|

시장보고서

상품코드

2061595

지능형 교통 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Intelligent Transport Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

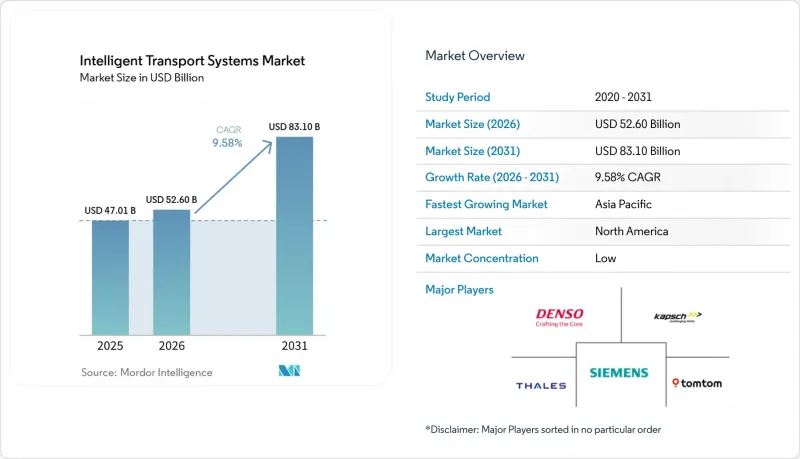

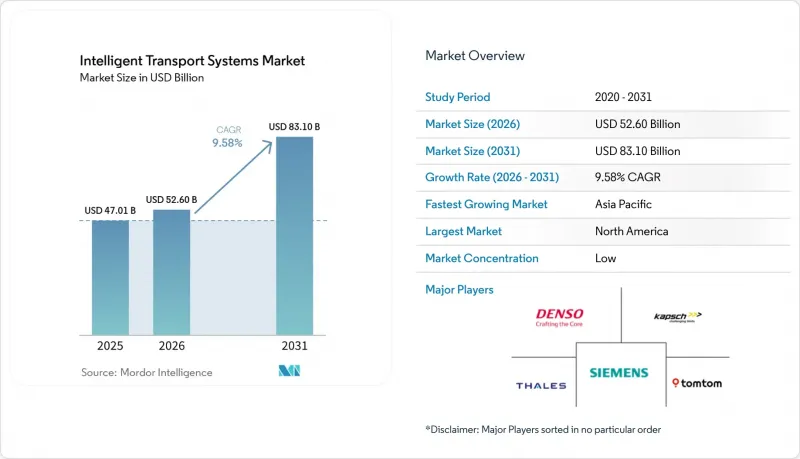

Mordor Intelligence에 의하면, 지능형 교통 시스템(ITS) 시장 규모는 2025년 470억 1,000만 달러로 평가되었습니다. 2026년에는 526억 달러로 확대되어 2031년까지 831억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 9.58%를 나타낼 것으로 전망됩니다.

본 보고서는 운송 수단(도로, 철도 등), 구성 요소(하드웨어, 소프트웨어 등), 유형(ATMS, ATIS 등), 용도(교통 관리 등), 도입 형태(On-Premise, 클라우드 등), 기술(IoT 센서 및 V2X, AI 및 머신러닝 분석 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 지능형 교통 시스템(ITS) 시장 동향 및 분석

정부의 스마트시티 및 교통 안전에 대한 자금 지원이 급증하고 있습니다.

연방 및 초국가적 프로그램을 통해 커넥티드 코리도 구축에 전례 없는 규모의 자금이 투입되고 있습니다. 미국 교통부는 2024년 한 해에만 5,400만 달러 규모의 SMART 보조금을 지원하여, 각 기관이 사후 대응형 교통 계획에서 AI를 활용한 예측형 교통 흐름 제어 방식으로 전환하는 것을 목표로 하고 있습니다. 이와 더불어, EU의 ‘디지털 유럽 프로그램’은 2027년까지 디지털 인프라에 75억 유로를 배정하고 있으며, 지능형 교통 시스템(ITS)은 배출량을 줄이면서 경쟁력을 높이기 위한 핵심 요소로 자리 잡고 있습니다. 애리조나주의 1,960만 달러 규모 V2X 회랑과 같은 주 차원의 노력은 자금이 얼마나 신속하게 수익 창출이 가능한 데이터 자산으로 전환될 수 있는지를 입증하고 있습니다. 과거에는 5년에 달하던 계약 체결 주기가 현재는 2년 이내에 완료되고 있으며, 즉시 도입 가능한 하드웨어와 턴키 방식의 분석 기능을 패키지로 제공하는 벤더가 우대받고 있습니다. 조기 도입 기업들은 다른 지역이 동등한 수준의 센서 밀도를 확보하기 전에 데이터 스트림을 수집함으로써 지속적인 선점 우위를 확보하고 있습니다.

심화되는 도시 지역의 교통 체증이 ATMS 도입을 촉구하고 있습니다.

매일 발생하는 교통 체증으로 인해, 첨단 교통 관리 시스템은 ‘있으면 편리한 것’에서 재정적 필수 사항으로 변모했습니다. 메릴랜드주 앤 아란델 카운티에서 실시된 감사 결과, 교통량이 많은 교차로 한 곳당 이용자들이 연간 32만 4,000달러의 시간 손실과 4만 8,000달러의 추가 연료비를 부담하고 있는 것으로 밝혀졌으며, 이는 ATMS의 신속한 도입을 촉진하는 계기가 되었습니다. 베이징의 ‘차량·도로·클라우드’ 연계 프로그램은 1,200개 교차로의 평균 이동 시간을 15% 단축했으며, 경쟁 관계에 있는 다른 대도시들도 유사한 조치를 취하도록 압박하고 있습니다. 보스턴에서는 AI를 활용한 신호 제어 조정을 통해 도심 주요 교차로에서의 정차 횟수가 30% 감소했습니다. 이는 기존의 제어 장치를 콘크리트로 다시 구축하는 것이 아니라, 소프트웨어를 통해 재사용할 수 있음을 보여줍니다. 철강 및 아스팔트 가격 급등으로 인해 2024년에는 고속도로 건설 비용이 24% 상승했습니다. 이로 인해 예산에 제약이 있는 행정 기관의 경우, 소프트웨어를 통한 최적화가 유일하게 실행 가능한 교통 체증 대책이 되고 있습니다.

막대한 설비 투자와 기존 인프라의 개보수 비용

2024년 고속도로 건설 비용의 연간 인플레이션율은 24%에 달했고, 예산의 실질 가치를 떨어뜨리고 각 기관이 비긴급 업그레이드를 미루게 하는 사태를 초래했습니다. 미국철강협회(AISI)에 따르면, 철강 가격은 11.2% 상승하여 초당적 인프라 법안의 구매력을 약 40% 감소시켰습니다. 코펜하겐의 8,000만 유로 규모 스마트 조명 프로젝트와 같은 대규모 개보수 공사는 여전히 수년에 걸친 투자 회수 기간이 필요하기 때문에 지방채 시장에서는 자금 조달에 어려움을 겪고 있습니다. 그 결과, 많은 기관들이 제어기를 일괄 교체하는 대신 아날로그 제어반의 수명을 연장하는 등, 단계적이고 소프트웨어를 우선시하는 도입 방식으로 방침을 전환하고 있습니다. 통합 비용이 종종 장비 가격을 초과하기 때문에 조달 부서는 현대화 작업을 여러 회계 연도에 걸쳐 분산할 수밖에 없으며, 이로 인해 시스템 전체의 성능 향상이 지연되고 있습니다.

부문별 분석

해운 부문은 2025년 지능형 교통 시스템(ITS) 시장 매출의 6.35%에 불과했으나, 항만 자동화, 디지털 트윈, 자율 주행 예인선 도입에 힘입어 12.86%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 도로 부문은 61.45%의 점유율을 유지하며, 국가 안전 프로그램의 지원을 받아 지능형 교통 시스템(ITS) 시장 규모에서 가장 큰 비중을 차지하고 있습니다. AI 비전 및 5G 통신 기술을 탑재한 부두 크레인에 대한 투자를 통해 선석의 처리 능력이 향상되고, 트럭 운송 차량과의 연계가 강화됨에 따라 컨테이너 체류 시간이 20% 단축됩니다. EHang사의 자율 비행 택시 ‘EH216 S’의 도입은 항공 노선이 지상의 병목 현상을 어떻게 극복할 수 있는지를 보여주고 있지만, 이 하위 분야는 아직 발전 단계에 있습니다. 철도에는 우선 통행권 관리라는 장점이 있습니다. 미국의 화물 철도 사업자는 고장이 발생하기 몇 시간 전에 문제를 감지하는 엣지 분석을 활용해 기관차 고장을 40% 줄였습니다.

미래를 내다보면, 멀티모달 연동을 통해 선박 운항 일정과 철도의 슬롯, 트럭 배차가 조정되어 시스템 전체의 자산 활용도가 향상될 것입니다. 지능형 교통 시스템(ITS) 시장에서는 해운, 철도, 도로의 물류 흐름을 단일 데이터 패브릭으로 모델화하는 솔루션에 대한 평가가 높아지고 있습니다. 중국의 항만 클라우드 플랫폼은 이미 야드 크레인, 게이트 카메라, 세관 데이터베이스를 통합하여 전 세계 확산의 선구자 역할을 하고 있습니다. 도로 프로젝트에서는 현재 신호 타이밍을 대형 트럭에 전송하는 C-V2X 지원 교차로의 시범 운영이 진행 중이며, 이를 통해 공회전으로 인한 연료 소비를 줄이고 있습니다. 이러한 추세가 맞물리면서 자금은 운송 수단 간 화물 균형을 조정하는 소프트웨어 분야로 이동하고 있으며, 이는 출퇴근 시간대의 교통 체증과 배기가스 감축으로 이어지고 있습니다.

2025년 시점에서도 하드웨어는 여전히 매출의 48.55%를 차지했지만, 소프트웨어의 연평균 성장률(CAGR) 13.84%는 시장의 큰 전환점을 보여주었습니다. 각 기관은 진화하는 안전 기준에 대응할 수 있는 유연한 라이선싱 방식을 중시하고 있으며, 영구 라이선스 방식의 컨트롤러는 점차 사라져 가고 있습니다. 소프트웨어 패키지 분야에서는 서비스, 컨설팅, 통합 및 관리형 사이버 보안이 가장 빠르게 성장하고 있으며, 이는 정기적인 장비 교체가 아닌 지속적인 최적화에 대한 수요를 반영하고 있습니다. IoT 노드가 대중화됨에 따라, 지능형 교통 시스템(ITS) 시장 내 하드웨어 점유율은 점차 감소할 것입니다. 도로변 장치(RSU)는 AI 파이프라인에 데이터를 공급하는 단순한 데이터 수집 장치로 변화해 나갈 것입니다.

각 벤더사는 현재 분석 대시보드를 펌웨어 업데이트와 함께 제공함으로써, 일회성 거래를 지속적인 수익원으로 전환하고 있습니다. 엣지 컨테이너를 통해 새로운 알고리즘의 무선(OTA) 배포가 가능해져, 하드웨어 수명을 연장하고 총 소유 비용(TCO)을 절감합니다. 이는 예산이 빠듯한 상황에서 중요한 판매 포인트가 됩니다. 모듈형 게이트웨이가 일체형 캐비닛을 대체함에 따라, 조달 모델은 자본 지출에서 SaaS와 유사한 운영비 모델로 전환됩니다. 그 결과, 선순환이 만들어집니다. 즉, 지속적인 수익이 연구 개발(R&D)에 재투자되어 시스템 성능 향상으로 이어지고, 이는 플랫폼에 대한 고객의 의존도를 더욱 높입니다.

지역별 분석

2025년, 북미는 지능형 교통 시스템(ITS) 시장 매출의 27.65%를 차지했습니다. 2025년도에 620억 달러가 배정된 커넥티드카 관련 연방 보조금 등은 프로젝트의 가시성을 높여주며, 주 차원의 후속 프로젝트를 촉진했습니다. 애리조나주의 1,960만 달러 규모 V2X 회랑 프로젝트는 실현 가능한 투자 수익률(ROI)을 입증하고 있는 반면, 텍사스주 교통국(DOT)이 실시한 C-V2X 교차로 시험은 해당 지역을 인프라와 차량의 융합 분야에서 선도적인 위치로 자리매김하게 했습니다. 지방자치단체의 시범 사업에는 사회적 목표도 포함되어 있습니다. 앨버커키의 마이크로 트랜짓 서비스는 식료품점 접근이 어려운 지역과 식료품점을 연결해 주며, 데이터 기반의 시스템이 형평성 격차를 해소하는 데 어떻게 기여하고 있는지 보여줍니다. 명확한 책임 체계와 풍부한 벤처 캐피털이 엣지 AI 스타트업을 공공 부문 입찰로 끌어들이며, 불투명한 규정을 가진 지역에 비해 사업 확장을 가속화하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 10.16%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 대도시의 교통 체증과 디지털 경제 목표 달성을 위한 정부의 지원이 적극적인 도입 일정을 촉진하고 있습니다. 중국에서 여객 운항 허가를 받은 EHang사의 자율 비행 택시 ‘EHang EH216 S’ 기단은 첨단 항공 모빌리티 분야의 규제 유연성을 여실히 보여주고 있습니다. 베이징의 1,200개 교차로에 구축된 ‘차량·도로·클라우드’ 연계 시스템은 이동 시간을 15% 단축시켰으며, 현재는 국가 표준의 기반이 되고 있습니다. 싱가포르의 10억 싱가포르 달러 규모 AI 펀드와 중국이 2025년까지 달성한 2,000만 대의 NEV(신에너지차) 도입 목표는 공급업체들에게 예측 가능한 수요 곡선을 제공합니다. 로봇 택시 제휴는 시범 운영 규모를 넘어 확대되고 있으며, 선전에서 Pony AI가 체결한 1,000대 규모의 계약은 상용화의 길을 확고히 하고, 분석 엔진에 공급되는 데이터 양을 늘리고 있습니다.

유럽에서는 안전 및 기후 변화와 관련된 조화로운 법규제 하에 꾸준한 확장이 이어지고 있습니다. ‘일반 안전 규정 II’는 ADAS 장비의 탑재를 의무화하고 있으며, 도로 측과 차세대 차량군 간의 데이터 교환을 필수로 규정하고 있습니다. 코펜하겐에서 진행된 8,000만 유로 규모의 스마트 조명 개보수 사업은 55%의 에너지 절감 효과를 달성했으며, ITS 예산이 탄소 배출 감축 목표와 어떻게 부합하는지를 보여주었습니다. 2027년까지 75억 유로가 투입될 EU의 ‘디지털 유럽’ 기금은 디지털 트윈 시범 사업과 국경을 초월한 회랑에 대한 자금 지원을 보장합니다. 지멘스 모빌리티가 독일 철도(Deutsche Bahn)와 체결한 수십억 유로 규모의 계약은 단편적인 업그레이드가 아닌, 턴키 플랫폼의 구매를 의미합니다. 한편, 엄격한 GDPR(EU 개인정보보호규정) 및 AI 투명성 관련 규정은 도입 속도를 늦추는 동시에 국민의 신뢰를 높이고, 시장에서의 지속적인 확산을 촉진하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the intelligent transport systems market size is expected to increase from USD 47.01 billion in 2025 to USD 52.60 billion in 2026 and reach USD 83.10 billion by 2031, growing at a CAGR of 9.58% over 2026-2031.

This report is Segmented by Mode of Transport (Roadways, Railways, and More), Component (Hardware, Software, and More), Type (ATMS, ATIS, and More), Application (Traffic Management, and More), Deployment Mode (On-Premise, Cloud, and More), Technology (IoT Sensors and V2X, AI and Machine-Learning Analytics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Intelligent Transport Systems Market Trends and Insights

Government Smart-City and Traffic-Safety Funding Surge

Federal and supranational programmes are directing unprecedented sums into connected-corridor build-outs. The U.S. Department of Transportation awarded USD 54 million in SMART grants during 2024 alone, aiming to shift agencies from reactive timing plans to predictive, AI-assisted flow control. In parallel, the EU's Digital Europe Programme has earmarked EUR 7.5 billion through 2027 for digital infrastructure, with intelligent transportation systems tagged as a centerpiece because they cut emissions while lifting competitiveness. State-level executions such as Arizona's USD 19.6 million V2X corridor prove how quickly funds translate into assets that produce monetisable data. Contract award cycles that once stretched five years now close inside two, rewarding vendors that package turnkey analytics with shovel-ready hardware. Early adopters gain durable first-mover advantages by harvesting data streams before peer regions possess equivalent sensor density.

Escalating Urban Congestion Demanding ATMS Roll-outs

Daily gridlock has turned advanced traffic management systems from nice-to-have to fiscal necessity. An audit in Anne Arundel County, Maryland found a single busy junction costs users USD 324,000 in lost time and USD 48,000 in excess fuel each year, catalysing rapid ATMS procurement. Beijing's vehicle-road-cloud program has shaved 15% off average trip times across 1,200 intersections, compelling rival megacities to follow suit. Boston's AI-enabled signal adjustments removed 30% of stops at major downtown nodes, showing that legacy controllers can be repurposed via software rather than rebuilt in concrete. Escalating steel and asphalt prices, highway construction costs rose 24% in 2024-leave software optimisation as the only viable congestion remedy for budget-constrained agencies.

High Capex and Legacy Infrastructure Retrofit Costs

Annual highway construction cost inflation reached 24% in 2024, eroding the real value of earmarked budgets and pushing agencies to defer non-critical upgrades. Steel prices rose 11.2%, dampening the purchasing power of the Bipartisan Infrastructure Law by roughly 40%, according to the American Iron and Steel Institute. Large-scale retrofits like Copenhagen's EUR 80 million smart-lighting project still demand multi-year paybacks that municipal bond markets struggle to underwrite. Consequently, many agencies pivot to incremental, software-first deployments that extend the life of analogue cabinets instead of wholesale controller swaps. Integration fees often eclipse device prices, forcing procurement offices to spread modernisation across several fiscal cycles and delaying system-wide performance gains.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Road-Safety Regulations (e-Call, ADAS Integration)

- Edge-Native AI Digital Twins Enabling Real-Time Flow Optimisation

- Rising Cybersecurity-Liability Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The maritime segment captured just 6.35% of Intelligent Transportation Systems market revenue in 2025 but posts the fastest 12.86% CAGR as ports deploy automation, digital twins, and autonomous tugs. Roadways retained 61.45% share, equivalent to the largest slice of the Intelligent Transportation Systems market size, supported by national safety programmes. Investments in quay cranes fitted with AI vision and 5G links improve berth throughput and synchronise with trucking fleets, cutting container dwell time by 20%. EHang's EH216 S autonomous air-taxi rollout illustrates how airways leapfrog ground bottlenecks, although the sub-sector remains nascent. Railways benefit from right-of-way control; U.S. freight operators reduced locomotive failures 40% via edge analytics that flag defects hours before breakdowns.

Looking ahead, cross-modal orchestration aligns sailing schedules with rail slots and truck dispatch, raising asset utilisation system-wide. The Intelligent Transportation Systems market increasingly rewards solutions that model maritime, rail, and road flows in a single data fabric. China's port cloud platforms already integrate yard cranes, gate cameras, and customs databases, foreshadowing global adoption. Roadway projects now pilot C-V2X intersections that broadcast signal timing to heavy-duty trucks, reducing idle fuel. Collectively, these trends shift funding toward software layers that balance freight among modes, lessening peak-hour congestion and emissions.

Hardware still represented 48.55% revenue in 2025, yet software's 13.84% CAGR signals a profound pivot. Agencies value flexible licensing that keeps pace with evolving safety standards, pushing perpetual-license controllers aside. Services, consulting, integration, and managed cybersecurity, expand fastest inside the software bundle, reflecting a need for continuous optimisation rather than periodic box swaps. The Intelligent Transportation Systems market share for hardware will erode as IoT nodes commoditise; roadside units become simple data collectors feeding AI pipelines.

Vendors now bundle analytics dashboards with firmware updates, converting one-time transactions into annuities. Edge containers allow over-the-air deployment of new algorithms that lengthen hardware life and lower total cost of ownership, a key selling point amid budget squeezes. As modular gateways replace monolithic cabinets, procurement shifts from capital outlay to operating-expenditure models akin to SaaS. The outcome is a virtuous cycle: recurring revenue funds R&D that in turn raises system performance, deepening customer dependence on the platform.

Geography Analysis

North America contributed 27.65% of Intelligent Transportation Systems market revenue in 2025. Federal grants, such as the USD 62 billion connected-vehicle earmark for fiscal 2025, stabilise pipeline visibility and spark state-level copycat projects. Arizona's USD 19.6 million V2X corridor demonstrates replicable ROI, while Texas DOT's C-V2X intersection trials position the region as a leader in infrastructure-vehicle fusion. Municipal pilots also layer social goals: Albuquerque's micro-transit service links food deserts to grocers, showing how data-rich systems tackle equity gaps. Clear liability frameworks and deep venture capital pools pull edge-AI startups into public-sector tenders, accelerating rollouts versus regions with opaque rules.

Asia Pacific is the fastest-growing region at a 10.16% CAGR through 2031. Megacity congestion and state backing for digital economy goals push aggressive deployment timetables. China's EHang EH216 S autonomous flying-taxi fleet, cleared for passenger service, underscores regulatory agility in advanced air mobility. Beijing's 1,200-intersection vehicle-road-cloud scheme trimmed travel time 15% and now anchors national standards. Singapore's SGD 1 billion AI reserve and China's 20 million NEV target by 2025 give suppliers predictable demand curves. Robotaxi partnerships scaling beyond pilot fleets, Pony AI's 1,000-vehicle pact in Shenzhen, validate commercialisation pathways and pump data volumes that feed analytics engines.

Europe sustains steady expansion under harmonised safety and climate legislation. The General Safety Regulation II mandates ADAS equipment, compelling roadsides to exchange data with next-generation fleets. Copenhagen's EUR 80 million smart-lighting retrofit achieved 55% energy savings, revealing how ITS budgets align with carbon targets. EU Digital Europe funds of EUR 7.5 billion through 2027 ensure capital availability for digital twin pilots and cross-border corridors. Siemens Mobility's multibillion Euro Deutsche Bahn contract exemplifies turnkey platform purchasing over piecemeal upgrades, while stringent GDPR and AI-transparency rules moderate adoption speed yet raise public trust, fostering durable market adoption.

- Siemens AG

- Thales Group

- IBM Corporation

- Garmin Ltd.

- NoTraffic

- TomTom N.V.

- Cubic Corporation

- Mobileye

- Applied Information

- Denso Corporation

- Cisco Systems Inc.

- Kapsch TrafficCom AG

- Huawei Technologies Co. Ltd.

- Iteris Inc.

- Q-Free ASA

- Swarco AG

- TransCore LP

- Advantech Co. Ltd.

- Continental AG

- Siemens Mobility (Yunex Traffic)

- AtkinsRealis

- Econolite Group Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government smart-city and traffic-safety funding surge

- 4.2.2 Escalating urban congestion demanding ATMS roll-outs

- 4.2.3 Mandatory road-safety regulations (e-Call, ADAS integration)

- 4.2.4 Edge-native AI digital twins enabling real-time flow optimisation

- 4.2.5 Integration of EV-charging assets with ITS platforms

- 4.2.6 Data-monetisation models from connected-vehicle analytics

- 4.3 Market Restraints

- 4.3.1 High capex and legacy infrastructure retrofit costs

- 4.3.2 Interoperability and standards fragmentation across regions

- 4.3.3 Rising cybersecurity-liability compliance costs

- 4.3.4 AI-algorithm transparency rules slowing advanced deployments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Transport

- 5.1.1 Roadways

- 5.1.2 Railways

- 5.1.3 Airways

- 5.1.4 Maritime

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Type

- 5.3.1 Advanced Traffic Management Systems (ATMS)

- 5.3.2 Advanced Traveler Information Systems (ATIS)

- 5.3.3 Advanced Transportation Pricing Systems (ATPS)

- 5.3.4 Advanced Public Transportation Systems (APTS)

- 5.3.5 Advanced Commercial Vehicle Operations (ACVOS)

- 5.3.6 Cooperative Vehicle-Infrastructure Systems (CVIS)

- 5.4 By Application

- 5.4.1 Traffic Management

- 5.4.2 Public Transport and Ticketing

- 5.4.3 Road Safety and Security

- 5.4.4 Freight and Fleet Management

- 5.4.5 Environmental and Emission Monitoring

- 5.4.6 Smart Parking and Guidance

- 5.4.7 Tolling and Congestion Pricing

- 5.4.8 Connected and Autonomous Vehicle (CAV) Support

- 5.4.9 Other Applications

- 5.5 By Deployment Mode

- 5.5.1 On-Premise

- 5.5.2 Cloud

- 5.5.3 Edge / Fog

- 5.6 By Technology

- 5.6.1 IoT Sensors and V2X

- 5.6.2 AI and Machine-Learning Analytics

- 5.6.3 Digital Twin Platforms

- 5.6.4 5G and C-V2X Connectivity

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 United Kingdom

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Egypt

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Siemens AG

- 6.4.2 Thales Group

- 6.4.3 IBM Corporation

- 6.4.4 Garmin Ltd.

- 6.4.5 NoTraffic

- 6.4.6 TomTom N.V.

- 6.4.7 Cubic Corporation

- 6.4.8 Mobileye

- 6.4.9 Applied Information

- 6.4.10 Denso Corporation

- 6.4.11 Cisco Systems Inc.

- 6.4.12 Kapsch TrafficCom AG

- 6.4.13 Huawei Technologies Co. Ltd.

- 6.4.14 Iteris Inc.

- 6.4.15 Q-Free ASA

- 6.4.16 Swarco AG

- 6.4.17 TransCore LP

- 6.4.18 Advantech Co. Ltd.

- 6.4.19 Continental AG

- 6.4.20 Siemens Mobility (Yunex Traffic)

- 6.4.21 AtkinsRealis

- 6.4.22 Econolite Group Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment