|

시장보고서

상품코드

2073469

민간 항공기 객실 인테리어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Commercial Aircraft Cabin Interior - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

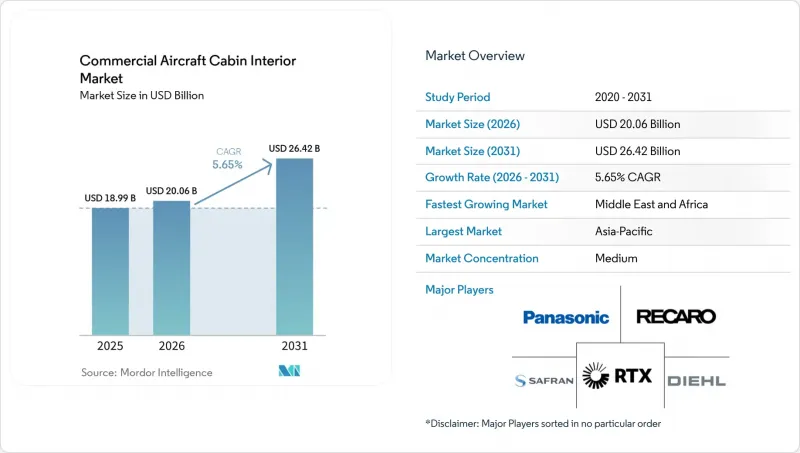

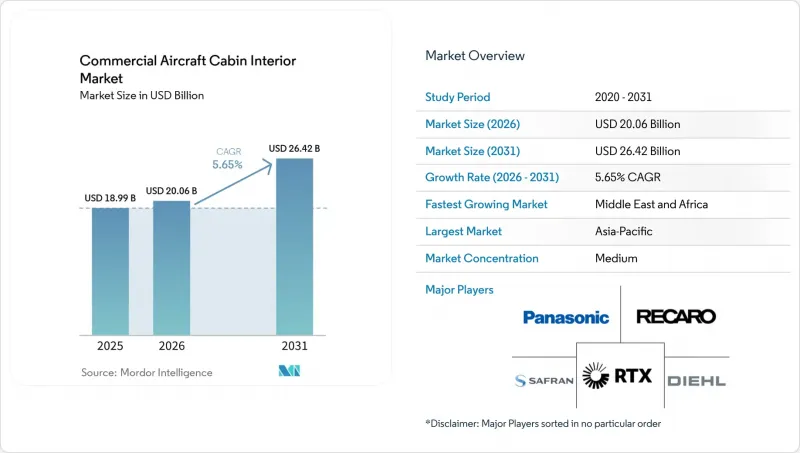

Mordor Intelligence에 의하면, 민간 항공기 객실 인테리어 시장 규모는 2025년 189억 9,000만 달러로 평가되었습니다. 2026년에는 200억 6,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR 5.65%로 성장을 지속하여, 2031년에는 264억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(좌석, 객실 조명, 기타), 항공기 유형(협폭기, 광폭기, 기타), 객실 등급(일등석, 비즈니스석, 기타), 장착 유형(OEM 및 애프터마켓), 소재(복합재료, 기타), 지역(북미, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 민간 항공기 객실 인테리어 시장 동향 및 인사이트

객실 공간의 수익화를 위해 프리미엄 이코노미석으로의 개조가 급증하고 있습니다.

각 항공사는 항공기의 수용 인원을 늘리지 않으면서도 수익성을 높일 수 있는 프리미엄 이코노미 구역을 도입하기 위해 객실 재구성을 가속화하고 있습니다. 델타항공은 프리미엄 이코노미 클래스 도입 후 노선 수익률이 15% 상승했으며, 2026년에 도입 프로그램이 완료되면 연간 5억 달러의 매출 증가가 예상됩니다. 유나이티드 항공은 2024년 말까지 이미 200대 이상의 항공기를 개조했으며, 좌석 간격 확대와 기내식 서비스 향상을 병행함으로써 레저 여행객의 업그레이드 수요와 비용에 민감한 비즈니스 여행객 모두를 유치했습니다. 접근성 기준을 준수하기 위해 화장실과 통로의 개보수 공사를 동시에 진행함으로써, 가동 중단 시간을 일괄적으로 관리하고 프로젝트의 경제성을 높이고 있습니다. 객실 밀도를 최적화하여 수익 희석화를 억제하고 있으며, 이용률이 높은 나로우바디 항공기가 첫 도입 기종으로 주목받고 있습니다. 북미의 주요 항공사들이 이익 증가를 입증하는 가운데, 유럽과 아시아태평양의 항공사들도 유사한 개선 프로그램을 빠른 속도로 추진하고 있습니다.

16-g 좌석 인증 의무화가 좌석 교체 주기를 앞당기고 있습니다.

연방항공청(FAA)의 16-g 동적 검사 기준에 따라, 2009년 이전에 설치된 구형 좌석을 교체해야 합니다. 아메리칸 항공은 협폭기 및 지역 항공기 전 기종에 대해 이 규제를 준수하기 위해 2024년에 21억 달러를 예산에 반영하고, 운항 중단에 따른 벌금을 피하기 위해 규정 준수 일정을 앞당겼습니다. 노후화된 CRJ 및 ERJ 기종을 운항하는 지역 항공사들도 자본 여력이 부족한 상황임에도 불구하고 마찬가지로 기종 교체를 피할 수 없게 되어, 집중적인 발주 붐이 일어나 공급업체의 생산 능력을 한계에 몰아넣고 있습니다. 제조업체는 생산 라인보다 인증 검사소를 우선시하고 있어, 규제 대상이 아닌 좌석 프로그램의 리드타임이 길어지고 있습니다. 이 규정이 세계에 미치는 영향력은 FAA가 사실상의 기준을 승인하도록 허용하는 양자 간 감항성 협정에서 비롯된 것이며, 신흥 시장의 항공사들도 이와 유사한 교체 주기에 휘말리고 있습니다.

좌석 및 발포재 인증 과정에서 발생하는 공급망 병목 현상

개정된 난연성 프로토콜에 따르면, FAA 검사를 통과하기 위해서는 새로운 형태의 배합이 필요하며, 해당 검사 기간은 현재 12-18개월에 달하고 있습니다. RECARO Aircraft Seating은 2024년 와이드바디 항공기용 프로그램의 납기가 평균 6-8개월 지연되고 있다고 밝혔습니다. Thompson Aero는 대체 소재가 검사 절차를 통과할 때까지 최신 프리미엄 이코노미 클래스 좌석의 판매를 일시적으로 중단했습니다. 높은 운항 빈도로 운항되는 협폭기체를 운용하는 항공사는 내장 공사 지연으로 인해 예정된 대규모 점검 기간을 초과하게 될 경우 수익에 타격을 입게 됩니다. 이러한 병목 현상은 개선의 추진력을 약화시켜, 예상 연평균 성장률(CAGR)을 0.8포인트 낮췄습니다.

부문별 분석

2025년, 좌석은 민간 항공기 객실 인테리어 시장 점유율의 29.88%를 차지하며, 시장에서 주요 가치 창출 요인으로 자리매김했습니다. 각 항공사는 프리미엄 비즈니스 클래스 좌석 1석당 1만 5,000-2만 5,000달러, 이코노미 클래스 모듈 1개당 2,500-4,000달러를 지불하고 있으며, 좌석 프로그램이 개조 예산의 주축을 이루고 있음이 확인되었습니다. 한편, 기내 인터넷 접속(IFEC) 플랫폼은 접속 서비스가 단순한 혜택에서 수익원으로 변화함에 따라 8.26%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다.

새로운 수요는 경량화, 무선 충전, 승무원용 경보 기능을 통합한 좌석에 집중되고 있습니다. 이코노미 클래스의 좌석 배치는 고밀도화가 진행되는 한편, 승객의 불편함을 줄이기 위해 슬림하고 인체공학에 기반한 설계가 중시되고 있습니다. 한편, IFEC 제공업체들은 대역폭의 이중화를 확보하기 위해 위성에 의존하지 않는 아키텍처로 전환하고 있습니다. 민간 항공기 객실 인테리어 시장에서는 IFEC 도입과 순추천지수(NPS) 향상 간의 상관관계가 지속적으로 확인되고 있으며, 이를 통해 항공사는 협폭기 노선에서도 라운지와 같은 경험을 추가 판매할 수 있게 되었습니다. 갤리 재설계와 LED 조명 업그레이드는 좌석 및 IFEC에 대한 투자를 보완하는 것이지만, 부품 가격이 저렴하기 때문에 그 절대 금액은 여전히 소규모에 그치고 있습니다.

협폭기(narrow-body)는 2025년 수요의 48.62%를 차지하며, 민간 항공기 객실 인테리어 시장 규모에서 가장 큰 절대적 점유율을 차지했습니다. 비행 시간당 수요 밀도와 OEM 수주 잔고에서 70%의 점유율을 바탕으로, 이 부문은 좌석 및 주요 장비 공급업체들에게 여전히 매우 중요한 위치를 차지하고 있습니다. 지역 제트기는 지방 도시 간 직항 노선 증가에 힘입어 6.78%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다.

와이드 바디 항공기는 프리미엄 클래스의 혁신에 중점을 두고 있으며, 풀 하이트 프라이버시 도어, 셀프 서비스 라운지, 차세대 IFEC는 장거리 노선에서 필수적인 장비로 자리 잡았습니다. 한편, A380 등 와이드바디 항공기의 경우, 퇴역이 가속화되고 있어 내장재에 대한 투자는 소극적인 임베디드니다. 민간 항공기 객실 인테리어 시장에서는 각 항공사가 운항 능력의 적정화에 주력하고 있으며, 그 결과 과도한 규모의 기종에서 가동률이 높은 단일 통로 항공기나 차세대 지역 제트기로 자본이 간접적으로 재분배되고 있습니다.

지역별 분석

아시아태평양은 2025년 지출의 37.11%를 차지하며, 민간 항공기 객실 인테리어 시장에서 가장 영향력 있는 지역으로 자리매김했습니다. 중국만 해도 2024년에 400대 이상의 신조 항공기를 인도받았으며, 2030년까지 연간 평균 500대를 도입하는 것을 목표로 하고 있어 안정적인 라인핏 수요를 창출하고 있습니다. 인도에서는 항공 수요의 급증과 적극적인 기종 확충 계획이 추가적인 호재로 작용하고 있는 반면, 일본은 프리미엄 운임 점유율을 유지하기 위해 고급 객실 개선에 투자를 집중하고 있습니다. 동남아시아의 저비용 항공사(LCC)는 운임을 낮게 유지하기 위해 신속한 회전율과 높은 좌석 수를 중시하는 통일된 기내 인테리어를 채택하고 있습니다.

중동 및 아프리카는 2031년까지의 연평균 성장률(CAGR)이 7.31%로, 가장 빠른 성장세를 보이고 있습니다. 에티오피아 항공은 객실 인테리어 개보수와 아시아·북미 노선 확장을 병행하며 와이드바디 항공기의 성장을 주도하고 있습니다. 이와 대조적으로, 남아프리카 항공은 재편 기간을 활용해 기내 인테리어를 표준화하고, 기종 간 상호 운용성을 높이고 있습니다. 인프라 부족, MRO(정비·수리·오버홀) 역량의 한계, 환율 제약 등이 걸림돌로 작용하고 있지만, 긍정적인 인구 동향과 관광 산업의 회복이 이러한 장애 요인을 상쇄하고 있습니다. 민간 항공기 리스 회사는 최신 객실 인테리어를 갖춘 비교적 새로운 항공기를 도입함으로써, 막대한 설비 투자 없이도 현대화를 가속화하는 데 있어 매우 중요한 역할을 수행하고 있습니다. 운항 기수는 적지만, 중동의 항공사들은 프리미엄 클래스의 동향에 지대한 영향력을 행사하고 있습니다. 만안 지역 국가들의 국적 항공사들은 샤워 시설, 사교 공간, 맞춤형 조명을 갖춘 초장거리 노선용 기내 설계를 선도적으로 도입해 왔으며, 그 영향이 다른 지역으로도 확산되고 있습니다. 남미에서는 팬데믹 이후 항공사들의 기단 합리화에 따라, 주로 협폭기 개조를 중심으로 활동이 완만하지만 꾸준히 진행되고 있습니다. 이러한 지역별 상반된 동향으로 인해 민간 항공기 객실 인테리어 시장은 다양성을 유지하며, 지역적 충격에 대해서도 탄력성을 유지하고 있습니다.

북미와 유럽에서는 성숙한 교체 주기가 나타나고 있으며, 민간 항공기 객실 인테리어 시장은 개조 프로그램에 중점을 두고 있습니다. 미국의 항공사들은 미국 교통부(DOT)가 정한 접근성 관련 기한을 준수하는 것과, 광고 수익원을 창출하는 커넥티드 객실 생태계 도입에 주력하고 있습니다. 유럽의 항공사들은 지속가능성에 대한 요구와 승객의 편의성 향상을 동시에 충족시키기 위해, 인증 획득이 지연되고 있음에도 불구하고 바이오 소재의 도입을 시도하고 있습니다. 두 지역에서의 규제 측면에서의 주도적 역할은 공급업체가 더 광범위한 시장에 진출할 자격을 유지하기 위해 충족해야 하는 사실상 세계적인 기준을 확립하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 주요 산업 동향

제5장 시장 구도

제6장 시장 규모 및 성장 예측

제7장 경쟁 구도

제8장 시장 기회 및 향후 전망

제9장 민간 항공기 객실 인테리어 부문 CEO에 이용한 중요 전략적 과제

KTH 26.07.08According to Mordor Intelligence, the commercial aircraft cabin interior market size is expected to grow from USD 18.99 billion in 2025 to USD 20.06 billion in 2026 and is forecast to reach USD 26.42 billion by 2031 at 5.65% CAGR over 2026-2031.

This report is Segmented by Product Type (Seating, Cabin Lighting, and More), Aircraft Type (Narrowbody Aircraft, Widebody Aircraft, and More), Cabin Class (First Class and Business Class, and More), Fit Type (Original Equipment Manufacturer and Aftermarket), Material (Composites, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Commercial Aircraft Cabin Interior Market Trends and Insights

Surge in Premium-Economy Retrofits to Monetize Cabin Real Estate

Airlines are intensifying cabin reconfigurations to include premium-economy sections that deliver yield uplifts without adding aircraft capacity. Delta Air Lines registered 15% higher route yields after rolling out premium-economy and forecasts incremental USD 500 million annual revenue once the installation program concludes in 2026. United Airlines already retrofitted more than 200 aircraft by late 2024, pairing seat-pitch increases with upgraded meal service to attract both leisure up-sellers and cost-conscious corporate travelers. Integrated lavatory and aisle modifications undertaken simultaneously for accessibility compliance improve project economics by bundling downtime. Cabin density optimization limits revenue dilution, and high-utilization narrowbody fleets emerge as first adopters. As leading North American carriers demonstrate profit accretion, operators in Europe and Asia-Pacific are fast-tracking similar retrofit programs.

Mandatory 16-g Seat Certification Driving Seat Replacement Cycles

Federal Aviation Administration (FAA) 16-g dynamic testing thresholds enforce the replacement of legacy seats installed before 2009. American Airlines allocated USD 2.1 billion in 2024 to meet the mandate across narrowbody and regional fleets, compressing compliance timelines to avoid grounding penalties. Regional carriers operating aging CRJ and ERJ platforms are similarly compelled despite thinner capital buffers, creating concentrated ordering sprees that stretch supplier capacity. Manufacturers prioritize certification labs over production lines, extending lead times for non-regulated seat programs. The rule's global reach stems from bilateral airworthiness agreements that allow the FAA to approve the de facto benchmark, pulling emerging-market operators into the same replacement cycle.

Supply-Chain Bottlenecks in Seat and Foam Certifications

Updated flammability protocols require fresh foam formulations to pass FAA testing, which now stretches 12-18 months. RECARO Aircraft Seating cited average delivery slippages of 6-8 months on widebody programs during 2024. Thompson Aero temporarily halted sales of its newest premium-economy seat until alternative foams clear testing pipelines. Airlines operating high-cycle narrowbodies face revenue hits when heavy checks overrun scheduled downtimes due to delayed interiors. These bottlenecks diminish retrofit momentum, shaving 0.8 percentage points off the forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Ultra-Lightweight Composite Panels Reducing Fuel Burn and SAF Costs

- Accessibility Mandates Creating New Spend Categories

- High Up-Front Capital Needs as Airlines Recover Post-COVID

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Seating contributed 29.88% of the commercial aircraft cabin interior market share in 2025 and remained the prime value driver within the market. Airlines paid USD 15,000-25,000 per premium-business-class unit and USD 2,500-4,000 for economy modules, ensuring that seat programs anchor retrofit budgets. IFEC platforms, however, clock the fastest 8.26% CAGR as connectivity transforms from a perk into a revenue line.

New demand concentrates on seats that combine reduced weight, wireless charging, and integrated crew alerts. Economy layouts grow denser yet emphasize slim-line ergonomics to mitigate passenger discomfort. Meanwhile, IFEC providers pivot to satellite-agnostic architectures to ensure bandwidth redundancy. The commercial aircraft cabin interior market continues to link IFEC adoption with higher net-promoter scores, empowering airlines to up-sell lounge-style experiences even on narrowbody routes. Galley redesigns and LED lighting upgrades complement seat and IFEC spending, but their absolute values remain smaller given lower component prices.

Narrowbody jets captured 48.62% of 2025 demand, embedding the highest absolute footprint within the commercial aircraft cabin interior market size. Flight-hour intensity and 70% dominance in the OEM backlog keep this category crucial for seat and monument suppliers. Regional jets register the strongest 6.78% CAGR, fueled by point-to-point connectivity growth in secondary cities.

Widebodies skew toward premium-class innovation: full-height privacy doors, self-serve lounges, and next-gen IFEC are table stakes on long-haul routes. Conversely, widebodies such as the A380 witness modest interior investment as retirements accelerate. The commercial aircraft cabin interior market observes carriers' focus on right-sizing capacity, indirectly redirecting capital from oversized models toward high-utilization single-aisles and new-generation regional jets.

Complete Report Scope:

- By Product Type

- Seating

- Cabin Lighting

- In-flight Entertainment and Connectivity (IFEC)

- Galley and Monument

- Lavatory Systems

- Cabin Windows and Windshields

- Overhead Stowage Bins

- Interior Panels and Floorboards

- Others

- By Aircraft Type

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Jets

- By Cabin Class

- First Class and Business Class

- Premium Economy Class

- Economy Class

- By Fit Type

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By Material

- Composites

- Aluminum Alloys

- Steel and Other Alloys

- Advanced Thermoplastics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Singapore

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Qatar

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific controlled 37.11% of 2025 spending, making it the most influential territory within the commercial aircraft cabin interior market. China alone took delivery of more than 400 new aircraft in 2024 and targets an average of 500 annual arrivals by 2030, generating steady linefit volumes. India's air-traffic surge and aggressive fleet expansion plans add further ballast, while Japan channels investment toward high-end cabin refinements to protect its premium yield share. Southeast Asian low-cost carriers adopt uniform interiors emphasizing rapid turnarounds and high seat counts to keep fares low.

The Middle East and Africa region witnesses the fastest growth at a 7.31% CAGR through 2031. Ethiopian Airlines leads widebody growth, pairing cabin retrofits with route expansion into Asia and North America. In contrast, South African Airways uses its restructuring period to standardize interiors for better fleet interchangeability. Infrastructure gaps, limited MRO capacity, and foreign-exchange constraints pose hurdles, yet favorable demographics and tourism recovery offset these impediments. Commercial aircraft leasing firms play a pivotal role by importing younger aircraft equipped with contemporary interiors, accelerating modernization without large cap-ex. While smaller in fleet count, Middle East airlines exert outsized influence on premium-class design trends. Flag carriers in the Gulf continue to pioneer ultra-long-haul configurations with showers, social zones, and bespoke lighting that inspire emulation elsewhere. South America sees steady, though slower, activity, primarily centered on narrowbody retrofits as airlines rationalize fleets post-pandemic. These geographical cross-currents keep the commercial aircraft cabin interior market diversified and resilient against localized shocks.

North America and Europe exhibit mature replacement dynamics, where the commercial aircraft cabin interior market skews toward retrofit programs. US carriers focus on meeting DOT accessibility timelines and launching connected-cabin ecosystems that unlock ad revenue streams. European operators combine sustainability imperatives with passenger-comfort upgrades, experimenting with bio-sourced materials despite certification drag. Regulatory leadership in both regions establishes de facto global benchmarks that suppliers must satisfy to remain eligible for broader markets.

- Safran SA

- Collins Aerospace (RTX Corporation)

- RECARO Aircraft Seating GmbH & Co. KG (RECARO Holding GmbH)

- Diehl Stiftung & Co. KG

- Panasonic Holdings Corporation

- Astronics Corporation

- JAMCO Corporation

- Thompson Aero Seating Limited (Aviation Industry Corporation of China)

- GKN Aerospace Services Limited (Melrose Industries PLC)

- FACC AG

- STG Aerospace Limited (Heads-Up Technologies, Inc.)

- Luminator Technology Group

- SCHOTT AG

- Expliseat S.A.S.

- Acro Aircraft Seating Ltd.

- Geven S.p.A.

- ZIM Aircraft Seating GmbH

- Hong Kong Aircraft Engineering Company Limited

- Mirus Aircraft Seating Ltd.

- Aviointeriors S.p.A.

- Thales Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 KEY INDUSTRY TRENDS

- 4.1 Air Passenger Traffic

- 4.1.1 North America

- 4.1.2 Europe

- 4.1.3 Asia-Pacific

- 4.1.4 South America

- 4.1.5 Middle East and Africa

- 4.2 New Aircraft Deliveries

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia-Pacific

- 4.2.4 South America

- 4.2.5 Middle East and Africa

- 4.3 GDP per Capita (Value in USD)

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia-Pacific

- 4.3.4 South America

- 4.3.5 Middle East and Africa

- 4.4 Revenue of Aircraft Manufacturers

- 4.5 Aircraft Backlog

- 4.6 Gross Orders

- 4.7 Expenditure of Airlines on Fuel

5 MARKET LANDSCAPE

- 5.1 Market Overview

- 5.2 Market Drivers

- 5.2.1 Surge in premium-economy retrofits to monetize cabin real estate

- 5.2.2 Mandatory 16-g seat certification driving seat replacement cycles

- 5.2.3 Ultra-lightweight composite panels reducing fuel burn and sustainable aviation fuel (SAF) costs

- 5.2.4 Accessibility mandates creating new spend categories

- 5.2.5 Connected-cabin data monetization accelerating IFEC upgrades

- 5.2.6 A350 and B787 fleets reaching 8-year retrofit window

- 5.3 Market Restraints

- 5.3.1 Supply-chain bottlenecks in seat and foam certifications

- 5.3.2 High up-front capital needs as airlines recover post-COVID

- 5.3.3 Certification complexity for novel eco-materials

- 5.3.4 Rising FST compliance costs

- 5.4 Value Chain Analysis

- 5.5 Regulatory Landscape

- 5.6 Technological Outlook

- 5.7 Porter's Five Forces Analysis

- 5.7.1 Threat of New Entrants

- 5.7.2 Bargaining Power of Suppliers

- 5.7.3 Bargaining Power of Buyers

- 5.7.4 Threat of Substitutes

- 5.7.5 Intensity of Competitive Rivalry

6 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 6.1 By Product Type

- 6.1.1 Seating

- 6.1.2 Cabin Lighting

- 6.1.3 In-flight Entertainment and Connectivity (IFEC)

- 6.1.4 Galley and Monument

- 6.1.5 Lavatory Systems

- 6.1.6 Cabin Windows and Windshields

- 6.1.7 Overhead Stowage Bins

- 6.1.8 Interior Panels and Floorboards

- 6.1.9 Others

- 6.2 By Aircraft Type

- 6.2.1 Narrowbody Aircraft

- 6.2.2 Widebody Aircraft

- 6.2.3 Regional Jets

- 6.3 By Cabin Class

- 6.3.1 First Class and Business Class

- 6.3.2 Premium Economy Class

- 6.3.3 Economy Class

- 6.4 By Fit Type

- 6.4.1 Original Equipment Manufacturer (OEM)

- 6.4.2 Aftermarket

- 6.5 By Material

- 6.5.1 Composites

- 6.5.2 Aluminum Alloys

- 6.5.3 Steel and Other Alloys

- 6.5.4 Advanced Thermoplastics

- 6.6 By Geography

- 6.6.1 North America

- 6.6.1.1 United States

- 6.6.1.2 Canada

- 6.6.1.3 Mexico

- 6.6.2 Europe

- 6.6.2.1 United Kingdom

- 6.6.2.2 France

- 6.6.2.3 Germany

- 6.6.2.4 Spain

- 6.6.2.5 Italy

- 6.6.2.6 Russia

- 6.6.2.7 Rest of Europe

- 6.6.3 Asia-Pacific

- 6.6.3.1 China

- 6.6.3.2 India

- 6.6.3.3 Japan

- 6.6.3.4 South Korea

- 6.6.3.5 Indonesia

- 6.6.3.6 Singapore

- 6.6.3.7 Rest of Asia-Pacific

- 6.6.4 South America

- 6.6.4.1 Brazil

- 6.6.4.2 Argentina

- 6.6.4.3 Chile

- 6.6.4.4 Rest of South America

- 6.6.5 Middle East and Africa

- 6.6.5.1 Middle East

- 6.6.5.1.1 United Arab Emirates

- 6.6.5.1.2 Saudi Arabia

- 6.6.5.1.3 Turkey

- 6.6.5.1.4 Qatar

- 6.6.5.1.5 Rest of Middle East

- 6.6.5.2 Africa

- 6.6.5.2.1 South Africa

- 6.6.5.2.2 Nigeria

- 6.6.5.2.3 Kenya

- 6.6.5.2.4 Rest of Africa

- 6.6.5.1 Middle East

- 6.6.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Market Concentration

- 7.2 Strategic Moves

- 7.3 Market Share Analysis

- 7.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 7.4.1 Safran SA

- 7.4.2 Collins Aerospace (RTX Corporation)

- 7.4.3 RECARO Aircraft Seating GmbH & Co. KG (RECARO Holding GmbH)

- 7.4.4 Diehl Stiftung & Co. KG

- 7.4.5 Panasonic Holdings Corporation

- 7.4.6 Astronics Corporation

- 7.4.7 JAMCO Corporation

- 7.4.8 Thompson Aero Seating Limited (Aviation Industry Corporation of China)

- 7.4.9 GKN Aerospace Services Limited (Melrose Industries PLC)

- 7.4.10 FACC AG

- 7.4.11 STG Aerospace Limited (Heads-Up Technologies, Inc.)

- 7.4.12 Luminator Technology Group

- 7.4.13 SCHOTT AG

- 7.4.14 Expliseat S.A.S.

- 7.4.15 Acro Aircraft Seating Ltd.

- 7.4.16 Geven S.p.A.

- 7.4.17 ZIM Aircraft Seating GmbH

- 7.4.18 Hong Kong Aircraft Engineering Company Limited

- 7.4.19 Mirus Aircraft Seating Ltd.

- 7.4.20 Aviointeriors S.p.A.

- 7.4.21 Thales Group

8 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 8.1 White-Space and Unmet-Need Assessment