|

시장보고서

상품코드

2061627

상처 드레싱 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Wound Dressings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

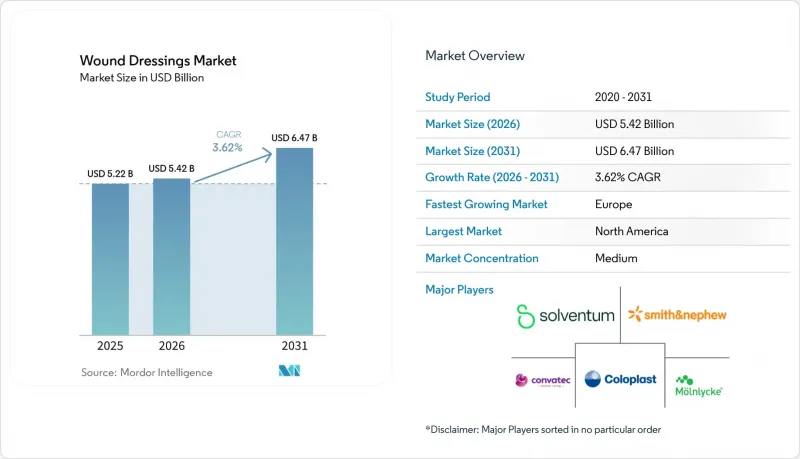

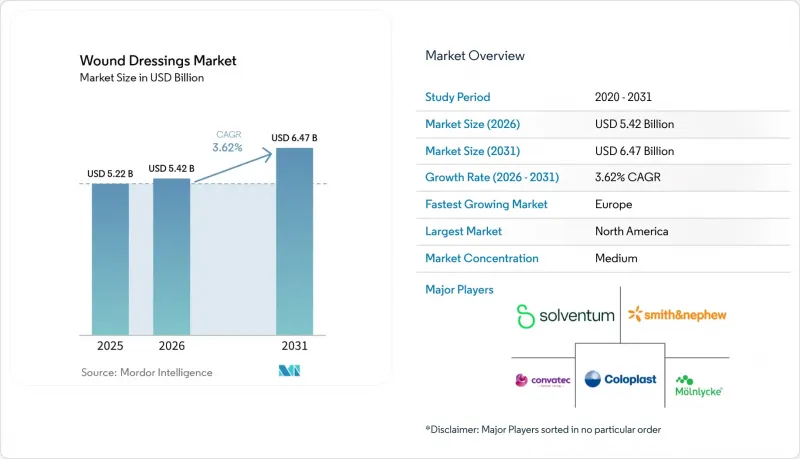

Mordor Intelligence에 의하면, 상처 드레싱 시장 규모는 2025년 52억 2,000만 달러로 평가되었고, 2026년에는 54억 2,000만 달러로 추정되고, 2026-2031년 CAGR 3.62%로 성장을 지속할 전망이며, 2031년에는 64억 7,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(첨단 상처 드레싱(폼, 하이드로콜로이드 등) 및 기존 상처 드레싱(붕대 등)), 용도별(외과적 및 외상성 상처, 당뇨병성 족부 궤양 등), 최종 사용자별(병원 및 외과 센터, 전문 상처 클리닉 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 상처 드레싱 시장 동향 및 분석

만성 상처 및 당뇨병성 궤양의 발생률 증가

세계의 당뇨병 환자 수는 2022년 성인 기준 8억 2,800만 명에 달했으며, 2050년까지 13억 1,000만 명에 이를 것으로 예상되며, 의료 시스템에 부담을 주는 만성 상처가 급증하고 있습니다. 당뇨병 환자의 19%에서 34%가 평생 동안 발 궤양을 앓게 되며, 이 중 최대 24%는 절단 수술을 받게 됩니다. 육아 조직 형성을 촉진하기 위해 보습성 하이드로콜로이드, 항균성 은 폼, 콜라겐 매트릭스 등의 사용이 증가하고 있지만, 자원이 제한된 지역에서는 여전히 비용적인 장벽이 존재합니다. 미국당뇨병학회가 권장하는 다학제적 풋케어 팀은 OECD 국가들에서 점차 정착되고 있지만, 의료 인력 부족과 낮은 건강 리터러시 수준이 다른 지역에서의 도입을 가로막고 있습니다. 그 결과, 당뇨병성 궤양 관리가 상처 드레싱 시장의 주요 성장 동력으로 부상하고 있습니다.

세계의 외과 수술 건수 증가

매년 3억 건 이상의 수술이 이루어지고 있으며, 자원이 부족한 환경에서는 수술 부위 감염이 전체 환자의 최대 11%에서 계속해서 합병증을 유발하고 있습니다. 관절 치환술이나 심장 우회술과 같은 고위험 수술에서는 부종과 세균 오염을 줄이기 위해 예방적 목적으로 일회용 NPWT 시스템에 대한 의존도가 높아지고 있습니다. 스미스 앤 네퓨(Smith & Nephew)의 'PICO'나 솔벤텀(Solventum)의 'Prevena'와 같은 기기들은 2024-2025년 FDA 승인을 획득했으며, 이는 소형 펌프 방식에 대한 규제 당국의 높은 신뢰도를 입증하고 있습니다. 한편, 신흥국에서는 예산 제약으로 인해 깨끗하고 위험이 낮은 상처의 대부분이 여전히 거즈로 관리되고 있어, 상처 드레싱 시장 내의 양극화된 제품 수요가 지속되고 있습니다.

기존 드레싱에 비해 높은 가격 프리미엄

고급 드레싱, 하이드로콜로이드 및 NPWT(음압상처치료) 기기는 일반 거즈보다 5배에서 20배 더 비쌉니다. 이러한 가격 차이로 인해 아시아, 아프리카, 라틴아메리카 전역의 공공 자금을 지원하는 병원에서의 도입이 가로막히고 있습니다. WHO의 필수 의약품 목록은 여전히 거즈와 붕대를 권장하고 있으며, 저비용 조달을 우선시하는 경향을 더욱 강화하고 있습니다. 상처 관리 제품과 외과용 소모품을 세트로 묶어 구매하는 일괄 구매 계약은 예산을 기존 드레싱 제품으로 더욱 유도하고 있으며, 이미 상처 드레싱 시장 전체의 성장세를 웃도는 성장률을 뒷받침하고 있습니다.

부문별 분석

2025년, 상처 드레싱 시장 매출의 65.55%를 첨단 드레싱 재료가 차지했으며, 그 중심에는 만성 상처 클리닉에서 널리 사용되는 폼, 하이드로콜로이드 및 은을 주성분으로 하는 제품군이 있었습니다. 폼과 하이드로콜로이드는 뛰어난 다용도성이 강점으로, 욕창부터 수술 후 절개 부위에 이르기까지 모든 상황에 대응합니다. 항균형 드레싱은 은 요오드 또는 PHMB를 활용하고 있지만, 관리 방침이 강화됨에 따라 성장이 둔화될 가능성이 있습니다. 스마트 센서가 탑재된 드레싱은 FDA의 소프트웨어 검증 결과를 기다리고 있어 현재 시범 단계에 머물러 있습니다. 한편, 알긴산염, 콜라겐, 고흡수성 소재는 삼출액이 많은 상처나 재생 중인 조직에 대응하는 틈새 시장을 차지하고 있습니다.

기존 드레싱은 시장 점유율은 낮지만, 2031년까지 연평균 성장률(CAGR) 5.25%로 성장할 전망이며, 이는 상처 드레싱 시장 전체의 평균을 크게 상회하는 수치입니다. 이는 인도, 나이지리아, 인도네시아 각국 정부가 1차 의료 및 비상 시 비축용으로 거즈의 대량 조달을 확대하고 있기 때문입니다. 또한, 재난 구호 프로토콜에서도 확장성과 보관 안정성 때문에 거즈가 선호되고 있습니다. 가격 격차의 확대로 인해 양극화된 시장 구조가 유지되고 있습니다. 고소득 국가에서는 첨단 혁신 기술이 임상 성과를 향상시키고 있는 반면, 비용 상한선이 설정된 지역에서는 여전히 기초적인 제품이 주류를 이루고 있습니다.

지역별 분석

북미는 메디케어의 적용 범위, 높은 1인당 지출, 그리고 성숙한 전문 상처 치료 네트워크에 힘입어 2025년에도 45.13%의 점유율을 유지하며 선도적인 위치를 지켰습니다. 미국 내 3,700만 명 이상의 성인이 당뇨병을 앓고 있을 뿐만 아니라, 2023년에는 65세 이상 인구가 전체 인구의 17.3%를 차지할 것으로 예상에 따라, 만성 상처 사례 수는 여전히 많은 수준을 유지하고 있습니다. 해당 지역 시장 성장은 공급업체들에게 더 낮은 비용으로 동등한 치료 효과를 입증하도록 요구하는 가치 기반 구매 모델에 의해 제약을 받고 있습니다.

유럽은 독일 내 500곳 이상의 전문 상처 치료 센터가 존재한다는 점, 'Greener NHS' 프레임워크에 기반한 탄소중립 조달 의무, 그리고 프랑스 및 북유럽 국가들의 광범위한 재택 간호 보험 급여에 힘입어, 2031년까지 4.51%라는 지역 내 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이 대륙의 65세 이상 인구 비율은 2050년까지 30%에 육박할 것으로 예상되며, 만성 상처 치료에 대한 수요가 확대될 것으로 전망됩니다. 회원국 간의 규제 차이는 제품 포트폴리오 확장을 복잡하게 만들지만, 한편으로는 현지화 전략을 펼칠 여지도 제공합니다.

아시아태평양, 중동 및 아프리카, 남미 지역에서는 중국과 인도의 수술 건수 증가와 세계 최대 규모의 당뇨병 환자층을 배경으로, 가장 급격한 시장 규모 성장이 예상됩니다. 조달 시장에서는 여전히 기존 드레싱이 주류를 이루고 있지만, 주요 도시의 병원에서는 NPWT(음압상처치료)나 하이드로콜로이드 제제의 시범 도입이 진행되고 있으며, 구매력 향상에 따라 보급 기반이 점차 마련되고 있습니다. 다양한 승인 절차와 가격 기준을 성공적으로 극복하는 기업은 상처 드레싱 시장에서 시장 점유율을 더욱 확대할 기회를 얻을 수 있을 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the wound dressings market size is expected to grow from USD 5.22 billion in 2025 to USD 5.42 billion in 2026 and is forecast to reach USD 6.47 billion by 2031 at 3.62% CAGR over 2026-2031.

This report is Segmented by Type (Advanced Wound Dressings [Foams, Hydrocolloids, and More] and Traditional Wound Dressings [Bandages, and More]), Application (Surgical and Traumatic Wounds, Diabetic Foot Ulcers and More), End User (Hospitals and Surgical Centers, Specialty Wound Clinics, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Wound Dressings Market Trends and Insights

Rising Incidence of Chronic Wounds & Diabetic Ulcers

Global diabetes prevalence hit 828 million adults in 2022 and is projected to reach 1.31 billion by 2050, triggering an upsurge in chronic wounds that strain health-system capacity. Between 19% and 34% of people with diabetes develop foot ulcers over their lifetime, and up to 24% of those cases progress to amputation. Moisture-retentive hydrocolloids, antibacterial silver foams, and collagen matrices are increasingly adopted to accelerate granulation, but cost barriers persist in resource-limited regions. Multidisciplinary foot-care teams recommended by the American Diabetes Association have gained traction in OECD countries, yet clinician shortages and low health literacy impede replication elsewhere. As a result, diabetic ulcer management is emerging as the primary growth engine of the wound dressings market.

Escalating Volume of Surgical Procedures Worldwide

More than 300 million surgeries are performed each year, and surgical site infections continue to complicate up to 11% of cases in low-resource settings. High-risk procedures such as joint replacements and cardiac bypass increasingly rely on prophylactic single-use NPWT systems that reduce edema and bacterial contamination. Devices like Smith & Nephew's PICO and Solventum's Prevena earned FDA clearances in 2024-2025, underscoring regulatory confidence in miniaturized pump formats. Conversely, the majority of clean, low-risk wounds in emerging economies are still managed with gauze due to budget ceilings, sustaining dual-track product demand within the wound dressings market.

High Price-Premium Over Traditional Dressings

Advanced foams, hydrocolloids, and NPWT devices cost five to twenty times more than basic gauze, a differential that blocks uptake in publicly funded hospitals across Asia, Africa, and Latin America. The WHO Essential Medicines List continues to recommend gauze and bandages, reinforcing low-cost procurement preferences. Bulk purchasing contracts that bundle wound products with surgical supplies further steer budgets toward traditional dressings, fueling a growth rate that already exceeds the overall wound dressings market trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Technological Shift Toward Moist-Active & NPWT-Integrated Dressings

- Expanding Reimbursement for Home-Based Wound Care in OECD Nations

- Limited Clinician & Patient Awareness in Emerging Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Advanced dressings accounted for 65.55% of wound dressings market revenue in 2025, anchored by foam, hydrocolloid, and silver platforms widely used in chronic-wound clinics. Foams and hydrocolloids thrive on versatility, handling everything from pressure ulcers to post-surgical incisions. Antimicrobial formats harness silver, iodine, or PHMB, but tightening stewardship policies could soften growth. Smart sensor-enabled dressings remain in pilot phases pending FDA software validation, while alginate, collagen, and super-absorbent materials occupy niche positions addressing highly exudative or regenerating tissues.

Traditional dressings, despite lower value capture, are growing at 5.25% CAGR through 2031, well above the wound dressings market average, as governments in India, Nigeria, and Indonesia scale mass-procurement of gauze for primary-care and emergency stockpiles. Disaster relief protocols also favor gauze for scalability and shelf stability. The widening price gap sustains a dual-speed landscape: advanced innovations push clinical outcomes in high-income settings, while basic products retain primacy wherever cost ceilings prevail.

Geography Analysis

North America retains leadership with 45.13% share in 2025, propelled by Medicare coverage, high per-capita spending, and mature specialty-wound networks. The prevalence of diabetes, exceeding 37 million adults in the United States, together with 17.3% of the population aged 65+ in 2023, sustains a heavy chronic-wound caseload. Market growth in the region is moderated by value-based purchasing models that pressure suppliers to prove outcome parity at lower cost.

Europe posts the fastest regional CAGR at 4.51% to 2031, supported by 500-plus specialized wound centers in Germany, net-zero procurement mandates under the Greener NHS framework, and extensive home-care reimbursement in France and the Nordics. The continent's 65-plus cohort will reach nearly 30% by 2050, guaranteeing chronic-wound demand expansion. Regulatory heterogeneity across member states complicates portfolio rollouts yet offers scope for localization strategies.

Asia-Pacific, Middle East & Africa, and South America represent the steepest volume growth, led by rising surgical counts and the world's largest diabetes cohorts in China and India. Procurement remains dominated by traditional dressings, but tier-one urban hospitals are piloting NPWT and hydrocolloids, setting an adoption runway as purchasing power improves. Companies able to navigate divergent approval pathways and price thresholds stand to gain an incremental slice of the wound dressings market.

- Advancis Medical

- Argentum Medical

- Axio Biosolutions

- B. Braun

- Baxter

- Cardinal Health

- Coloplast

- Convatec

- DermaRite Industries

- DeRoyal Industries

- Hollister

- Integra LifeSciences

- Johnson & Johnson

- Lohmann & Rauscher

- MediWound

- Medline Industries

- Medtronic

- MiMedx Group

- Molnlycke Health Care

- Organogenesis

- Hartmann Group

- Smiths Group

- Solventum Corporation

- Urgo Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Chronic Wounds & Diabetic Ulcers

- 4.2.2 Escalating Volume of Surgical Procedures Worldwide

- 4.2.3 Technological Shift Toward Moist-active & NPWT-integrated Dressings

- 4.2.4 Expanding Reimbursement for Home-based Wound Care in OECD Nations

- 4.2.5 Hospital Decarbonisation Targets Favouring Bio-derived & Compostable Dressings

- 4.2.6 Smart Dressings Enabling Tele-wound-care Billing & Remote Dosing Algorithms

- 4.3 Market Restraints

- 4.3.1 High Price-premium Over Traditional Dressings

- 4.3.2 Limited Clinician & Patient Awareness in Emerging Economies

- 4.3.3 Regulatory Scrutiny on Cumulative Silver-ion Exposure

- 4.3.4 Volatile Supply of Marine & Crustacean Biopolymers Due to Aquaculture Disease Outbreaks

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Advanced Wound Dressings

- 5.1.1.1 Foams

- 5.1.1.2 Hydrocolloids

- 5.1.1.3 Films

- 5.1.1.4 Alginates

- 5.1.1.5 Hydrogels

- 5.1.1.6 Collagens & ECM

- 5.1.1.7 Antimicrobial / Silver

- 5.1.1.8 Super-absorbent Polymers

- 5.1.1.9 Interactive Smart Dressings

- 5.1.2 Traditional Wound Dressings

- 5.1.2.1 Bandages

- 5.1.2.2 Gauzes

- 5.1.2.3 Sponges & Pads

- 5.1.2.4 Cotton Rolls & Others

- 5.1.1 Advanced Wound Dressings

- 5.2 By Application

- 5.2.1 Surgical & Traumatic Wounds

- 5.2.2 Diabetic Foot Ulcers

- 5.2.3 Pressure Ulcers

- 5.2.4 Venous & Arterial Ulcers

- 5.2.5 Burns

- 5.2.6 Other Chronic / Acute Wounds

- 5.3 By End User

- 5.3.1 Hospitals & Surgical Centers

- 5.3.2 Specialty Wound Clinics

- 5.3.3 Home-Healthcare Settings

- 5.3.4 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.3.1 Advancis Medical

- 6.3.2 Argentum Medical

- 6.3.3 Axio Biosolutions

- 6.3.4 B. Braun Melsungen

- 6.3.5 Baxter International

- 6.3.6 Cardinal Health

- 6.3.7 Coloplast

- 6.3.8 ConvaTec Group

- 6.3.9 DermaRite Industries

- 6.3.10 DeRoyal Industries

- 6.3.11 Hollister Incorporated

- 6.3.12 Integra LifeSciences

- 6.3.13 Johnson & Johnson (Ethicon)

- 6.3.14 Lohmann & Rauscher

- 6.3.15 MediWound

- 6.3.16 Medline Industries

- 6.3.17 Medtronic

- 6.3.18 MiMedx Group

- 6.3.19 Molnlycke Health Care

- 6.3.20 Organogenesis

- 6.3.21 Paul Hartmann AG

- 6.3.22 Smith & Nephew

- 6.3.23 Solventum Corporation

- 6.3.24 Urgo Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment