|

시장보고서

상품코드

2061528

자율주행차 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Autonomous (Driverless) Cars - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

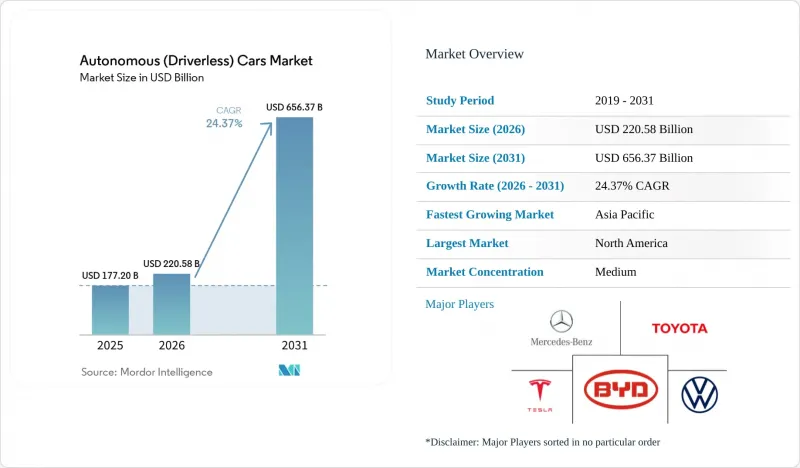

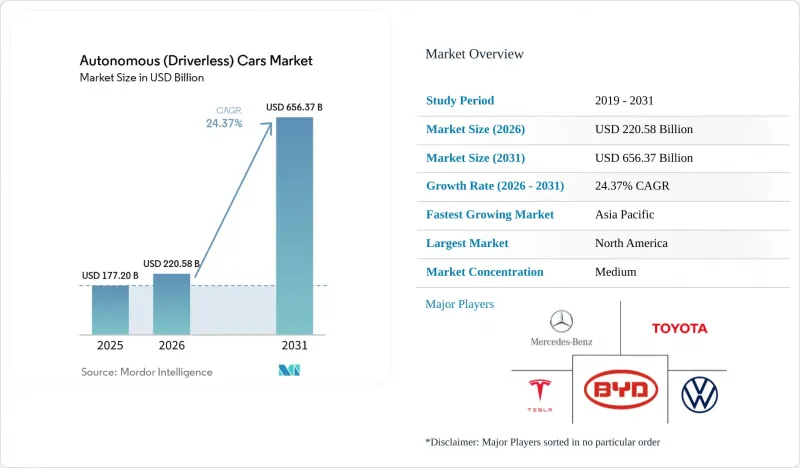

Mordor Intelligence에 의하면, 자율주행차 시장 규모는 2025년 1,772억 달러로 평가되었고, 2026년에는 2,205억 8,000만 달러로 추정되고, 2031년까지 6,563억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) 중 연평균 성장률은 24.37%를 보일 전망입니다.

본 보고서는 자동화 수준별(레벨 1, 레벨 2, 레벨 3 및 그 이상), 차종별(해치백, 세단, SUV, MPV), 구동 방식별(ICE, BEV, HEV), 모빌리티 형태별(개인 소유, 공유), 구성 요소별(하드웨어, 소프트웨어, 서비스) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(대수)으로 제시되어 있습니다.

세계의 자율주행차(무인차) 시장 동향 및 인사이트

아시아의 메가시티에서 로봇 택시 시범 운영의 급속한 확대

2024년 하반기, 바이두의 ‘Apollo Go’는 중국 내 여러 도시에서 누적 탑승 횟수 측면에서 중요한 이정표를 달성했습니다. 한편, Waymo는 피닉스와 샌프란시스코 두 도시에서 매주 상당한 수의 유료 승차 기록을 세우고 있었습니다. 2025년 4월, 도쿄도는 도로교통법을 개정하여 특정 지역에서의 레벨 4 자율주행 도입의 길을 열었습니다. 이러한 움직임에 따라, 자동차 업계의 거물인 도요타와 닛산은 시범 사업의 일정을 앞당겼습니다. Waymo의 단위 경제성은 개선되는 추세를 보이고 있으며, 해당 기업의 평균 승차 비용은 경쟁력 있는 수준으로 낮아졌습니다. 이와 동시에 바이두는 2024년 말까지 우한에서 기여 이익이 흑자로 전환되었다고 발표했습니다. 게다가, 이 지역의 지자체는 서유럽 지자체에 비해 상업용 라이선스 발급에 적극적인 태도를 보이고 있으며, 그 결과 단기적인 성장이 현저히 가속화되고 있습니다.

EU 및 중국의 ADAS 중심 안전 규제에 관한 정부의 의무화 조치

유럽연합(EU)은 2024년 7월 규정 2019/2144를 시행하여, 모든 신형 승용차에 자동 긴급 제동 시스템, 지능형 속도 보조 시스템, 차선 유지 보조 시스템 및 운전자 모니터링 시스템의 장착을 의무화했습니다. 중국은 GB/T 40429-2021을 공표하고, 2024년에 베이징과 선전에서 여러 건의 레벨 3 운행 허가를 발급했습니다. 이를 통해 핸즈프리 고속도로 주행이 단기적으로 달성 가능한 목표로 설정되었습니다. 일본, 한국 및 아세안(ASEAN) 국가들은 유엔 규정 157호를 채택하고 있어, 아시아 전역에서 일관된 규제를 추진하는 동력이 형성되고 있습니다. 이러한 규제의 통합으로 인해 첨단 센서에 대한 수요가 증가하고 단가가 하락함에 따라, 레벨 3 시스템에 투자하는 자동차 제조업체들의 투자 회수 기간이 단축될 것입니다.

미국 내 주별 자율주행차 규제의 차이로 인해 상용화 확대가 지연되고 있습니다.

미국에는 자율주행차를 총괄하는 단일 연방 차원의 체계가 존재하지 않기 때문에 각 기업은 주마다 다른 고유한 규정을 준수해야 합니다. 캘리포니아주는 보행자를 끌고 간 사고를 계기로 Cruise의 허가를 취소했으며, 애리조나주는 특정 지자체 내에서의 상업적 서비스를 제한했습니다. 이러한 규제상의 분절은 규정 준수 프로그램의 중복을 초래하고, 주를 넘나드는 화물 운송의 자동화를 지연시켜, 결과적으로 단기 성장률이 몇 퍼센트 포인트 하락하게 됩니다.

부문별 분석

2025년, 레벨 1 운전 지원 시스템은 자율주행차(무인차) 시장 점유율의 43.47%를 차지했습니다. 이 부문은 자동 긴급 제동 및 차선 유지 보조와 같은 의무화된 기능의 혜택을 받고 있으며, 이러한 기능들은 현재 유럽과 중국의 보급형 모델에 기본 사양으로 탑재되고 있습니다. 레벨 3 조건부 자율주행은 네바다주, 캘리포니아주, 독일 및 일본에서 규제 승인을 받아 프리미엄 모델 중심으로 확대되고 있습니다. 메르세데스-벤츠는 2024년에 ‘드라이브 파일럿’으로 200만 마일의 주행 실적을 기록했으며, BMW는 2026년에 ‘하이웨이 어시스턴트’를 도입할 계획입니다. 이 부문의 변화는 하드웨어의 대중화와 구독형 소프트웨어의 수익화를 보여줍니다.

우한, 피닉스, 도쿄에서 로보택시 서비스 지역이 확대됨에 따라, 레벨 5 완전 자율주행 시장은 2031년까지 연평균 성장률(CAGR) 24.39%로 성장할 것으로 전망됩니다. 자율주행차(무인차) 시장에서는 사업자들이 높은 일일 가동률을 통해 센서 군의 비용을 상각하고, 고정자산을 하루 최대 18시간 동안 수익원으로 전환하고 있는 모습을 볼 수 있습니다. 미들 마일 화물 운송 및 셔틀 서비스에 레벨 4 자율주행 기술을 도입한 것은 지오펜싱된 구역 내에서 상업적 실현 가능성을 입증하고 있습니다. 레벨 3 차량의 구독 모델은 지속적인 수익 창출 가능성을 시사하는 반면, 레벨 5 차량군은 도시 모빌리티의 경제성을 재정의하고 있습니다.

2025년, 자율주행차(무인차) 시장 점유율의 78.81%를 SUV와 MPV가 차지했습니다. 이는 해당 차종들이 가진 높은 루프 라인과 프론트 페시아 덕분에, 외관을 해치지 않으면서도 LiDAR, 레이더, 카메라 어레이를 여유 있게 탑재할 수 있기 때문입니다. Waymo의 재규어 I-PACE와 Baidu의 Apollo Moon은 센서를 널찍하게 배치할 수 있는 SUV 형태를 채택하고 있습니다. 자율주행차 시장에서는 승차 정원과 센서의 발열이 중요한 고려 사항이 되므로, SUV의 우위가 유지될 것입니다.

솔리드 스테이트 LiDAR가 10cm 미만으로 소형화되고, 연산 유닛이 콤팩트한 대시보드 아래에 장착될 수 있게 됨에 따라, 해치백 시장은 2031년까지 연평균 성장률(CAGR) 25.11%로 확대될 것으로 전망됩니다. 자동차 제조업체들은 대량 생산되는 B부문 플랫폼에 자율주행 기술을 도입할 수 있으며, 아시아의 인구 밀도가 높은 도시 지역에서는 갓길 진입이 용이한 소형 차량이 선호됩니다. 테슬라 ‘모델 S’나 루시드 ‘에어’의 도입 사례에서 볼 수 있듯이, 장거리 주행 시 공기역학적 성능과 배터리 효율이 필수적인 상황에서는 세단이 여전히 중요한 역할을 합니다.

지역별 분석

2025년 기준, 북미는 자율주행차(무인차) 시장 점유율의 38.71%를 차지했습니다. Waymo는 미국 4개 도시에서 주당 10만 회 이상의 승차 서비스를 제공하고 있으며, 테슬라는 감독 하에 진행되는 완전 자율주행 프로그램에 다수의 차량을 등록했습니다. 캘리포니아주가 Cruise의 허가를 취소한 이후에도, 규제 간의 차이는 여전히 걸림돌로 남아 있습니다. 그러나 V2X 도로측 장비에 대한 연방 정부의 지출은 주간 고속도로 회랑에서의 자율주행 화물 운송 확대를 뒷받침하고 있습니다. 캐나다의 온타리오주와 퀘벡주에서는 무인 레벨 4 주행 시험이 허용되고 있지만, 대상 차량 수가 적기 때문에 단기적인 도입 대수는 제한적입니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 25.05%를 나타낼 것으로 전망됩니다. 바이두 아폴로 고(Baidu Apollo Go)는 600만 건의 승차라는 이정표를 달성했으며, 포니.ai(Pony.ai)와 오토엑스(AutoX)는 베이징, 광저우, 선전에서 차량 수를 확대했습니다. 일본의 도로교통법 개정에 따라 레벨 4 차량의 지오펜스 구역 내 운행이 허용됨에 따라, 도쿄 오다이바에서 도요타의 시범 사업과 요코하마에서 닛산의 시험 주행이 가능해졌습니다. 인도는 고해상도 지도의 보급률이 향상되고 명확한 규제 체계가 확립되기까지는 아직 초기 단계에 머물러 있지만, 한국에서는 세종시의 전용 차로에서 레벨 4 자율주행 버스에 대한 운행 허가가 내려졌습니다.

유럽에서는 레벨 2 기능을 표준 사양으로 장착하도록 의무화하는 일반 안전 규정의 혜택을 받고 있습니다. 메르세데스-벤츠는 2024년 독일에서 '드라이브 파일럿'을 출시한 데 이어, 네바다주와 캘리포니아주에서도 서비스를 확대했습니다. BMW는 2026년까지 레벨 3 자율주행 기술을 도입하는 것을 목표로 하고 있습니다. 차량의 탈탄소화 관련 규제로 인해 자율주행 전기 트럭의 도입이 가속화되고 있습니다. Einride는 독일, 네덜란드, 스웨덴에서 200대의 무인 트럭을 운행하고 있으며, 볼보는 항만 셔틀용으로 'Vera' 시스템을 도입했습니다. 남미와 중동에서는 틈새 서비스가 시범적으로 도입되고 있지만, 고정밀 지도의 부족과 규제 체계가 미비하여 본격적인 보급에는 차질이 생기고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the autonomous (driverless) cars market size is expected to grow from USD 177.20 billion in 2025 to USD 220.58 billion in 2026, and is forecast to reach USD 656.37 billion by 2031, at a CAGR of 24.37% during the forecast period (2026-2031).

This report is Segmented by Level of Automation (Level 1, Level 2, Level 3, and More), Vehicle Type (Hatchbacks, Sedans, and SUVs and MPVs), Propulsion Type (ICE, BEV, and HEV), Mobility Form (Personal Ownership and Shared Mobility), Component (Hardware, Software, and Services), and Geography. Market Forecasts are Provided in Value (USD) and Volume (Units).

Global Autonomous (Driverless) Cars Market Trends and Insights

Rapid Expansion of Robo-Taxi Pilots across Asian Mega-Cities

In late 2024, Baidu's Apollo Go achieved a significant milestone of cumulative rides across multiple cities in China. Meanwhile, Waymo was recording a substantial number of paid rides weekly in both Phoenix and San Francisco. In April 2025, Tokyo revised its Road Traffic Act, paving the way for Level 4 operations in specific districts. This move prompted automotive giants Toyota and Nissan to hasten their pilot schedules. Waymo's unit economics are on the upswing, with the company's average ride cost dropping to a competitive level. Concurrently, Baidu celebrated achieving positive contribution margins in Wuhan by the end of 2024. Furthermore, municipalities in the region are more amenable to issuing commercial licenses than their Western counterparts, resulting in a notable near-term growth boost.

Government Mandates for ADAS-Centric Safety Regulations in the EU and China

The European Union enforced Regulation 2019/2144 in July 2024, obligating all new passenger vehicles to include autonomous emergency braking, intelligent speed assistance, lane-keeping assist, and driver monitoring systems . China released GB/T 40429-2021 and granted multiple Level 3 permits in Beijing and Shenzhen during 2024, setting hands-free highway operation as an attainable near-term goal . Japan, South Korea, and ASEAN states have adopted UN Regulation 157, creating a contiguous regulatory pull across Asia. The shared compliance calendar increases volume for advanced sensors, reduces per-unit cost, and shortens payback periods for automakers that invest in Level 3 systems.

Patchwork State-Level AV Regulations in the United States Delay Commercial Scale

There is no single federal framework governing autonomous vehicles in the United States; therefore, companies must navigate unique rules in each state. California revoked Cruise permits after a pedestrian-dragging event, and Arizona limited commercial services in certain municipalities. This fragmentation leads to duplicative compliance programs and slows interstate freight automation, resulting in a few percentage points of reduced near-term growth.

Other drivers and restraints analyzed in the detailed report include:

- Falling LiDAR and AI Compute Costs Unlocking Mass-Market Level 3 Launches

- 5G-V2X Corridor Roll-Outs in North American Freight Networks

- Public Mistrust Intensified by High-Profile Robotaxi Incidents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Level 1 driver assistance captured 43.47% of the autonomous (driverless) cars market share in 2025. The segment benefits from mandatory features, such as autonomous emergency braking and lane-keeping assist, which are now standard in entry trims across Europe and China. Level 3 conditional automation is being scaled in premium models following regulatory approvals in Nevada, California, Germany, and Japan. Mercedes-Benz logged 2 million miles on Drive Pilot during 2024, and BMW plans to deploy Highway Assistant in 2026. The segment transition indicates hardware commoditization and the monetization of subscription software.

Level 5 full automation is projected to grow at a 24.39% CAGR through 2031, as robo-taxi fleets in Wuhan, Phoenix, and Tokyo enlarge service areas. The autonomous (driverless) cars market observes operators amortizing sensor suites across high daily utilization, turning fixed assets into revenue generators for up to 18 hours per day. Level 4 deployments in middle-mile freight and shuttle services demonstrate commercial viability in geo-fenced zones. Subscription models in Level 3 vehicles signal recurring revenue potential, while Level 5 fleets redefine the economics of urban mobility.

SUVs and MPVs held 78.81% of the autonomous (driverless) cars market share in 2025 because their larger rooflines and front fascias can comfortably house LiDAR, radar, and camera arrays without aesthetic trade-offs. Waymo's Jaguar I-PACE and Baidu's Apollo Moon rely on sport-utility form factors for roomy sensor placement. The autonomous (driverless) cars market will retain SUV dominance, where passenger capacity and sensor heat dissipation are key considerations.

Hatchbacks are forecast to expand at a 25.11% CAGR to 2031 as solid-state LiDAR shrinks below 10 centimeters and compute units fit under compact dashboards. Automakers can bring autonomy to high-volume B-segment platforms, and dense Asian cities favor compact dimensions for easier curb access. Sedans remain relevant where long-range aerodynamics and battery efficiency are essential, as seen in the Tesla Model S and Lucid Air deployments.

Geography Analysis

North America generated 38.71% of the autonomous (driverless) cars market share in 2025. Waymo operated more than a lakh weekly rides across four United States cities, and Tesla enrolled multiple vehicles in its supervised Full Self-Driving program. Regulatory fragmentation remains a hurdle after California revoked Cruise's permits; however, federal spending on V2X roadside units supports autonomous freight deployment on interstate corridors. Canada allows Level 4 testing without safety drivers in Ontario and Quebec, but its smaller addressable fleet tempers near-term volume.

Asia Pacific is projected to register a 25.05% CAGR through 2031. Baidu Apollo Go crossed the 6 million ride milestone, and Pony.ai plus AutoX expanded fleets in Beijing, Guangzhou, and Shenzhen. Japan's Road Traffic Act revision allows Level 4 vehicles to operate within geofenced districts, enabling Toyota's pilots in Tokyo's Odaiba and Nissan's trials in Yokohama. India remains nascent until HD mapping density improves and a clear regulatory framework emerges, while South Korea grants Level 4 permits for autonomous buses on dedicated lanes in Sejong City.

Europe benefits from the General Safety Regulation that mandates Level 2 features as standard. Mercedes-Benz launched Drive Pilot in Germany in 2024, followed by Nevada and California. BMW targets a Level 3 rollout by 2026. Fleet decarbonization rules are accelerating the adoption of autonomous electric trucks. Einride has deployed 200 driverless trucks across Germany, the Netherlands, and Sweden, while Volvo introduced the Vera system for port shuttles. South America and the Middle East pilot niche services, yet sparse HD maps and evolving rules delay broader scale.

- Waymo LLC

- Tesla, Inc.

- General Motors Co. (Cruise LLC)

- Baidu Inc. (Apollo)

- Toyota Motor Corporation

- Volkswagen AG

- Mercedes-Benz Group AG

- BMW AG

- Nissan Motor Co. Ltd.

- AB Volvo

- Hyundai Motor Group

- BYD Auto Co., Ltd.

- Pony.ai Inc.

- AutoX Inc.

- Uber Technologies Inc.

- Aptiv PLC

- Mobileye Global Inc.

- NVIDIA Corporation

- Magna International Inc.

- Continental AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Robo-Taxi Pilots across Asian Mega-Cities

- 4.2.2 Government Mandates for ADAS-Centric Safety Regulations in the EU and China

- 4.2.3 Falling LiDAR and AI Compute Costs Unlocking Mass-Market L3 Launches

- 4.2.4 5G-V2X Corridor Roll-outs in North American Freight Networks

- 4.2.5 Power-Efficient Automotive SoCs Enabling In-Vehicle Edge AI

- 4.2.6 Fleet Decarbonization Targets Accelerating Autonomous Middle-Mile Logistics in Europe

- 4.3 Market Restraints

- 4.3.1 Patchwork State-Level AV Regulations in the United States Delay Commercial Scale

- 4.3.2 Public Mistrust Intensified by High-Profile Robotaxi Incidents in China

- 4.3.3 Automotive-Grade AI Chip Shortages and Fab Capacity Constraints

- 4.3.4 High-Definition Map Maintenance Costs in Emerging Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Level of Automation

- 5.1.1 Level 1- Driver Assistance

- 5.1.2 Level 2 - Partial Automation

- 5.1.3 Level 3 - Conditional Automation

- 5.1.4 Level 4 - High Automation

- 5.1.5 Level 5 - Full Automation

- 5.2 By Vehicle Type

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 Sport Utility Vehicles (SUVs) and Multi-Purpose Vehicles (MPVs)

- 5.3 By Propulsion Type

- 5.3.1 Internal Combustion Engine (ICE)

- 5.3.2 Battery Electric Vehicles (BEV)

- 5.3.3 Hybrid Electric Vehicles (HEV)

- 5.4 By Mobility Form

- 5.4.1 Personal Ownership

- 5.4.2 Shared Mobility (Robo-Taxi, Shuttle)

- 5.5 By Component

- 5.5.1 Hardware

- 5.5.1.1 Sensors (LiDAR, RADAR, Cameras, Ultrasonic, IMU)

- 5.5.1.2 Computing Platforms (SoCs, GPUs)

- 5.5.1.3 Actuators and Control Systems

- 5.5.2 Software

- 5.5.2.1 Perception and Planning Suites

- 5.5.2.2 Mapping and Localization Engines

- 5.5.2.3 Driver Monitoring and HMI

- 5.5.3 Services

- 5.5.3.1 Integration and Validation

- 5.5.3.2 Remote Operation and Tele-operation

- 5.5.1 Hardware

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Waymo LLC

- 6.4.2 Tesla, Inc.

- 6.4.3 General Motors Co. (Cruise LLC)

- 6.4.4 Baidu Inc. (Apollo)

- 6.4.5 Toyota Motor Corporation

- 6.4.6 Volkswagen AG

- 6.4.7 Mercedes-Benz Group AG

- 6.4.8 BMW AG

- 6.4.9 Nissan Motor Co. Ltd.

- 6.4.10 AB Volvo

- 6.4.11 Hyundai Motor Group

- 6.4.12 BYD Auto Co., Ltd.

- 6.4.13 Pony.ai Inc.

- 6.4.14 AutoX Inc.

- 6.4.15 Uber Technologies Inc.

- 6.4.16 Aptiv PLC

- 6.4.17 Mobileye Global Inc.

- 6.4.18 NVIDIA Corporation

- 6.4.19 Magna International Inc.

- 6.4.20 Continental AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment