|

시장보고서

상품코드

2061608

혈소판 응집 기기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Platelet Aggregation Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

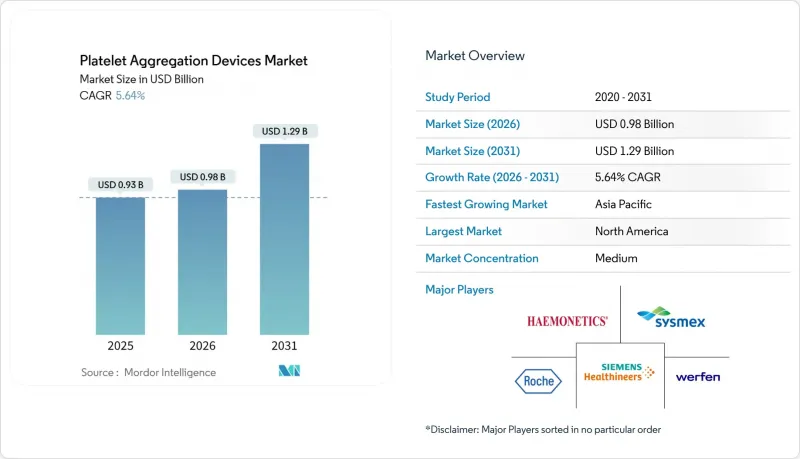

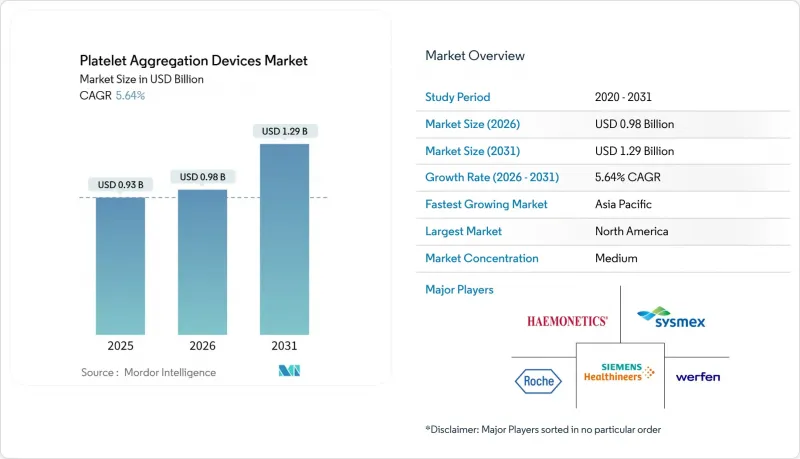

Mordor Intelligence에 의하면, 혈소판 응집 기기 시장 규모는 2025년 9억 3,000만 달러로 평가되었습니다. 2026년 9억 8,000만 달러에서 2031년까지 12억 9,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 5.64%를 나타낼 것으로 예측됩니다.

본 보고서는 제품(시스템, 시약 등), 기술(광투과형 응집 측정법, 임피던스 응집 측정법 등), 검체 유형(혈소판 농축 혈장 등), 용도(임상 진단, 항혈소판 요법 모니터링 등), 최종 사용자(병원, 진단실험실 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 혈소판 응집 기기 시장 동향 및 인사이트

심혈관 질환 및 출혈성 질환의 발생률 증가

심혈관 질환의 유병률은 계속 증가하고 있으며, 병원에서는 정기적인 혈소판 검사 건수를 늘리도록 권고받고 있습니다. 미국심장협회(AHA)는 2050년까지 고혈압 유병률이 61%, 당뇨병 유병률이 26.8%를 나타낼 것으로 예측하고 있으며, 이러한 추세가 혈소판 분석기의 장기적인 활용을 뒷받침하고 있습니다. 또한, 임상팀은 CAR-T 등 혈액학적 치료에서 혈소판 기능 장애의 발생률이 높다는 사실을 확인했으며, 이로 인해 종양학 분야의 복잡한 검사 수요가 더욱 증가하고 있습니다. 이러한 질병 부담의 집중으로 인해 혈소판 응집 측정 기기 시장 전체 수요가 증가하고 있습니다. 미국 및 유럽연합(EU)의 전국 심장병 등록 데이터에 따르면, 2024년부터 2025년에 걸쳐 이중 항혈소판 요법을 받는 환자 수가 8% 증가한 것으로 보고되었습니다. 세계 혈우병 연맹의 관련 자료에 따르면, 2024년에는 혈소판 기능 장애로 진단받은 환자가 41만 8,000명에 달하고, 2022년 대비 12% 증가했습니다. 심장 중재술 전문의는 경피적 관상동맥 중재술(PCI) 전에 클로피도그렐 비반응자를 식별하기 위해 응집 기기를 활용하는 반면, 혈액 전문의는 그란츠만 혈소판 무력증과 같은 유전성 결핍증의 표현형을 확인하기 위해 동일한 플랫폼을 사용하고 있습니다.

고령 인구 증가

유엔의 예측에 따르면, 65세 이상 세계 인구는 2024년 10억 명에서 2050년에는 16억 명에 달할 것으로 전망됩니다. 노화는 내피 기능 장애 및 혈소판 반응성 증가와 관련이 있어, 정형외과 및 신경외과 수술 시 항응고 요법의 관리를 복잡하게 만들고 있습니다. 유럽 및 북미의 노인병동에서는 대퇴골 경부 골절 치료나 뇌졸중 재활 과정에서 항혈소판제의 투여량을 환자별로 맞춤 설정하기 위해 탁상형 혈소판 응집 기기를 도입하기 시작했습니다. 세계에서 가장 고령화된 사회를 지탱하고 있는 일본의 병원에서는 혈전성 사건을 미연에 방지하기 위해 정기적인 외래 진료 시 혈소판 기능 검사를 실시하고 있으며, 이것이 혈소판 응집 측정 기기에 대한 수요를 뒷받침하고 있습니다. 소량의 검체만으로도 충분한 완전 자동화 플랫폼을 제공하는 업체들은 이러한 인구 동향에 따른 수요를 확보하고 있습니다. 왜냐하면 소량의 검체로도 충분하다는 점이 허약한 고령자의 채혈 시 제약 조건과 부합하기 때문입니다.

첨단 시스템에 필요한 고액의 초기 투자 비용 및 소모품 비용

완전 자동 혈소판 응집 워크스테이션의 가격은 12만-18만 달러이며, 연간 유지보수 계약비로 추가로 1만 5,000-2만 5,000달러가 소요됩니다. 소모품 비용은 환자 1인당 12-18달러이지만, 포괄 보상 코드로 환급되는 일반적인 응고 검사에서는 2달러 미만입니다. 한 자릿수 이익률로 운영되는 지역 병원들은 공급업체가 자본 지출을 검사별 비용으로 전환하는 시약 임대 계약을 제공하지 않는 한 투자를 주저하고 있습니다. 3차 의료기관이라 하더라도, 설비투자위원회는 구매를 승인하기 위해 순환기내과, 혈액내과, 수술 전후 관리 부서 등 다양한 직종이 참여한 이용 계획서를 요구합니다. 이러한 비용 측면의 역풍으로 인해, 가격에 민감한 아시아 및 라틴아메리카에서는 혈소판 응집 기기 시장의 연평균 성장률(CAGR)이 1% 가까이 하락했습니다.

부문별 분석

시스템 부문은 2025년 매출의 49.90%를 차지하며, 병원 핵심 검사실에 도입된 광학식 및 임피던스식 분석 장치의 기존 도입 현황을 반영했습니다. 한편, 소모품 및 부속품은 세척으로 인한 가동 중단 시간과 교차 오염 위험을 대폭 줄여주는 일회용 마이크로플루이딕스 디스크에 힘입어, 2031년까지 연평균 성장률(CAGR) 8.90%를 기록하며 혈소판 응집 기기 시장 전체를 상회하는 성장이 예상됩니다. 시약 계약에서는 현재 작용제와 소프트웨어 잠금 해제 코드가 세트로 판매되고 있으며, 과거에는 단발성 하드웨어 판매에 그쳤던 것이 지속적인 수익원으로 전환되었습니다. 검사실이 전혈 임피던스법으로 전환됨에 따라 수요가 새로운 시약 제제로 이동하고 있으며, 이로 인해 공급업체 시장 점유율이 세분화되면서 특수한 작용제를 제공하는 틈새 시장 공급업체에게 진입의 여지가 생기고 있습니다. 캘리브레이터나 피펫 팁 등의 액세서리는 이익률이 낮은 제품이지만, 병원이 인증을 유지하기 위해 제조업체가 검증한 워크플로우를 따라야 하기 때문에 여전히 필수적인 존재입니다.

소모품의 이익률 때문에 공급업체들이 분석기에 드라이블록을 미리 설치하도록 권장하고 있으며, 병원 측은 보증 조건을 충족하기 위해 정품 제조업체로부터만 소모품을 조달할 수밖에 없는 실정입니다. 이러한 락인 전략은 전환 비용을 높임으로써 예측 기간 동안 수익의 가시성을 강화합니다. 지역 유통업체들도 예방 정비 키트를 시약 재주문 기준량과 함께 판매하고 있어, 기기 1대당 연간 지출액이 증가하고 있습니다. 그 결과, 설비 교체 주기가 정체된 성숙한 지역이라 하더라도 소모품에 기인한 혈소판 응집 기기 시장 규모는 꾸준히 확대될 것입니다.

임상 검사는 2025년 매출의 63.50%를 차지했는데, 이는 순환기 전문의와 혈액 전문의가 일상적인 모니터링, 수술 전 위험 평가, 그리고 출혈성 질환의 감별 진단에 응집 측정에 의존하고 있기 때문입니다. 개인 맞춤형 항혈소판 요법에 대한 규제 당국의 장려로 인해 일일 검사 건수가 증가하면서, 카테터 검사실과 뇌졸중 병동에서 장비의 이용률이 높은 수준을 유지하고 있습니다. 의약품 개발 및 독성학 분야는 규모는 작지만 연평균 성장률(CAGR) 8.78%를 나타낼 것으로 전망됩니다. 이는 종양학 및 순환기 계통의 임상시험에서 FDA의 안전성 체크리스트의 일환으로 혈소판 감소증 모니터링이 현재 필수로 규정되어 있기 때문입니다. 스폰서 기업들은 파마코 인포매틱스용으로 원시 동태 곡선을 출력할 수 있는 플랫폼을 원하고 있으며, 이 기능을 제공할 수 있는 것은 극히 일부의 프리미엄 기기뿐이기 때문에 더 높은 가격 책정이 가능해졌습니다.

전이 및 신경퇴행성 질환에서 혈소판의 역할을 조사하는 학술 컨소시엄은 첨단 응집 측정법에 사용될 유럽연구위원회(ERC) 및 미국 국립보건원(NIH)의 연구비를 지원받고 있습니다.

지역별 분석

북미는 2025년 매출의 39.40%를 차지하며, 병원이 AI 강화형 분석 장비에 적극적으로 예산을 편성했고, 보험사가 첨단 심장 치료에 대해 보험금을 지급한 것이 그 요인으로 꼽힙니다. 캐나다 온타리오주와 브리티시컬럼비아주의 의료 시스템에서는 HL7 인터페이스를 활용하여 아침 회진 전에 결과를 전달할 수 있도록, 지방에서 보내온 검체를 하룻밤 사이에 처리하는 참조 검사실 허브의 시범 운영이 진행되었습니다.

유럽에서는 IVDR(체외진단용 의료기기 규정)에 따라 엄격한 증거 요건이 부과되고 있어, 제조업체들은 인증 기관의 역량이 가장 뛰어난 독일, 프랑스, 영국에 시장 출시를 집중할 수밖에 없는 실정입니다. 독일 연방합동위원회는 2025년 병원 품질 지표를 개정하여, PCI(경피적 관상동맥성형술) 환자에 대한 혈소판 기능 검사 실시율을 포함시킴으로써 성과연동형 보상 제도를 통해 그 도입을 촉진했습니다. 영국 NHS 공급망은 2026년에 기본 계약을 재협상하여 소모품과 유지보수를 통합하고, 가동 중단 시간 감축에 대해 보상을 제공하는 성과 연계형 계약으로 전환했습니다.

아시아태평양은 연평균 성장률(CAGR) 8.02%를 나타낼 것으로 예측되며, 이를 주도할 요인은 중국의 전국 응고 장애 등록 제도입니다. 이 제도는 2025년 말까지 120만 명의 환자를 등록했고, 원인을 알 수 없는 출혈 사례에 대해 혈소판 기능 검사를 의무화하고 있습니다. 초고령 사회인 일본과 한국에서는 채혈량을 최소화하는 마이크로플루이딕스 디스크 시스템이 우선적으로 채택되고 있는 반면, 호주의 외상 센터에서는 대량 수혈 프로토콜에 점탄성 물질과 혈소판을 결합한 카트리지가 도입되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the platelet aggregation devices market size is projected to expand from USD 0.93 billion in 2025 and USD 0.98 billion in 2026 to USD 1.29 billion by 2031, registering a CAGR of 5.64% between 2026 to 2031.

This report is Segmented by Product (Systems, Reagents, and More), Technology (Light-Transmission Aggregometry, Impedance Aggregometry, and More), Sample Type (Platelet-Rich Plasma and More), Application (Clinical Diagnostics, Antiplatelet-Therapy Monitoring, and More), End User (Hospitals, Diagnostic Laboratories, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Platelet Aggregation Devices Market Trends and Insights

Rising Incidence of Cardiovascular & Bleeding Disorders

Cardiovascular disease prevalence continues to climb, prompting hospitals to increase routine platelet testing volumes. The American Heart Association projects hypertension rates rising to 61% and diabetes to 26.8% by 2050, trends that drive long-term utilization of platelet analyzers. Clinical teams also observe high rates of platelet dysfunction in hematologic therapies such as CAR-T, adding to the complex testing needs of oncology departments. These converging disease burdens intensify demand across the platelet aggregation devices market. National cardiology registries in the United States and the European Union reported an 8% rise in patients receiving dual antiplatelet therapy between 2024 and 2025. Parallel data from the World Federation of Hemophilia counted 418,000 individuals with diagnosed platelet-function disorders in 2024, a 12% increase from 2022. Interventional cardiologists rely on aggregometers to identify clopidogrel non-responders before percutaneous coronary interventions, while hematologists use the same platforms to phenotype inherited deficiencies, such as Glanzmann thrombasthenia.

Growing Geriatric Population Base

United Nations projections place the global population aged >= 65 years at 1.6 billion by 2050, up from 1.0 billion in 2024. Aging is associated with endothelial dysfunction and heightened platelet reactivity, complicating anticoagulant management during orthopedic or neurologic procedures. European and North American geriatric wards have begun installing benchtop aggregometers to individualize antiplatelet dosing for hip-fracture repair and stroke rehabilitation. Japanese hospitals, serving the world's oldest society, run platelet function panels during routine outpatient visits to pre-empt thrombotic events, reinforcing demand for platelet aggregation devices. Vendors that offer low-volume, fully automated platforms capture this demographic-driven spend because more minor sample requirements align with frail-elderly phlebotomy constraints.

High Capital & Consumable Cost of Advanced Systems

Fully automated platelet-aggregation workstations list between USD 120,000 and USD 180,000, with annual service contracts adding another USD 15,000-25,000. Consumables cost USD 12-18 per patient, compared with under USD 2 for routine coagulation tests reimbursed under bundled codes. Community hospitals operating on single-digit margins hesitate to invest unless vendors offer reagent-rental contracts that shift capital expense into per-test fees. Even in tertiary centers, cap-ex committees require multidisciplinary utilization cards from cardiology, hematology, and perioperative services to approve a purchase. This cost headwind trims the platelet aggregation devices market CAGR by nearly a percentage point in price-sensitive Asia and Latin America.

Other drivers and restraints analyzed in the detailed report include:

- Technological Shift to Automated/Integrated Analyzers

- Hospital Adoption of Point-of-Care Platelet Function Testing

- Shortage of Skilled Hemostasis Technologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Systems generated 49.90% of 2025 revenue, reflecting the legacy installed base of optical and impedance analyzers in hospital core laboratories. Consumables and accessories, however, are set to outpace the overall platelet aggregation devices market with an 8.90% CAGR through 2031, bolstered by single-use microfluidic discs that slash cleaning downtime and cross-contamination risk. Reagent contracts now bundle agonists with software-unlock codes, converting what was once a one-time hardware sale into an annuity stream. As laboratories migrate toward whole-blood impedance methods, demand shifts to new reagent formulations, fragmenting supplier shares and opening space for niche providers of specialty agonists. Accessories such as calibrators and pipette tips hold slim margins but remain indispensable because hospitals must follow manufacturer-validated workflows to safeguard accreditation.

Margins on consumables encourage vendors to preinstall drive locks in their analyzers, forcing hospitals to source supplies exclusively from the original manufacturer to maintain warranty compliance. That lock-in strategy deepens switching costs and reinforces revenue visibility throughout the forecast period. Regional distributors also bundle preventive-maintenance kits with reagent reorder thresholds, increasing annual spend per instrument. Consequently, the platelet aggregation devices market size attributed to consumables will continue to grow steadily, even in mature regions where capital refresh cycles have plateaued.

Clinical testing accounted for 63.50% of 2025 revenue, as cardiologists and hematologists rely on aggregometry for routine monitoring, preoperative risk assessments, and differential diagnosis of bleeding disorders. The regulatory push for personalized antiplatelet therapy fuels daily test volumes, keeping instrument utilization high in catheterization labs and stroke units. Drug development and toxicology, while smaller, is forecast to expand at an 8.78% CAGR because oncology and cardiovascular trials now require thrombocytopenia surveillance as part of FDA safety checklists. Sponsors demand platforms that output raw kinetic curves for pharmaco-informatics, a capability offered by only a handful of premium devices, thereby commanding higher price points.

Academic consortia investigating platelet involvement in metastasis and neurodegeneration receive European Research Council and NIH grants earmarked for advanced aggregometry.

Geography Analysis

North America accounted for 39.40% of 2025 revenue, driven by hospitals budgeting aggressively for AI-enhanced analyzers and insurers reimbursing high-acuity cardiac procedures. Canada's Ontario and British Columbia health systems piloted reference-lab hubs that process rural samples overnight, leveraging HL7 interfaces to return results before morning rounds.

Europe enforces stringent evidence requirements under IVDR, pushing manufacturers to concentrate market launches in Germany, France, and the United Kingdom, where notified-body capacity is highest. Germany's Federal Joint Committee updated hospital quality indicators in 2025 to include platelet-function testing rates for PCI patients, promoting adoption through pay-for-performance incentives. The United Kingdom's NHS Supply Chain renegotiated framework agreements in 2026, combining consumables and maintenance into outcome-based contracts that reward reductions in downtime.

Asia-Pacific is forecast to grow at an 8.02% CAGR, led by China's national coagulation-disorder registry, which enrolled 1.2 million patients by end-2025 and mandates platelet-function testing for unexplained bleeding cases. Japan and South Korea, both super-aged societies, prioritize microfluidic disc systems that minimize draw volumes, while Australian trauma centers integrate viscoelastic-plus-platelet cartridges into massive transfusion protocols.

- AggreDyne Inc.

- Alpha Laboratories Ltd.

- Bash Medical Ltd.

- Bio/Data

- Chrono-Log

- Drucker Diagnostics LLC

- Entegrion Inc.

- Roche

- Grifols

- Haemonetics

- Helena Biosciences Europe

- Helena Laboratories

- Helmer Scientific

- Instrumentation Laboratory (Stago)

- Siemens Healthineers

- Sienco Inc.

- Sysmex

- Tem Innovations GmbH

- Werfen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Cardiovascular and Bleeding Disorders

- 4.2.2 Growing Geriatric Population Base

- 4.2.3 Technological Shift to Automated/Integrated Analyzers

- 4.2.4 Hospital Adoption of Point-of-Care Platelet Function Testing

- 4.2.5 AI-Driven Decision Support in Antiplatelet Therapy

- 4.2.6 Micro-Fluidic Disc-Based LTA Reducing Sample Volume

- 4.3 Market Restraints

- 4.3.1 High Capital and Consumable Cost of Advanced Systems

- 4.3.2 Shortage of Skilled Hemostasis Technologists

- 4.3.3 Regulatory Delays for Optical-AI Hybrid Devices

- 4.3.4 Inter-Laboratory Result Variability Undermining Reimbursement

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Systems

- 5.1.2 Reagents

- 5.1.3 Consumables and Accessories

- 5.2 By Application

- 5.2.1 Clinical Applications

- 5.2.2 Antiplatelet-therapy Monitoring

- 5.2.3 Disease & Translational Research

- 5.2.4 Drug Development & Toxicology

- 5.2.5 Others

- 5.3 By Technology

- 5.3.1 Light Transmission Aggregometry

- 5.3.2 Impedance/Multiple-Electrode Aggregometry

- 5.3.3 Viscoelastic Platelet Mapping Assays

- 5.3.4 Micro-fluidic Disc-based Aggregometry

- 5.3.5 Flow-Cytometry-based Aggregometry

- 5.4 By Sample Type

- 5.4.1 Whole Blood

- 5.4.2 Platelet-Rich Plasma (PRP)

- 5.4.3 Washed Platelets

- 5.5 By End-User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Blood Banks

- 5.5.4 Research & Academic Institutes

- 5.5.5 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AggreDyne Inc.

- 6.3.2 Alpha Laboratories Ltd.

- 6.3.3 Bash Medical Ltd.

- 6.3.4 Bio/Data Corporation

- 6.3.5 Chrono-Log Corporation

- 6.3.6 Drucker Diagnostics LLC

- 6.3.7 Entegrion Inc.

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 Grifols S.A.

- 6.3.10 Haemonetics Corporation

- 6.3.11 Helena Biosciences Europe

- 6.3.12 Helena Laboratories Corporation

- 6.3.13 Helmer Scientific Inc.

- 6.3.14 Instrumentation Laboratory (Stago)

- 6.3.15 Siemens Healthineers AG

- 6.3.16 Sienco Inc.

- 6.3.17 Sysmex Corporation

- 6.3.18 Tem Innovations GmbH

- 6.3.19 Werfen

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment