|

시장보고서

상품코드

2061538

이탈리아의 호흡기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Italy Respiratory Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

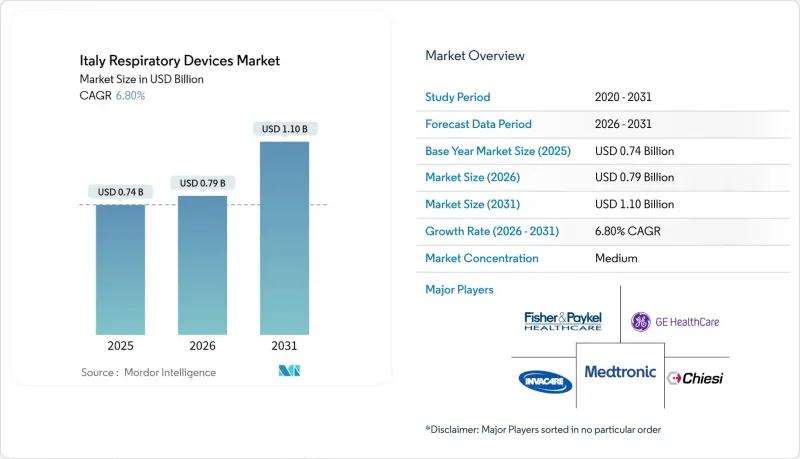

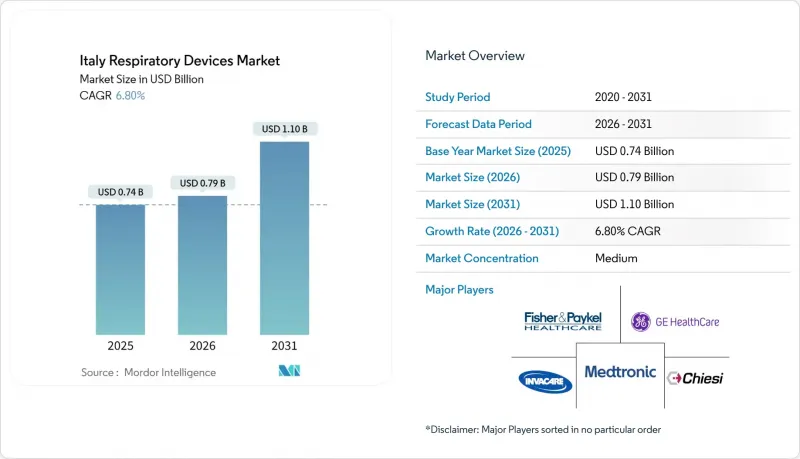

Mordor Intelligence에 의하면, 이탈리아의 호흡기 시장 규모는 2025년에 7억 4,000만 달러로 평가되었습니다. 2026년에 7억 9,000만 달러에 달하고, 2031년까지 11억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 6.80%를 나타낼 것으로 전망됩니다.

본 보고서는 기기 유형(진단·모니터링, 치료용, 일회용), 질환별(COPD, 천식, 수면무호흡증후군, 폐렴 등), 연령대(성인, 고령자, 소아), 최종 사용자(병원 및 클리닉, 재택의료, 당일 수술센터 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

이탈리아의 호흡기 시장 동향 및 인사이트

만성 호흡기 질환(COPD, 천식, OSA)의 유병률 증가

이탈리아에서는 COPD나 천식을 앓고 있는 사람이 총 650만 명에 달하며, 중등도에서 중증의 수면무호흡증 사례 중 약 80%가 진단받지 못한 채로 남아 있습니다. 2023/2024년 겨울에는 SARS-CoV-2와 인플루엔자 바이러스의 동시 유행으로 인해, 고령층의 급성 악화로 인한 입원이 급증했습니다. RSV(호흡기 세포융합 바이러스)만으로도 60세 이상 시민을 대상으로 매년 약 2만 6,000건의 입원과 1,800명의 사망을 초래하고 있어, 조기 발견 도구와 호흡 지원 시스템의 필요성이 부각되고 있습니다. 가정용 수면 검사의 확대와 CPAP 기기의 보험 적용 범위 확대로 인해 잠재적 수요가 현실화될 것으로 예상되며, 호흡기 시장 전체에서 진단용 수면 다원검사 기록기 및 자동 조절식 양압 호흡기 출하 대수가 증가할 것으로 전망됩니다.

재택 호흡 지원 및 원격 모니터링의 도입 확대

‘국가 부흥·회복탄력성 계획’에서는 디지털 모니터링 플랫폼을 갖춘 1차 의료 거점에 47억 5,000만 유로(51억 달러)를 배정하고 있습니다. 이 플랫폼은 실시간 맥박 산소 포화도, 폐활량 측정 및 CPAP 준수 데이터를 호흡기 전문의에게 전송합니다. 롬바르디아주의 COD19 프로젝트에서 연결형 맥박 산소 측정기와 채팅 기반의 간호사 트리아지를 도입한 결과, COPD로 인한 재입원률이 20% 감소했습니다. 2025년 이탈리아의 150개 보험사를 대상으로 실시된 조사에서는 보상 관련 불명확성과 개인정보 보호 규정 준수가 주요 장애 요인으로 부각되었으며, 국가 조달 기준과 명확한 데이터 거버넌스 규정이 확립된다면 보다 신속한 보급이 가능할 것으로 시사되었습니다.

첨단 의료기기의 높은 초기 비용과 제한된 보험 급여

휴대용 산소 농축기, 적응형 서보 환기 시스템 및 연결형 네뷸라이저의 가격은 1,500-8,000유로이지만, 이탈리아 국립 보건 서비스(SSN)의 경우 엄격하게 정의된 적응증에 대해서만 일부가 보상됩니다. 중등도 질환을 앓고 있는 환자들은 본인 부담으로 치료를 받거나 치료를 미루는 경우가 많아, 이로 인해 호흡기 시장의 성장이 주춤하고 있습니다. 행정 절차의 복잡성, 여러 가지 승인 서류, 전문의 소개, 연례 재인증과 같은 요건들은 디지털 활용 능력이 제한적인 고령자들의 이용을 저해하고 있으며, 기기 사용에 있어 양극화를 조장하고 있습니다.

부문별 분석

2025년 매출의 47.67%는 치료용 기기가 차지했습니다. 이는 병원이 중환자실용 인공호흡기를 교체하고, 재택 간호 서비스 업체들이 CPAP 대여 프로그램을 확대했기 때문입니다. 한편, 일회용 제품은 연평균 성장률(CAGR) 8.8%를 나타낼 것으로 예측되며, 이는 호흡기 시장의 제품군 중 가장 높은 수치입니다. 단일 환자용 호흡 회로, 항균 HME 필터 및 CPAP 마스크는 분기마다 교체해야 하므로, 예측 가능한 소모품으로서 안정적인 수익원이 되고 있습니다. 진단 제품, 휴대용 폐활량계, 맥박 산소 포화도 측정기, 이산화탄소 측정기가 나머지 시장 점유율을 차지하고 있지만, 원격 모니터링 시범 사업이 개념 검증(PoC) 단계에서 보험 적용 대상인 표준 치료로 전환됨에 따라 그중요성이 커지고 있습니다.

인공호흡기 관련 폐렴에 대한 인식이 높아짐에 따라 일회용 회로를 권장하는 엄격한 병원 프로토콜이 도입되면서, 튜브 길이나 커넥터를 맞춤형으로 제작하는 현지 제조업체에 대한 수요가 증가하고 있습니다. 동시에, 연결형 일회용 제품에는 교체 주기를 추적하는 RFID 칩이 내장되어 있어, 예측 기반의 재주문이 가능합니다. 다국적 기업들은 장비 임대 계약에 일회용 제품을 묶어 판매함으로써, 고객들을 3년에서 5년짜리 계약에 묶어두고 있습니다. 이탈리아의 중소기업들은 신속한 시제품 제작과 맞춤형 서비스를 통해 시장 점유율을 유지하고 있으며, 이를 통해 호흡기 시장에서 세계 공급업체와 국내 공급업체 간의 경쟁 균형이 유지되고 있습니다.

2025년 매출액 중 만성폐쇄성폐질환(COPD)가 여전히 33.34%를 차지했으며, 이는 장기 산소 요법, 네뷸라이저를 통한 기관지 확장제 투여, 그리고 가압식 인공호흡기가 필요한 350만 명 이상의 임상 진단 사례를 반영한 것입니다. 수면무호흡증후군은 2031년까지 연평균 9.58%의 성장률을 보일 것으로 예상되며, 이는 적응증 중 가장 높은 성장률입니다. 재택 수면 다원검사 및 자동 조절식 CPAP 기기에 대한 보험 적용 범위 확대가 이 분야 시장 규모를 견인하고 있습니다. 폐렴이나 바이러스 감염증의 계절적 증가 또한 인공호흡기나 고유량 산소 요법의 구매를 촉진하고 있습니다. 이는 겨울철에 정점을 찍는 일시적인 요인이지만, 코로나19로 인한 중환자실(ICU) 시설 확충 이후에는 정체 상태를 보이고 있습니다.

호흡기학회와 일반 개업의들의 계몽 활동이 강화됨에 따라, 의료기관으로의 조기 의뢰가 늘어나고 있으며, 진단 후 6개월 이내의 CPAP 도입률이 향상되고 있습니다. 한편, 기관지확장증이나 폐섬유증과 같은 새로운 틈새 적응증은 자비적 사용 프로그램을 통해 주목을 받고 있으며, 이는 향후 휴대용 산소 농축기나 진동식 PEP 장치에 대한 수요의 씨앗이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the italy respiratory devices market size is projected to be USD 0.74 billion in 2025, USD 0.79 billion in 2026, and reach USD 1.10 billion by 2031, growing at a CAGR of 6.80% from 2026 to 2031.

This report is Segmented by Device Type (Diagnostic & Monitoring, Therapeutic, Disposables), Disease Indication (COPD, Asthma, Sleep Apnea, Pneumonia, and More), Age (Adult, Geriatric, Pediatric), End-User (Hospitals & Clinics, Home Healthcare, Ascs, and More). Market Forecasts are Provided in Terms of Value (USD).

Italy Respiratory Devices Market Trends and Insights

Increasing Prevalence of Chronic Respiratory Diseases (COPD, Asthma, OSA)

A combined 6.5 million Italians live with COPD or asthma, and an estimated 80% of moderate-to-severe sleep-apnea cases remain undiagnosed. During the 2023/2024 winter, co-circulating SARS-CoV-2 and influenza viruses led to a spike in hospital admissions for acute exacerbations among older adults. RSV alone drives roughly 26,000 hospitalizations and 1,800 deaths each year in citizens aged 60+, underscoring the need for early detection tools and ventilatory support systems. Expanding home-sleep testing and broader reimbursement of CPAP devices are expected to surface latent demand, lifting unit shipments of diagnostic polysomnography recorders and auto-adjusting positive airway pressure devices across the respiratory devices market.

Rising Adoption of Home-Care Respiratory Support & Tele-Monitoring

The National Recovery and Resilience Plan earmarks EUR 4.75 billion (USD 5.1 billion) for primary-care hubs equipped with digital monitoring platforms that push real-time oximetry, spirometry, and CPAP-adherence data to pulmonologists. Lombardy's COD19 project showed a 20% cut in COPD readmissions by deploying connected pulse oximeters and chat-based nurse triage. A 2025 survey of 150 Italian payers highlighted reimbursement ambiguity and privacy compliance as leading obstacles, signaling that national procurement standards and clear data-governance rules will unlock faster scale-up.

High Upfront Cost of Advanced Devices & Limited Reimbursement

Portable oxygen concentrators, adaptive servo-ventilation systems, and connected nebulizers cost EUR 1,500-8,000 but receive partial reimbursement only for narrowly defined indications under Servizio Sanitario Nazionale. Patients with moderate disease often self-finance or delay therapy, dampening unit growth in the respiratory devices market. Administrative complexity, multi-form authorization, specialist referrals, and annual recertification discourage uptake among elderly users with limited digital literacy, perpetuating a two-tier device landscape.

Other drivers and restraints analyzed in the detailed report include:

- EU Climate Policy Driving Switch to Low-GWP Inhalers

- Regional Tele-Health Pilots Accelerating Digital Device Uptake

- Stringent EU-MDR Compliance Timelines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic equipment generated 47.67% of 2025 revenue as hospitals renewed ICU ventilator fleets and home-care providers expanded CPAP rental programs. Disposables, however, are projected to grow at an 8.8% CAGR, the highest among product lines in the respiratory devices market. Single-patient breathing circuits, antibacterial HME filters, and CPAP masks require quarterly replacement, creating a predictable consumables annuity. Diagnostic products, portable spirometers, pulse oximeters, and capnographs capture the remainder but gain relevance as tele-monitoring pilots transition from proof-of-concept to reimbursed standard of care.

Rising awareness of ventilator-associated pneumonia is driving stricter hospital protocols that favor single-use circuits, propelling volume for local converters that customize tubing lengths and connectors. At the same time, connected disposables embed RFID chips that track change intervals, enabling predictive reordering. Multinationals bundle disposables with equipment leases, locking customers into contracts for three to five years. Italian SMEs defend their market share through rapid prototyping and customization, helping the respiratory devices market maintain a competitive balance between global and domestic suppliers.

COPD still accounted for 33.34% of 2025 sales, reflecting over 3.5 million clinically diagnosed cases that require long-term oxygen therapy, nebulized bronchodilators, and pressure support ventilators. Sleep apnea is projected to grow 9.58% annually to 2031, the fastest rate among indications. Expanded reimbursement for home polysomnography and auto-titrating CPAP devices is boosting the market size for this category. Seasonal spikes in pneumonia and viral infections also drive purchases of ventilators and high-flow oxygen, an episodic driver that peaks during winter but has plateaued after COVID-19 ICU upgrades.

Improved awareness campaigns by pulmonology societies and general practitioners lead to earlier referrals, raising CPAP initiation rates within six months of diagnosis. Meanwhile, emerging niche indications such as bronchiectasis and pulmonary fibrosis receive attention through compassionate-use programs that seed future demand for portable oxygen concentrators and oscillatory PEP devices.

List of Companies Covered in this Report:

- Air Liquide

- Allied Healthcare Products

- Breas Medical AB (Fosun Pharma)

- Chiesi Farmaceutici

- Dragerwerk

- Fisher & Paykel Healthcare

- GE Healthcare

- Getinge

- Hamilton Medical

- Invacare

- Koninklijke Philips

- Lowenstein Medical

- Masimo

- Medtronic

- OMRON

- Resmed

- Siare Engineering International Group

- Smiths Medical ( ICU Medical )

- Teleflex

- Vyaire Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Chronic Respiratory Diseases (COPD, Asthma, OSA)

- 4.2.2 Rising Adoption of Home-Care Respiratory Support & Tele-Monitoring

- 4.2.3 Technological Shifts Toward Non-Invasive & Portable Devices

- 4.2.4 Aging Population & High Smoking Rates

- 4.2.5 EU Climate Policy Driving Switch to Low-GWP Inhalers

- 4.2.6 Regional Tele-Health Pilots (E.G., Lombardy) Accelerating Digital Device Uptake

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Advanced Devices & Limited Reimbursement

- 4.3.2 Stringent EU-MDR Compliance Timelines

- 4.3.3 Consolidation of Hospital Tenders Squeezing SME Margins

- 4.3.4 Cyber-Security & Data-Privacy Hurdles for Connected Devices

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 Spirometers

- 5.1.1.2 Sleep Test Devices

- 5.1.1.3 Peak Flow Meters

- 5.1.1.4 Pulse Oximeters

- 5.1.1.5 Capnographs

- 5.1.1.6 Other Diagnostic & Monitoring

- 5.1.2 Therapeutic Devices

- 5.1.2.1 CPAP Devices

- 5.1.2.2 BiPAP Devices

- 5.1.2.3 Humidifiers

- 5.1.2.4 Nebulizers

- 5.1.2.5 Oxygen Concentrators

- 5.1.2.6 Ventilators

- 5.1.2.7 Inhalers

- 5.1.2.8 Other Therapeutic Devices

- 5.1.3 Disposables

- 5.1.3.1 Masks

- 5.1.3.2 Breathing Circuits

- 5.1.3.3 Other Disposables

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Disease Indication

- 5.2.1 COPD

- 5.2.2 Asthma

- 5.2.3 Sleep Apnea

- 5.2.4 Pneumonia & Acute Respiratory Infections

- 5.2.5 Others

- 5.3 By Age

- 5.3.1 Adult

- 5.3.2 Geriatric

- 5.3.3 Pediatric

- 5.4 By End-User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Home Healthcare Settings

- 5.4.3 Ambulatory Surgical Centers

- 5.4.4 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Air Liquide Medical Systems

- 6.3.2 Allied Healthcare Products

- 6.3.3 Breas Medical AB (Fosun Pharma)

- 6.3.4 Chiesi Farmaceutici S.p.A.

- 6.3.5 Dragerwerk AG & Co. KGaA

- 6.3.6 Fisher & Paykel Healthcare

- 6.3.7 GE Healthcare

- 6.3.8 Getinge AB

- 6.3.9 Hamilton Medical AG

- 6.3.10 Invacare Corporation

- 6.3.11 Koninklijke Philips N.V.

- 6.3.12 Lowenstein Medical

- 6.3.13 Masimo Corporation

- 6.3.14 Medtronic plc

- 6.3.15 Omron Healthcare

- 6.3.16 ResMed Inc.

- 6.3.17 Siare Engineering International Group

- 6.3.18 Smiths Medical ( ICU Medical )

- 6.3.19 Teleflex Inc.

- 6.3.20 Vyaire Medical

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment