|

시장보고서

상품코드

2061624

다발성 경화증 치료제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Multiple Sclerosis Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

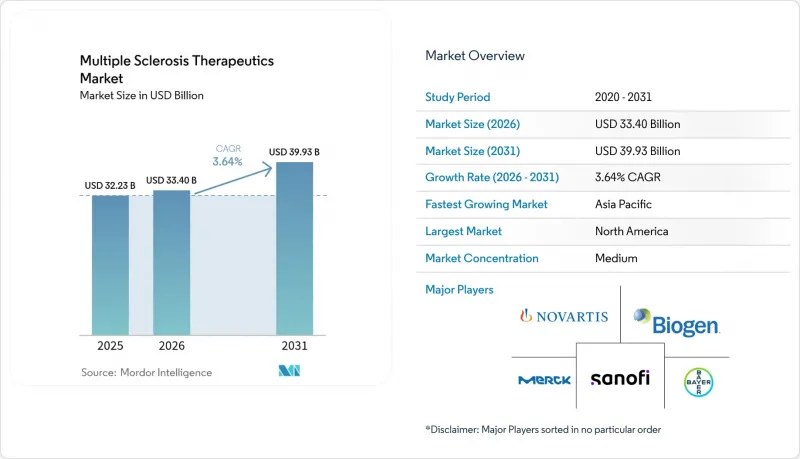

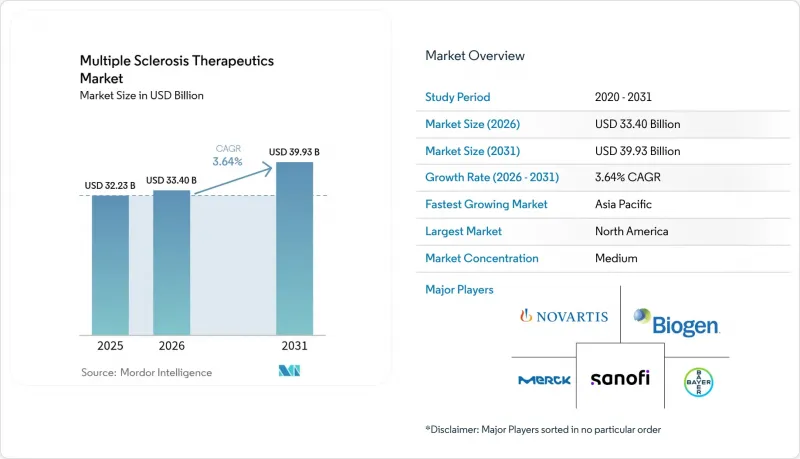

Mordor Intelligence에 의하면, 다발성 경화증 치료제 시장 규모는 2025년 322억 3,000만 달러로 평가되었습니다. 2026년 334억 달러에서 2031년까지 399억 3,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 3.64%를 나타낼 것으로 예측됩니다.

본 보고서는 약물 유형(고분자, 저분자), 투여 경로(경구, 주사제, 기타), 적응증(재발-완화형 다발성 경화증(RRMS), 이차 진행형 다발성 경화증(SPMS), 원발성 진행형 다발성 경화증(PPMS), 일과성 뇌허혈 발작(CIS)), 약물 분류별(면역조절제, 단일클론항체, S1P 조절제, 항종양제/기타), 유통 채널(병원 등), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러)으로 표시되어 있습니다.

세계의 다발성 경화증 치료제 시장 동향 및 분석

전 세계 다발성 경화증(MS) 유병률 증가

MRI 검사 접근성 확대와 질환의 초기 활동을 포착하는 개정된 진단 기준의 보급으로 인해, 2024년에는 전 세계 다발성 경화증(MS) 진단 건수가 280만 건을 넘어섰습니다. 유병률은 여전히 고위도 지역에서 가장 높은 수준을 유지하고 있는 반면, 비타민 D 노출량 감소, 오염, 그리고 취약 집단의 엡스타인-바 바이러스(EBV) 혈청 양성률과 같은 위험 요인이 겹치는 급속한 도시화가 진행되는 지역에서는 발병률이 가속화되고 있습니다.

각사는 이러한 분포에 맞추어 제품을 출시하고 있으며, 유병률이 높은 지역에서는 오리지널 바이오의약품을 우선적으로 공급하고, 예산 압박이 심하고 진단 시장이 급속히 확대되고 있는 지역에서는 바이오시밀러나 제네릭 의약품을 활용하고 있습니다. 조사 대상 시장에서 방사선과 및 신경과 네트워크와의 제휴는 환자 조기 확보, 치료 기간 연장, 그리고 환자 1인당 생애 가치 향상으로 이어지는 길로 자리 잡고 있습니다. 또한, MRI 및 혈청 마커를 중심으로 한 초기 검사를 표준화하고 신속한 의뢰 체계를 구축함으로써 치료 시작을 앞당기는 임상의를 위한 교육 프로그램 역시 시장에 긍정적인 영향을 미치고 있습니다. 이러한 역학에 기반한 노력은 수요를 안정화시키고, 예측 기간 동안의 가격 변동 영향을 완화하는 데 도움이 됩니다.

고효능 단일클론 항체를 이용한 DMT로의 전환

규제 당국은 2024년부터 2025년에 걸쳐 재발성 다발성 경화증(MS) 치료용 여러 가지 단일클론 항체를 승인했습니다. 이러한 승인은 연간 재발률의 현저한 감소와 MRI 소견상 병변의 강력한 억제를 근거로 합니다. 임상 현장에서는 진행성 초기 질환 환자에 대한 고효능 치료법의 조기 도입으로 전환되어, 2025년에는 치료 시작까지의 중앙값이 1.8년으로 단축되었습니다. 2024년에 승인된 오클레리주맙 및 오파투무맙 피하주사 제제 덕분에 간호사의 감독 하에 가정에서 투여할 수 있게 되었으며, 의료 자원이 제한된 환경에서 정맥주사 센터의 병목 현상이 해소되었습니다. 이러한 약물에 대한 보험 급여 동향은 투여량 및 복약 순응도를 확인하는 디지털 지원 도구의 보급과 연동되는 경향을 보이고 있으며, 이는 현재 다발성 경화증 치료제 시장에서 급여 논의의 중요한 요소로 작용하고 있습니다. 의사가 질환의 초기 단계에서 중증도에 맞추어 치료를 시행하는 사례가 늘어남에 따라, 가치 제안에서는 질환의 진행 억제나 급성기 의료 사건의 감소가 강조되고 있으며, 이러한 점들은 비용 대비 효과 모델에서 뒷받침되고 있습니다. 치료 과정의 초기 단계에서 고효능 치료법을 이처럼 활용하는 것은 향후 예측 기간 동안 지속적인 도입을 촉진할 것입니다.

면역억제성 DMT의 이상반응 프로파일

CD20 및 α4 인테그린 단일클론 항체는 JC 바이러스 선별 검사나 진행성 다발성 백질뇌증에 대한 영상 검사의 강화 등, 체계적인 모니터링과 위험 완화 조치가 필요한 위험을 수반합니다. 규제 당국은 예방접종 일정 및 감염병 감시를 지도하는 안전성 프로그램과 첨부문서의 갱신을 규정하고 있으며, 이로 인해 처방 의사의 진료 조정 업무가 더욱 복잡해지고 있습니다. 빈번한 임상 검사나 영상 검사의 필요성은 비용 증가를 초래하며, 설령 그 유효성이 설득력 있다 하더라도, 알려진 위험 인자를 가진 환자에게 이러한 검사를 선택하는 것을 방해할 수 있습니다. 시판 후 약물감시 기록에는 면역 억제와 관련된 중증 감염증이 기재되어 있으며, 이로 인해 정기적인 첨부문서 개정 및 진료상 권고가 이루어지고 있습니다.

부문별 분석

2025년에는 고분자 의약품이 매출의 58.60%를 차지했으며, 피하 투여 제제 및 간호사의 감독 하에 이루어지는 재택 투여를 지원하는 케어 모델에 힘입어 2031년까지 연평균 7.50%의 성장률을 보일 것으로 전망됩니다. 바이오의약품 시장에서는 항체가 주류를 이루고 있으며, 연 2회 또는월1회 투여로 인해 일상적인 의사결정 부담이 줄어들기 때문에 치료의 지속성이 향상되고, 재발에 따른 급성기 의료 이용이 감소합니다. 다발성 경화증 치료제 시장에서는 연결 기기나 환자 보고 결과(PRO) 도구를 통한 실세계 데이터 수집이라는 지불 주체의 요구 사항을 충족하는 고분자 플랫폼이 선호되고 있습니다. 저분자 약물은 경구 투여의 편의성과 신속한 치료 개시 덕분에 주사에 대한 거부감을 줄여 신규 환자의 접근성을 높일 수 있다는 점에서 전략적으로 중요한 위치를 계속 차지하고 있습니다. 복약 순응도 관리의 디지털화가 포장 및 허브 서비스로 확대되는 가운데, 제약사들은 보험 적용 범위 및 환급 확인 절차를 간소화하는 통합을 중시하고 있습니다.

2025년에는 주사제가 매출에서 주도적인 위치를 차지하며 시장 점유율의 48.02%를 차지했습니다. 이는 인터페론, 글라티라머 아세테이트, 정맥 주사형 항체 등의 치료법이 확립된 역할을 수행하고 있음을 보여주며, 이들 모두는 통제된 투여 환경이 필요합니다. 한편, 경구 요법은 8.50%의 성장률이 예상되며, 이는 전체 시장의 연평균 성장률(CAGR)의 2배 이상에 해당합니다. 이러한 성장을 이끄는 주요 요인은 하루 한 번 투여하는 S1P 조절제의 매력에 있습니다. 특히, 치료 시작 첫해에 간소화된 일상적인 치료를 선호하는 환자에게 있어 그 이점은 뚜렷합니다. 이러한 추세는 환자가 보고한 선호도와 실제 복용 준수 데이터 간의 일치로 더욱 뒷받침되며, 특히 그 유효성이 다른 치료법과 동등한 경우 경구 요법의 채택을 뒷받침하는 근거가 되고 있습니다. 동시에, 피하 투여형 단일클론 항체는 치료 과정을 간소화하고 있습니다. 높은 유효성을 유지하면서 정맥 주사 투여를 위한 내원 횟수를 줄임으로써, 특히 정맥 주사 투여 체계가 제한적인 지역에서 뚜렷한 이점을 제공합니다. 이러한 변화하는 추세로 인해, 투여 빈도가 낮고 철저한 임상 모니터링을 중요시하는 환자들에게 주사제가 계속해서 필수적인 치료제가 될 것임이 보장됩니다.

지역별 분석

2025년에는 환자 1인당 지출액 증가, 신속한 규제 심사, 그리고 보험사의 적시 접근 결정에 힘입어 북미가 매출의 41.76%를 차지했습니다. 현재 지역별 정책 논의에서는 실제 현장에서 장애의 양상이 임상시험 결과와 다를 경우 약제비의 일부를 환급하는 성과연동형 계약이 중시되고 있습니다. 이러한 접근 방식은 입증된 치료 지속률과 기능적 결과에 대한 중점을 더욱 강화하고 있습니다. 고효능 의약품의 바이오시밀러가 미국 시장 진출을 앞두고 있는 가운데, 오리지널 제약사들은 분자적 동일성을 넘어선 차별화를 꾀하기 위해 기기 개선 및 지원 체계 구축에 주력하고 있습니다. 통합 의료 네트워크에 소속된 의료 제공업체는 지불자의 감사 요건을 충족하는 폐쇄형 루프 데이터를 수집할 수 있는 시스템을 갖추고 있어, 복약 순응도에 기반한 보상 제도의 혜택을 누리는 데 유리한 입장에 있습니다. 이러한 요인들로 인해 다발성 경화증 치료제 시장은 시스템 차원의 가치를 입증하는 실세계 데이터에 계속해서 주목하고 있습니다.

유럽은 2025년 매출에서 큰 비중을 차지하며, 독일, 영국, 프랑스, 이탈리아, 스페인이 매출의 대부분을 차지했습니다. 이러한 동향은 순비용에 영향을 미치기 때문에 기준 가격 책정 및 통제된 접근 방식에 대한 의존도가 높아지고 있음을 반영하고 있습니다. 영국의 국립보건기술평가원(NICE)은 비용 대비 효과 기준을 강화하여, 긍정적인 지침을 얻기 위해서는 실제 임상 환경에서의 결과 및 복약 순응도 기록과 부합하는 근거를 요구하고 있습니다.

아시아태평양은 규제 절차의 신속화와 국가 승인과의 일관성이 강화되는 지역 승인에 힘입어, 2031년까지 연평균 7.22%의 성장이 예상됩니다. 2024년부터 2025년에 걸쳐 중국은 여러 가지 새로운 질환 수정 요법을 승인하고, 유럽보다 더 신속하게 보험 급여 절차로 이행함에 따라 출시 직후부터 대상 환자층이 확대되었습니다. 인도의 현지 제약사들은 수출용으로 기존 플랫폼을 확장하여, 브랜드 의약품의 가격 책정에 제약이 있는 지역에서 의약품 접근성을 높이고 있습니다. 반면, 혁신적인 기업들은 의료기기 특허와 지원 서비스를 통해 시장 점유율을 지키고 있습니다. 아시아태평양의 주요 도시는 주요 병원 네트워크 간 약국 청구 데이터와 전자건강기록(EHR) 데이터의 상호 운용성이 향상되고 있어, AI를 활용한 복약 순응도 플랫폼의 시범 도입에 최적의 환경입니다. 이러한 동향은 아시아태평양의 다발성 경화증 치료제 시장이 예측 기간 동안 규제 절차의 신속화와 디지털 기술 도입을 지속적으로 병행해 나갈 것임을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the multiple sclerosis therapeutics market size is projected to expand from USD 32.23 billion in 2025 and USD 33.40 billion in 2026 to USD 39.93 billion by 2031, registering a CAGR of 3.64% between 2026 to 2031.

This report is Segmented by Drug Type (Large-Molecule, Small-Molecule), Route (Oral, Injectable, Others), Indication (RRMS, SPMS, PPMS, CIS), Drug Class (Immunomodulators, Monoclonal Antibodies, S1P Modulators, Antineoplastics/Others), Distribution Channel (Hospital, and More), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global Multiple Sclerosis Therapeutics Market Trends and Insights

Rising Global Prevalence of MS

Diagnosed multiple sclerosis cases surpassed 2.8 million globally in 2024, driven by broader MRI access and the wider use of updated diagnostic criteria that capture earlier disease activity. Prevalence remains highest at higher latitudes, while incidence is accelerating in fast-urbanizing regions that face overlapping risks from lower vitamin D exposure, pollution, and Epstein-Barr virus seroprevalence among susceptible populations.

Companies are staging launches to align with this distribution, prioritizing originator biologics where prevalence is dense and using biosimilars or generics where budget pressure is stronger, and diagnosis ramps faster. Partnerships with radiology and neurology networks are becoming a route to earlier patient capture, longer therapy duration, and greater lifetime value per patient in the studied market. The market also benefits from clinician education programs that standardize early workups around MRI and serum markers and prompt referral pathways, thereby hastening treatment initiation. These epidemiology-linked actions support steadier volumes, helping cushion pricing cycles over the forecast period.

Shift Toward High-Efficacy Monoclonal-Antibody DMTs

Regulators cleared multiple monoclonal antibodies for relapsing MS in 2024-2025, with approvals anchored in robust reductions in annualized relapse rates and strong MRI lesion suppression. Clinical practice shifted toward earlier use of high-efficacy therapies for patients with aggressive early disease, reducing the median time to initiation to 1.8 years in 2025. Subcutaneous formulations of ocrelizumab and ofatumumab, approved in 2024, enabled home administration under nurse supervision and removed infusion-center bottlenecks in thinly resourced settings. Payer coverage trends for these agents often track digital supports that verify dosing and persistence, which now factor into reimbursement discussions in the multiple sclerosis therapeutics market. As physicians increasingly match therapy to early disease severity, value propositions emphasize disability slowing and reduced acute-care events, which resonate in cost-effectiveness models. This use of high-efficacy treatment earlier in the course of care supports sustained adoption over the forecast period.

Adverse-Event Profile of Immunosuppressive DMTs

CD20 and alpha 4 integrin monoclonal antibodies carry risks that require structured monitoring and risk-mitigation steps, including screening for JC virus and heightened imaging vigilance for progressive multifocal leukoencephalopathy. Regulators specify safety programs and label updates that guide vaccination scheduling and infection surveillance, thereby increasing the complexity of care coordination for prescribers. The need for frequent lab work and imaging adds cost that can deter selection for patients with known risk markers, even when efficacy is persuasive. Post-marketing pharmacovigilance records document serious infections associated with immunosuppression, which trigger periodic label refinements and practice advisories.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Once-Daily Oral DMTs

- Pipeline of CNS-Penetrant BTK Inhibitors

- High Treatment Cost and Payer Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Large-molecule drugs accounted for 58.60% of revenue in 2025 and are projected to grow at 7.50% annually through 2031, driven by subcutaneous formats and care models that support home administration with nurse oversight. antibodies dominate the biologics mix, with twice-yearly or monthly dosing that reduces day-to-day decision-making load, helping persistence and reducing acute care utilization tied to relapses. The multiple sclerosis therapeutics market favors large-molecule platforms that align with payer requirements for real-world data capture through connected devices and patient-reported outcome tools. Small molecules remain strategically important where oral convenience and rapid initiation can open access for new starts that avoid injection hesitancy. As digital adherence moves into packaging and hub services, manufacturers emphasize integration that simplifies verification for coverage and reimbursement.

In 2025, injectables dominated the revenue landscape, capturing 48.02% of the market share. This highlights the established role of therapies like interferons, glatiramer acetate, and infusion-based antibodies, all of which require controlled administration settings. Meanwhile, oral therapies are projected to grow at a rate of 8.50%, more than double the overall CAGR. A significant factor driving this growth is the appeal of once-daily S1P modulators, particularly for patients who prefer simplified routines during their initial year of treatment. This trend is further supported by the alignment between patient-reported preferences and real-world adherence data, which strengthens the case for oral therapies, especially when their efficacy is comparable to alternatives. At the same time, subcutaneous monoclonal antibodies are simplifying the treatment process. By reducing the need for infusion visits while maintaining high efficacy, they provide a notable advantage, particularly in regions with limited infusion capacity. These evolving dynamics ensure that injectables remain essential for patients who prioritize less frequent administration along with hands-on clinical monitoring.

Geography Analysis

North America accounted for 41.76% of revenue in 2025, driven by elevated per-patient spending, swift regulatory reviews, and timely payer access decisions. Regional policy discussions now emphasize outcome-linked contracts that partially refund drug costs if real-world disability trends differ from trial results. This focus strengthens the emphasis on verified persistence and functional outcomes. As biosimilars for high-efficacy agents approach their U.S. market debut, originators are shifting attention to device enhancements and supportive ecosystems, differentiating beyond molecule identity. Providers in integrated delivery networks are well-positioned to benefit from adherence-linked reimbursements, given their systems' ability to capture closed-loop data that meets payer audit requirements. These factors keep the Multiple Sclerosis Therapeutics market focused on real-world evidence demonstrating system-level value.

Europe captured a significant share of 2025 revenue, with Germany, the U.K., France, Italy, and Spain accounting for the majority of sales. Growth trends reflect a more substantial reliance on reference pricing and managed access to influence net costs. The U.K.'s National Institute for Health and Care Excellence has tightened cost-effectiveness thresholds, requiring evidence aligned with real-world outcomes and adherence documentation for positive guidance.

Asia-Pacific is projected to grow at 7.22% through 2031, driven by faster regulatory processes and provincial approvals increasingly aligned with national approvals. During 2024-2025, China approved several novel disease-modifying therapies and moved them into reimbursement pathways more quickly than European timelines, expanding eligible patient pools shortly after launch. Local producers in India have scaled older platforms for export, supporting access in regions with constrained branded pricing, while innovators defend their market share through device patents and support services. Urban centers across the Asia-Pacific are well-suited to pilot AI-enabled adherence platforms, given the growing interoperability of pharmacy claims and EHR data across major hospital networks. These trends indicate that the Multiple Sclerosis Therapeutics market in Asia-Pacific will continue to combine regulatory speed with digital adoption over the forecast period.

- Abbvie

- Acorda Therapeutics

- Bayer

- Biogen

- Bristol-Myers Squibb

- Celgene Corp.

- Roche

- GlaxoSmithKline

- InnoCare Pharma

- Johnson & Johnson Services, Inc. (Janssen)

- MediciNova Inc.

- Merck

- Mitsubishi Tanabe Pharma

- Novartis

- Pfizer

- Sanofi

- Teva Pharmaceutical Industries

- TG Therapeutics Inc.

- Tiziana Life Sciences PLC

- Viatris

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Prevalence of MS

- 4.2.2 Shift Toward High-Efficacy Monoclonal-Antibody DMTs

- 4.2.3 Broader Reimbursement & Access Programs in OECD Markets

- 4.2.4 Rapid Uptake of Once-Daily Oral DMTs

- 4.2.5 Pipeline of CNS-Penetrant BTK Inhibitors

- 4.2.6 AI-Driven Adherence Platforms Improving Real-World Persistence

- 4.3 Market Restraints

- 4.3.1 Adverse-Event Profile of Immunosuppressive DMTs

- 4.3.2 High Treatment Cost and Payer Pressure

- 4.3.3 Upcoming Biosimilar Wave Eroding Branded Prices

- 4.3.4 Insufficient Predictive Biomarkers for Therapy Selection

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Bargaining Power Suppliers

- 4.7.2 Bargaining Power Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Type

- 5.1.1 Large-molecule Drugs

- 5.1.2 Small-molecule Drugs

- 5.2 By Route of Administration

- 5.2.1 Oral

- 5.2.2 Injectable

- 5.2.3 Others

- 5.3 By Disease Indication

- 5.3.1 Relapsing-Remitting MS (RRMS)

- 5.3.2 Secondary Progressive MS (SPMS)

- 5.3.3 Primary Progressive MS (PPMS)

- 5.3.4 Clinically Isolated Syndrome (CIS)

- 5.4 By Drug Class

- 5.4.1 Immunomodulators

- 5.4.2 Monoclonal Antibodies

- 5.4.3 S1P Receptor Modulators

- 5.4.4 Antineoplastics / Others

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacy

- 5.5.2 Retail Pharmacy

- 5.5.3 Online/Specialty Pharmacy

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Acorda Therapeutics Inc.

- 6.3.3 Bayer AG

- 6.3.4 Biogen Inc.

- 6.3.5 Bristol Myers Squibb Co.

- 6.3.6 Celgene Corp.

- 6.3.7 F. Hoffmann-La Roche AG

- 6.3.8 GSK Plc

- 6.3.9 InnoCare Pharma

- 6.3.10 Johnson & Johnson Services, Inc. (Janssen)

- 6.3.11 MediciNova Inc.

- 6.3.12 Merck KGaA (EMD Serono)

- 6.3.13 Mitsubishi Tanabe Pharma

- 6.3.14 Novartis AG

- 6.3.15 Pfizer Inc.

- 6.3.16 Sanofi

- 6.3.17 Teva Pharmaceutical Industries Ltd.

- 6.3.18 TG Therapeutics Inc.

- 6.3.19 Tiziana Life Sciences PLC

- 6.3.20 Viatris Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment