|

시장보고서

상품코드

2061609

헬스케어 공급망 관리 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Healthcare Supply Chain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

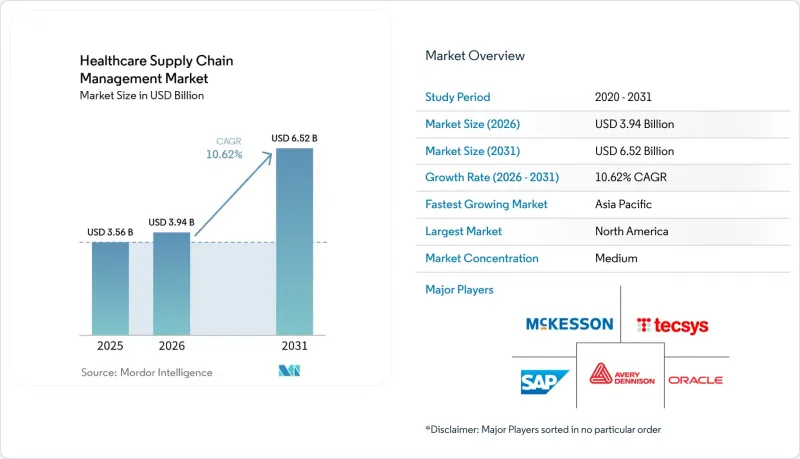

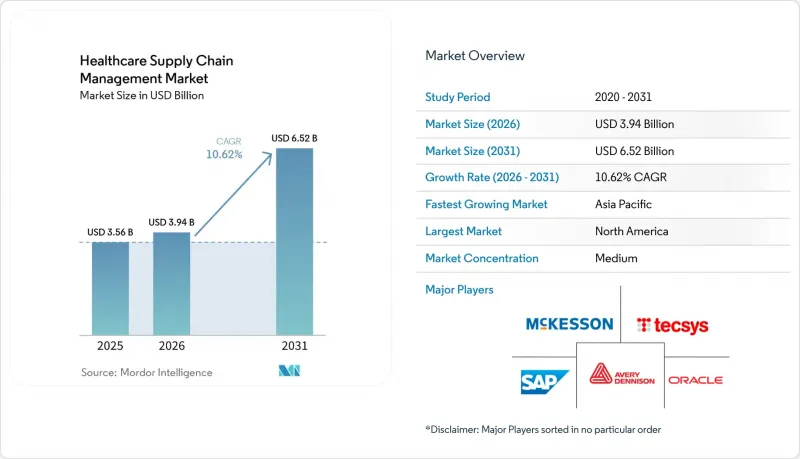

Mordor Intelligence에 의하면, 헬스케어 공급망 관리 시장 규모는 2025년에 35억 6,000만 달러로 평가되었고, 2026년 39억 4,000만 달러로 추정되고, 2031년까지 65억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 10.62%를 나타낼 전망입니다.

본 보고서는 구성 요소별(소프트웨어, 하드웨어 등), 도입 형태별(온프레미스 및 클라우드 기반), 최종 사용자별(의료 제공업체, 의료 보험자 등), 그리고 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망은 금액(달러)으로 제시되어 있습니다.

세계의 헬스케어 공급망 관리 시장 동향 및 인사이트

재고 낭비를 줄이기 위한 클라우드 우선 업그레이드

미국 병원의 약 70%가 2026년까지 핵심 공급 업무를 클라우드 플랫폼에서 운영할 계획이며, 이를 통해 실시간 가시성이 확보되어 과잉 재고를 줄이고 품절 사태를 방지할 수 있게 됩니다. 이러한 플랫폼에 내장된 머신러닝 엔진은 소비 패턴, 계절성, 시술 일정 및 공급업체의 리드 타임을 분석하여, 재고를 임상적으로는 안전하면서도 재무적으로는 효율적인 수준으로 유지합니다. 이전을 완료한 의료 시스템에서는 재고 관련 비용이 최대 30%까지 절감된 것은 물론, 제품 부족 현상이 줄어들어 의료진의 만족도도 향상된 것으로 보고되었습니다. 또한, 클라우드 아키텍처는 전자의무기록과의 통합을 효율화하고, 여러 거점 간의 연계를 간소화합니다. 이는 의료 제공업체 네트워크의 통합이 진행되는 가운데 매우 중요합니다.

UDI 및 추적 및 추적성에 관한 규제 의무화

FDA의 의료기기 고유 식별(UDI) 시스템 및 DSCSA(의약품 안전 추적법)의 일련번호 부여 요건에 따라, 모든 의료기기 및 의약품 단위에는 제조 공장에서 환자의 병상까지 이어지는 전체 유통망 전반에 걸쳐 추적 가능한 기계 판독 가능 코드를 부여해야 합니다. 컴플라이언스 대응 플랫폼은 이 데이터를 자동으로 수집, 저장 및 교환함으로써 리콜 조사에 소요되는 시간을 수주에서 수시간으로 단축하고, 환자의 안전을 강화합니다. 조기에 대응한 의료기관은 유효기간 자동 알림 및 종단간 추적성 감사를 통해 업무상의 이점을 얻을 수 있습니다.

초기 통합 및 교육에 드는 막대한 비용

중규모 시스템의 경우, 풀스택 플랫폼 도입에는 소프트웨어, 하드웨어, 인터페이스 및 6-12개월간의 직원 교육 비용을 포함해 200만-1,500만 달러의 비용이 소요됩니다. 전자차트나 재무 모듈과의 복잡한 연동으로 인해 초기 예산이 두 배로 늘어나는 경우가 많아, 투자 회수 기간이 18-24개월로 길어지며, 이는 소규모 의료기관에게는 큰 걸림돌이 되고 있습니다.

부문별 분석

2025년 현재, 소프트웨어 플랫폼은 헬스케어 공급망 관리 시장의 60.70%를 차지했으며, 이는 조달, 계약, 물류, 규정 준수를 조정하는 통합형 지휘 체계에 대한 시급한 수요를 반영하고 있습니다. 서비스 부문은 규모는 작지만, 도입 지원, 워크플로 재설계 및 변경 관리 지원에 대한 의료 제공업체의 의존도가 높아 11.45%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 하드웨어(RFID 리더기, 자동 조제 캐비닛, IoT 센서)는 예산이 클라우드 라이선스로 전환되고 있는 상황에서도 실시간 데이터 수집에 있어 여전히 필수적인 요소로 남아 있습니다.

이 소프트웨어의 장점은 차이점 파악, 수요 예측, 규정 준수 관련 과제의 가시화를 수행하는 내장형 분석 기능에서 비롯됩니다. Oracle Health의 차세대 EHR은 공급망 모듈을 통합하고 있어, 임상의는 환자 차트 화면을 떠나지 않고도 자동 재고 보충 주문을 할 수 있습니다. 이러한 통합을 통해 조달 결정이 임상 경로와 일치하게 되어 낭비를 줄이고, 사례별 비용 관리를 개선합니다.

지역별 분석

2025년, 북미는 헬스케어 공급망 관리 시장 점유율 45.10%를 유지했습니다. DSCSA의 시행 시한과 성숙한 GPO 생태계가 안정적인 수요를 뒷받침하는 한편, IDN 간의 지속적인 통합이 엔터프라이즈급 플랫폼 도입을 촉진하고 있습니다. 캐나다 주정부 자금을 지원하는 의료 시스템은 급증하는 치료 비용을 억제하기 위해 공급망 지휘 센터에 투자하고 있습니다.

아시아태평양은 2031년까지 12.42%라는 가장 높은 연평균 성장률(CAGR)을 기록할 전망입니다. 중국과 인도에서 병원 건설이 급속히 진행되고 있으며, 백신 자급자족 프로그램과 디지털 헬스 인프라 구축을 위한 정부의 주도적인 추진이 이러한 도입을 뒷받침하고 있습니다. 태국 공급업체 관리 재고(VMI) 시범 사업과 싱가포르의 IoT 기반 병원 단지는 이 지역의 혁신을 상징합니다. 첨단 치료제를 위한 콜드체인이 확대됨에 따라, 아시아태평양의 헬스케어 공급망 관리 시장 규모는 2030년까지 두 배로 증가할 것으로 전망됩니다.

유럽에서는 의료기기 규정(MDR), 기후 변화 대응에 부합하는 ESG 요건, 그리고 브렉시트를 계기로 한 완충 재고 전략에 힘입어 꾸준한 성장이 예상됩니다. 다국적 의료 시스템은 다국어 라벨 관리, 환경 지표 추적, 그리고 각국 고유의 전자 조달 포털과의 연동을 통합하는 플랫폼을 필요로 합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the healthcare supply chain management market size was valued at USD 3.56 billion in 2025 and estimated to grow from USD 3.94 billion in 2026 to reach USD 6.52 billion by 2031, at a CAGR of 10.62% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Hardware and More), by Deployment Mode (On-Premise and Cloud-Based), End-User (Healthcare Providers, Healthcare Payers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Supply Chain Management Market Trends and Insights

Cloud-First Upgrades to Cut Inventory Waste

Nearly 70% of U.S. hospitals plan to run core supply operations on cloud platforms by 2026, unlocking real-time visibility that trims excess stock and reduces stockouts. Machine-learning engines embedded in these platforms analyze consumption patterns, seasonality, procedure schedules, and supplier lead times to keep inventory within clinically safe but financially lean thresholds. Health systems that completed migration report inventory-related savings of up to 30% alongside improved clinician satisfaction due to fewer product shortages. Cloud architecture also streamlines integration with electronic health records and simplifies multi-site coordination, critical as provider networks consolidate.

Mandatory UDI & Track-and-Trace Regulations

The FDA's Unique Device Identification system and DSCSA serialization requirements force every device and drug unit to carry a machine-readable code that travels across the entire chain, from factory to bedside. Compliance platforms automatically capture, store, and exchange this data, cutting recall investigation times from weeks to hours and strengthening patient safety. Providers that align early gain operational benefits through automated expiration alerts and end-to-end provenance auditing.

High Up-Front Integration & Training Costs

Implementing a full-stack platform demands USD 2-15 million for a mid-sized system, covering software, hardware, interfaces, and six-to-twelve-month staff education. Complex links to electronic health records and financial modules often double initial budgets, stretching payback horizons to 18-24 months and deterring smaller providers.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Demand Sensing & Predictive Restocking

- Rapid Outsourcing to GPOs for Cost Containment

- Cyber-Security & Data-Privacy Liabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms accounted for 60.70% of the healthcare supply chain management market in 2025, reflecting urgent demand for unified command centers that coordinate sourcing, contracting, logistics, and compliance. Services, though smaller, post the fastest 11.45% CAGR thanks to provider reliance on implementation, workflow redesign, and change-management support . Hardware-RFID readers, automated dispensing cabinets, and IoT sensors-remains indispensable for real-time data capture, even as budgets tilt toward cloud licenses.

Software's edge stems from embedded analytics that spot variance, predict demand, and surface compliance gaps. Oracle Health's next-generation EHR integrates supply chain modules, enabling clinicians to place auto-replenish orders without leaving patient charts. Such convergence aligns procurement decisions with clinical pathways, shrinking waste and improving case costing

Geography Analysis

North America retained 45.10% of healthcare supply chain management market share in 2025. DSCSA deadlines and a mature GPO ecosystem underpin stable demand, while ongoing consolidation among IDNs fuels enterprise-scale platform rollouts. Canada's provincially funded health systems invest in supply-chain command centers to curb rising procedure costs.

Asia-Pacific records the steepest 12.42% CAGR to 2031. Rapid hospital construction in China and India, vaccine self-sufficiency programs, and governmental push for digital health infrastructure drive adoption. Thailand's vendor-managed inventory pilots and Singapore's IoT-enabled hospital campuses showcase regional innovation. The healthcare supply chain management market size for Asia-Pacific is projected to double by 2030 as cold-chain for advanced therapeutics scales.

Europe shows steady growth underpinned by Medical Device Regulation (MDR), climate-aligned ESG mandates, and Brexit-triggered buffer-stock strategies. Multinational health systems seek platforms that consolidate multilingual labeling, track environmental metrics, and interface with country-specific e-procurement portals.

- GHX

- Tecsys Inc.

- Infor

- Oracle

- SAP

- Mckesson

- Syft

- Cardinal Health

- Owens & Minor

- LogiTag Systems

- Jump Technologies

- Epicor

- JDA (Blue Yonder)

- Manhattan Associates

- IBM

- Medline Industries

- FlexLogistics

- ClarusONE

- Zebra Technologies

- OptiFreight(UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first upgrades to cut inventory waste

- 4.2.2 Mandatory UDI & track-and-trace regulations

- 4.2.3 AI-driven demand sensing & predictive restocking

- 4.2.4 Rapid outsourcing to GPOs for cost containment

- 4.2.5 Vendor-managed inventory for critical drugs

- 4.2.6 Climate-resilient cold-chain design mandates

- 4.3 Market Restraints

- 4.3.1 High up-front integration & training costs

- 4.3.2 Cyber-security & data-privacy liabilities

- 4.3.3 Shortage of supply-chain IT talent in hospitals

- 4.3.4 Opaque supplier ESG data blocking compliance

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.3 By End User

- 5.3.1 Healthcare Providers

- 5.3.2 Healthcare Payers

- 5.3.3 Pharma & Biotech Companies

- 5.3.4 Contract Manufacturing Organizations

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 GHX

- 6.3.2 Tecsys Inc.

- 6.3.3 Infor

- 6.3.4 Oracle (Cerner)

- 6.3.5 SAP SE

- 6.3.6 McKesson Corporation

- 6.3.7 Syft

- 6.3.8 Cardinal Health

- 6.3.9 Owens & Minor

- 6.3.10 LogiTag Systems

- 6.3.11 Jump Technologies

- 6.3.12 Epicor

- 6.3.13 JDA (Blue Yonder)

- 6.3.14 Manhattan Associates

- 6.3.15 IBM

- 6.3.16 Medline Industries

- 6.3.17 FlexLogistics

- 6.3.18 ClarusONE

- 6.3.19 Zebra Technologies

- 6.3.20 OptiFreight(UPS)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment