료 환경에서 사지 손상을 치료하는 정형외과 의사들 사이에서 미니 C암의 도입이 가속화되고 있습니다. 고정형과 이동형 제품 라인 간에 소프트웨어 기능이 지속적으로 상호 융합되면서 카테고리 간의 경계가 모호해지고 있지만, 도입 비용과 수술실 구성은 여전히 설비 투자 예산의 분수령이 되고 있습니다.

2025년 매출의 63.02%를 차지할 것으로 예상되는 평판 패널 검출기 시스템은 연평균 성장률(CAGR) 5.65%로 성장할 것으로 전망됩니다. 이미지 인텐시파이어에서 벗어나는 움직임은 브라질의 2024년 방사선량 추적 규정 및 아르헨티나의 유사한 규정에 의해 촉진되고 있습니다. 양자 효율이 높은 CMOS 평판 패널은 비정질 실리콘 제품에 비해 피폭량을 25-30% 줄여줍니다. 설치 대수의 약 3분의 1을 차지하는 이미지 인텐시파이어 튜브는 교체 부품의 입수 어려움과 개당 18,000-22,000달러에 달하는 높은 비용이라는 과제에 직면해 있습니다. 이러한 요인들로 인해 총 소유 비용 측면에서 볼 때 평판 패널이 비용 대비 효율이 더 높습니다. 또한, 구형 시스템에 대해 최대 30%의 크레딧을 제공하는 트레이드인 프로그램을 통해 평면 패널의 도입이 가속화되고 있습니다. 남미의 공공 의료기관에서는 초기 비용을 절감하기 위한 리스 옵션이 도입되고 있어, C암 분야의 영상 증강 시스템 시장 점유율은 꾸준히 감소할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the south america c-Arms market size is expected to increase from USD 352.75 million in 2025 to USD 372.01 million in 2026 and reach USD 485.28 million by 2031, growing at a CAGR of 5.46% over 2026-2031.

This report is Segmented by Device Type (Fixed C-Arms, Mobile C-Arms), Detector Technology (Image-Intensifier, Flat-Panel), Application (Cardiology, Gastroenterology, Neurology, Orthopedics & Trauma, and More), End User (Hospitals, Ambulatory Surgical Centres, Specialty Clinics), and Geography (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). Market Forecasts are Provided in Value (USD).

South America C-Arms Market Trends and Insights

Rising Geriatric Population and Chronic Disease Burden

Colombia is expected to perform 39,270 arthroplasties annually by 2050, a 52.7% jump that will require more intra-operative imaging cycles. Brazil recorded 202,940 traumatic amputations between 2008 and 2023, costing USD 54.87 million in yearly reimbursements, reinforcing continual capital outlays for high-throughput systems. Between 2000 and 2023, Brazil experienced a significant increase in its population aged 60 and above, rising from 8.7% to 15.6%. This demographic shift has driven higher demand for image-guided procedures in orthopedics, vascular care, and oncology. Argentina and Chile, with similar aging trends and chronic disease prevalence, are also seeing increased utilization of fluoroscopy for stenting, vertebroplasty, and tumor ablation. Public imaging facilities in metropolitan Brazil are operating at 70-80% capacity, resulting in extended wait times and prompting insured patients to seek services at private clinics equipped with mobile C-arms. To address bed shortages and upgrade outdated systems, state authorities in Sao Paulo and Minas Gerais are co-investing in ambulatory surgical centers. Despite budget constraints, this mismatch between demographic needs and technological capabilities continues to sustain demand for medical equipment.

Adoption of Minimally Invasive, Image-Guided Surgeries

Minimally invasive spine procedures are expanding across South America, aided by regional training hubs in Bogota that improve surgeon proficiency. In Brazil, bone-anchored hearing implant operations cut complication rates by 49% and operating times by half. when performed with image-guided tools. Robotic thoracic programs now operate on 41 da Vinci systems concentrated in Sao Paulo and Rio de Janeiro, confirming hospital demand for real-time fluoroscopy that syncs with robotics. As more surgeries migrate to outpatient environments, the South America C Arms market benefits from compact, mobile platforms that dock easily into hybrid ORs, ensuring workflow continuity without permanent infrastructure changes.

High Acquisition and Maintenance Costs

Brazil imposes 20-60% tariffs on imported medical devices, escalating capital budgets for tertiary hospitals even after extended 60-day payment terms were introduced in 2024. Argentine peso devaluation deepens price uncertainty, compelling facilities to prioritize essential consumables over elective imaging upgrades. Flat-panel C-Arms range from USD 50,000 to USD 175,000, deterring smaller clinics that lack volume guarantees. Access inequities persist in Chile, where privately insured patients enjoy 2.8-times greater orthopedic surgery rates than their public counterparts, highlighting the affordability divide.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Flat-Panel and 3D Imaging

- Post-COVID Backlog of Elective Surgeries

- Shortage of Skilled Imaging Technologists and Surgeons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed systems held 67.91% of the South American C-Arms market share in 2025, driven by high-throughput trauma centers that demand ceiling-mounted stability and large detector sizes. Mobile platforms are, however, forecast to outpace at a 5.82% CAGR because outpatient units prize maneuverability for multi-disciplinary theater rosters. Siemens Healthineers' autonomous CIARTIC Move, launched in 2024, reduces position setup time by half, underscoring why mobile innovation resonates at staff-constrained sites.

Implementation of cone-beam CT within mobile footprints is closing the capability gap with fixed fluoroscopy suites, allowing advanced trauma and spinal workflows in lower-acuity facilities. As refurbish-friendly regulations take hold in Brazil and Argentina, mini C-Arm adoption is accelerating among orthopedists treating extremity injuries in ambulatory settings. Continuous cross-pollination of software features across fixed and mobile lines blurs category boundaries, yet installation cost and theater configuration remain the dividing line for capital budgeting.

Flat-panel detector systems, accounting for 63.02% of 2025 sales, are expected to grow at a 5.65% CAGR. The shift from image intensifiers is being driven by 2024 dose-tracking regulations in Brazil and similar mandates in Argentina. CMOS flat panels, with higher quantum efficiency, reduce exposure by 25-30% compared to amorphous-silicon alternatives. Image-intensifier tubes, which still represent about one-third of the installed base, face challenges such as limited availability of replacement parts and high costs ranging from USD 18,000 to 22,000 per tube. These factors make flat panels more cost-effective in terms of total ownership. Furthermore, trade-in programs offering up to 30% credit on legacy systems encourage faster adoption of flat panels. As public networks in South America introduce leasing options to avoid upfront payments, the market share of image-intensifier systems in the C-Arms segment is anticipated to decline steadily.

List of Companies Covered in this Report:

- Allengers Medical Systems Ltd.

- Canon

- Carestream Health

- DMS Imaging SA

- Eurocolumbus S.p.A.

- Fujifilm Holdings Corp.

- GE Healthcare

- Hologic

- Koninklijke Philips

- Medtronic

- Nanjing Perlove Medical Equip. Co., Ltd.

- Orthoscan

- Shimadzu

- Siemens Healthineers

- Skanray Technologies Ltd.

- Stephanix

- Trivitron Healthcare

- United Imaging Healthcare Co., Ltd.

- Varian Medical Systems

- Ziehm Imaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Geriatric Population & Chronic Disease Burden

- 4.2.2 Adoption of Minimally-Invasive, Image-Guided Surgeries

- 4.2.3 Technological Advances in Flat-Panel & 3-D Imaging

- 4.2.4 Post-COVID Backlog of Elective Surgeries

- 4.2.5 Expansion of Ambulatory Surgical Centres in Tier-2 Brazilian & Colombian Cities

- 4.2.6 OEM Financing & Leasing Models Lowering Capex Barriers

- 4.3 Market Restraints

- 4.3.1 High Acquisition & Maintenance Costs

- 4.3.2 Shortage of Skilled Imaging Technologists & Surgeons

- 4.3.3 Currency Volatility Impacting Import Pricing & Procurement

- 4.3.4 Growth of Refurbished C-Arm Market Suppressing New Sales

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Fixed C-Arms

- 5.1.2 Mobile C-Arms

- 5.1.2.1 Full-Size C-Arms

- 5.1.2.2 Mini C-Arms

- 5.2 By Detector Technology

- 5.2.1 Image-Intensifier Systems

- 5.2.2 Flat-Panel Detector Systems

- 5.3 By Application

- 5.3.1 Cardiology

- 5.3.2 Gastroenterology

- 5.3.3 Neurology

- 5.3.4 Orthopedics & Trauma

- 5.3.5 Oncology

- 5.3.6 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centres

- 5.4.3 Specialty Clinics & Diagnostic Centres

- 5.5 By Country

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Chile

- 5.5.4 Colombia

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Allengers Medical Systems Ltd.

- 6.3.2 Canon Medical Systems Corp.

- 6.3.3 Carestream Health

- 6.3.4 DMS Imaging SA

- 6.3.5 Eurocolumbus S.p.A.

- 6.3.6 Fujifilm Holdings Corp.

- 6.3.7 GE Healthcare

- 6.3.8 Hologic Inc.

- 6.3.9 Koninklijke Philips N.V.

- 6.3.10 Medtronic plc

- 6.3.11 Nanjing Perlove Medical Equip. Co., Ltd.

- 6.3.12 OrthoScan Inc.

- 6.3.13 Shimadzu Corporation

- 6.3.14 Siemens Healthineers AG

- 6.3.15 Skanray Technologies Ltd.

- 6.3.16 Stephanix

- 6.3.17 Trivitron Healthcare

- 6.3.18 United Imaging Healthcare Co., Ltd.

- 6.3.19 Varian Medical Systems Inc.

- 6.3.20 Ziehm Imaging GmbH

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment