|

시장보고서

상품코드

2061535

남미의 난소암 진단 및 치료 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)South America Ovarian Cancer Diagnostics And Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

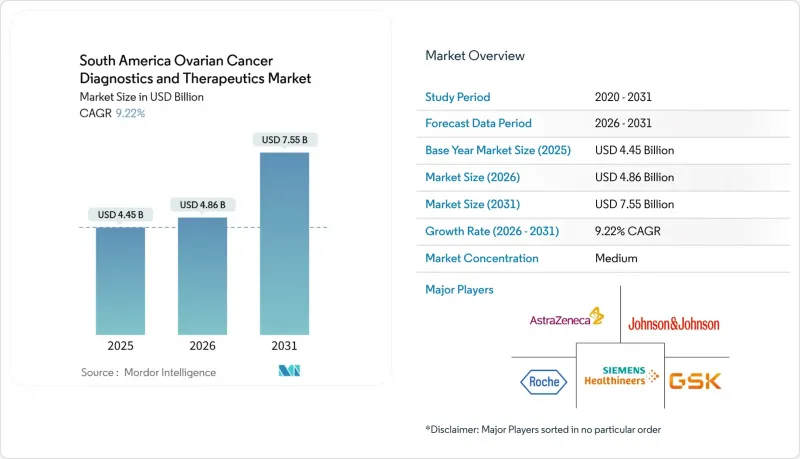

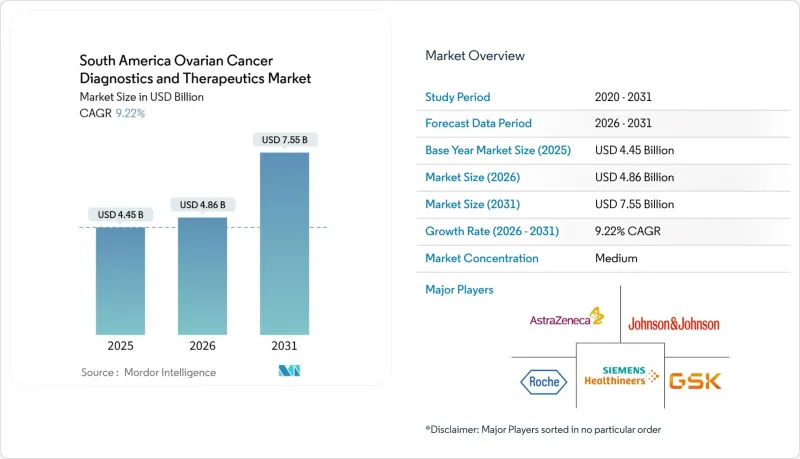

Mordor Intelligence에 의하면, 남미의 난소암 진단 및 치료 시장 규모는 2025년 44억 5,000만 달러로 평가되었고, 2026년 48억 6,000만 달러로 추정되고, 2031년까지 75억 5,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 9.22%를 나타낼 것으로 예측됩니다.

본 보고서는 암 유형별(상피성 난소종양 등), 진단법별(생검 등), 치료법별(화학요법, 방사선 요법, 표적 요법 등), 최종 사용자별(병원, 암 전문센터 등) 및 지역별(브라질, 아르헨티나 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

남미의 난소암 진단 및 치료 시장 동향과 인사이트

난소암 발병률 증가

안데스 지역 국가들에서는 난소암의 연령 조정 발병률이 연평균 2.1%에서 2.7%의 속도로 증가하고 있으며, 이는 세계 평균을 상회하는 수치입니다. 2022년 브라질에서는 7,710건의 새로운 난소암 진단 사례가 보고되었으며, 2030년까지 연평균 9% 증가세가 예상됩니다. 이러한 예측은 체계적인 선별 접근 방식이 아닌, 기회를 포착하는 선별 접근 방식이 지속적으로 채택되고 있기 때문입니다. 진단된 사례의 60% 이상이 FIGO 3기 또는 4기 상태를 유지하고 있으며, 전체 생존 기간은 32개월에 그치고 있습니다. 이 진행 단계에서의 진단으로 인해, 백금 제제를 이용한 화학요법이나 1차 치료제로서의 PARP 억제제를 이용한 유지 요법에 대한 수요가 크게 증가하고 있습니다. 이 문제에 대처하기 위해 각국의 보건부는 위험군별 선별 검사 프로그램의 시범 운영을 진행하고 있습니다. 예를 들어, 칠레의 유전성 암 등록 제도에서는 BRCA 유전자 보유자를 예방적 수술로 직접 연결하는 시스템이 도입되어 있습니다. 각 제약사는 이 지역을 신약 출시의 우선 지역으로 삼고 있으며, 그 예로 브라질에서 올라팔리브의 승인이 미국보다 8개월 빨랐다는 점을 들 수 있습니다.

고령 여성 인구 증가

2035년까지 남미의 65세 이상 여성 비율은 2025년의 8.1%에서 11.3%로 증가할 것으로 예측됩니다. 난소암 발병 위험은 55세에서 74세 사이에 정점에 달하므로, 고령화가 진행됨에 따라 신규 환자 수와 유지 요법 기간이 모두 증가할 것으로 예측됩니다. 이에 대응하여 3차 의료기관에서는 다제 병용이나 허약과 같은 과제에 대처하기 위해 노인종양과를 설치하고 있습니다. 또한, 기존의 입원 화학요법보다 경구 표적 치료제나 외래에서의 정맥 주사 요법이 우선시되고 있습니다. 평균 수명의 연장에 따라, 정기 검진도 증가하고 있습니다. CA-125의 정기적인 측정 및 액체 생검이 보험 적용 대상이 됨에 따라, 영상 검사에서 진행이 확인되기 전에 생화학적 재발을 조기에 발견할 수 있게 되었습니다.

인식 부족으로 인한 진행기 진단

페루와 콜롬비아의 지방 지역에서는 증상 관련 인식 제고 캠페인의 도달률이 여성의 35% 미만에 그치고 있습니다. 이러한 낮은 도달률로 인해 진단까지의 지연 기간 중앙값은 7.2개월로, 상파울루나 부에노스아이레스와 같은 대도시권에서 관찰된 수치의 2배 이상에 달할 전망입니다. 4기 진단을 받은 환자들은 대개 종양 감량술의 대상이 되지 못하며, 주로 장기간에 걸친 항암치료나 완화 치료로 인해 치료비가 2.8배나 더 많이 드는 상황에 직면하고 있습니다. 칠레에서는 지역 보건 요원을 활용한 시범 프로그램에서 가능성을 엿볼 수 있지만, 지속 가능한 자금 조달이라는 과제는 여전히 해결되지 않은 상태입니다.

부문별 분석

2025년 기준으로 상피성 종양은 남미 난소암 진단 및 치료 시장 매출의 68.67%를 차지했으며, 2031년까지 연평균 성장률(CAGR)은 11.5%를 나타낼 것으로 전망됩니다. 상피성 암의 절반 이상을 차지하는 고악성도 장액성 암은 BRCA 및 HRD 유병률이 가장 높으며, 이로 인해 PARP 억제제의 사용이 촉진되고 있습니다. PI3K 및 AKT 억제제에 대한 현지 임상시험이 활발해지고 있으며, 특히 명세포형 및 자궁내막형 변이형에서 그 효과가 두드러집니다. 현재 브라질에서는 알페리시브를 사용한 2상 임상시험이 환자 180명을 대상으로 진행되고 있습니다.

분자 수준에서의 세분화가 진행됨에 따라, 치료 알고리즘이 더욱 정교해질 것으로 예측됩니다. 종합적인 유전체 프로파일링의 도입이 확대됨에 따라, 종양 전문의는 PIK3CA, ARID1A, PTEN 등 치료 대상이 되는 변이를 특정할 수 있게 되었으며, 표적 치료제의 병용을 통한 치료 기회가 생겨나고 있습니다. 환자 지원 단체는 실험적 치료에 대한 접근성을 높이기 위해, 특정 아형에 초점을 맞춘 임상시험의 참여 기준을 적극적으로 추진하고 있습니다.

혈액 기반 CA-125 검사는 여전히 진단 워크플로의 핵심을 이루고 있으며, 2025년 매출의 34.45%를 차지했습니다. 그러나 난소암을 대상으로 한 최초의 종합적 ctDNA 검사인 Guardant360 CDx가 승인됨에 따라, 액체 생검 검사가 보급되면서 그 우위는 점차 줄어들고 있으며, 액체 생검 검사 시장은 연평균 성장률(CAGR) 12.80%로 성장하고 있습니다. 남미의 액체 생검 플랫폼 시장은 침습적인 조직 재생검 없이도 내성 변이를 검출할 수 있는 능력에 힘입어, 2031년까지 9억 5,000만 달러에 육박할 것으로 전망됩니다.

차세대 염기서열 분석 역량을 확대하기 위해 검사 기관 네트워크 통합이 진행되고 있으며, 주요 기업들은 상파울루나 부에노스아이레스 등 주요 거점에 첨단 시스템을 도입하고 있습니다. 또한, 보험사가 분자 검사를 동반 요법과 함께 처리하는 사례가 늘어나고 있으며, 이것이 보급을 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the south america ovarian cancer diagnostics and therapeutics market size is projected to expand from USD 4.45 billion in 2025 and USD 4.86 billion in 2026 to USD 7.55 billion by 2031, registering a CAGR of 9.22% between 2026 to 2031.

This report is Segmented by Cancer Type (Epithelial Ovarian Tumors, and More, Diagnostic Modality (Biopsy, and More)), Therapeutic Modality (Chemotherapy, Radiation Therapy, Targeted Therapy, and More), End User (Hospitals, Cancer Specialty Centers, and More), and Geography (Brazil, Argentina, and More). The Market Forecasts are Provided in Terms of Value (USD).

South America Ovarian Cancer Diagnostics And Therapeutics Market Trends and Insights

Increasing Incidences of Ovarian Cancer

In Andean nations, age-standardized incidence rates of ovarian cancer are rising at an annual rate between 2.1% and 2.7%, surpassing the global average. In 2022, Brazil reported 7,710 new ovarian cancer diagnoses and anticipates a 9% yearly increase through 2030. This projection is driven by the continued adoption of opportunistic rather than systematic screening approaches. Over 60% of diagnosed cases remain at FIGO stages III or IV, limiting overall survival to 32 months. This late-stage diagnosis has significantly increased the demand for platinum-based chemotherapy and first-line PARP inhibitor maintenance treatments. To address this, health ministries are piloting risk-stratified screening programs. For instance, Chile's hereditary registry now connects BRCA carriers directly to prophylactic surgeries. Pharmaceutical companies are prioritizing the region for drug launches, as evidenced by the eight-month approval lead for olaparib in Brazil compared to the United States.

Rising Geriatric Female Population

By 2035, the percentage of South American women aged 65 and older is projected to rise from 8.1% in 2025 to 11.3%. Since the risk of ovarian cancer peaks between ages 55 and 74, this growing elderly demographic is expected to increase both the number of incident cases and the duration of maintenance therapy. In response, tertiary centers are establishing geriatric oncology units to address challenges like polypharmacy and frailty, favoring oral targeted agents and outpatient infusions over traditional inpatient chemotherapy. With longer life expectancies, there is also a rise in surveillance testing. Serial CA-125 assays and liquid biopsies are now reimbursed, enabling earlier detection of biochemical recurrences before they progress to imaging.

Low Awareness Leading to Late-Stage Diagnosis

In rural Peru and Colombia, symptom-awareness campaigns reach fewer than 35% of women. This limited reach results in a median diagnostic delay of 7.2 months, more than double that observed in metropolitan Sao Paulo and Buenos Aires. Patients diagnosed at Stage IV are often ineligible for cytoreductive surgery and face treatment costs that are 2.8 times higher, primarily due to extended chemotherapy and palliative care. While Chile's pilot program utilizing community health workers shows potential, the issue of sustainable funding remains unresolved.

Other drivers and restraints analyzed in the detailed report include:

- Growing Healthcare Expenditure & Insurance Coverage

- Rapid Uptake of PARP Inhibitors & Other Targeted Therapies

- High Cost of Targeted Drugs & Companion Diagnostics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epithelial tumors accounted for 68.67% of South America's ovarian cancer diagnostics and therapeutics market revenue in 2025, with an anticipated growth rate of 11.5% CAGR through 2031. High-grade serous carcinoma, representing over half of all epithelial diagnoses, demonstrates the highest prevalence of BRCA and HRD, driving the adoption of PARP inhibitors. Local trials for PI3K and AKT inhibitors are gaining momentum, particularly for clear-cell and endometrioid variants, with alpelisib currently in a phase II study in Brazil involving 180 patients.

Ongoing molecular segmentation is expected to further refine treatment algorithms. The increasing adoption of comprehensive genomic profiling enables oncologists to identify actionable mutations such as PIK3CA, ARID1A, and PTEN, creating opportunities for targeted therapy combinations. Advocacy groups are actively promoting subtype-specific clinical-trial enrollment criteria to accelerate access to experimental treatments.

Blood-based CA-125 assays remain a cornerstone of diagnostic workflows, contributing 34.45% of 2025's revenue. However, their dominance is diminishing as liquid-biopsy assays gain traction, growing at a 12.80% CAGR following the approval of Guardant360 CDx, the first comprehensive ctDNA test for ovarian cancer. The market for liquid-biopsy platforms in South America is projected to approach USD 950 million by 2031, driven by their ability to detect resistance mutations without the need for invasive tissue re-biopsies.

Laboratory networks are consolidating to scale next-generation sequencing capabilities, with major players deploying advanced systems in key locations such as Sao Paulo and Buenos Aires. Additionally, payers are increasingly bundling reimbursements for molecular testing with companion therapeutics, facilitating broader adoption.

List of Companies Covered in this Report:

- Abbvie

- AstraZeneca

- Bio-Rad Laboratories

- Boehringer Ingelheim

- Bristol-Myers Squibb

- Clovis Oncology, Inc.

- Danaher Corp. (Beckman Coulter)

- Eli Lilly and Company

- Roche

- GE HealthCare Technologies Inc.

- GlaxoSmithKline

- Guardant Health, Inc.

- Hologic

- Illumina

- ImmunoGen, Inc.

- Johnson & Johnson

- Merck

- Myriad Genetics

- Novartis

- Pfizer

- QIAGEN

- Quest Diagnostics

- Siemens Healthineers

- TESARO (a GSK company)

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidences of Ovarian Cancer

- 4.2.2 Rising Geriatric Female Population

- 4.2.3 Growing Healthcare Expenditure & Insurance Coverage

- 4.2.4 Rapid Uptake of PARP Inhibitors & Other Targeted Therapies

- 4.2.5 Expansion of BRCA/HRD Testing Reimbursement Programs

- 4.2.6 On-Shoring of Oncology API Manufacturing Following 2025 Tariff Shifts

- 4.3 Market Restraints

- 4.3.1 Low Awareness Leading to Late-Stage Diagnosis

- 4.3.2 High Cost of Targeted Drugs & Companion Diagnostics

- 4.3.3 Pathology Workforce Shortages Causing Biomarker Test Delays

- 4.3.4 Fragmented Reimbursement for Companion Diagnostics Vs. Drugs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Cancer Type

- 5.1.1 Epithelial Ovarian Tumors

- 5.1.2 Ovarian Germ Cell Tumors

- 5.1.3 Others

- 5.2 By Diagnostic Modality

- 5.2.1 Biopsy

- 5.2.2 Blood Tests

- 5.2.3 Ultrasound

- 5.2.4 PET

- 5.2.5 CT Scan

- 5.2.6 MRI

- 5.2.7 Liquid Biopsy (ctDNA)

- 5.2.8 Other Diagnostics

- 5.3 By Therapeutic Modality

- 5.3.1 Chemotherapy

- 5.3.2 Radiation Therapy

- 5.3.3 Targeted Therapy

- 5.3.4 Immunotherapy

- 5.3.5 Hormonal Therapy

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Cancer Specialty Centers

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Ambulatory Surgical Centers

- 5.4.5 Research Institutes

- 5.5 By Geography

- 5.5.1 Brazil

- 5.5.2 Argentina

- 5.5.3 Colombia

- 5.5.4 Chile

- 5.5.5 Peru

- 5.5.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 AstraZeneca plc

- 6.3.3 Bio-Rad Laboratories, Inc.

- 6.3.4 Boehringer Ingelheim GmbH

- 6.3.5 Bristol-Myers Squibb Company

- 6.3.6 Clovis Oncology, Inc.

- 6.3.7 Danaher Corp. (Beckman Coulter)

- 6.3.8 Eli Lilly and Company

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 GE HealthCare Technologies Inc.

- 6.3.11 GSK plc

- 6.3.12 Guardant Health, Inc.

- 6.3.13 Hologic, Inc.

- 6.3.14 Illumina, Inc.

- 6.3.15 ImmunoGen, Inc.

- 6.3.16 Johnson & Johnson Services, Inc.

- 6.3.17 Merck & Co., Inc.

- 6.3.18 Myriad Genetics, Inc.

- 6.3.19 Novartis AG

- 6.3.20 Pfizer Inc.

- 6.3.21 QIAGEN N.V.

- 6.3.22 Quest Diagnostics Incorporated

- 6.3.23 Siemens Healthineers AG

- 6.3.24 TESARO (a GSK company)

- 6.3.25 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment