|

시장보고서

상품코드

2061625

항공기 객실 인테리어 복합재료 부품 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aircraft Cabin Interior Composite Parts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

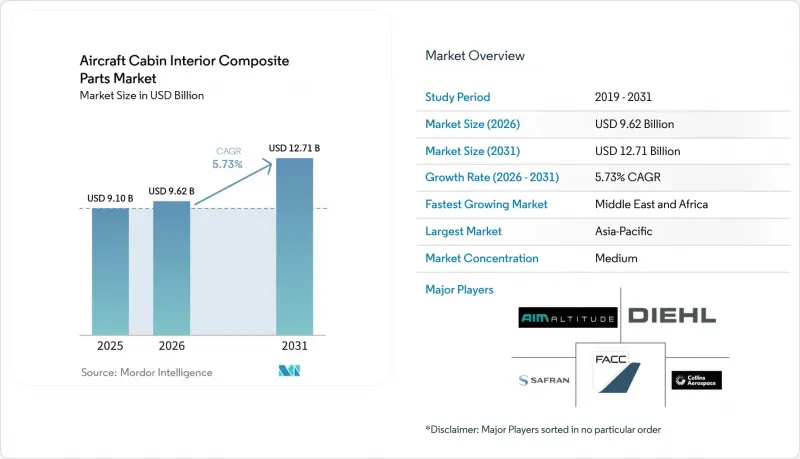

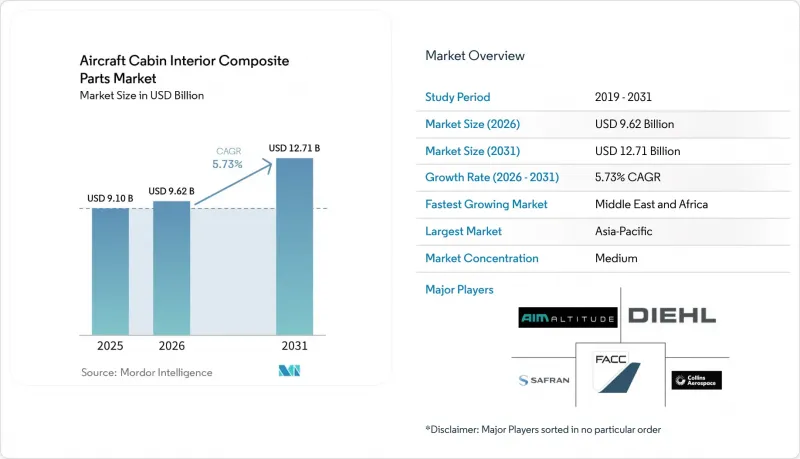

Mordor Intelligence에 의하면, 항공기 객실 인테리어 복합재료 부품 시장 규모는 2025년 91억 달러로 평가되었고, 2026년에는 96억 2,000만 달러로 추정되고, 2026-2031년 CAGR 5.73%로 성장을 지속할 전망이며, 2031년까지 127억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 항공기 유형별(나로우바디, 와이드바디, 리저널 제트 등), 부품 유형별(바닥 및 천장 패널, 측벽 및 라이너, 좌석 구조, 갤리 및 화장실, 머리 위 수납장 등), 최종 사용자별(OEM 및 애프터마켓), 그리고 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공기 객실 인테리어 복합재료 부품 시장 동향 및 분석

단일 통로 항공기 생산 확대가 복합재 패널 수요를 견인하고 있습니다.

에어버스는 2027년까지 월 75대의 A320neo 생산을 목표로 하고 있으며, 한편 보잉은 B737 MAX의 생산을 운항 중단 전 수준으로 회복해 가고 있어, 복합재 사이드월, 천장 라이너 및 갤리 기념물에 대한 기체 장착 수요가 증가하고 있습니다. 협폭기 기내에는 120-150제곱미터 규모의 복합재 표면이 사용되고 있으며, 생산량 증가에 따라 항공우주 등급 프리프레그 공급이 부족해지면서 OEM 업체들은 추가적인 2차 패널 제조업체를 인증할 수밖에 없는 상황입니다. 이에 대해 공급업체들은 AFP(알루미늄 섬유 프리프레그)의 생산 능력을 확대하여 대응하고 있습니다. 스피릿 에어로시스템즈는 A220 기체 납품 속도를 따라잡기 위해 2025년에 벨파스트 공장의 생산 능력을 30% 증대했습니다. 생산량 증가는 비용 절감 압박을 가중시키고 있으며, 제조업체들은 이익률을 유지하기 위해 적층 공정의 자동화나 재생 섬유의 활용을 서둘러야 하는 상황에 놓여 있습니다.

자동 섬유 배열(AFP) 기술이 리드 타임을 대폭 단축하고, 복잡한 성형을 가능하게 합니다.

ElectroImpact사의 AFP 4.0 플랫폼은 2025년에 분당 50.8미터의 적층 속도를 달성하고, 측벽의 사이클 타임을 8시간에서 90분 미만으로 단축하여, 동일한 교대 근무 시간 내에 경화가 가능하도록 했습니다. 그 결과, 생산성이 4배에서 8배로 향상됨에 따라, 이전에는 수작업으로 적층하던 곡면이 있는 변기 쉘과 같은 복잡한 부품에 대해서도 수익성이 확보되는 입찰이 가능해졌습니다. FACC사의 'Airspace XL' 오버헤드 빈 계약에서는 AFP를 활용하여 2미터에 달하는 스팬의 치수 공차를 ±0.5mm 이내로 유지하고 있으며, 이는 수작업으로는 도저히 따라갈 수 없는 정밀도입니다. 도입은 시간당 인건비가 40달러를 넘는 북미와 유럽에서 시작되었지만, 일본에서 수상 경력이 있는 열가소성 수지용 AFP 프로젝트는 아시아태평양이 자동화 격차를 좁혀가고 있음을 보여주고 있습니다.

항공우주 등급 복합재료의 높은 비용이 가격에 민감한 부문을 제약하고 있습니다.

헥셀의 페놀계 프리프레그 정가는 1kg당 80-120달러인 반면, 일반적인 에폭시계 프리프레그는 1kg당 25-35달러입니다. 이러한 가격 차이로 인해 ATR 72-600이나 엠브라에르 E2를 운항하는 지역 항공사들은 10-15%의 중량 증가라는 단점이 있음에도 불구하고 복합재 도입을 주저하고 있습니다. 중국공급 과잉으로 인해 2025년에는 T700 등급 섬유 가격이 1kg당 28달러까지 하락했으나, 유럽과 미국의 항공기 제조업체들은 추적 가능성에 대한 우려로 인해 저비용 제조업체를 인증하는 데 소극적인 태도를 보이고 있습니다. 그 결과 발생하는 비용 측면의 역풍으로 인해 저가형 항공기의 보급이 제한되어, 예측 연평균 성장률(CAGR)이 0.9% 하향 조정되었습니다.

부문별 분석

2025년 좁은 동체 항공기 프로그램에서 항공기 객실 인테리어 복합재료 부품 시장 점유율은 49.75%였으며, 에어버스가 월 75대의 A320neo 생산을 목표로 하고 있는 만큼, 시장 점유율은 꾸준히 확대될 전망입니다. 각 단일 통로 항공기의 객실에는 최대 150제곱미터의 복합재 측벽, 천장 패널, 수납장이 사용되므로, 생산량 증가에 따라 연간 수천 제곱미터 수요가 추가됩니다. 와이드 바디기는 기체 1대당 더 많은 복합재를 사용하지만, 생산 속도는 느립니다. 2025년 A350의 인도 대수는 총 90대였으나, B777X의 도입이 2026년으로 연기됨에 따라 단기적인 생산량은 제한적입니다.

비즈니스 제트기 시장은 2031년까지 연평균 성장률(CAGR) 6.75%를 나타낼 것으로 예측되며, Global 8000이나 G700과 같은 초장거리 모델이 7,500해리 이상의 항속 거리를 확보하기 위해 복합 소재에 의존하고 있기 때문에 다른 모든 부문을 능가하는 성장률을 보이고 있습니다. 제곱미터당 5,000-8,000달러에 달하는 고가의 캐빈 맞춤 제작 예산 덕분에, Bucher나 EnCore와 같은 공급업체들은 생산 대수가 적음에도 불구하고 AFP(Advanced Fiber Plexus) 및 열가소성 수지 용접 기술에 대한 투자 비용을 회수할 수 있게 되었습니다. 또한, 수년에 걸쳐 대규모 발주를 진행하는 분양 소유 프로그램이 수요를 더욱 뒷받침하고 있어, 이 부문이 전체 성장에서 차지하는 비중이 높아지고 있습니다.

지역별 분석

아시아태평양은 COMAC의 C919 생산이 50대로 확대되고, 에어 인디아와 인디고가 사상 최대 규모의 협폭기 주문을 한 데다, 지역 내 인건비가 비용 경쟁력 있는 복합재 제조를 뒷받침함에 따라 2025년 수요의 35.45%를 차지했습니다. 2025년 12월 JAMCO가 Iacobucci를 인수함에 따라, 해당 기업은 갤리 사업 기반을 확대하고 일본 공급업체의 유럽 애프터마켓 진출을 강화했습니다. 사프란이 하이데라바드에 패널 생산 시설을 검토하고 있다는 사실은 인도 내 개조 작업이 증가하는 가운데 현지화가 더욱 확대되고 있음을 보여줍니다.

중동 및 아프리카는 에미레이트 항공이 B777X를 도입하고, 카타르 항공이 A350을 인도받으며, 사우디아라비아가 '비전 2030' 항공 프로젝트에 투자함에 따라 2031년까지 연평균 성장률(CAGR) 7.10%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 예측됩니다. 2027년 가동을 목표로 하는 두바이의 2만 5,000제곱미터 규모 사프란 좌석 제조 공장은 공급망을 단축하고, 8-12주가 소요되는 물류 공정을 줄이기 위한 노력의 한 예입니다. 데넬 에어로스트럭처스가 2025년에 체결한 A350 측벽 제조 계약은 방위 산업 분야에서 민간용 복합재 내장재 분야로의 사업 다각화를 보여줍니다.

2025년, 북미와 유럽은 합쳐서 전 세계 수요의 절반 이상을 차지했으며, 그 기반이 되는 것은 보잉의 시애틀 거점, 에어버스의 함부르크 및 툴루즈 생산 라인, 그리고 스피릿 에어로시스템즈, 딜, 트라이엄프와 같은 1차 공급업체들의 긴밀한 네트워크입니다. 인건비 상승과 REACH 화학물질 규제로 인해 제조업체들은 AFP 자동화 및 열가소성 매트릭스로의 전환을 강요받고 있지만, 항공기 제조업체와의 근접성과 심도 있는 엔지니어링 전문 지식 덕분에 복잡하고 수익성이 높은 기념비적 구조물 및 비즈니스 제트기 내장재 분야에서 경쟁 우위를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the aircraft cabin interior composite parts market size is expected to grow from USD 9.10 billion in 2025 to USD 9.62 billion in 2026 and is forecasted to reach USD 12.71 billion by 2031 at a 5.73% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Narrowbody, Widebody, Regional Jets, and More), Component Type (Floor and Ceiling Panels, Sidewall and Liners, Seating Structures, Galleys and Lavatories, Overhead Stowage Bins, and More), End-User (OEM and Aftermarket), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aircraft Cabin Interior Composite Parts Market Trends and Insights

Ramp-Up of Single-Aisle Production Drives Composite Panel Demand

Airbus aims to build 75 A320neo units each month by 2027, while Boeing is restoring B737 MAX output to pre-grounding levels, pushing ship-set demand for composite sidewalls, ceiling liners, and galley monuments higher.A narrowbody cabin consumes 120-150 square meters of composite surface, and every increase in production rate tightens the supply of aerospace-grade prepregs, forcing OEMs to qualify additional Tier 2 panel fabricators. Suppliers respond by expanding AFP capacity; Spirit AeroSystems raised throughput 30% at its Belfast plant in 2025 to keep pace with A220 fuselage deliveries. Higher volumes amplify cost-reduction pressure, compelling fabricators to automate layup and explore recycled fibers to sustain margins.

Automated Fiber Placement Slashes Turnaround Time and Unlocks Complexity

Electroimpact's AFP 4.0 platform reached 50.8 meters per minute layup rates in 2025, shrinking sidewall cycle times from 8 hours to under 90 minutes and enabling same-shift curing. The resulting four- to eight-fold productivity gain supports profitable bids on complex parts, such as contoured lavatory shells, that were previously hand-laid. FACC's Airspace XL overhead-bin contract leverages AFP to hold dimensional tolerances within +-0.5 mm over two-meter spans, precision that manual methods cannot match. Although adoption began in North America and Europe, where labor costs exceed USD 40 per hour, award-winning thermoplastic-AFP projects in Japan show that the Asia-Pacific region is closing the automation gap.

High Cost of Aerospace-Grade Composites Constrains Price-Sensitive Segments

Hexcel's phenolic prepregs list at USD 80-120 per kg, compared with USD 25-35 per kg for standard epoxy towpregs, a gap that deters regional carriers operating ATR 72-600s or Embraer E2s from adopting composites, despite a 10-15% weight penalty. Overcapacity in China drove T700-grade fiber prices to USD 28 per kg in 2025, but Western airframers are hesitant to qualify low-cost mills due to concerns over traceability. The resulting cost headwind limits penetration in lower-tier aircraft, trimming forecast CAGR by 0.9 percentage points.

Other drivers and restraints analyzed in the detailed report include:

- Airline Demand for Lightweight Cabins Intensifies Amid Rising SAF Costs

- Closed-Loop Recycled-Carbon Programs Gain Momentum in Sidewall Applications

- Lengthy Certification and Qualification Cycles Delay Time-to-Market

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The aircraft cabin interior composite parts market share for narrowbody programs is 49.75% in 2025 and is poised to expand steadily as Airbus targets 75 A320neo units per month. Each single-aisle cabin consumes up to 150 square meters of composite sidewalls, ceiling panels, and bins, so incremental production adds thousands of square meters of annual demand. Widebodies deploy more composites per frame but progress at slower build rates. A350 deliveries totaled 90 units in 2025, while the B777X entry was pushed back to 2026, resulting in limited near-term volume.

Business jets are forecast to grow at a 6.75% CAGR through 2031, outpacing all other categories as ultra-long-range models like the Global 8000 and G700 rely on composite materials to reach 7,500-plus nautical miles. High cabin customization budgets of USD 5,000-8,000 per square meter enable suppliers such as Bucher and EnCore to recoup investments in AFP and thermoplastic welding, despite lower unit counts. Fractional-ownership programs, which place large multi-year orders, further underpin demand, lifting the segment's contribution to overall growth.

Geography Analysis

Asia-Pacific accounted for 35.45% of 2025 demand as COMAC's C919 ramped to 50 units, Air India and IndiGo placed record narrowbody orders, and regional labor costs supported cost-competitive composite fabrication. JAMCO's acquisition of Iacobucci in December 2025 expanded its galley footprint and underlined Japanese suppliers' push into the European aftermarket. Safran's evaluation of a Hyderabad panel facility signals broader localization as Indian retrofit work rises.

The Middle East and Africa is expected to be the fastest-growing region, at a 7.10% CAGR through 2031, as Emirates inducts B777X aircraft, Qatar Airways receives A350s, and Saudi Arabia invests in Vision 2030 aviation projects. Safran's forthcoming 25,000 square-meter Dubai seat plant, due in 2027, exemplifies moves to shorten supply lines and cut 8-12-week logistics legs. Denel Aerostructures' 2025 contract to build A350 sidewalls illustrates diversification away from defense toward civil composite interiors.

North America and Europe jointly held just over half of global demand in 2025, anchored by Boeing's Seattle hub, Airbus's Hamburg and Toulouse lines, and a dense network of Tier 1 suppliers, including Spirit AeroSystems, Diehl, and Triumph. Rising labor costs and REACH chemical rules are pushing fabricators toward AFP automation and thermoplastic matrices, yet proximity to airframers and deep engineering expertise sustain a competitive advantage for complex, high-margin monuments and business-jet interiors.

- AVIC Cabin Systems (UK) Limited

- RTX Corporation

- Diehl Stiftung & Co. KG

- FACC AG

- JAMCO Corporation

- The Gill Corporation

- The NORDAM Group LLC

- Triumph Group, Inc.

- Safran SA

- Singapore Technologies Engineering Ltd.

- RECARO Aircraft Seating GmbH & Co. KG

- Thompson Aero Seating

- Geven SPA

- Bucher Leichtbau AG

- EnCore Corporate, Inc.

- Elbe Flugzeugwerke GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ramp-up of single-aisle production (A320neo/B737 MAX)

- 4.2.2 Automated fiber-placement (AFP) slashing panel TAT

- 4.2.3 Airline demand for lightweight cabins to cut fuel burn

- 4.2.4 Closed-loop recycled-carbon programs for sidewalls

- 4.2.5 Hydrogen-electric demonstrators requiring cryogenic-ready cabins

- 4.2.6 Stricter FST (fire-smoke-toxicity) regulations

- 4.3 Market Restraints

- 4.3.1 High cost of aerospace-grade composites

- 4.3.2 Lengthy certification and qualification cycles

- 4.3.3 EU chemical-policy volatility disrupting epoxy/phenolic supply

- 4.3.4 Skilled-labor shortages in AFP and thermoplastic welding

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Narrowbody Aircraft

- 5.1.2 Widebody Aircraft

- 5.1.3 Regional Jets

- 5.1.4 Business Jets

- 5.2 By Component Type

- 5.2.1 Floor and Ceiling Panels

- 5.2.2 Sidewall and Liners

- 5.2.3 Seating Structures

- 5.2.4 Galleys and Lavatories

- 5.2.5 Overhead Stowage Bins

- 5.2.6 Other Interior Component

- 5.3 By End-User

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 AVIC Cabin Systems (UK) Limited

- 6.4.2 RTX Corporation

- 6.4.3 Diehl Stiftung & Co. KG

- 6.4.4 FACC AG

- 6.4.5 JAMCO Corporation

- 6.4.6 The Gill Corporation

- 6.4.7 The NORDAM Group LLC

- 6.4.8 Triumph Group, Inc.

- 6.4.9 Safran SA

- 6.4.10 Singapore Technologies Engineering Ltd.

- 6.4.11 RECARO Aircraft Seating GmbH & Co. KG

- 6.4.12 Thompson Aero Seating

- 6.4.13 Geven SPA

- 6.4.14 Bucher Leichtbau AG

- 6.4.15 EnCore Corporate, Inc.

- 6.4.16 Elbe Flugzeugwerke GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment