|

시장보고서

상품코드

2061615

미국의 수직 농업 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Vertical Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

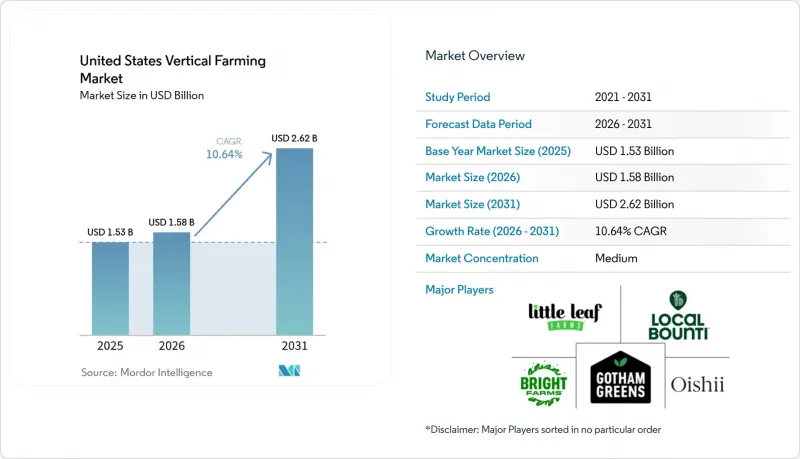

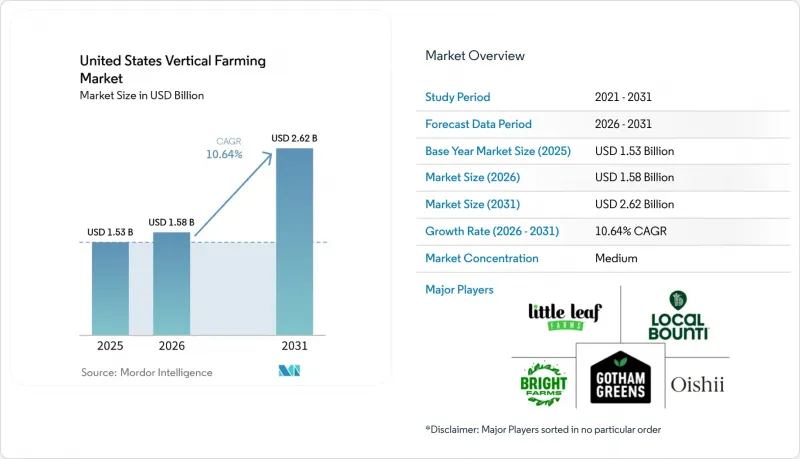

Mordor Intelligence에 의하면, 미국의 수직 농업 시장 규모는 2025년에 15억 달러로 평가되었습니다. 2026년 16억 달러에서 2031년까지 26억 달러에 이를 것으로 예측됩니다. 2026년부터 2031년 CAGR은 10.6%를 나타낼 전망입니다.

본 보고서는 성장 메커니즘(수경 재배, 에어로포닉스, 아쿠아포닉스), 구조(빌딩형, 창고형, 컨테이너형), 작물 유형(잎채소, 허브, 마이크로그린 등), 구성 요소(하드웨어, 소프트웨어, 서비스), 최종 사용자(소매·슈퍼마켓, 외식 산업 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 수직 농업 시장 동향과 인사이트

지역산 무농약 잎채소에 대한 수요

대형 식품 체인점들이 농약 미사용 농산물을 조달 기준으로 삼는 경향이 강해지고 있어, 소매 수요가 미국의 수직 농업 시장을 지탱하고 있습니다. 실내 농장은 항상 무농약 및 제초제 미사용 요건을 충족하고 있으며, 계절을 불문하고 노지 재배 농가나 많은 온실 재배 농가를 능가하는 실적을 올리고 있습니다. 이러한 소매업체들의 기대에 부응하는 움직임은 연방 정부의 이니셔티브에 힘입어 더욱 가속화되고 있습니다. 예를 들어, 미국 농무부(USDA)는 2025년 1월, 도시 농업 및 혁신적인 생산과 관련된 새로운 보조금으로 1,440만 달러를 지원한다고 발표했으며, 2020년 이후 총 지원액은 5,370만 달러에 달했습니다. 이러한 동향은 포장 샐러드 및 절단 채소 부문에서 계약의 투명성, 소매업체와의 관계, 가격 규율을 강화하고 있습니다. 경기 침체기에 실내 재배 잎채소가 ‘선택 구매 품목’으로 취급될 위험을 줄임으로써, 시장의 관심은 소매 카테고리 관리와 공급 보장으로 옮겨가고 있습니다. 이러한 상호 연관된 수요 패턴은 미국의 수직 농업 시장이 소비자의 참신함에 대한 선호보다 안정적인 소매 파트너십에 대한 의존도를 높이고 있음을 여실히 보여주고 있습니다.

푸드 마일리지 감소와 당일 배송을 통한 신선도

수송 거리 단축은 장거리 국내 운송 과정에서 잎채소가 겪는 심각한 신선도 저하 문제를 해결함으로써, 미국의 수직 농업 시장의 효율화를 촉진하고 있습니다. 캘리포니아주나 애리조나주에서 생산된 기존 농산물은 동부 지역의 소매 유통망에 도착하기까지 4-6일이 소요되는 경우가 많아, 매장에서 판매되는 기간이나 소비자의 구매 기회가 제한적이었습니다. 반면, 주요 도시에서 200마일 이내 거리에 위치한 실내 농장에서는 수확 후 24시간 이내에 농산물을 배송할 수 있어, 소매점 진열 기간을 5-7일 연장할 수 있습니다. 2025년 9월 왕 씨 등이 발표한 연구에 따르면, 인근 지역에서 조달함으로써 수확 후 호흡으로 인한 손실이 18%에서 22%까지 감소했고, 이로 인해 소매업체의 이익률이 직접적으로 향상되었으며 가격 인하 폭이 축소되었다고 강조하고 있습니다. 이러한 변화는 도시 지역의 유통 경로에서 ‘당일 배송을 통한 신선도’가 단순한 마케팅 메시지에서 계약상의 기준으로 진화하고 있는 이유를 뒷받침하며, 지역 밀착형 실내 농업의 정당성을 확고히 하고 있습니다.

전력 소비량과 전력 가격의 변동이 이익률을 압박하고 있습니다.

조명, 기후 제어, 제습과 같은 에너지 집약적 시스템에 대한 의존으로 인해, 전력은 미국의 수직 농업 시장의 주요 비용 요인이 되고 있습니다. 2024년, 카이저 씨 등이 발표한 보고서에 따르면, 전력 비용이 생산 비용의 20%에서 40%를 차지하며, 조명만으로도 전체 전력 소비량의 60%에서 85%를 소비하는 것으로 나타났습니다. AGEYE의 2025년 조사 결과에 따르면, 건설 전 재무 모델에서는 냉난방(HVAC) 및 제습 비용이 30%에서 50%까지 과소평가되는 경우가 많으며, 그 결과 비용 추정이 낙관적으로 나오기 쉽습니다. 2026년 『Nature Communications』에 게재된 연구에 따르면, 대부분의 수직 농장은 기존 수입품에 비해 탄소 경쟁력을 갖추기 위한 에너지 집약도 기준을 초과하는 것으로 밝혀졌습니다. 동적 조명 제어를 통해 전력 비용을 12% 절감할 수 있지만, 노후된 시설의 개보수에는 막대한 비용이 드는 경우가 많아 현실적이지 않습니다. 따라서, 특히 중서부 및 북동부 지역에서 시장은 전기 요금 변동의 영향을 받기 쉬워졌으며, 비용을 안정화하고 경쟁력을 높이기 위해서는 재생에너지 도입, 에너지 저장 시스템 및 고효율 기술의 도입이 시급하다는 점이 부각되고 있습니다.

부문별 분석

2025년, 수경 재배는 미국의 수직 농장 시장에서 56.8%의 점유율을 차지하며 시장을 독점했습니다. 이는 잎채소와의 뛰어난 궁합, 확립된 영양액 시스템, 그리고 기존 실내 농장 레이아웃에의 쉬운 통합이 원동력이 되고 있습니다. 예측 가능한 생산량과 표준화된 재배 주기를 실현하는 이러한 능력은 상추나 시금치와 같은 주요 상업용 작물에 대한 소매업체 수요와 부합합니다. 그러나 수경 재배의 보급으로 인해 제품의 차별화가 약화되면서, 성공을 위해서는 사업 규모, 실행력, 고객 접근성이 더욱 중요해지고 있습니다.

에어로포닉스는 2026년부터 2031년까지 연평균 성장률(CAGR) 16%를 나타낼 것으로 예측되며, 수경 재배보다 물 사용량이 70%에서 95% 적다는 효율성과, 고부가가치이며 물에 민감한 작물에 유익한 뿌리 영역의 산소 공급이 향상되고 있다는 점에서 가장 빠르게 성장하는 재배 방식으로 부상하고 있습니다. 2026년 2월에 특허를 취득한 Local Bounti사의 AI 지원 하이브리드 시스템과 같은 혁신은 사업자들이 생산량을 최적화하는 과정에서 재배 방식의 유연성이 높아지고 있음을 보여줍니다. 아쿠아포닉스는 식물과 물고기의 생물학적 특성을 모두 관리해야 하는 운영상의 복잡성 때문에 여전히 틈새 분야로 남아 있지만, 추적 가능성과 폐쇄형 생산이 부가가치를 창출하는 기관용 시장이나 제약 업계와 같은 전문 시장에서 활용되고 있습니다. 이러한 모든 재배 방식은 다양한 수요에 부응하기 위해 효율성, 혁신, 그리고 특정 용도로 진화하는 시장을 반영하고 있습니다.

2025년 시장 가치의 68.6%를 차지한 건물형 농장은 미국의 수직 농업 시장에서 가장 큰 비중을 차지하는 구조 유형입니다. 기존 창고나 산업용 공간을 대규모 생산 시설로 전환할 수 있을 뿐만 아니라, 고밀도 다층 레이아웃과 엄격한 환경 제어를 통해 높은 수확량을 확보하고 있습니다. 이러한 장점은 전국 및 지역 차원의 소매 계약을 이행하는 데 필수적이며, 건물형 농장의 확장성 덕분에 사업자는 고정 비용을 더 많은 생산량에 분산시켜 시장에서 확고한 입지를 다지고 있습니다.

한편, 2026년부터 2031년까지 연평균 성장률(CAGR) 12.2%가 예상되는 운송용 컨테이너 농장은 가장 빠르게 성장하는 구조 유형으로 부상하고 있습니다. 이러한 모듈식 구조와 신속한 구축 능력 덕분에, 영구적인 건설이 현실적으로 어려운 식품 사막 지역, 군사 시설 및 기관 캠퍼스에서 이상적인 선택지가 되고 있습니다. 예를 들어, 오폴로 팜이 2025년 피닉스에서 선보인 자동화 큐브는 컨테이너 시스템이 어떻게 컴팩트하고 자동화된 솔루션을 통해 인력과 공간의 제약을 해결할 수 있는지 입증했습니다. 이 두 형태 중간에 위치한 창고형 농장은 컨테이너보다 더 많은 재배 용량을 제공하지만, 전용으로 설계된 다층 건물에 비해 건설 밀도가 낮습니다. 이러한 구조 유형은 대규모 지역 허브와 소규모 모듈식 유닛 간의 균형을 이루는 시장을 반영하며, 미국의 수직 농업 시장을 다양하고 적응력이 뛰어난 솔루션으로 발전시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the united states vertical farming market size was valued at USD 1.5 billion in 2025 and is estimated to grow from USD 1.6 billion in 2026 to reach USD 2.6 billion by 2031, at a CAGR of 10.6% during the forecast period 2026-2031.

This report is Segmented by Growth Mechanism (Hydroponics, Aeroponics, and Aquaponics), by Structure (Building-Based, Warehouse, and Container), by Crop Type (Leafy Greens, Herbs, Microgreens, and More), by Component (Hardware, Software, and Services), and by End User (Retail and Supermarkets, Foodservice, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Vertical Farming Market Trends and Insights

Demand for Local Pesticide-Free Greens

Retail demand is anchoring the United States vertical farming market, as major grocery chains increasingly treat pesticide-free produce as a procurement standard. Indoor farms consistently meet zero-pesticide and no-herbicide requirements, outperforming field growers and many greenhouse suppliers across seasons. This alignment with retail expectations is further supported by federal initiatives, such as the USDA's January 2025 announcement of USD 14.4 million in new Urban Agriculture and Innovative Production grants, bringing total commitments since 2020 to USD 53.7 million. These developments strengthen contract visibility, retailer relationships, and pricing discipline in packaged salads and fresh-cut categories. By reducing the risk that indoor greens are treated as discretionary products during economic downturns, the market is shifting its focus to retail category management and supply assurance. This interconnected demand pattern underscores the United States vertical farming market's growing reliance on stable retail partnerships rather than consumer novelty preferences.

Food-Mile Reduction and Same-Day Freshness

Shorter delivery distances are driving efficiency in the United States vertical farming market by addressing the significant shelf-life losses leafy greens face during long cross-country transit. Conventional produce from California and Arizona often takes 4 to 6 days to reach eastern retail networks, leaving limited time for store handling and consumer purchase. In contrast, indoor farms within 200 miles of major cities can deliver produce within 24 hours of harvest, extending retail shelf life by 5 to 7 days. A September 2025 study by Wang and coauthors highlighted that proximity sourcing reduced postharvest respiration losses by 18% to 22%, directly improving retailer margins and reducing markdowns. This shift underscores why same-day freshness is evolving from a marketing message to a contractual standard in urban distribution corridors, solidifying the case for regional indoor farming.

Power Intensity and Electricity-Price Volatility Pressure Margins

Electricity is a major cost driver for the United States vertical farming market due to the reliance on energy-intensive systems like lighting, climate control, and dehumidification. In 2024, Kaiser and coauthors reported that electricity constitutes 20% to 40% of production costs, with lighting alone consuming 60% to 85% of total electricity. AGEYE's 2025 findings showed that pre-build financial models often underestimate HVAC and dehumidification costs by 30% to 50%, leading to weaker cost assumptions. A 2026 study in Nature Communications found that most vertical farms exceed the energy-intensity threshold for carbon-competitive positioning against traditional imports. While dynamic lighting can cut electricity costs by 12%, retrofitting older facilities is often unaffordable. This leaves the market vulnerable to tariff volatility, particularly in the Midwest and Northeast, highlighting the urgent need for renewable energy adoption, storage systems, and efficient technologies to stabilize costs and enhance competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Water-Efficient Production under Western Drought Pressure

- AI Vision, Pollination, and Crop Recipes Enable Premium Fruit Crops

- Post-Bankruptcy Financing Gap Raises Cost of Capital

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydroponics dominated the United States vertical farming market with a 56.8% share in 2025, driven by its compatibility with leafy greens, established nutrient systems, and ease of integration into existing indoor farm layouts. Its ability to deliver predictable outputs and standardized crop cycles aligns with retailer demand for crops like lettuce and spinach, which remain the top commercial products. However, the widespread adoption of hydroponics has reduced product differentiation, making operational scale, execution, and customer access more critical for success.

Aeroponics, with a projected 16% CAGR during 2026-2031, is emerging as the fastest-growing mechanism due to its efficient water usage, 70% to 95% less than hydroponics, and enhanced root-zone oxygenation, which benefits high-value, water-sensitive crops. Innovations like Local Bounti's AI-assisted hybrid system, patented in February 2026, highlight the increasing flexibility of growth methods as operators optimize throughput. While aquaponics remains a niche due to its operational complexity in managing both plant and fish biology, it serves specialized markets like institutional and pharmaceutical channels, where traceability and closed-loop production add value. Together, these mechanisms reflect a market evolving towards efficiency, innovation, and targeted applications to meet diverse demands.

Building-based farms accounted for 68.6% of the 2025 market value, making them the largest structure type in the United States vertical farming market. Their ability to repurpose existing warehouse and industrial spaces for high-volume production, in addition to the dense multi-tier layouts and tighter climate control, ensures higher harvest volumes. These advantages are critical for meeting national and regional retail contracts, and the scalability of building-based formats allows operators to spread fixed costs over greater output, solidifying their central role in the market.

Meanwhile, shipping-container farms, with a projected CAGR of 12.2% during 2026-2031, are emerging as the fastest-growing structure type. Their modular and rapid-deployment capabilities make them ideal for food deserts, military locations, and institutional campuses where permanent construction is less practical. For instance, Opollo Farm's 2025 automated cube deployment in Phoenix demonstrated how container systems can address labor and space constraints through compact, automated solutions. Warehouse-based farms, positioned between these two formats, offer more cultivation volume than containers but lower build intensity compared to purpose-designed multi-level buildings. Together, these structure types reflect a market balancing large regional hubs with smaller, modular units, driving the evolution of the United States vertical farming market toward diverse and adaptable solutions.

List of Companies Covered in this Report:

- Little Leaf Farms, LLC

- Gotham Greens Holdings, LLC

- BrightFarms Inc. (Cox Enterprises, Inc.)

- Oishii Farm Corporation

- Local Bounti Corporation

- Plenty Unlimited Inc.

- AeroFarms, Inc.

- 80 Acres Farms, Inc.

- Square Roots, Inc.

- Farm.One, Inc.

- American Hydroponics, Inc.

- Argus Control Systems Limited

- Priva Holding B.V.

- Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)

- Fluence Bioengineering, Inc. (ams-OSRAM AG)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Demand for local pesticide-free greens

- 4.2.2 Food-mile reduction and same-day freshness

- 4.2.3 Water-efficient production under western drought pressure

- 4.2.4 Retailer demand for year-round supply resilience

- 4.2.5 Renewable power and microgrid contracting improves economics

- 4.2.6 AI vision, pollination, and crop recipes enable premium fruit crops

- 4.3 Market Restraints

- 4.3.1 Crop profitability remains concentrated in leafy greens and herbs

- 4.3.2 Power intensity and electricity-price volatility pressure margins

- 4.3.3 Post-bankruptcy financing gap raises cost of capital

- 4.3.4 State and local zoning, permitting, and interconnection complexity

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Growth Mechanism

- 5.1.1 Hydroponics

- 5.1.2 Aeroponics

- 5.1.3 Aquaponics

- 5.2 By Structure

- 5.2.1 Building-based Vertical Farms

- 5.2.2 Warehouse-based Vertical Farms

- 5.2.3 Shipping-Container Vertical Farms

- 5.3 By Crop Type

- 5.3.1 Leafy Greens

- 5.3.2 Herbs

- 5.3.3 Microgreens

- 5.3.4 Fruits and Berries

- 5.3.5 Flowers and Ornamentals

- 5.4 By Component

- 5.4.1 Hardware

- 5.4.1.1 Lighting Systems

- 5.4.1.2 HVAC and Climate Control

- 5.4.1.3 Sensors and Monitoring

- 5.4.1.4 Irrigation and Nutrient Delivery

- 5.4.1.5 Racks, Trays, and Conveyance

- 5.4.1.6 Power and Backup Systems

- 5.4.2 Software

- 5.4.2.1 Farm Operating Systems

- 5.4.2.2 AI and Computer Vision

- 5.4.2.3 Workflow, ERP, and Traceability

- 5.4.3 Services

- 5.4.3.1 Design and Integration

- 5.4.3.2 Maintenance and Agronomy Support

- 5.4.3.3 Managed Operations

- 5.4.1 Hardware

- 5.5 By End User

- 5.5.1 Retail and Supermarkets

- 5.5.2 Foodservice

- 5.5.3 Direct-to-Consumer and E-commerce

- 5.5.4 Institutional and Government

- 5.5.5 Pharmaceutical and Cosmetic Ingredient Buyers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Little Leaf Farms, LLC

- 6.4.2 Gotham Greens Holdings, LLC

- 6.4.3 BrightFarms Inc. (Cox Enterprises, Inc.)

- 6.4.4 Oishii Farm Corporation

- 6.4.5 Local Bounti Corporation

- 6.4.6 Plenty Unlimited Inc.

- 6.4.7 AeroFarms, Inc.

- 6.4.8 80 Acres Farms, Inc.

- 6.4.9 Square Roots, Inc.

- 6.4.10 Farm.One, Inc.

- 6.4.11 American Hydroponics, Inc.

- 6.4.12 Argus Control Systems Limited

- 6.4.13 Priva Holding B.V.

- 6.4.14 Netafim Ltd. (Orbia Advance Corporation, S.A.B. de C.V.)

- 6.4.15 Fluence Bioengineering, Inc. (ams-OSRAM AG)