|

시장보고서

상품코드

2072472

수직 농업 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vertical Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

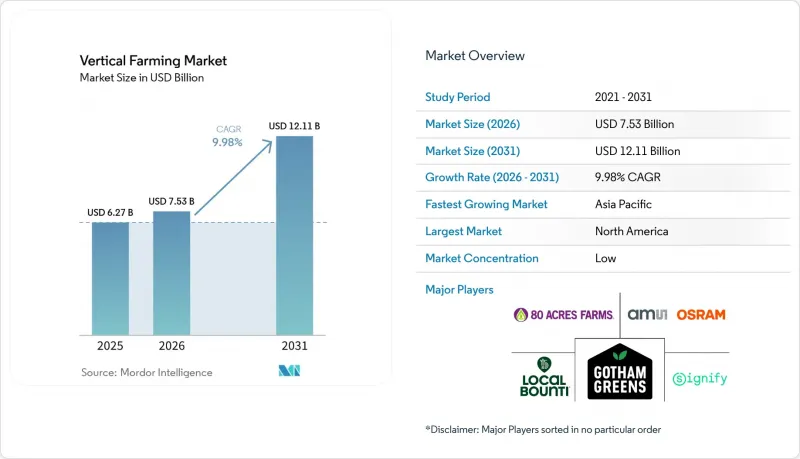

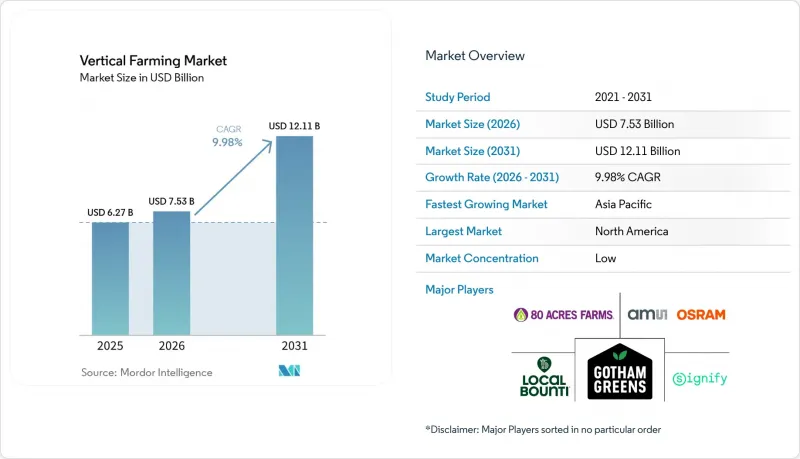

Mordor Intelligence에 의하면, 수직 농업 시장 규모는 2025년에 62억 7,000만 달러로 평가되었습니다. 2026년 75억 3,000만 달러에서 2031년까지 121억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 9.98%를 나타낼 전망입니다.

본 보고서는 재배 방식(수경 재배, 에어로포닉스, 아쿠아포닉스), 농장 구조(건물형 수직 농장 등), 구성 요소(조명, 기후 제어 등), 작물 유형(토마토, 베리류, 상추 및 잎채소, 피망 등), 지역(북미, 남미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 수직 농업 시장 동향 및 인사이트

도시 지역에서의 지역산·무농약 농산물에 대한 수요

지역에서 재배된 무농약 농산물에 대한 도시 지역 수요는 특히 인구 밀도가 높은 대도시권의 대형 식품 소매업체 및 외식 산업용도매업체를 중심으로 수직 농업 시장의 중요한 상업적 원동력이 되고 있습니다. 북미의 주요 환경 제어형 농업 기업인 고담 그린스(Gotham Greens)는 2026년 2월, 실내 재배 포장 샐러드, 양상추, 허브의 미국 시장 점유율 합계가 10%에 육박했으며, 2026년 1월까지의 13주간 소매 측정 기간 동안 전년 대비 22% 증가를 기록했다고 보고했습니다. 이는 실내 재배 농산물이 틈새 프리미엄 상품 카테고리에서 더 광범위한 시장에서의 입지를 확보해 나가고 있음을 보여줍니다. 이러한 동향이 중요한 이유는 수직 농업 시장이 ‘무농약’이라는 표기뿐만 아니라 예측 가능한 연중 공급 측면에서도 경쟁력을 발휘하고 있어, 이를 통해 소매업체는 안전 재고를 줄이고 재고 보충을 보다 효율적으로 관리할 수 있게 되기 때문입니다. 또한, 대도시권의 소비 거점 근처에서 농산물을 재배할 경우, 높은 신선도가 유통 면에서 경쟁 우위를 가져다줍니다. 운송 시간이 단축됨에 따라 유통기한이 연장되고, 가격 인하 압력도 완화되기 때문입니다. 그 결과, 수직 농업 시장은 신뢰성, 산지, 폐기물 감축이 개별적인 구매 요인이 아니라 종합적으로 우선시되는 소매업체를 중심으로 성장세를 보이고 있습니다.

LED, 로봇 공학, 센서 기술의 비용 절감

설비 비용의 감소는 신규 도입 및 업그레이드 시 자본 효율성을 높여주기 때문에 수직 농업 시장의 성장을 뒷받침하는 가장 뚜렷한 요인 중 하나로 계속해서 자리 잡고 있습니다. 시그니파이(Signify)는 2025년 6월 ‘Philips GrowWise’ 스마트 스펙트럼 시스템을 출시하며, 이 플랫폼이 실시간 일조 조건을 바탕으로 스펙트럼을 자동으로 조정함으로써 최대 6%의 에너지 절감 또는 작물 생육 개선을 실현할 수 있다고 발표했습니다. 2026년 3월 『Frontiers in Plant Science』지에 게재된 연구에 따르면, 상추의 경우 지속적인 저휘도 LED 조명을 통해 시험 조건 하에서 수확량 감소 없이 에너지 이용 효율이 21% 향상되었으며, LED 운영 비용이 16.5% 절감된 것으로 밝혀졌습니다. 또한, 영국 애그리테크 센터는 2026년 3월, 해당 센터의 ‘Advanced Crop Dynamic Control’ 시험에서 시스템이 아직 통합 초기 단계임에도 불구하고, 식물 중심의 조명 제어를 통해 에너지 효율을 21%에서 25%까지 향상시켰습니다고 보고했습니다. 그 결과, 수직 농업 시장에서는 조달 경제성 측면에서 실질적인 재설정이 이루어지고 있습니다. 이는 구매를 미루어 왔던 사업자들이, 과거 벤처 캐피털 주도의 건설 주기 중에 도입되었던 것보다 더 효율적인 하드웨어 및 자동화 시스템을 이제 평가할 수 있게 되었기 때문입니다.

높은 전력 부하와 자본 집약성

완전 밀폐형 생산 시스템은 에너지 집약적인 조명 및 기후 제어 인프라에 의존하고 있기 때문에 운영 경제성은 여전히 수직 농업 시장에서 가장 큰 제약 요인 중 하나입니다. 실내 농장에서는 일반적으로 인공 LED 조명이 전력 부하의 가장 큰 부분을 차지하며, 안정적인 재배 조건을 유지하기 위한 냉각, 환기, 제습 시스템 역시 운영 비용을 크게 증가시키고 있습니다. 이러한 비용 압박은 산업용 전기 요금이 높은 지역에서 특히 심각한 문제로 대두되고 있으며, 이는 수익성이 낮은 작물의 상업적 실현 가능성을 제한하는 한편, 업계가 고부가가치 잎채소나 특산품에 집중하는 경향을 강화하고 있습니다. 지역 기업인 바운티 코퍼레이션이 미국 증권거래위원회(SEC)에 제출한 서류는 이 분야에서 자본 구조가 얼마나 중요한지를 여실히 보여주고 있습니다. 이 회사는 수율과 생산 능력을 지속적으로 최적화하는 한편, 2025년부터 2026년에 걸쳐 부채 재편을 단행하고 성장 자금을 조달할 예정입니다. 따라서 수직 농업 시장은 여전히 근본적인 제약에 직면해 있습니다. 즉, 기술적인 실현 가능성이 반드시 재정적으로 지속 가능한 전개로 이어지는 것은 아니라는 뜻입니다.

부문별 분석

수경 재배는 수직 농업 시장에서 가장 큰 비중을 차지하는 재배 방식으로, 2025년에는 56.7%의 시장 점유율을 기록했습니다. 이러한 우위는 여러 가지 실내 농장 형태에 걸쳐 영양분 공급, 재배 주기 제어 및 뿌리권 관리 분야에서 쌓아온 오랜 상업적 실적을 바탕으로 합니다. 또한, 2018년부터 2023년에 걸쳐 많은 사업자들이 이 시스템 아키텍처를 기반으로 투자를 진행했기 때문에 수경 재배 도입 실적도 여전히 가장 탄탄합니다. 이러한 도입 실적은 현재도 수직 농업 업계의 조달, 생산자 교육 및 자재 조달에 계속해서 영향을 미치고 있습니다. 그 결과, 새로운 시스템이 개선되더라도 시장 점유율의 재분배는 완만한 속도로 진행되고 있습니다.

에어로포닉스는 가장 빠르게 성장하고 있는 기술로, 수직 농업 시장에서 2026년부터 2031년까지 연평균 성장률(CAGR) 13.1%로 확대될 것으로 전망됩니다. 이 모델은 표준 재순환식 수경 재배 시스템이 제공하는 수준을 뛰어넘어, 더 우수한 뿌리 환경 위생 상태와 추가적인 물 절약을 추구하는 사업자들에게 매력적인 선택지입니다. 아쿠아포닉스도 주목을 받고 있으며, 순환형 식량 시스템과 이중 수익원을 통해 운영상의 복잡성이 증가하더라도 그 도입은 정당화됩니다. JR 동일본 스타트업과 플랫폼은 2025년 8월, 아쿠아포닉스를 기반으로 한 순환형 식량 생산의 상용화를 위한 자본·업무 제휴를 발표했습니다. 이는 해당 회사의 아쿠아포닉스 시설이 일본 전국 5곳으로 확대된 데 따른 조치입니다. 이러한 움직임은 수경재배에서 수직 농업 시장이 단번에 벗어나는 것이 아니라, 통합형 식량 시스템으로 점차 확대되고 있다는 관점을 뒷받침하는 것입니다.

건물형 농장은 가장 큰 부문으로, 2025년 수직 농업 시장 규모의 72.4%를 차지했습니다. 이러한 우위는 더 큰 생산 능력, 더욱 통합된 기후 제어 시스템, 그리고 상업적 규모에서의 고정비 흡수 능력 면에서의 우위를 반영하고 있습니다. 또한, 이러한 프로젝트는 수많은 소규모 모듈형 도입 사례에 비해 운영 모델이 명확하기 때문에 기관 투자자의 자본을 유치하기 쉬운 경향이 있습니다. 실제로, 최대 규모의 건물형 시설은 대도시권공급망 내에서 수직 농업 시장의 확대를 위한 벤치마크로서 계속해서 역할을 수행하고 있습니다. 이러한 지위 덕분에, 이 구조는 대량 생산을 목표로 하는 상업 계획의 중심에 계속해서 자리 잡고 있습니다.

운송 컨테이너형 농장은 가장 빠르게 성장하고 있는 구조로, 2026년부터 2031년까지 연평균 성장률(CAGR) 12.3%를 나타낼 것으로 전망됩니다. 그 매력은 신속한 전개, 지리적 유연성, 그리고 공급 부족 지역에 진출하는 사업자에게 부담이 적다는 점에 있습니다. 2025년 7월, 500곳 이상의 가동 중인 컨테이너 농장을 포함한 Freight Farms의 자산이 Growcer에 양도된 것은 모기업이 파산한 후에도 컨테이너형 시스템에 대한 수요가 지속되고 있음을 보여줍니다. 또한, 두바이의 ‘기가팜(GigaFarm)’ 프로젝트는 규모 면에서 정반대의 사례로 주목받고 있습니다. 계획된 200기의 성장 타워 중, 첫 20기에 사용될 구성 부품이 2025년에 출하되었으며, 프로젝트 전체의 연간 생산량은 3,000메트르톤을 목표로 하고 있습니다. 이러한 경향을 종합해 보면, 수직 농업 시장에서 컨테이너형이나 건물형은 단순한 대체 수단이라기보다는 시장 진입 및 사업 확장의 각 단계에서 상호 보완적인 도구로 활용되고 있음을 알 수 있습니다.

지역별 분석

북미는 수직 농업 시장에서 가장 큰 비중을 차지하는 지역으로, 2025년에는 시장 점유율의 41.8%를 차지했습니다. 이 지역은 밀집된 대도시권의 소매 네트워크, 확립된 콜드체인 시스템, 그리고 실내 농업의 규모를 뒷받침하는 기술 자본의 집중이라는 이점을 누리고 있습니다. 현지 기업인 Bounti Corporation은 2025 회계연도 매출이 4,837만 달러에 달했으며, 약 1만 3,000개 매장에 상품을 공급하고 있어, 일부 미국 사업자들이 이미 달성한 상업적 확장의 규모를 보여주고 있습니다. 캐나다는 제2의 거점으로서의 위상을 지속적으로 강화하고 있으며, GoodLeaf Farms사는 2025년 11월에 3,790만 달러(5,200만 캐나다 달러)를 조달하여, 앨버타주 및 퀘벡주 거점의 생산 능력을 두 배로 늘리는 한편, 온타리오주에 새로운 연구개발 센터를 건설했습니다.

아시아태평양은 수직 농업 시장에서 가장 빠르게 성장하고 있는 지역 부문으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 12.8%를 나타낼 것으로 전망됩니다. 일본, 중국, 싱가포르, 한국에서 발생하는 토지 부족, 식품 안전에 대한 기대, 그리고 시설 농업에 대한 정부의 지원 강화가 이러한 성장을 뒷받침하고 있습니다. 중국의 2026년 정책 방침에서는 시설 농업의 현대화와 인공지능, 사물인터넷(IoT), 로봇, 드론의 보다 광범위한 활용이 공식적으로 지지되고 있으며, 이를 통해 해당 지역의 장기적인 발전 기반이 강화되고 있습니다. 중동 역시 수직 농업 시장에서 전략적으로 중요한 위치를 차지하고 있으며, 2026년에는 Bustanica사가 소매, 호텔·외식, 대규모 케이터링 분야로 사업 범위를 확대할 예정입니다. 아프리카와 남미는 수직 농업 시장에서 여전히 초기 단계의 기회에 머물러 있으며, 프로젝트 활동은 제한적인 편이고, 당장 대규모 상업적 확장을 하기보다는 우선 도시 지역의 영양 공급이나 모듈형 도입 모델을 통해 전개될 가능성이 높은 상황입니다.

유럽의 수직 농업 시장은 현지산 실내 재배 농산물에 대한 소비자 수요가 높은 반면, 전력 비용의 급등과 자금 조달 조건이 까다로워지고 있어 상황이 복잡합니다. 존스 푸드 컴퍼니 리미티드는 오카도 그룹으로부터 거듭된 자금 지원을 받았음에도 불구하고, 2025년 4월에 파산 관리 절차에 들어갔습니다. 이는 수익성 확보가 기대되지 않는 상황에서는 비용 압박으로 인해 규모 확대에 대한 야망이 무너져 버린다는 것을 보여줍니다. 한편, 이 지역은 기술 개발 분야에서 여전히 큰 영향력을 행사하고 있으며, 특히 네덜란드, 이탈리아, 영국을 기반으로 한 조명, 제어 시스템, 엔지니어링 플랫폼 분야에서 그 존재감이 두드러집니다. 2026년 4월 시스코가 플래닛 팜스 홀딩 S.p.A.와 제휴한 것은 유럽이 자율형 실내 농업 인프라 분야에서 활발한 움직임을 보이고 있으며, 영국 및 북유럽 시장으로의 지리적 확장을 계획하고 있음을 시사합니다. 따라서 유럽은 수직 농업 시장에 있어 여전히 중요한 위치를 차지하고 있지만, 그 성장 경로는 다른 몇몇 지역에 비해 에너지 비용이나 자본 관리의 엄격성에 크게 좌우됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the vertical farming market size was valued at USD 6.27 billion in 2025 and estimated to grow from USD 7.53 billion in 2026 to reach USD 12.11 billion by 2031, at a CAGR of 9.98% during the forecast period (2026-2031).

This report is Segmented by Growing Mechanism (Hydroponics, Aeroponics, and Aquaponics), by Farm Structure (Building-Based Vertical Farms and More), by Components (Lighting, Climate Control, and More), by Crop Type (Tomato, Berries, Lettuce and Leafy Greens, Pepper, and More), and by Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Vertical Farming Market Trends and Insights

Urban Demand for Local Pesticide-Free Produce

Urban demand for locally grown, pesticide-free produce has become a significant commercial driver for the vertical farming market, particularly among large grocery retailers and foodservice distributors in densely populated metropolitan areas. Gotham Greens, a major controlled-environment agriculture operator in North America, reported in February 2026 that the combined United States market share for indoor-grown packaged salads, lettuce, and herbs reached nearly 10%, with a 22% year-over-year increase during the 13-week retail measurement period ending January 2026. This indicates that indoor produce is transitioning from a niche premium shelf category to a broader market presence. This trend is important because the vertical farming market competes not only on pesticide-free labeling but also on predictable, year-round delivery, enabling retailers to reduce safety stock and manage replenishment more efficiently. Additionally, freshness offers a distribution advantage when produce is grown near metropolitan consumption hubs, as shorter transport times extend shelf life and reduce markdown pressures. As a result, the vertical farming market is gaining traction in retail accounts where reliability, provenance, and waste reduction are prioritized collectively rather than as separate purchasing factors.

Falling LED, Robotics, and Sensing Costs

Falling equipment costs remain one of the clearest growth supports for the vertical farming market because they improve the capital efficiency of new installations and upgrades. Signify launched its Philips GrowWise smart spectrum system in June 2025 and stated that the platform can deliver up to 6% energy savings or crop growth improvement through automatic spectral adjustment based on real-time sunlight conditions. A March 2026 study in Frontiers in Plant Science found that continuous, low-intensity LED lighting improved energy use efficiency by 21% and reduced LED application costs by 16.5% for lettuce, without yield loss under the tested conditions. The United Kingdom Agri-Tech Center also reported in March 2026 that its Advanced Crop Dynamic Control trial improved energy efficiency by 21% to 25% through plant-led lighting control, even while the system remained at an early stage of integration. As a result, the vertical farming market is seeing a practical reset in procurement economics, as operators who delayed purchases can now evaluate more efficient hardware and automation systems than those installed during the earlier venture-heavy build cycle.

High Electricity Load and Capital Intensity

Operating economics remain one of the largest constraints in the vertical farming market because fully enclosed production systems depend on energy-intensive lighting and climate-control infrastructure. Artificial LED lighting typically accounts for the largest electricity load in indoor farms, while cooling, ventilation, and dehumidification systems add substantial operating costs to maintain stable growing conditions. These cost pressures are especially challenging in regions with high industrial electricity prices, limiting the commercial viability of lower-margin crop categories and reinforcing industry focus on premium leafy greens and specialty produce. Local Bounti Corporation's filings with the U.S. Securities and Exchange Commission (SEC) underline how capital structure remains critical in this space, with the company reshaping debt and adding growth capital during 2025 and 2026 while continuing to optimize yields and capacity . The vertical farming market, therefore, continues to face a fundamental constraint: technical feasibility does not always translate into financially sustainable deployment.

Other drivers and restraints analyzed in the detailed report include:

- Climate-Resilient Year-Round Production

- Government Food-Security Incentives and Ag-Tech Funding

- Limited Economically Viable Crop Basket at Scale

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hydroponics was the largest growing mechanism in the vertical farming market, with a 56.7% share in 2025. Its lead came from a long commercial record in nutrient delivery, crop-cycle control, and root-zone management across several indoor farm formats. The hydroponic installed base also remained the deepest because many operator investments made between 2018 and 2023 were built around this system architecture. That installed base still shapes procurement, grower training, and input sourcing in the vertical farming industry. As a result, share rebalancing remains gradual even as newer systems improve.

Aeroponics is the fastest-growing technology and is projected to expand at a 13.1% CAGR during 2026-2031 in the vertical farming market. The model appeals to operators seeking better root-zone hygiene and additional water savings beyond those offered by standard recirculating hydroponic systems. Aquaponics is also gaining attention, where circular food systems and dual revenue streams can justify more operational complexity. JR East Startup and Platform announced a capital and business alliance in August 2025 to commercialize aquaponics-based circular food production, as its aquaponics facilities expanded to 5 sites across Japan. That supports the view that the vertical farming market is slowly expanding into integrated food systems rather than moving away from hydroponics all at once.

Building-based farms were the largest segment, accounting for 72.4% if the vertical farming market size in 2025. Their lead reflects a larger productive capacity, more integrated climate systems, and better fixed-cost absorption at a commercial scale. These projects also tend to attract institutional capital more easily because their operating models are clearer than in many smaller modular deployments. In practice, the largest building-based assets still set the benchmark for how the vertical farming market scales in metropolitan supply chains. That position has kept this structure at the center of high-volume commercial planning.

Shipping-container-based farms were the fastest-growing structure and are projected to grow at a 12.3% CAGR during 2026-2031. Their appeal comes from rapid deployment, geographic flexibility, and lower commitment for operators entering undersupplied regions. The July 2025 transfer of Freight Farms assets to Growcer, which included more than 500 active container farm locations, showed that demand for container-based systems persisted even after the original company failed. The Dubai GigaFarm project also highlights the other end of the scale spectrum, with the first components for the initial 20 of 200 planned growth towers shipped in 2025, and full project output targeted at 3,000 metric tons annually. Taken together, these patterns show that the vertical farming market uses container and building-based formats less as substitutes and more as complementary tools for different stages of market entry and scale-up.

Complete Report Scope:

- By Growing Mechanism

- Hydroponics

- Aeroponics

- Aquaponics

- By Farm Structure

- Building-based Vertical Farms

- Shipping-container-based Vertical Farms

- By Component

- Lighting Systems

- Climate Control Systems

- Sensors and Monitoring Devices

- Irrigation and Fertigation Systems

- Software and Control Platforms

- Farm Structure Materials and Growing Racks

- By Crop Type

- Lettuce and Leafy Greens

- Herbs

- Tomatoes

- Berries

- Cucumbers

- Peppers

- Microgreens

- Other Crops

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Netherlands

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Singapore

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Israel

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Egypt

- Rest of Africa

- North America

Geography Analysis

North America was the largest regional contributor to the vertical farming market, accounting for 41.8% of the market share in 2025. The region benefits from dense metropolitan retail networks, established cold-chain systems, and a concentration of technology capital that supports the scale of indoor farming. Local Bounti Corporation reported FY2025 sales of USD 48.37 million and serves around 13,000 retail doors, demonstrating the commercial reach already achieved by some United States operators. Canada continues to strengthen its position as a secondary hub, with GoodLeaf Farms raising USD 37.9 million (CAD 52 million) in November 2025, to double capacity at its Alberta and Quebec sites and to build a new research and development center in Ontario.

Asia-Pacific was the fastest-growing regional segment in the vertical farming market and is projected to grow at a 12.8% CAGR during 2026-2031. Land scarcity, food safety expectations, and stronger state-backed support for facility agriculture across Japan, China, Singapore, and South Korea are shaping growth. China's 2026 policy direction formally supports upgrades in facility agriculture and the broader use of artificial intelligence, the Internet of Things, robots, and drones, which strengthens the region's long-term deployment base. The Middle East also carries strong strategic weight in the vertical farming market, with Bustanica broadening its commercial reach into retail, hospitality, and large-scale catering in 2026. Africa and South America remain early-stage opportunities in the vertical farming market, with project activity still more limited and more likely to build first through smaller urban nutrition and modular deployment models than through immediate large-scale commercial rollouts.

Europe presents a more mixed picture in the vertical farming market, as strong consumer demand for local indoor produce sits alongside elevated electricity costs and tighter financing conditions. Jones Food Company Limited entered administration in April 2025 after repeated rounds of funding support from Ocado Group, illustrating how cost pressure can overwhelm scale ambition when profitability remains out of reach. At the same time, the region remains influential in technology development, especially through lighting, control systems, and engineering platforms tied to the Netherlands, Italy, and the United Kingdom. Cisco's April 2026 work with Planet Farms Holding S.p.A. signals that Europe remains active in autonomous indoor farming infrastructure and in planned geographic expansion to the United Kingdom and Nordic markets. Europe, therefore, remains important to the vertical farming market, but its growth path depends more tightly on energy costs and capital discipline than in some other regions.

- 80 Acres Farms Inc.

- Gotham Greens Holdings LLC

- Local Bounti Corporation

- Crop One Holdings Inc.

- Oishii Farm Corporation

- GrowUp Farms Limited

- Planet Farms Holding S.p.A.

- Jones Food Company Limited

- Intelligent Growth Solutions Limited

- Urban Crop Solutions BV

- Signify N.V.

- ams-OSRAM AG

- Heliospectra AB

- Green Sense Farms Holdings, Inc.

- Vertical Future Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Urban demand for local pesticide-free produce

- 4.2.2 Falling LED, robotics, and sensing costs

- 4.2.3 Climate-resilient year-round production

- 4.2.4 Government food-security incentives and ag-tech funding

- 4.2.5 Carbon-credit and ESG premium revenue stacking

- 4.2.6 Waste-heat and low-cost power co-location economics

- 4.3 Market Restraints

- 4.3.1 High electricity load and capital intensity

- 4.3.2 Limited economically viable crop basket at scale

- 4.3.3 Tighter lender and insurer underwriting after sector failures

- 4.3.4 Food-safety and biologic-risk insurance inflation

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Growing Mechanism

- 5.1.1 Hydroponics

- 5.1.2 Aeroponics

- 5.1.3 Aquaponics

- 5.2 By Farm Structure

- 5.2.1 Building-based Vertical Farms

- 5.2.2 Shipping-container-based Vertical Farms

- 5.3 By Component

- 5.3.1 Lighting Systems

- 5.3.2 Climate Control Systems

- 5.3.3 Sensors and Monitoring Devices

- 5.3.4 Irrigation and Fertigation Systems

- 5.3.5 Software and Control Platforms

- 5.3.6 Farm Structure Materials and Growing Racks

- 5.4 By Crop Type

- 5.4.1 Lettuce and Leafy Greens

- 5.4.2 Herbs

- 5.4.3 Tomatoes

- 5.4.4 Berries

- 5.4.5 Cucumbers

- 5.4.6 Peppers

- 5.4.7 Microgreens

- 5.4.8 Other Crops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Netherlands

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Singapore

- 5.5.3.5 South Korea

- 5.5.3.6 Australia

- 5.5.3.7 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Israel

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 80 Acres Farms Inc.

- 6.4.2 Gotham Greens Holdings LLC

- 6.4.3 Local Bounti Corporation

- 6.4.4 Crop One Holdings Inc.

- 6.4.5 Oishii Farm Corporation

- 6.4.6 GrowUp Farms Limited

- 6.4.7 Planet Farms Holding S.p.A.

- 6.4.8 Jones Food Company Limited

- 6.4.9 Intelligent Growth Solutions Limited

- 6.4.10 Urban Crop Solutions BV

- 6.4.11 Signify N.V.

- 6.4.12 ams-OSRAM AG

- 6.4.13 Heliospectra AB

- 6.4.14 Green Sense Farms Holdings, Inc.

- 6.4.15 Vertical Future Ltd.