|

시장보고서

상품코드

2061523

유세포 분석 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Flow Cytometry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

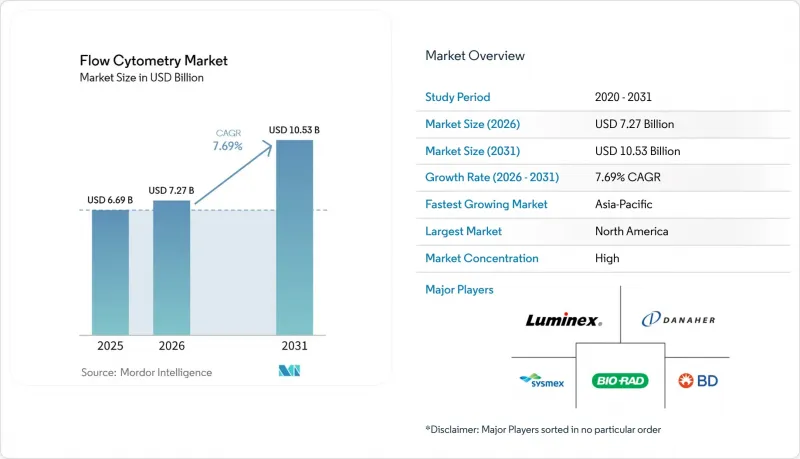

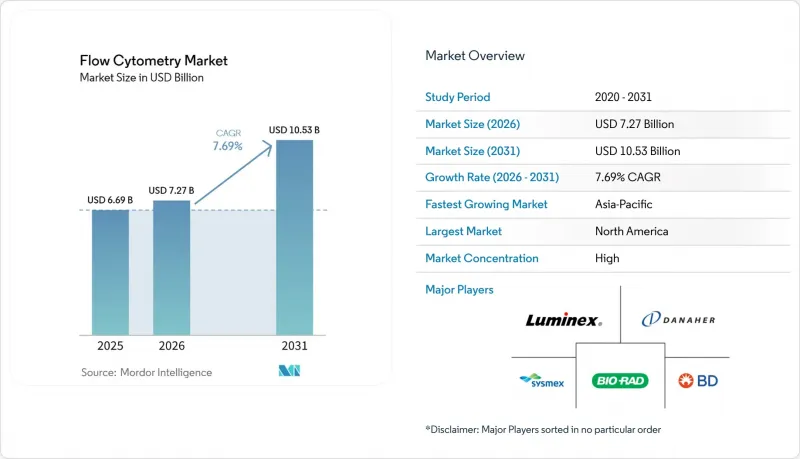

유세포 분석 시장 규모는 2025년에 66억 9,000만 달러로 평가되었고, 2026년에 72억 7,000만 달러로 추정되고, 2031년까지 105억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 7.69%로 성장할 전망입니다.

본 보고서는 제품 및 서비스별(장비-세포 분석 장치 및 세포 선별 장치, 시약 및 소모품, 소프트웨어, 서비스), 기술별(세포 기반 유세포 분석 등), 용도별(임상 진단, 신약 개발 등), 최종 사용자별(병원 및 클리닉 등), 지역별(북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 유세포 분석 시장 동향 및 인사이트

줄기세포 및 재생의학 워크플로우에서는 폐쇄형 유세포 분석이 채택되고 있습니다.

임상용 배치의 오염과 개방형 분리기 간의 연관성을 지적한 FDA 지침에 따라, 동종 이식용 개발 기업들은 현재 주변 환경에 노출되지 않고 CD34+ 세포를 분리하기 위해 MACSQuant Tyto나 AQUIOS STEM과 같은 폐쇄형 분리기 사용을 의무화하고 있습니다. 위탁 개발 기관(CDO)의 보고에 따르면, 로트 불합격률이 40% 감소했으며, 자체 CAR-T 제조 기간이 21일에서 16일로 단축되었습니다. 이러한 시간 단축은 환자 대기 명단에 직접적인 영향을 미치고 있습니다. 간엽계 줄기세포를 활용한 퇴행성 관절염 임상시험을 포함한 재생의학 프로젝트는 신규 소터 도입의 18%를 차지하며, 2023년의 11%에서 증가했습니다. 기존의 제트 인 에어(JIA) 시스템을 일회용 유체 시스템으로 개조할 수 있는 공급업체들은 경쟁 우위를 점하고 있지만, 중소규모 기업들은 GMP 준수를 위해 필요한 재설계에 필요한 자금을 조달하는 데 어려움을 겪고 있습니다. 상환 제도 정비가 더딘 지역에서는 병원 측이 폐쇄형 시스템으로의 업그레이드에 따른 설비 투자(CAPEX)를 상쇄하기 위해 시약 임대 계약을 검토하고 있습니다.

임상 진단 : 미세잔존병변(MRD) 검출을 위한 스펙트럼 유세포 분석 도입

이 스펙트럼 분석 장치는 100만 개의 정상 세포 중에서 백혈병 세포 1개를 검출할 수 있으며, 이는 기존 장비로는 여러 개의 튜브를 사용해야만 달성할 수 있는 감도입니다. 써모피셔는 2025년에 ‘Attune Xenith’를 출시하여, 한 번의 측정으로 24색 패널을 분석할 수 있게 함으로써, 과거 2영업일이 소요되던 순차 염색 과정을 없앴습니다. 현재 미국의 보험 급여 범위에는 19색 MRD 패널이 487달러로 포함되어 있어, 지역 암 진료 센터에 있어 스펙트럼 분석기는 경제적인 선택지가 되고 있습니다. Cytek사의 ‘Aurora Evo’는 데이터 수집 속도를 초당 7만 건으로 두 배로 높여, 검사 기관이 8시간 근무 교대당 120건의 MRD 검체를 처리할 수 있게 했습니다. 유럽임상종양학회(ESMO)의 지침이 급성 림프구성 백혈병의 MRD 검사에 스펙트럼 유동세포측정법(spectral flowmetry)의 도입을 권장함에 따라, 독일, 프랑스, 영국 전역에서 이 기술의 도입이 가속화되었습니다.

부문별 분석

2025년에는 장비가 매출의 42.55%라는 최대 점유율을 차지한 것으로 평가되었고, 이는 이미징 모듈과 음향 집속 챔버를 갖춘 스펙트럼 소터를 우선시하는 예산 배분 추세를 반영한 것입니다. 시약 및 소모품은 지속적인 수익원으로 자리 잡고 있으며, 고성능 면역종양학 키트가 현재 소모품 매출의 31%를 차지하고 있어, 설비 투자 변동에 관계없이 공급업체의 현금 흐름을 안정적으로 유지하고 있습니다. 소프트웨어는 가장 빠르게 성장하는 분야이며, 오토게이팅 엔진과 GDPR(EU 개인정보보호규정) 준수 데이터 레지던시를 갖춘 클라우드 네이티브 분석이 다중 사이트 임상시험에 확산됨에 따라 2031년까지 연평균 성장률(CAGR) 13.25%로 성장할 전망입니다. 설치 및 원격 지원 계약은 현지의 유세포 분석 전문가 부족을 보완하고 가동 중단 시간을 60% 줄여주고 있지만, 연간 운영 비용이 현저히 증가하고 있습니다.

세포 분석 장치의 출하 대수는 규제 당국의 승인과 처리 능력이 최우선으로 고려되기 때문에 임상 진단 분야에서 주류를 이루고 있는 반면, 소터는 하류 오믹스 분석을 위한 희귀 세포 분리가 필요한 연구 개발(R&D) 예산 분야에서 주류를 이루고 있습니다. 2024년 유럽에서 발생한 표지판 시설 화재와 같은 항체 공급 차질은 다각화된 밸류체인과 검증된 대체 클론의 중요성을 여실히 보여주고 있습니다. ISO 17034 인증을 획득한 색소, 비드 및 보정용 대조군은 GMP 환경에서의 품질 관리 워크플로우를 가속화합니다. 사전 최적화된 MRD(미세잔류병변) 또는 CAR-T 특성 평가 패널을 통해 분석법 개발 기간이 6개월에서 4주로 단축되어, 적극적인 임상 일정을 뒷받침하고 있습니다.

2025년에는 진단 및 연구 분야의 면역 표현형 분석과 세포 사멸 관련 응용 분야가 주도적인 역할을 하며, 세포 기반 분석법이 매출의 65.53%를 차지했습니다. 이미징 유세포 분석 시장은 규모는 작지만, 항체-약물 복합체(ADC)의 세포 내 흡수 연구에서 형태학에 기반한 희귀 세포 검출에 대한 제약 업계 수요에 힘입어 연평균 성장률(CAGR) 15.85%로 성장하고 있습니다. 비즈 기반의 다중 유세포 분석법은 여전히 고다중도 면역 분석에서 중요한 역할을 하고 있지만, 더 낮은 비용으로 높은 처리량을 제공하는 평면 어레이와의 경쟁에 직면해 있습니다. 음향 집속식 유세포 분석는 시스 용액 소비량을 70% 줄여주어, 수자원 확보가 어려운 지역의 연구소에 매력적인 장비입니다.

순환 종양 세포 계수에 사용되는 이미징 플랫폼에 대한 일본의 신속 승인 제도 덕분에, 국내 업체들은 유럽 및 미국의 경쟁사들보다 9개월 먼저 시장에 진출할 수 있게 되었습니다. 이미징 사이토메트리의 40만-60만 달러에 달하는 도입 비용이 보급의 걸림돌이 되고 있어, 연구 중심 시설과 중규모 병원 사이에서 양극화된 시장이 형성되고 있습니다. 이미징 플랫폼용 유세포 분석 시장 규모는 종양학 및 유전자 치료 워크플로우로의 급속한 확대를 반영하여, 2031년까지 16억 달러를 넘어설 것으로 전망됩니다.

지역별 분석

2025년에는 북미가 매출의 41.13%를 차지하며 시장을 주도했습니다. 이는 메디케어의 19가지 색상 MRD(잔존 병변) 검사에 대한 보험 적용 코드와, 고매개변수 유세포분석을 중시하는 수십억 달러 규모의 제약 연구개발비에 힘입은 결과입니다. 미국만 해도 2024년에 신약 개발에 1,020억 달러를 투자했으며, 초기 단계의 종양학 임상시험에서 스펙트럼 분석기에 대한 강력한 수요를 창출하고 있습니다. 캐나다 주 정부는 온타리오주와 브리티시컬럼비아주에 12대의 분광 분석 장비를 도입하여 MRD 검사를 일원화하고, 외딴 지역의 지역사회에서 검사에 대한 접근성을 개선했습니다. 멕시코의 INCAN은 국내 CAR-T 임상시험을 지원하기 위해 영상 플랫폼으로 업그레이드하여, 이 지역 내 세포 치료의 허브로서의 입지를 확고히 했습니다.

아시아태평양은 수입품보다 30% 저렴한 가격의 중국산 스펙트럼 시스템이 승인된 것을 배경으로, 연평균 성장률(CAGR) 12.51%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. Mindray는 3년 동안 검사별 비용을 고정하는 시약 렌탈 패키지를 통해 2025년 중국 시장에서 9%의 시장 점유율을 확보했습니다. 인도 정부 산하 종양 센터는 2027년까지 연간 200만 건의 백혈병 선별 검사를 실시한다는 계획에 따라, 고성능 분석 장비 14대를 추가로 도입했습니다. 일본은 순환 종양 세포(CTC)용 이미징 사이토메트리 개발을 가속화하여, 국내 기업들에게 아시아 전역에서 선도적 우위를 안겨주었습니다.

IVDR로의 전환기에 있는 유럽에서는 카탈로그 주문이 밀려 있는 상황임에도 불구하고, 여전히 고가 기기 시장으로서의 입지를 유지하고 있습니다. 독일의 한 대학 병원은 CAR-T 연구를 위해 스펙트럼 소터의 업그레이드에 1,800만 유로를 투자했습니다. 영국은 유세포 분석 관련 서비스를 7개 허브로 통합하여, MRD 검사당 비용을 22% 절감했습니다. 프랑스는 6개의 새로운 스펙트럼 플랫폼을 승인하여 경쟁을 심화시키는 한편, 평균 판매 가격을 8% 인하했습니다. 이탈리아와 스페인은 시약 비용 절감을 최우선으로 하고 있어, 이식 프로그램과 관련이 없는 한 고사양 장비로의 업그레이드를 미루고 있습니다.

중동 및 아프리카에서는 사우디아라비아와 아랍에미리트에 22대의 스펙트럼 분석 장비를 도입하여 각국의 암 등록 제도를 강화했습니다. 남미는 통화 약세라는 역풍에 직면해 있으며, 브라질의 공립 연구소에서는 설비 투자 비용을 상쇄하기 위해 시약 대여 방식으로의 전환이 진행되고 있습니다. 전반적으로, 지역별 정책 지원과 현지 생산 역량이 도입의 방향을 결정짓는 경향이 강해지고 있으며, 대륙마다 서로 다른 성장 곡선이 형성되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the flow cytometry market size is projected to be USD 6.69 billion in 2025, USD 7.27 billion in 2026, and reach USD 10.53 billion by 2031, growing at a CAGR of 7.69% from 2026 to 2031.

This report is Segmented by Product and Services (Instruments [Cell Analyzers and Cell Sorters], Reagents & Consumables, Software, and Services), Technology (Cell-Based Flow Cytometry, and More ), Application (Clinical Diagnostics, Drug Discovery & Development, and More), End-User (Hospitals & Clinics, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Flow Cytometry Market Trends and Insights

Stem-Cell & Regenerative-Medicine Workflows Adopt Closed-System Cytometers

Allogeneic developers now mandate closed-system sorters, such as the MACSQuant Tyto and AQUIOS STEM, to isolate CD34+ cells without ambient exposure, following FDA guidance linking open-air sorting to contamination in clinical-grade batches. Contract development organizations report 40% fewer failed lots, cutting autologous CAR-T manufacturing from 21 days to 16 days, a time saving that directly affects patient backlog. Regenerative-medicine projects, including osteoarthritis trials employing mesenchymal stromal cells, now account for 18% of new sorter placements, up from 11% in 2023. Vendors able to retrofit legacy jet-in-air systems with disposable fluidics gain an advantage, while smaller firms struggle to finance the redesign needed for GMP compliance. In regions where reimbursement lags, hospitals consider reagent-rental contracts to offset cap-ex outlays for closed-system upgrades.

Clinical Diagnostics Adoption of Spectral Cytometers for Minimal Residual Disease

Spectral analyzers detect one leukemic cell among 1 million healthy cells, a sensitivity conventional instruments cannot match without multiple tubes. Thermo Fisher introduced the Attune Xenith in 2025, resolving 24-color panels in a single run and eliminating sequential staining that once consumed two working days. U.S. reimbursement now covers 19-color MRD panels at USD 487, making spectral instruments economic for community oncology centers. Cytek's Aurora Evo doubles acquisition speed to 70,000 events per second, enabling reference labs to process 120 MRD samples per 8-hour shift. As guidelines from the European Society for Medical Oncology endorsed spectral flow for MRD in acute lymphoblastic leukemia, procurement cycles accelerated across Germany, France, and the United Kingdom.

Other drivers and restraints analyzed in the detailed report include:

- AI-Guided Spectral Unmixing & Auto-Gating Shorten Core-Lab Turnaround

- Multi-Parametric Immuno-Oncology Panels Spur High-Parameter Purchases

- Shortage of Skilled Cytometrists Shifts Testing to Reference Labs

- EU MDR / IVDR Reagent Registration Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Instruments held the largest 42.55% revenue share in 2025, reflecting budget cycles favoring spectral sorters with imaging modules and acoustic-focusing chambers. Reagents and consumables provide recurring revenue, with high-parameter immuno-oncology kits now accounting for 31% of consumables, stabilizing vendor cash flow even as capital spending fluctuates. Software is the fastest-growing element, advancing at a 13.25% CAGR to 2031 as cloud-native analytics with auto-gating engines and GDPR-compliant data residency penetrate multi-site trials JIM. Installation and remote-support contracts offset local cytometrist shortages, cutting downtime by 60% but adding notable annual operating fees.

Cell analyzer shipments dominate clinical diagnostics because regulatory clearance and throughput are paramount, while sorters dominate R&D budgets that require rare-cell isolation for downstream omics. Antibody supply disruptions such as the 2024 European conjugation-facility fire highlight the value of diversified supply chains and validated substitute clones. Dyes, beads, and compensation controls certified under ISO 17034 accelerate quality-control workflows in GMP environments. Pre-optimized MRD or CAR-T characterization panels now cut assay development from six months to four weeks, supporting aggressive clinical timelines.

Cell-based assays constituted 65.53% of revenue in 2025, anchored by immunophenotyping and apoptosis applications across diagnostics and research. Imaging flow cytometry, though smaller, grows at a 15.85% CAGR, propelled by pharmaceutical demand for morphology-based rare-cell detection in antibody-drug conjugate internalization studies. Bead-based multiplex flow remains important in high-plex immunoassays but faces competition from planar arrays offering higher throughput at lower cost. Acoustic-focusing cytometers reduce sheath-fluid consumption by 70%, appealing to laboratories in regions with water constraints.

Japan's fast-track pathway for imaging platforms used in circulating tumor-cell enumeration provides domestic vendors a nine-month time-to-market lead over Western competitors. Imaging cytometry's USD 400,000-600,000 capital cost limits broader adoption, creating a two-tier market between research-intensive centers and mid-tier hospitals. The flow cytometry market size for imaging platforms is forecast to exceed USD 1.6 billion by 2031, reflecting the modality's rapid expansion into oncology and gene-therapy workflows.

Geography Analysis

North America led with 41.13% revenue in 2025, underpinned by Medicare's 19-color MRD reimbursement code and multibillion-dollar pharmaceutical R&D spend that favors high-parameter cytometry. The United States alone invested USD 102 billion in drug discovery during 2024, creating strong demand for spectral analyzers in early-stage oncology trials. Canada's provincial systems centralized MRD testing by installing 12 spectral instruments in Ontario and British Columbia, improving access in remote communities. Mexico's INCAN upgraded to imaging platforms to support domestic CAR-T trials, positioning itself as a regional cell-therapy hub.

Asia-Pacific is the fastest-growing region, with a 12.51% CAGR, driven by China's approvals for locally built spectral systems priced 30% below imports. Mindray captured 9% of Chinese placements in 2025 through reagent-rental bundles that lock per-test costs for three years. India's government oncology centers added 14 high-parameter analyzers to execute 2 million planned leukemia screens annually by 2027. Japan fast-tracked the development of imaging cytometry for circulating tumor cells, giving domestic firms a head start across Asia.

Europe, in IVDR transition, faces catalog backlogs but remains a premium instrument market. German university hospitals spent EUR 18 million upgrading spectral sorters for CAR-T studies. The United Kingdom consolidated flow services into seven hubs, trimming MRD cost per test by 22%. France approved six new spectral platforms, intensifying competition and sinking average selling prices by 8%. Italy and Spain prioritize reagent cost containment, delaying high-parameter upgrades unless tied to transplant programs.

Middle East & Africa installed 22 spectral analyzers across Saudi Arabia and the United Arab Emirates to bolster national cancer registries. South America faces currency headwinds; Brazil's public laboratories shift toward reagent-rental to offset cap-ex. Overall, regional policy support and local manufacturing capacity increasingly define adoption trajectories, creating differentiated growth curves across continents.

- Agilent Technologies (ACEA)

- Apogee Flow Systems

- BD Biosciences (Becton, Dickinson & Co.)

- Beckman Coulter Life Sciences (Danaher)

- Bio-Rad Laboratories

- Curiox Biosystems

- Cytek Biosciences

- Immudex

- Luminex (DiaSorin Group)

- Merck KGaA (MilliporeSigma)

- Miltenyi Biotec

- Mindray

- NanoCellect Biomedical

- On-Chip Biotechnologies

- Sony Biotechnology

- Standard BioTools (Fluidigm)

- Stratedigm

- Sysmex

- Thermo Fisher Scientific (Invitrogen)

- Union Biometrica

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stem-Cell & Regenerative-Medicine Workflows Adopt Closed-System Cytometers

- 4.2.2 Clinical Diagnostics Adoption of Spectral Cytometers for Minimal Residual Disease

- 4.2.3 AI-Guided Spectral Unmixing & Auto-Gating Shortens Core-Lab Turnaround

- 4.2.4 Point-of-Care Microfluidic Cytometers Penetrate Emerging Markets

- 4.2.5 Multi-Parametric Immuno-Oncology Panels Spur High-Parameter Purchases

- 4.2.6 GDPR/IVDR-Ready Cloud Analytics Platforms Expand Across Europe

- 4.3 Market Restraints

- 4.3.1 Shortage of Skilled Cytometrists Shifts Testing to Reference Labs

- 4.3.2 EU MDR / IVDR Reagent Registration Delays

- 4.3.3 Capital Cost of Image-Enabled Spectral Sorters

- 4.3.4 Cyber-Security & Data-Sovereignty Concerns in Government Hospitals

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product & Service

- 5.1.1 Instruments

- 5.1.1.1 Cell Analyzers

- 5.1.1.2 Cell Sorters

- 5.1.2 Reagents & Consumables

- 5.1.2.1 Antibodies

- 5.1.2.2 Dyes & Beads

- 5.1.2.3 Kits & Panels

- 5.1.3 Software

- 5.1.4 Services

- 5.1.1 Instruments

- 5.2 By Technology

- 5.2.1 Cell-Based Flow Cytometry

- 5.2.2 Bead-Based Flow Cytometry

- 5.2.3 Imaging Flow Cytometry

- 5.2.4 Acoustic-Focusing Flow Cytometry

- 5.3 By Application

- 5.3.1 Clinical Diagnostics

- 5.3.1.1 Oncology

- 5.3.1.2 Hematology

- 5.3.1.3 Infectious Diseases

- 5.3.1.4 Organ Transplantation

- 5.3.2 Drug Discovery & Development

- 5.3.3 Stem-Cell Therapy & Regenerative Medicine

- 5.3.4 Immunology

- 5.3.5 Other Applications

- 5.3.1 Clinical Diagnostics

- 5.4 By End-User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Pharmaceutical & Biotechnology Companies

- 5.4.3 Contract Research & Reference Laboratories

- 5.4.4 Other End-Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Agilent Technologies (ACEA)

- 6.3.2 Apogee Flow Systems

- 6.3.3 BD Biosciences (Becton, Dickinson & Co.)

- 6.3.4 Beckman Coulter Life Sciences (Danaher)

- 6.3.5 Bio-Rad Laboratories

- 6.3.6 Curiox Biosystems

- 6.3.7 Cytek Biosciences

- 6.3.8 Immudex

- 6.3.9 Luminex (DiaSorin Group)

- 6.3.10 Merck KGaA (MilliporeSigma)

- 6.3.11 Miltenyi Biotec

- 6.3.12 Mindray

- 6.3.13 NanoCellect Biomedical

- 6.3.14 On-Chip Biotechnologies

- 6.3.15 Sony Biotechnology

- 6.3.16 Standard BioTools (Fluidigm)

- 6.3.17 Stratedigm

- 6.3.18 Sysmex Corporation

- 6.3.19 Thermo Fisher Scientific (Invitrogen)

- 6.3.20 Union Biometrica

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment