|

시장보고서

상품코드

2072702

미국의 C암 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. C-arms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

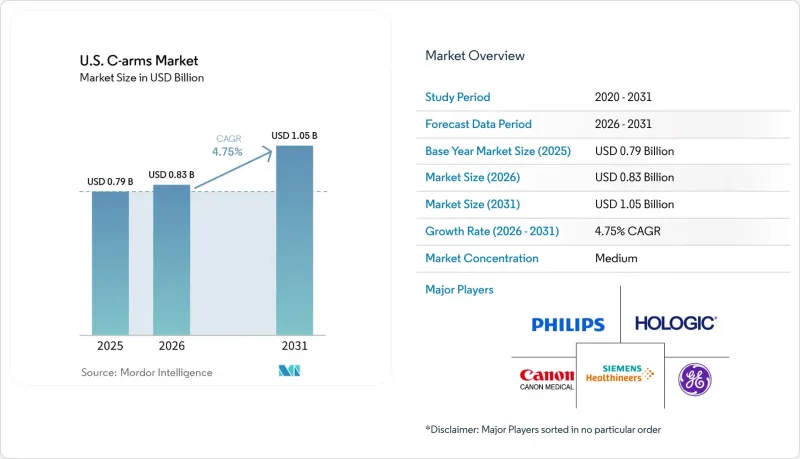

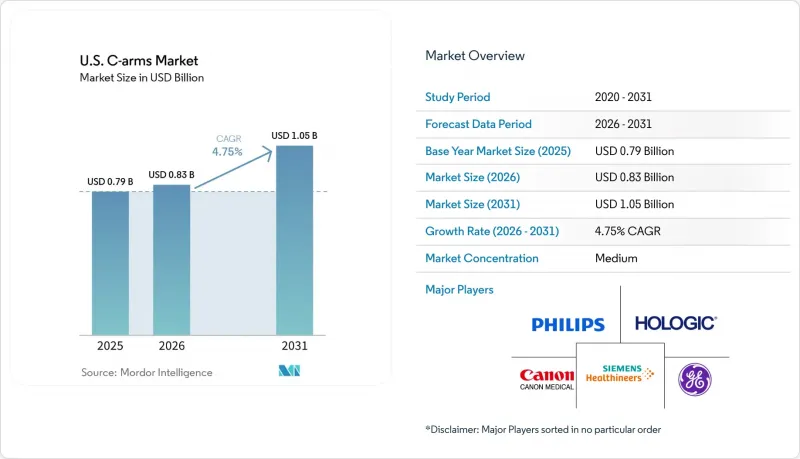

Mordor Intelligence에 의하면, 미국의 C암 시장 규모는 2025년 7억 9,000만 달러로 평가되었고, 2026년에는 8억 3,000만 달러로 추정되고, 2026-2031년 CAGR 4.75%로 성장을 지속할 전망이며, 2031년에는 10억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(고정식 C-암, 이동식 C-암), 용도별(순환기, 소화기, 신경, 정형외과 및 외상, 방사선 및 종양, 기타 용도), 그리고 최종 사용자별(병원, 외래수술센터(ASC), 전문 클리닉, 기타 최종 사용자)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

미국의 C-암 시장 동향 및 분석

외래 및 당일 수술 건수 증가

수술 건수가 병원의 수술실에서 외래 진료로 이동하고 있는 것이 미국 C-암 시장 수요를 견인하고 있습니다. CMS(미국 의료보험 및 의료보조 서비스 센터)는 2024년에 ASC(외래수술센터(ASC))에서 시행 가능한 시술 목록을 37건, 2025년에는 21건 더 확대하여, 어깨 및 발목 재건술, 혈관 내 필터 제거술 등, 외래 환경에서 투시 영상 진단이 필요한 사례가 증가하고 있습니다. 이러한 시술의 대부분은 수술 중 영상 확인이 필요하기 때문에 외래 진료 시설 운영자들은 별도의 영상 촬영실 없이도 이러한 요구를 충족시킬 수 있는 시스템을 찾고 있습니다. MedPAC 보고서에 따르면, 시술을 ASC로 이전함으로써 건당 환자 부담금이 684달러 감소하는 것으로 나타났으며, 이는 이러한 전환을 더욱 촉진하는 동시에 소형이고 효율적인 C-암 시스템에 대한 수요를 높이고 있습니다.

미국 내 정형외과 및 외상 영상 진단 수요 증가

골절 고정이나 척추 수술 등의 시술에 있어 실시간 영상 진단이 필수적이기 때문에 정형외과 및 외상 치료는 계속해서 미국 C-암 시장의 주요 성장 동력으로 자리잡고 있습니다. 미국 관절 치환 등록부(American Joint Replacement Registry)의 2025년 보고서에서는 440만 건의 수술이 분석되었으며, 그중 초회 인공 슬관절 전치환술이 51.2%, 인공 고관절 전치환술이 32.4%를 차지했습니다. 외래 진료의 추세가 두드러지며, 2024년까지 무릎 관절 치환술의 72%가 외래 시설에서 시행될 것으로 예측됩니다. MedPAC은 ASC(외래수술센터(ASC))에서 메디케어 대상 무릎 관절 전치환술이 33% 증가했고, 고관절 전치환술이 34% 증가했다는 점을 지적하며, 이러한 환경에서 휴대용 영상 진단 솔루션에 대한 수요가 높아지고 있음을 부각시키고 있습니다.

높은 설비 투자 비용과 자금 조달 조건의 강화

설비 투자는 미국 C-암 시장에서 특히 지역 병원, 독립 의료 센터 및 소규모 시설의 경우 여전히 주요 제약 요인으로 작용하고 있습니다. 구매자들은 스캐너의 가격뿐만 아니라 서비스 계약, 소프트웨어 업그레이드, 수술실 준비 상황 및 교육 요구 사항도 평가했습니다. 이동식 및 고정식 투시 시스템은 로봇 수술 시스템이나 디지털 기록 시스템에 대한 투자와 자금을 놓고 경쟁하고 있으며, 그 결과 새로운 플랫 패널 디스플레이 시스템의 장점이 있음에도 불구하고 일부 의료 기관에서는 구형 영상 증강 장치를 계속 사용할 수밖에 없는 상황에 처해 있습니다. 공동 구매 계약을 통해 재정적 압박은 다소 완화되지만, 생산성 향상이나 시술 건수 증가에 따른 투자 회수가 지연될 것으로 예상되는 경우, 자금 조달 심사가 엄격해지면서 발주가 지연될 수 있습니다.

부문별 분석

2025년, 고정식 C-암은 매출의 62.35%를 차지했으며, 미국 C-암 시장에서 우위를 유지했습니다. 이 장비의 사용은 카테터 검사실, 하이브리드 수술실 및 중재 시술실에 집중되어 있으며, 이러한 장소에서는 기동성보다 넓은 시야의 영상 촬영과 워크플로우의 안정성이 우선시됩니다. 성장률은 이동식 플랫폼보다 완만하지만, 병원이 최신 선량 관리 기준을 충족하기 위해 아날로그 장비에서 디지털 평판 장비로 업그레이드할 때, 고정식 시스템은 교체 주기의 혜택을 누리고 있습니다. 21 CFR 1020.32에 근거한 FDA의 성능 기준 또한 이러한 업데이트 추세를 더욱 뒷받침하고 있습니다.

이동식 C-암 시장은 2031년까지 연평균 성장률(CAGR) 5.98%를 나타낼 것으로 예측되며, 미국 C-암 시장에서 가장 빠르게 성장하는 플랫폼이 될 전망입니다. 이러한 수요를 주도하고 있는 것은 영구적인 인프라가 필요 없는 유연한 수술 중 영상 진단 솔루션을 필요로 하는 병원, 외래수술센터(ASC), 그리고 다학제 진료 센터입니다. Siemens Healthineers는 환자 위치를 자동으로 조정하여 수술실의 효율성을 높여주는 'CIARTIC Move' 덕분에 이 부문의 발전에 기여했습니다. 사지 정형외과 및 현장 진단(Point-of-Care) 분야 수요를 충족시키는 미니 C-암의 틈새 시장도 확대되고 있으며, Turner Imaging Systems의 'SMART-C' 500대의 도입 대수 달성 및 2026년 4월 매출액 67% 증가가 이를 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the u.S. c-arms market size is expected to grow from USD 0.79 billion in 2025 to USD 0.83 billion in 2026 and is forecast to reach USD 1.05 billion by 2031 at 4.75% CAGR over 2026-2031.

This report is Segmented by Type (Fixed C-Arms, Mobile C-Arms), by Application (Cardiology, Gastroenterology, Neurology, Orthopedics and Trauma, Radiology and Oncology, Other Applications), and by End User (Hospitals, Ambulatory Surgery Centers, Specialty Clinics, Other End Users). The Market Forecasts are Provided in Terms of Value (USD).

U.S. C-arms Market Trends and Insights

Expanding Ambulatory and Outpatient Procedural Volumes

The shift of surgical cases from hospital operating rooms to ambulatory care is driving demand in the United States C-arms market. CMS expanded the ASC-covered procedure list by 37 procedures in 2024 and 21 more in 2025, increasing cases requiring fluoroscopic imaging in outpatient settings, such as shoulder and ankle reconstructions and endovascular filter retrievals. Many of these procedures need intraoperative visualization, and outpatient operators seek systems that meet this demand without requiring fixed imaging rooms. MedPAC reported that moving cases to ASCs reduces patient costs by USD 684 per procedure, further supporting this migration and boosting demand for compact, efficient C-arm systems.

Rising U.S. Orthopedic and Trauma Imaging Demand

Orthopedic and trauma care remain key drivers of the United States C-arms market due to their reliance on real-time imaging for procedures like fracture fixation and spinal work. The American Joint Replacement Registry's 2025 report reviewed 4.4 million procedures, with primary total knee arthroplasties accounting for 51.2% and total hip arthroplasties for 32.4%. Outpatient trends are evident, with 72% of knee replacements performed in outpatient settings by 2024. MedPAC noted a 33% rise in Medicare total knee arthroplasties and a 34% increase in hip arthroplasties at ASCs, highlighting the growing need for mobile imaging solutions in these settings.

High Capital Cost and Financing Scrutiny

Capital spending remains a key restraint in the United States C-arms market, particularly for community hospitals, independent centers, and smaller facilities. Buyers evaluate not only scanner prices but also service commitments, software upgrades, room readiness, and training needs. Mobile and fixed fluoroscopy systems compete for capital with robotic surgery systems and digital record investments, leading some providers to extend the use of older image-intensifier units despite the benefits of newer flat-panel systems. Group purchasing agreements ease some financial pressure, but financing scrutiny delays orders when facilities anticipate slow returns from productivity or procedural growth.

Other drivers and restraints analyzed in the detailed report include:

- Faster Adoption of Mobile C-Arms in Hybrid and Same-Day Settings

- Workflow Improvements from Low-Dose and Flat-Panel Imaging Upgrades

- Radiation Safety Compliance Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, fixed C-arms accounted for 62.35% of revenue, maintaining their dominance in the United States C-arms market. Their usage is concentrated in catheterization labs, hybrid operating rooms, and interventional suites, where large-field imaging and workflow stability are prioritized over mobility. Although their growth is slower than mobile platforms, fixed systems benefit from replacement cycles as hospitals upgrade from analog to digital flat-panel units to meet modern dose management standards. The FDA's performance standard under 21 CFR 1020.32 further drives this replacement trend.

Mobile C-arms are projected to grow at a 5.98% CAGR through 2031, making them the fastest-growing platform in the United States C-arms market. Their demand is fueled by hospitals, ASCs, and multi-specialty centers seeking flexible intraoperative imaging solutions without permanent infrastructure. Siemens Healthineers advanced this segment with the CIARTIC Move, which automates positioning and improves operating room efficiency. The mini C-arm niche, catering to extremity orthopedics and point-of-care needs, is also expanding, as demonstrated by Turner Imaging Systems' 500th SMART-C installation and 67% sales growth in April 2026.

Complete Report Scope:

- By Type

- Fixed C-Arms

- Mobile C-Arms

- Full-Size C-Arms

- Mini C-Arms

- By Application

- Cardiology

- Gastroenterology

- Neurology

- Orthopedics and Trauma

- Radiology and Oncology

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgery Centers

- Specialty Clinics

- Other End Users

List of Companies Covered in this Report:

- Allengers

- Apelem

- Beckton Dickinson

- Canon

- DMS Imaging

- FUJIFILM

- GE Healthcare

- Hologic

- Koninklijke Philips

- Medtronic

- Orthoscan, Inc.

- PerkinElmer

- Shimadzu

- Siemens Healthineers

- Siemens Healthineers

- Stryker

- Turner Imaging System

- United Imaging Healthcare Co., Ltd.

- Varex Imaging

- Ziehm Imaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Ambulatory and Outpatient Procedural Volumes

- 4.2.2 Rising U.S. Orthopedic and Trauma Imaging Demand

- 4.2.3 Faster Adoption of Mobile C-Arms in Hybrid and Same-Day Settings

- 4.2.4 Workflow Improvements from Low-Dose and Flat-Panel Imaging Upgrades

- 4.2.5 Growing Use in Pain Management and Image-Guided Interventions

- 4.2.6 Replacement Demand from Installed Base Aging in Hospitals and Surgery Centers

- 4.3 Market Restraints

- 4.3.1 High Capital Cost and Financing Scrutiny

- 4.3.2 Radiation Safety Compliance Burden

- 4.3.3 Staff Training and Positioning Complexity

- 4.3.4 Slow Replacement Cycles in Budget-Constrained Facilities

- 4.4 Value Chain Analysis

- 4.5 Supply Chain Analysis

- 4.6 Technological Outlook

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE USD)

- 5.1 By Type

- 5.1.1 Fixed C-Arms

- 5.1.2 Mobile C-Arms

- 5.1.2.1 Full-Size C-Arms

- 5.1.2.2 Mini C-Arms

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Gastroenterology

- 5.2.3 Neurology

- 5.2.4 Orthopedics and Trauma

- 5.2.5 Radiology and Oncology

- 5.2.6 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Specialty Clinics

- 5.3.4 Other End Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Allengers Medical Systems Limited

- 6.3.2 Apelem

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Canon Medical Systems Corporation

- 6.3.5 DMS Imaging

- 6.3.6 FUJIFILM Holdings Corporation

- 6.3.7 GE Healthcare

- 6.3.8 Hologic, Inc.

- 6.3.9 Koninklijke Philips N.V.

- 6.3.10 Medtronic plc

- 6.3.11 Orthoscan, Inc.

- 6.3.12 PerkinElmer Inc.

- 6.3.13 Shimadzu Corporation

- 6.3.14 Siemens Healthcare Private Limited

- 6.3.15 Siemens Healthineers AG

- 6.3.16 Stryker Corporation

- 6.3.17 Turner Imaging Systems

- 6.3.18 United Imaging Healthcare Co., Ltd.

- 6.3.19 Varex Imaging Corporation

- 6.3.20 Ziehm Imaging GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment