|

시장보고서

상품코드

2061526

방위 항공기용 재료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Defense Aircraft Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

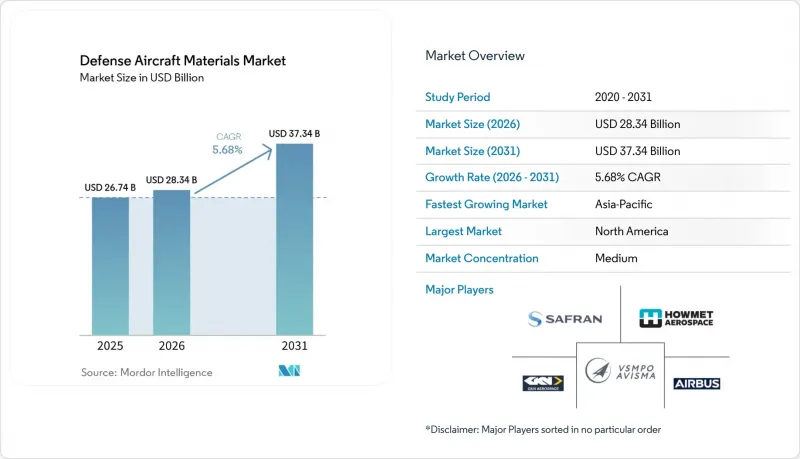

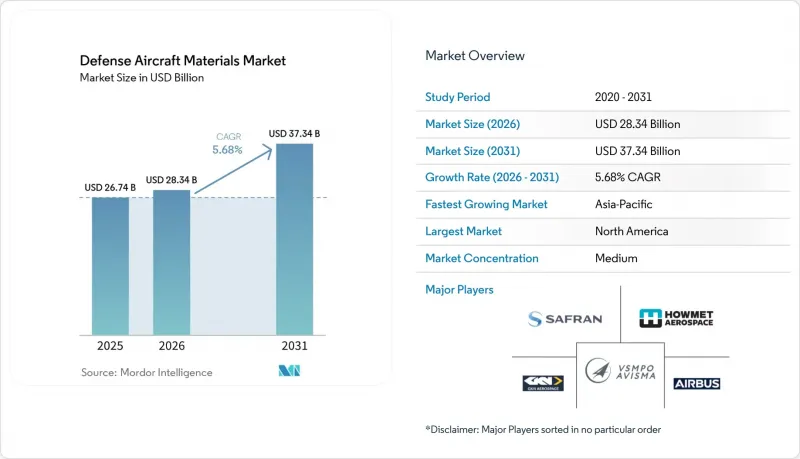

방위 항공기용 재료 시장 규모는 2025년 267억 4,000만 달러로 평가되었고, 2026년에는 283억 4,000만 달러로 추정되고, 2026-2031년 CAGR 5.68%로 성장을 지속할 전망이며, 2031년까지 373억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 항공기 유형별(고정익기, 회전익기), 재료 유형별(알루미늄, 티타늄, 강철, 초합금, 복합재료, 폴리머), 구성품별(기체, 엔진, 항공전자 장비, 착륙 장치, 내장재, 코팅), 최종 사용자 단계별(라인 핏, 레트로핏), 지역별(북미, 남미 등)로 분류되어 있습니다. 시장 전망은 금액(달러)으로 제시되어 있습니다.

세계의 방위 항공기용 재료 시장 동향 및 분석

국방 현대화 예산 증액

미국 국방부의 항공기 관련 지출은 2025 회계연도에 8% 증가했으며, F-35 블록 4 업그레이드에 520억 달러가 배정되었습니다. 이 업그레이드에는 새로운 티타늄 벌크헤드와 알루미늄 주익 스파가 필요합니다. 유럽의 NATO 회원국들은 2025년에 국방비를 6% 증액했고, 유로파이터 타이푼의 수명 연장 계약에 자금을 투입했습니다. 이로 인해 알루미늄 판재 소비량은 2024년 대비 15% 증가했습니다. 인도는 2025-2026 회계연도 자본 구매 예산으로 280억 달러를 배정했으며, 여기에는 국내에서 단조된 알루미늄·리튬 압출재를 사용하는 테자스 Mk1A 전투기 83대가 포함되어 있습니다. 한국은 KF-21 양산에 32억 달러를 예산으로 편성하고, 수출 허가 취득 지연을 피하기 위해 국내 프레스 기계를 통해 티타늄 단조품을 조달하고 있습니다. 중국의 2025년도 공식 국방 예산은 7.2% 증가했으나, 분석가들은 J-20 생산 가속화를 위한 군민 양용 프로그램에 추가로 30%의 예산이 편성된 것으로 추정하고 있습니다. 이러한 추세는 신규 생산과 정비 활동이 모두 활성화됨에 따라 방위 항공기용 재료 시장을 전반적으로 확대시킬 것입니다.

연료 절약을 위한 경량 소재의 필요성

나토(NATO) 회원국 공군은 항공 연료에 연간 100억 달러 이상을 지출하고 있으며, 이에 따라 조달 팀은 기체 중량을 8-12% 줄일 수 있는 알루미늄-리튬 합금이나 티타늄 합금을 우선적으로 채택하고 있습니다. KC-46 급유기는 알루미늄 7085로 제작된 프레임을 채택하여, 이를 통해 기체 중량을 1,320파운드(600kg) 줄였으며, 전체 수명 주기 동안의 연료 소비량을 4% 절감했습니다. F-35의 구조 중량의 15%는 Ti-6Al-4V가 차지하며, 주로 엔진 파일론과 주익 뿌리 부위의 금속 부품에 집중적으로 사용되고 있습니다. 이러한 부위에서는 강철에 비해 40% 더 높은 강도가 높은 비용을 정당화합니다. 에어버스는 A400M의 화물 패널에 알루미늄-리튬 합금 2195를 채택하여, 이를 통해 구조 중량을 10% 줄이고 항속 거리를 200해리 연장했습니다. 시코르스키사의 CH-53K는 티타늄 로터 헤드를 채택하여 공중 중량을 450kg 줄였으며, 이를 통해 1,800kg의 추가 적재가 가능해졌습니다. 이러한 소재 사양은 단조 및 압출 성형 공정에 대한 투자를 촉진하여 방위 항공기용 재료 시장의 장기적인 성장을 뒷받침하고 있습니다.

티타늄 및 초합금의 가격 변동

2024년 1월부터 2025년 12월까지, VSMPO-AVISMA가 차지하는 세계 항공우주 공급량의 35%를 마비시킨 제재 조치로 인해 티타늄 스폰지의 가격이 45% 급등했습니다. 보잉과 에어버스는 미국 내 스폰지 생산 시설을 재개했으나, 비용은 러시아산보다 여전히 30% 더 비싸며, 이로 인해 빌렛 가격 상승과 최대 26주에 달하는 리드타임 연장이 초래되고 있습니다. 니켈계 인코넬 및 하스텔로이의 현물 가격은 인도네시아의 광석 수출세와 중국의 희토류 규제를 배경으로 2025년에 28% 상승하여, 터빈 디스크 공급이 더욱 부족해졌습니다. OEM(원청 제조업체)은 고정가 계약을 통해 이러한 위험을 하류로 전가하고 있으며, 이로 인해 2차 공급업체의 이익률이 압박을 받고, 방위용 항공기 자재 시장의 성장이 둔화되고 있습니다.

부문별 분석

다목적 전투기는 연평균 성장률(CAGR) 5.76%로 성장하여 방위 항공기용 재료 시장 전체를 상회할 것으로 전망됩니다. 이러한 성장은 공군이 9G의 기동에 견딜 수 있도록 설계된 고강도 티타늄 격벽과 알루미늄 스퍼가 필요한 쌍발 플랫폼을 중심으로 기체를 통합하고 있기 때문입니다. 수송기 부문은 2025년에 매출의 23.45%를 차지한 것으로 평가되었으며, 이는 대량의 알루미늄 압출재와 티타늄 착륙장치용 단조품을 소비하는 C-130J 및 A400M 유지보수 프로그램에 힘입은 결과입니다. 제공권 확보용 전투기는 조달 대수는 적지만, 엔진 베이와 무기 파일론에는 고밀도 티타늄 및 초합금이 사용되고 있습니다. 훈련기 및 회전익기는 안정적인 수요를 창출하지만, 그 가치는 비교적 낮습니다. 알루미늄·리튬 합금 기체와 티타늄 로터 헤드 어셈블리가 애프터마켓 수주를 주도하고 있습니다. 사막의 모래먼지나 해상의 염분 함유 물보라와 같은 가혹한 운용 환경은 부식을 가속화하여 교체 주기를 단축시키고, 애프터마켓 수요를 증가시키고 있습니다.

고정익기는 회전익기에 비해 구조체가 크기 때문에 생산량의 대부분을 차지하고 있습니다. 또한, 다목적 설계의 기체는 단일 임무용 기존 기체보다 더 많은 금속 부품을 포함하고 있어, 티타늄 및 알루미늄 부품에 대한 지속적인 수요를 보장하고 있습니다. 이러한 추세는 복합재료가 점차 보급되고 있는 상황에서도 방위 항공기용 재료 시장의 지속적인 성장을 뒷받침하고 있습니다.

알루미늄 합금은 비용 효율성이 매우 중요한 기체 프레임 및 주익 리브에 광범위하게 채택됨에 따라, 2025년에는 매출의 37.95%를 차지했으며, 계속해서 주류를 이룰 것으로 전망됩니다. 한편, 티타늄 합금은 압축기 블레이드, 착륙 장치, 파일론 등의 용도에서 경량화가 직접적으로 항속 거리 향상으로 이어지기 때문에 2031년까지 연평균 성장률(CAGR) 5.83%로 성장할 것으로 전망됩니다. 초합금이나 고융점 금속은 틈새 시장 분야이긴 하지만, 1,100℃를 넘는 터빈 입구 온도에서는 필수 불가결한 소재로서, 엔진 부품에서 그 역할을 확고히 하고 있습니다.

고강도 강재는 뛰어난 인성이 요구되는 착륙 장치의 트러니언과 어레스팅 훅에 계속해서 사용되고 있습니다. 기존 알루미늄에 비해 10%의 경량화를 실현하고 비용 증가도 적당한 알루미늄-리튬 합금은 개조 프로그램에서 그 존재감을 확대되고 있습니다. 이러한 소재 구성에 따라 티타늄은 가치 측면에서 주도적인 위치를, 알루미늄은 수량 측면에서 기반을 차지하며, 방위 항공기용 재료 시장의 회복력을 확보하고 있습니다.

지역별 분석

북미는 미국 국방부의 항공기 지출 520억 달러와 연간 4만 톤의 항공우주용 알루미늄 및 8,000톤의 티타늄을 생산하는 국내 금속 산업의 견인 덕분에, 2025년에는 매출의 33.69%를 차지한 것으로 평가되었습니다. 아시아태평양은 중국의 J-20 생산량이 연간 80대에 달하고, 인도의 '아트마니르바르 바라트(자급자족 인도)' 정책에 따른 조달 의무, 그리고 한국의 KF-21 프로그램에 따른 벌크헤드 및 스퍼의 국내 생산 확보에 힘입어, 연평균 성장률(CAGR) 5.96%로 가장 높은 성장률을 보일 것으로 전망됩니다. 유럽은 시장 점유율 면에서는 뒤처져 있지만, FCAS와 템페스트 계획의 혜택을 누리고 있습니다. 이러한 계획은 초합금 및 티타늄 조달을 지역 내에서 현지화하는 것을 목표로 하고 있으며, 사프란(Safran)이나 에어버스 에어로스트럭처스(Airbus SE)와 같은 기업들에 수주 기회를 제공합니다.

지역별 공급망은 큰 변화를 겪고 있습니다. 미국 내 스폰지 알루미늄 생산 재개와 폴란드의 단조 생산 능력 확충으로 인해 대서양 횡단 의존도는 낮아지고 있습니다. 한편, 아시아 각국 정부는 전략적 자율성을 높이기 위해 단조 시설에 대한 지원을 실시했습니다. 중동에서는 F-15SA와 라팔 전투기의 애프터마켓 수요가 여전히 견조하지만, 국내 단조 능력이 제한적이어서 부가가치 창출에는 제약이 있습니다. 남미는 여전히 틈새 시장이며, 브라질의 KC-390 프로그램이 핵심을 이루고 있으며, 현지 조달에 관한 오프셋 요건에 의해 주도되고 있습니다. 전반적으로, 생산 거점의 이동으로 인해 성장이 재분배되는 한편, 모든 지역에서 절대적인 생산량이 증가함에 따라 전 세계 방위 항공기용 재료 시장의 다각화가 가속화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the defense aircraft materials market size is expected to grow from USD 26.74 billion in 2025 to USD 28.34 billion in 2026 and is forecasted to reach USD 37.34 billion by 2031 at a 5.68% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Fixed-Wing, Rotorcraft), Material Type (Aluminum, Titanium, Steel, Super-Alloys, Composites, Polymers), Component (Airframe, Engine, Avionics, Landing Gear, Interior, Coatings), End-User Phase (Linefit, Retrofit), and Geography (North America, South America, and More). Market Forecasts are Provided in Value (USD).

Global Defense Aircraft Materials Market Trends and Insights

Defense Modernization Budgets Rising

Pentagon's aircraft expenditures increased by 8% in fiscal 2025, allocating USD 52 billion for F-35 Block 4 upgrades, which require new titanium bulkheads and aluminum wing spars. European NATO members increased defense spending by 6% in 2025, funding Eurofighter Typhoon life-extension contracts that led to a 15% rise in aluminum-plate consumption compared to 2024. India allocated USD 28 billion for fiscal 2025-26 capital purchases, including 83 Tejas Mk1A fighters that utilize locally forged aluminum-lithium extrusions. South Korea budgeted USD 3.2 billion for KF-21 serial production, sourcing titanium forgings from domestic presses to avoid potential delays in obtaining export licenses. China's official 2025 defense budget increased by 7.2%, with analysts estimating an additional 30% embedded in military-civil programs to accelerate J-20 production. These developments collectively expand the defense aircraft materials market as both new production and overhaul activities intensify.

Lightweight-Materials Imperative for Fuel Savings

NATO air forces spend over USD 10 billion annually on aviation fuel, prompting procurement teams to prioritize aluminum-lithium and titanium alloys that reduce airframe weight by 8-12%. The KC-46 tanker features aluminum 7085 frames, which reduce aircraft weight by 1,320 pounds (600 kg) and achieve a 4% lifetime fuel savings. Ti-6Al-4V accounts for 15% of the F-35's structural mass, concentrated in engine pylons and wing-root fittings, where its 40% strength advantage over steel justifies its higher cost. Airbus employs an aluminum-lithium alloy, 2195, in the A400M cargo panels, which reduces structural weight by 10% and extends the range by 200 nautical miles. Sikorsky's CH-53K integrates titanium rotor heads, cutting 450 kg from empty weight and enabling an additional 1,800 kg payload. These material specifications drive investments in forging and extrusion processes, supporting long-term growth in the defense aircraft materials market.

Volatility in Titanium and Super-Alloy Prices

Titanium sponge prices surged by 45% between January 2024 and December 2025 due to sanctions that disrupted VSMPO-AVISMA's 35% share of the global aerospace supply. While Boeing and Airbus reopened US sponge production facilities, costs remain 30% higher than Russian supply, leading to increased billet prices and extended lead times of up to 26 weeks. Nickel-based Inconel and Hastelloy spot prices rose by 28% in 2025, driven by Indonesian ore-export taxes and Chinese restrictions on rare earths, further tightening turbine-disk supply. Original Equipment Manufacturers (OEMs) have passed these risks downstream through fixed-price contracts, compressing the margins of tier-two suppliers and moderating growth in the defense aircraft materials market.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Global MRO Demand for Aging Fleets

- Certified Metal Additive Manufacturing Adoption

- Substitution Threat from Composites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Multi-role fighters are projected to grow at a 5.76% CAGR, surpassing the overall defense aircraft materials market. This growth is driven by air forces consolidating their fleets around twin-engine platforms that require high-strength titanium bulkheads and aluminum spars designed for 9 g maneuvers. Transport aircraft are expected to account for 23.45% of revenue in 2025, supported by sustainment programs for C-130J and A400M, which consume significant volumes of aluminum extrusions and titanium landing-gear forgings. Combat-air-superiority fighters, despite smaller procurement runs, incorporate dense titanium and super-alloy content in engine bays and weapons pylons. Trainers and rotorcraft contribute steady but lower-value demand, with aluminum-lithium fuselages and titanium rotor-head assemblies driving aftermarket orders. Harsh operational environments, such as desert dust and maritime salt spray, accelerate corrosion, reducing replacement cycles and boosting aftermarket demand.

Fixed-wing platforms dominate volume concentration due to their larger structures compared to rotorcraft. Multi-role designs also integrate more metallic components than single-mission predecessors, ensuring a sustained demand for titanium and aluminum components. This trend supports continued growth in the defense aircraft materials market, even as composite materials gain traction.

Aluminum alloys are expected to remain dominant, accounting for 37.95% of revenue in 2025, due to their widespread use in fuselage frames and wing ribs where cost efficiency is critical. Titanium alloys, however, are projected to grow at a 5.83% CAGR through 2031, driven by applications in compressor blades, landing gear, and pylons, where weight reduction directly enhances combat radius. Super-alloys and refractory metals, while niche, are indispensable for turbine-inlet temperatures exceeding 1,100 °C, securing their role in engine components.

High-strength steels continue to be used in landing-gear trunnions and arresting hooks, which require exceptional toughness. Aluminum-lithium alloys, offering a 10% weight reduction over traditional aluminum at moderate cost premiums, are expanding their presence in retrofit programs. The material mix positions titanium as the value leader and aluminum as the volume anchor, ensuring resilience in the defense aircraft materials market.

Geography Analysis

North America is expected to account for 33.69% of the revenue in 2025, driven by USD 52 billion in Pentagon aircraft expenditures and a domestic metals industry that produces 40,000 tons of aerospace-grade aluminum and 8,000 tons of titanium annually. The Asia-Pacific region is projected to grow at the fastest rate, with a 5.96% CAGR, fueled by China's J-20 production reaching 80 units per year, India's Atmanirbhar Bharat sourcing mandates, and South Korea's KF-21 program securing local bulkhead and spar production. Europe, although trailing in market share, benefits from FCAS and Tempest programs, which aim to localize the procurement of super-alloys and titanium within the region, channeling orders to companies such as Safran and Airbus Aerostructures (Airbus SE).

Regional supply chains are undergoing significant changes. US sponge restarts and Polish forging capacity expansions reduce trans-Atlantic dependencies, while Asian governments subsidize forging facilities to enhance strategic autonomy. In the Middle East, aftermarket demand for F-15SA and Rafale fleets remains strong, although limited domestic forging capacity restricts the capture of value. South America remains a niche market, anchored by Brazil's KC-390 program and driven by offset requirements for local content. Overall, shifting production hubs are redistributing growth, while absolute volume increases across all regions reinforce the global diversification of the defense aircraft materials market.

- Howmet Aerospace Inc.

- GKN Aerospace Services Limited

- Safran S.A.

- SIFCO Industries, Inc.

- PJSC VSMPO-AVISMA Corporation

- Mecachrome

- Ducommun Incorporated

- ATI Inc. (Allegheny Technologies Incorporated)

- Airbus Aerostructures (Airbus SE)

- Aernnova Aerospace, S.A.

- Aviagroup Industries

- International Aerospace Manufacturing Pvt. Ltd.

- Hanwha Aerospace Co., Ltd.

- Air Industries Group

- Arrowhead Products, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Defense modernisation budgets rising

- 4.2.2 Lightweight-materials imperative for fuel savings

- 4.2.3 Expanding global MRO demand for ageing fleets

- 4.2.4 On-shoring and recycling to mitigate strategic-metal risk

- 4.2.5 Certified metal additive manufacturing adoption

- 4.2.6 OEM single-aisle production ramp-ups through 2030

- 4.3 Market Restraints

- 4.3.1 Volatility in titanium and super-alloy prices

- 4.3.2 Substitution threat from composites

- 4.3.3 Export-controlled titanium-sponge shortfalls

- 4.3.4 REACH/PFAS bans raising coating costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Fixed-Wing Aircraft

- 5.1.1.1 Combat Aircraft

- 5.1.1.2 Multi-role Aircraft

- 5.1.1.3 Training Aircraft

- 5.1.1.4 Transport Aircraft

- 5.1.1.5 Other Aircraft

- 5.1.2 Rotorcraft

- 5.1.2.1 Multi-Mission Helicopter

- 5.1.2.2 Transport Helicopter

- 5.1.2.3 Other Helicopter

- 5.1.1 Fixed-Wing Aircraft

- 5.2 By Material Type

- 5.2.1 Aluminum Alloys

- 5.2.2 High-Strength Steels

- 5.2.3 Titanium Alloys

- 5.2.4 Composite Materials

- 5.2.5 Super-alloys and Refractory Metals

- 5.2.6 Specialty Polymers and Adhesives

- 5.3 By Component

- 5.3.1 Airframe Structures

- 5.3.2 Engine Systems

- 5.3.3 Avionics and Electronics Housings

- 5.3.4 Landing Gear and Braking Systems

- 5.3.5 Interior and Seating

- 5.3.6 Coatings, Sealants and Consumables

- 5.4 By End-User Phase

- 5.4.1 Linefit

- 5.4.2 Retrofit

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest OF Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Howmet Aerospace Inc.

- 6.4.2 GKN Aerospace Services Limited

- 6.4.3 Safran S.A.

- 6.4.4 SIFCO Industries, Inc.

- 6.4.5 PJSC VSMPO-AVISMA Corporation

- 6.4.6 Mecachrome

- 6.4.7 Ducommun Incorporated

- 6.4.8 ATI Inc. (Allegheny Technologies Incorporated)

- 6.4.9 Airbus Aerostructures (Airbus SE)

- 6.4.10 Aernnova Aerospace, S.A.

- 6.4.11 Aviagroup Industries

- 6.4.12 International Aerospace Manufacturing Pvt. Ltd.

- 6.4.13 Hanwha Aerospace Co., Ltd.

- 6.4.14 Air Industries Group

- 6.4.15 Arrowhead Products, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment