|

시장보고서

상품코드

2061568

북미의 환자 모니터링 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Patient Monitoring - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

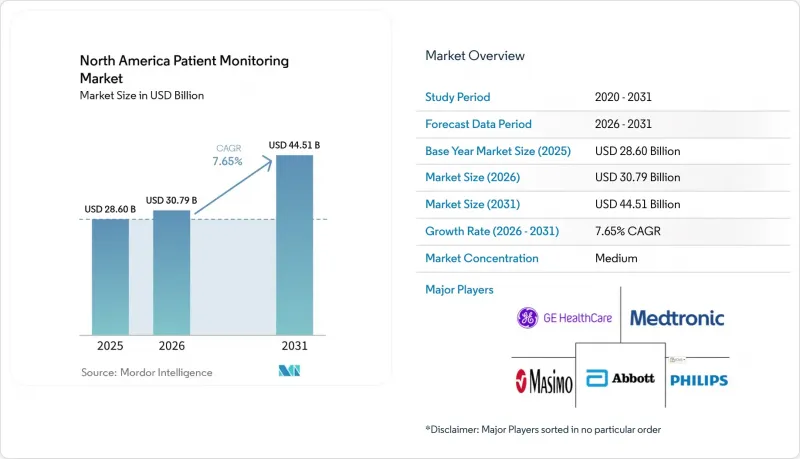

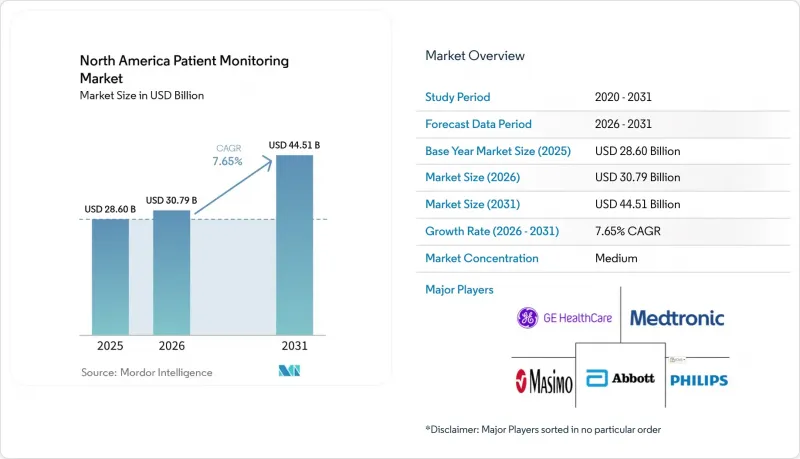

Mordor Intelligence에 의하면, 북미의 환자 모니터링 시장 규모는 2025년에 286억 달러로 평가되었고, 2026년 307억 9,000만 달러로 추정되고, 2031년까지 445억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.65%를 나타낼 전망입니다.

본 보고서는 유형별(기기(혈역학, 신경 모니터링, 심장, 다항목, 기타), 서비스(설치 및 유지보수, 교육 및 훈련, 기타)), 용도별(순환기, 신경, 호흡기, 기타), 최종 사용자별(병원 및 클리닉, 재택치료, 외래 및 전문 의료 센터) 및 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 환자 모니터링 시장 동향 및 인사이트

만성 질환 및 생활습관병의 발생률이 급증

1억 3,300만 명 이상의 미국 성인이 만성 질환을 앓고 있으며, 10명 중 6명이 적어도 한 가지 질환을 관리하고 있어 24시간 모니터링에 대한 수요가 지속되고 있습니다. 85세 이상 인구층에서는 유병률이 더욱 상승하고 있으며, 2024년에는 다중 질환 동반율이 12.3%에 달했고, 돌봄의 복잡성이 가중되었습니다. 지속 혈당 모니터는 이러한 추세를 여실히 보여주고 있습니다. 덱스콤(Dexcom)의 스텔로(Stelo) 센서는 인슐린 사용자 외에도 적용 대상을 확대하여, 2025년 3분기 매출을 21.6% 증가한 12억 1,000만 달러로 끌어올렸습니다. 이에 이어 애보트의 ‘Libre Rio’와 ‘Lingo’가 출시되었으며, 미국 내 2형 당뇨병 환자 3,700만 명을 대상으로 한 도입을 추진했습니다. 보험사가 번들화된 RPM 코드 하에서 여러 질환에 대한 모니터링 비용을 보상하게 됨에 따라, 만성 질환 관리 서비스의 신규 가입자가 늘어날 때마다 북미 환자 모니터링 시장은 확대되고 있습니다.

고령화와 보상 범위 확대

2030년까지 고령자는 북미 인구의 21.6%를 차지하게 될 전망이며, 젊은 성인에 비해 3배에 달하는 모니터링 자원을 소비하게 될 것입니다. CMS는 CPT 99457의 요금을 64.41달러로 인상하고, 20분마다 추가되는 검토에 대해 CPT 99458을 51.52달러로 책정하여, 진료소가 복합적인 동반 질환에 대한 추적 관리를 청구할 수 있도록 했습니다. 캐나다의 '커넥티드 케어 법'도 비슷한 움직임을 보이고 있으며, 온타리오주는 디지털 케어에 연간 8억 3,200만 캐나다 달러(6억 1,500만 달러)를 배정하고 있습니다. TELUS Health의 주 전역 대상 원격 환자 관리(RPM) 프로그램에는 이미 수천 명이 등록했으며, 이는 보상의 확실성이 시범 사업을 주류 업무 프로세스로 전환시킬 수 있음을 입증하고 있습니다.

의료진의 업무 흐름에 대한 거부감과 교육 부담

경고가 지나치게 많이 발생하면 신뢰를 잃게 됩니다. UPMC의 감사 결과, 병동 전체에서 6,560만 건의 경보가 기록되었으며, 이 중 88%가 생리학적 문제가 아닌 기술적 문제였기 때문에 직원의 40-50%가 번아웃을 겪고 있습니다. 모든 플랫폼에 새로운 대시보드, 임계값 및 에스컬레이션 절차를 도입하기 위해 수개월에 걸친 교육이 필요합니다. 에모리 헬스케어의 2025년 가상 간호 프로젝트에서는 6개월간의 교육 과정과 추가 인력 배치가 이루어졌습니다. 소규모 병원의 경우, 집중 관리 센터 설치를 정당화할 만큼의 환자 수가 부족하여, 이로 인해 도입이 제한되고 북미 환자 모니터링 시장의 단기적인 이익이 억제되고 있습니다.

부문별 분석

2025년 매출의 80.18%는 하드웨어가 차지했지만, 서비스 부문은 연평균 성장률(CAGR) 8.22%를 나타낼 것으로 예측되며, 이는 북미 환자 모니터링 시장에서 가장 높은 성장률입니다. 호아그 메모리얼 병원이 Philips사와 체결한 10년 임대 계약이 그 이유를 보여줍니다. 병원은 비용을 분산하고, 업그레이드를 확실하게 수행하며, 막대한 초기 비용을 지불하지 않고도 분석 기능을 확보할 수 있기 때문입니다. 관리형 모니터링, 미들웨어 개발, 트리아지 업무의 아웃소싱은 현재 프리미엄 가격으로 제공이 가능하며, 해당 서비스는 하드웨어의 상품화에 대응하는 전략적 헤지 수단이 되고 있습니다. 점점 더 많은 시스템이 설비 투자(Capex)를 운영 비용(OpEx)으로 전환함에 따라, 북미 환자 모니터링 시장의 서비스 규모는 의료기기 시장보다 더 빠르게 확대될 것으로 전망됩니다.

분석 기능과 커맨드 센터의 운영은 고객 유지율을 높이고 있습니다. 웨스트 테네시 헬스케어는 2025년, eICU 직원으로 중환자 전문의 12명을 추가로 채용하여 지방의 제휴 의료기관에 연중무휴 24시간 모니터링 체계를 제공했습니다. 패리시 헬스케어의 2,500만 달러 규모의 미들웨어 지출은 상호 운용성이 여전히 병목 현상임을 보여줍니다. 독자적인 데이터 표준이 점차 사라지는 가운데, 클라우드 호스팅, 사이버 보안, AI 분석을 통합 제공할 수 있는 업체들이 계약 갱신을 확보하고 있어, 북미 환자 모니터링 시장 전반에서 벤더 종속 현상이 강화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the north america patient monitoring market size was valued at USD 28.60 billion in 2025 and is estimated to grow from USD 30.79 billion in 2026 to reach USD 44.51 billion by 2031, at a CAGR of 7.65% during the forecast period (2026-2031).

This report is Segmented by Type (Device [Hemodynamic, Neuromonitoring, Cardiac, Multi-Parameter, and More] Service [Installation & Maintenance, Training & Education, and More), Application (Cardiology, Neurology, Respiratory, and More), End User (Hospitals & Clinics, Home Healthcare, Ambulatory & Specialty Centers), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America Patient Monitoring Market Trends and Insights

Incidence of Chronic & Lifestyle Diseases Surging

More than 133 million U.S. adults live with chronic illness, and 6 in 10 manage at least one condition, driving sustained demand for round-the-clock monitoring. Prevalence climbs further in the 85-plus cohort, where multi-morbidity reached 12.3% in 2024, intensifying care complexity. Continuous glucose monitors illustrate the trend: Dexcom's Stelo sensor broadened eligibility beyond insulin users, contributing to a 21.6% revenue jump to USD 1.21 billion in Q3 2025. Abbott's Libre Rio and Lingo followed, pushing adoption into the 37 million U.S. Type 2 population. Each new chronic-care enrollee expands the North America patient monitoring market, because payers now reimburse multi-condition oversight under bundled RPM codes.

Ageing Population & Reimbursement Expansion

Seniors will form 21.6% of North America's population by 2030, and they consume triple the monitoring resources of younger adults. CMS lifted CPT 99457 to USD 64.41 and added CPT 99458 at USD 51.52 for every extra 20 minutes of review, letting clinics bill for layered comorbidity tracking. Canada's Connected Care Act mirrors the move, while Ontario earmarks CAD 832 million (USD 615 million) annually for digital care. TELUS Health's province-wide RPM program already enrolls thousands, demonstrating how reimbursement certainty converts pilots into mainstream workflows.

Provider Workflow Resistance & Training Burden

Alarm overload erodes trust: a UPMC audit logged 65.6 million alerts across wards, 88% technical rather than physiologic, fueling burnout in 40-50% of staff. Every platform introduces new dashboards, thresholds, and escalation drills, requiring months of coaching. Emory Healthcare's 2025 virtual-nursing project came with a six-month curriculum and extra staffing. Small hospitals lack volume to justify centralized command centers, limiting adoption and tempering short-run gains in the North America patient monitoring market.

Other drivers and restraints analyzed in the detailed report include:

- Post-COVID Preference for Home & Remote Monitoring

- AI-Enabled Early-Warning Analytics

- High Capital & Integration Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware generated 80.18% of 2025 revenue, yet service lines are forecast to deliver an 8.22% CAGR, the quickest in the North America patient monitoring market. Hoag Memorial's decade-long lease with Philips shows why: hospitals spread payments, lock in upgrades, and secure analytics without large upfront checks. Managed monitoring, middleware development, and triage outsourcing now command premium pricing, turning services into a strategic hedge against hardware commoditization. The North America patient monitoring market size for services is projected to expand faster than devices as more systems convert capex to opex.

Analytics and command-center operations deepen stickiness. West Tennessee Healthcare added 12 intensivists to staff its eICU in 2025, giving rural affiliates 24/7 oversight. Middleware spending, USD 25 million at Parrish Healthcare, shows that interoperability remains a bottleneck. As proprietary data standards fade, vendors able to bundle cloud hosting, cybersecurity, and AI analytics win renewals, reinforcing vendor lock-in across the North America patient monitoring market.

List of Companies Covered in this Report:

- Abbott Laboratories

- Baxter

- Beckton Dickinson

- BIOTRONIK

- Boston Scientific

- Dexcom

- Edward Lifesciences

- GE HealthCare Technologies Inc.

- Honeywell International

- iRhythm Technologies

- Johnson & Johnson

- Koninklijke Philips

- Masimo

- Medtronic

- Nihon Kohden

- Omron Healthcare Co. Ltd.

- Resmed

- Siemens Healthineers

- Teladoc Health

- VitalConnect Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Incidence of Chronic & Lifestyle Diseases Surging

- 4.2.2 Ageing Population & Reimbursement Expansion

- 4.2.3 Post-COVID Preference for Home & Remote Monitoring

- 4.2.4 Ai-Enabled Early-Warning Analytics

- 4.2.5 Shift Toward Single-Use Sensors

- 4.2.6 Federal RPM Code Revisions

- 4.3 Market Restraints

- 4.3.1 Provider Workflow Resistance & Training Burden

- 4.3.2 High Capital & Integration Costs

- 4.3.3 Cyber-Insurance & Section-524B Compliance

- 4.3.4 Clinician Alert-Fatigue

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter?s Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 By Device

- 5.1.1.1 Hemodynamic Monitoring Devices

- 5.1.1.2 Neuromonitoring Devices

- 5.1.1.3 Cardiac Monitoring Devices

- 5.1.1.4 Multi-Parameter Monitors

- 5.1.1.5 Respiratory Monitoring Devices

- 5.1.1.6 Remote Patient Monitoring Devices

- 5.1.1.7 Other Devices

- 5.1.2 By Service

- 5.1.2.1 Installation & Maintenance Services

- 5.1.2.2 Training & Education Services

- 5.1.2.3 Remote Monitoring & Telehealth Services

- 5.1.2.4 Data Integration & Interoperability Services

- 5.1.2.5 Analytics & Reporting Services

- 5.1.2.6 Managed Monitoring Operations & Triage Services

- 5.1.1 By Device

- 5.2 By Application

- 5.2.1 Cardiology

- 5.2.2 Neurology

- 5.2.3 Respiratory

- 5.2.4 Diabetes Management

- 5.2.5 Fetal & Neonatal

- 5.2.6 Weight-Management & Fitness

- 5.2.7 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals & Clinics

- 5.3.2 Home Healthcare

- 5.3.3 Ambulatory & Specialty Centers

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 Baxter International Inc.

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Biotronik SE & Co. KG

- 6.3.5 Boston Scientific Corporation

- 6.3.6 Dexcom Inc.

- 6.3.7 Edwards Lifesciences Corporation

- 6.3.8 GE HealthCare Technologies Inc.

- 6.3.9 Honeywell International Inc.

- 6.3.10 iRhythm Technologies Inc.

- 6.3.11 Johnson & Johnson

- 6.3.12 Koninklijke Philips N.V.

- 6.3.13 Masimo Corporation

- 6.3.14 Medtronic plc

- 6.3.15 Nihon Kohden Corporation

- 6.3.16 Omron Healthcare Co. Ltd.

- 6.3.17 ResMed Inc.

- 6.3.18 Siemens Healthineers GmbH

- 6.3.19 Teladoc Health Inc.

- 6.3.20 VitalConnect Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment