|

시장보고서

상품코드

2061534

체외막 산소 공급(ECMO) 시스템 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Extracorporeal Membrane Oxygenation (ECMO) System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

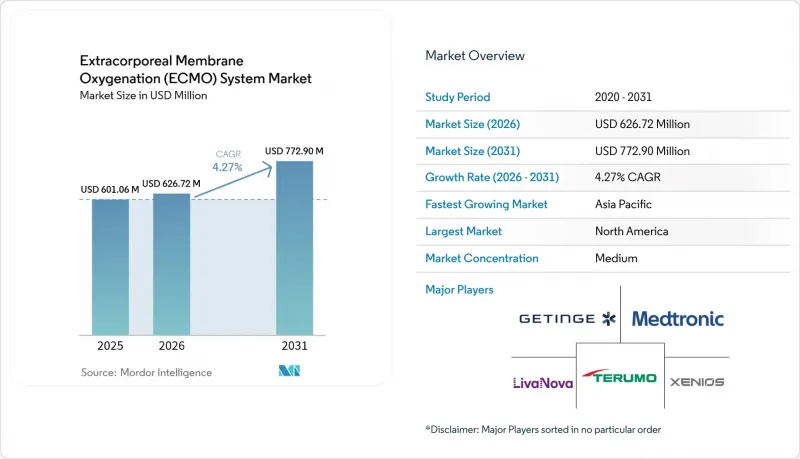

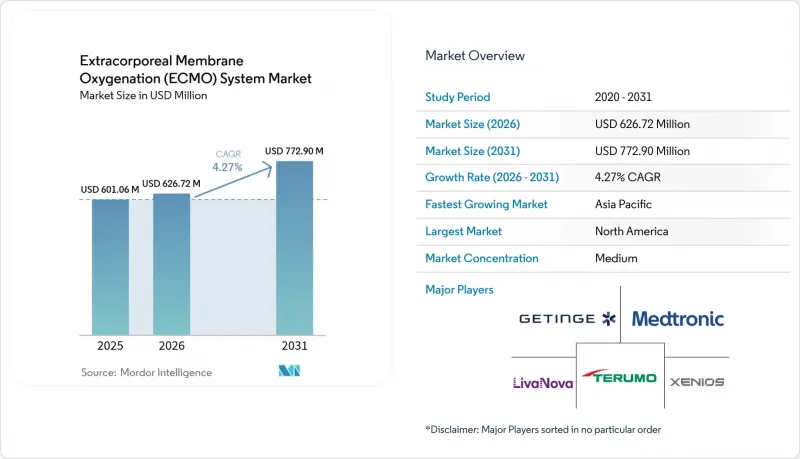

체외막 산소 공급(ECMO) 시스템 시장 규모는 2025년 6억 106만 달러로 평가되었고, 2026년에는 6억 2,672만 달러로 추정되고, 2026-2031년 CAGR 4.27%로 성장을 지속할 전망이며, 2031년에는 7억 7,290만 달러에 이를 것으로 예측됩니다.

본 보고서는 모달리티별(정맥-동맥(VA), 정맥-정맥(VV) 등), 구성 요소별(콘솔 및 펌프, 산소 발생기 등), 적응증별(호흡 부전 등), 연령대별(신생아, 성인 등), 최종 사용자별(3차 의료 병원 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 체외막 산소 공급(ECMO) 시스템 시장 동향 및 분석

전 세계적으로 증가하는 중증 급성 심폐부전 발생률

고령화 사회, 장시간 앉아 있는 생활 습관, 그리고 만성 질환 유병률 증가로 인해, 기존의 치료법을 최적화하더라도 난치성 심부전이나 폐부전으로 진행되는 환자들이 끊임없이 발생하고 있습니다. 코로나19의 유행은 인공호흡 전략이 생리학적 한계에 도달했을 때 ECMO가 수행하는 역할을 부각시켰으며, 등록 자료를 통해 체외식 지원이 필요한 급성 호흡곤란 증후군(ARDS) 사례 수가 지속적으로 보고되고 있습니다. 동시에, 심근경색 후 심원성 쇼크에 대해 정맥-동맥 우회로를 도입하는 의료기관이 늘어나고 있으며, 선진국과 개발도상국 모두에서 그 활용이 더욱 확대되고 있습니다.

끊임없는 기술 혁신을 통해, 콤팩트하고 통합된 ECMO 플랫폼이 구현되었습니다.

최신 장비는 펌프, 센서, 터치스크린 인터페이스를 통합하여, 병상 옆이나 구급차의 좁은 공간에도 들어갈 수 있는 슬림한 카트에 장착되어 있습니다. 메드트로닉의 VitalFlow 시스템은 단 40mL의 프라이밍 용량으로 작동하면서도, 성인에게 충분한 유량과 통합된 가스 교환 모니터링 기능을 제공합니다. 자기 부상식 펌프는 용혈을 최소화하며, AI 기반 대시보드는 혈전 형성 및 신경학적 사건을 높은 정확도로 예측합니다. 이러한 발전으로 인해 사용 문턱이 낮아지고, 병원 간 이송이 더욱 안전해짐에 따라 체외막 산소 공급(ECMO) 시스템 시장이 확대되고 있습니다.

훈련을 받은 ECMO 및 중환자 치료 담당자의 만성적인 부족

2025년에는 전 세계 간호사 부족 인원이 590만 명에 달한 것으로 평가되었고, ECMO 전문가 공급은 더욱 부족해지고 있습니다. 이는 인증 자격 취득에 최소 2년의 중환자실 근무 경력이 요구되기 때문입니다. 시뮬레이션을 기반으로 한 교육 과정 덕분에 기술 습득 기간은 단축되었지만, 신흥 시장에서는 여전히 인재 확보와 유지에 어려움을 겪고 있습니다. 간호사가 주도하는 ECMO 프로그램을 통해 미국의 일부 의료기관에서는 인력 배치 예산을 52% 절감할 수 있었지만, 이를 위해서는 강력한 조직적 지원이 필수적입니다.

부문별 분석

2025년 기준으로, 정맥-동맥형 ECMO는 체외막 산소 공급(ECMO) 시스템 시장의 54.60%를 차지했으며, 이는 심장과 폐를 모두 지원할 수 있는 다용도성을 반영한 것입니다. 쇼크나 외과적 분리 시나리오에서 시술 건수는 꾸준히 증가하고 있지만, 정맥-정맥형 구성의 연평균 성장률(CAGR)이 10.40%로 예측된다는 점은 순수한 호흡 구명 치료로의 전환을 시사합니다. 코로나19에 대한 연구 결과를 바탕으로 급성 호흡곤란 증후군(ARDS)의 치료 알고리즘이 재검토되는 가운데, 정맥-정맥 회로 방식의 체외막 산소 공급(ECMO) 시스템 시장 규모는 2031년까지 3억 5,870만 달러에 달할 것으로 전망됩니다. 현재 의료기관에서는 환자의 운동 능력을 유지하고 기관내 튜브를 제거하기 위해 '각성 상태 ECMO'를 도입하고 있으며, 이를 통해 인공호흡기 관련 폐렴의 위험을 줄이는 동시에 중환자실 입원 기간을 단축하고 있습니다.

정맥-동맥-정맥(VAV) 하이브리드 방식은 복잡한 혼합 부전을 치료하지만, 캐뉼라 삽입이 까다롭고 모니터링 요구 사항도 높기 때문에 여전히 틈새 시장으로 남아 있습니다. 레지스트리 분석에 따르면, 생존율의 추가적인 향상이 더 높은 출혈 위험을 정당화할 수 있는지에 대한 의문이 제기되고 있으며, 이러한 논쟁이 단기적인 도입을 저해할 가능성이 있습니다. 그럼에도 불구하고, 듀얼 루멘 캐뉼라 및 좌심실 부하 경감 기술의 혁신으로 인해 혈역학적 관리가 용이해짐에 따라, VA-ECMO의 성장이 다시 가속화될 가능성이 있습니다.

산소 발생기는 5-7일마다 정기적으로 교체해야 하기 때문에 2025년 매출 점유율은 29.60%로 정체되었지만, 병원이 올인원 워크스테이션으로의 업그레이드를 추진함에 따라 콘솔 및 원심 펌프 시장은 연평균 성장률(CAGR) 11.80%로 확대될 것으로 예측됩니다. 현재 각 벤더사는 가스 믹서, 온도 제어 및 혈역학 대시보드를 통합하고 있으며, 이를 통해 교체 주기를 연장함으로써 업셀링을 효과적으로 실현하고 있습니다. 펌프 기반 체외막 산소 공급(ECMO) 시스템 시장 규모는 2031년까지 2억 8,230만 달러에 달할 것으로 추정되며, 자기 부상식 임펠러를 통해 용혈 및 유지보수로 인한 가동 중단 시간이 줄어듭니다.

벽면 산소 배관이 필요 없는 새로운 이중실식 가스 교환기는 ICU의 인프라 비용을 절감하고, 자원이 제한된 환경에서도 도입이 가능하게 할 수 있습니다. 생체적합성 폴리머 코팅은 혈소판 활성화를 억제하여 산소화기의 수명을 연장하고 소모품 비용을 절감합니다. 이러한 변화로 인해 애프터마켓의 수익은 소폭 감소할 수도 있겠지만, 전반적인 보급은 촉진될 것입니다.

지역별 분석

북미는 2025년 기준 체외막 산소 공급(ECMO) 시스템 시장의 38.40%를 차지했으며, 안정적인 보험 급여, 성숙한 장기 이식 생태계, 그리고 250개 이상의 ELSO 등록 센터에 힘입어 성장하고 있습니다. 미국의 병원에서는 명확한 메디케어 청구 코드가 제공되므로, 관리자들은 추가적인 시스템 구축이나 전문 인력에 대한 자금 지원에 확신을 가지고 있습니다. 캐나다의 각 주에서는 허브 앤 스포크 방식을 채택하여, 이동 의료팀을 지역 중환자실(ICU)에 파견함으로써 자원을 최적화하고 공평한 접근성을 유지하고 있습니다.

아시아태평양은 가장 성장세가 두드러지는 지역으로, 2031년까지 연평균 성장률(CAGR)이 10.30%를 나타낼 것으로 전망됩니다. 중국은 코로나19 기간 동안 수천 대의 장비를 도입하여 국내 생산을 활성화했으며, 현재는 동남아시아 주변 시장에 공급하고 있습니다. 인도의 민간 병원 체인은 확대되는 중산층 심장 질환 환자층을 치료하고 있으며, 수입된 생명 유지 장치에 대한 유리한 세제 덕분에 교체 주기가 단축되고 있습니다. 일본에서는 고령화와 국민건강보험 제도가 도입을 뒷받침하고 있지만, 예산 측면에서는 근거에 기반한 적응증이 중시되고 있어 도입 대수 증가세는 제한되고 있습니다.

유럽에서는 각국의 공적 의료 서비스가 비용 절감을 위해 환자 선별을 엄격히 검토하는 가운데, 안정적인 한 자릿수 중반대의 성장률을 보이고 있습니다. 독일에는 100곳 이상의 ECMO 거점이 운영되고 있는 반면, 영국에서는 환자를 5개의 고환자수 센터로 집중시키고 있으며, 바이러스성 급성 호흡곤란 증후군(ARDS)의 생존율은 55%로 보고되고 있습니다. 중동에서는 아랍에미리트(UAE)와 사우디아라비아에 도입이 집중되어 있으며, 이들 국가에서는 정부계 펀드가 첨단 심장 의료시설에 자금을 지원하고 있습니다. 라틴아메리카에서는 브라질이나 아르헨티나 등 도입이 진행되고 있는 지역이 있지만, 통화 변동과 수입 관세가 성장을 저해하고 있습니다. 아프리카에서는 남아프리카공화국과 이집트를 제외한 지역에서의 도입은 아직 초기 단계에 있으며, 설비 투자 비용과 퍼퓨전 전문가 부족으로 인해 제약을 받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the extracorporeal membrane oxygenation system market size is expected to grow from USD 601.06 million in 2025 to USD 626.72 million in 2026 and is forecast to reach USD 772.9 million by 2031 at 4.27% CAGR over 2026-2031.

This report is Segmented by Modality (Veno-Arterial [VA], Veno-Venous [VV], and More), Component (Console / Pump, Oxygenator, and More), Application (Respiratory Failure, and More), Age Group (Neonates, Adults, and More), End User (Tertiary Care Hospitals, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Extracorporeal Membrane Oxygenation (ECMO) System Market Trends and Insights

Escalating Global Incidence of Severe Acute Cardio-Pulmonary Failure

Aging societies, sedentary lifestyles, and higher chronic disease prevalence create a steady flow of patients who progress to refractory heart or lung failure despite optimized conventional care. COVID-19 highlighted ECMO's role when ventilatory strategies reached physiological limits, and registries continue to report sustained ARDS caseloads that require extracorporeal support. Concurrently, more centers are deploying veno-arterial circuits for cardiogenic shock following myocardial infarction, further boosting utilization in both developed and developing regions.

Continuous Technological Innovations Delivering Compact, Integrated ECMO Platforms

Modern devices integrate pumps, sensors, and touchscreen interfaces into slimline carts that fit bedside or ambulance footprints. Medtronic's VitalFlow system runs on only 40 mL priming volume yet delivers full adult flows and integrated gas exchange monitoring. Magnetically levitated pumps minimize hemolysis, while AI-based dashboards predict clot formation and neurological events with high accuracy. These advances shrink the learning curve and make inter-facility transport safer, broadening the extracorporeal membrane oxygenation system market.

Persistent Shortage of Trained Perfusion And Critical-Care Personnel

Worldwide nursing deficits reached 5.9 million positions in 2025, and the pipeline for ECMO specialists is even tighter because certification demands at least 2 years of ICU experience. Simulation-based curricula shorten upskilling, yet emerging markets still struggle to attract or retain talent. Nurse-led ECMO programs have trimmed staffing budgets by 52% in some U.S. centers but depend on robust institutional support.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Reimbursement & Funding Mechanisms Across Developed Markets

- Rapid Growth of Advanced ICU Infrastructure In High-Population Emerging Economies

- Clinical Complications And Medicolegal Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Veno-arterial ECMO retained 54.60% of the extracorporeal membrane oxygenation system market in 2025, reflecting its dual heart-lung support versatility. Procedure volumes rise steadily in shock and surgical weaning scenarios, yet the 10.40% CAGR expected for veno-venous configurations signals a pivot toward pure respiratory rescue. The extracorporeal membrane oxygenation system market size for veno-venous circuits is projected to hit USD 358.7 million by 2031 as evidence from COVID-19 resets ARDS treatment algorithms. Centers now employ "awake ECMO" to keep patients mobilized and extubated, reducing ventilator-associated pneumonia risk while shortening ICU stays.

Veno-arterial-venous (VAV) hybrids treat complex mixed failures but remain niche because cannulation is intricate and monitoring demands are high. Registry analyses question if additional survival gains justify the higher bleeding risks, a debate likely to temper near-term adoption. Nonetheless, innovation in dual-lumen cannulas and left-ventricular unloading may refresh VA-ECMO growth by easing hemodynamic management.

Oxygenators locked in a 29.60% revenue share in 2025 due to recurring replacements every 5-7 days, but consoles and centrifugal pumps are forecast to expand at 11.80% CAGR as hospitals upgrade to all-in-one workstations. Vendors now integrate gas mixers, thermal control, and hemodynamic dashboards, effectively upselling replacement cycles. The extracorporeal membrane oxygenation system market size for pumps is estimated to reach USD 282.3 million by 2031, with magnetically levitated impellers reducing hemolysis and maintenance downtime.

Novel dual-chamber gas exchangers that forgo wall oxygen lines could cut ICU infrastructure costs, opening low-resource settings. Biocompatible polymer coatings diminish platelet activation, extending oxygenator life and lowering consumable costs, a shift that may slightly erode aftermarket revenues but boost overall adoption.

Geography Analysis

North America held 38.40% of the extracorporeal membrane oxygenation system market in 2025, buoyed by robust reimbursement, a mature organ-transplant ecosystem, and more than 250 ELSO-registered centers. U.S. hospitals enjoy clear Medicare billing codes, giving administrators confidence to fund additional circuits and specialized staff. Canadian provinces follow a hub-and-spoke model that dispatches mobile teams to regional ICUs, optimizing asset utilization and maintaining equitable access.

Asia-Pacific is the fastest-growing region with a projected 10.30% CAGR through 2031. China deployed thousands of units during COVID-19, sparking domestic manufacturing that now supplies peripheral markets in Southeast Asia. India's private hospital chains treat an expanding middle-class cardiac cohort, and favorable taxation on imported life-support equipment shortens replacement cycles. Japanese aging demographics and universal coverage encourage adoption, though budgets emphasize evidence-driven indications, keeping volume growth disciplined.

Europe posted steady mid-single-digit growth as national health services refine patient selection to cap costs. Germany operates 100-plus ECMO hubs, while the United Kingdom consolidated caseloads into five high-volume centers that report 55% survival in viral ARDS. Middle East adoption clusters in United Arab Emirates and Saudi Arabia, where sovereign wealth funds finance advanced cardiac institutes. Latin America shows pockets of uptake in Brazil and Argentina, although currency volatility and import tariffs temper growth. Africa's adoption remains nascent outside South Africa and Egypt, limited by capital costs and perfusionist scarcity.

- Getinge

- Medtronic

- LivaNova

- Terumo

- Fresenius Medical Care (Xenios)

- Eurosets Srl

- Abbott Laboratories

- MicroPort

- Nipro

- OriGen Biomedical

- Inspira Technologies OXY B.H.N.

- Abiomed (Johnson & Johnson MedTech)

- Hemovent GmbH

- Senko Medical Instrument

- Braile Biomedica

- Andocor NV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Incidence of Severe Acute Cardio-Pulmonary Failure

- 4.2.2 Continuous Technological Innovations Delivering Compact, Integrated ECMO Platforms

- 4.2.3 Expansion of Reimbursement & Funding Mechanisms across Developed Markets

- 4.2.4 Rapid Growth of Advanced ICU Infrastructure in High-Population Emerging Economies

- 4.2.5 Increasing Evidence Base Demonstrating Improved Survival & Cost-effectiveness

- 4.2.6 Formal Inclusion of ECMO in National and International Critical-Care Guidelines

- 4.3 Market Restraints

- 4.3.1 Persistent Shortage of Trained Perfusion and Critical-Care Personnel

- 4.3.2 Complex, Lengthy Regulatory Compliance for Class III Extracorporeal Devices

- 4.3.3 Clinical Complications and Medicolegal Risks Associated with ECMO Therapy

- 4.3.4 High Capital, Consumables and Lifecycle Costs of ECMO Therapy

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porters Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Modality

- 5.1.1 Veno-Arterial (VA)

- 5.1.2 Veno-Venous (VV)

- 5.1.3 Veno-Arterial-Venous (VAV)

- 5.2 By Component

- 5.2.1 Console / Pump

- 5.2.2 Oxygenator

- 5.2.3 Heat Exchanger

- 5.2.4 Cannulae & Tubing Sets

- 5.2.5 Sensors & Controllers

- 5.3 By Application

- 5.3.1 Respiratory Failure

- 5.3.2 Cardiac Failure

- 5.3.3 Extracorporeal CPR (ECPR)

- 5.4 By Age Group

- 5.4.1 Neonates

- 5.4.2 Pediatrics

- 5.4.3 Adults

- 5.5 By End User

- 5.5.1 Tertiary Care Hospitals

- 5.5.2 Specialty & Cardio-Thoracic Clinics

- 5.5.3 Emergency Care Units

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Getinge AB

- 6.3.2 Medtronic plc

- 6.3.3 LivaNova PLC

- 6.3.4 Terumo Corporation

- 6.3.5 Fresenius Medical Care (Xenios)

- 6.3.6 Eurosets Srl

- 6.3.7 Abbott Laboratories

- 6.3.8 MicroPort Scientific

- 6.3.9 Nipro Corporation

- 6.3.10 OriGen Biomedical

- 6.3.11 Inspira Technologies OXY B.H.N.

- 6.3.12 Abiomed (Johnson & Johnson MedTech)

- 6.3.13 Hemovent GmbH

- 6.3.14 Senko Medical Instrument

- 6.3.15 Braile Biomedica

- 6.3.16 Andocor NV

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment