|

시장보고서

상품코드

2062338

실크 단백질 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Silk Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

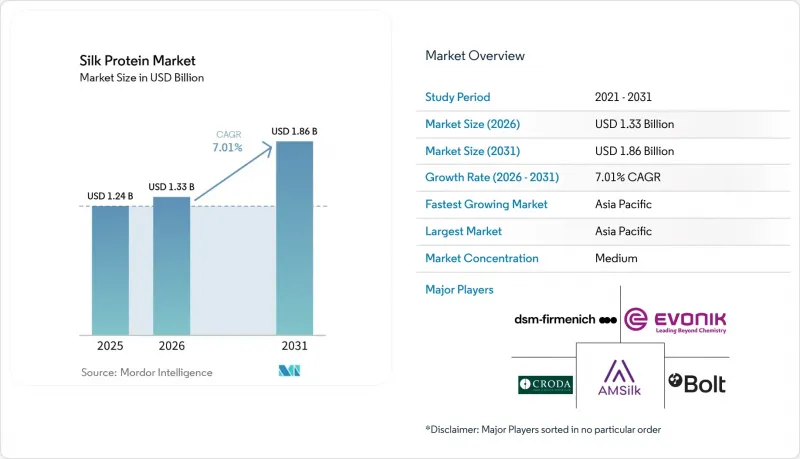

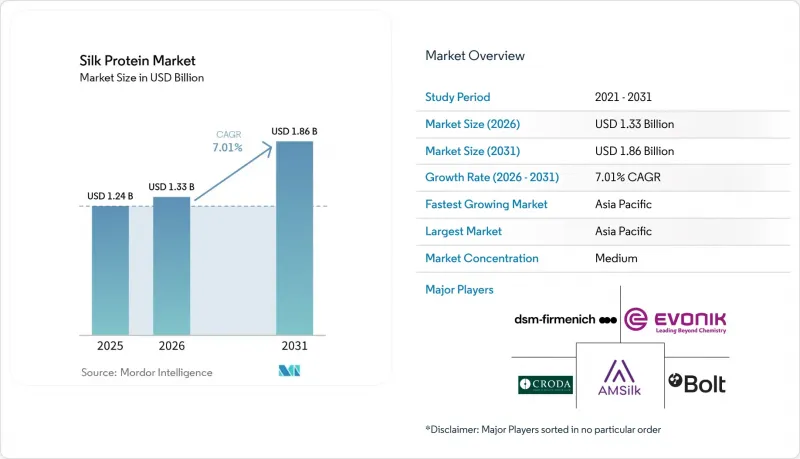

Mordor Intelligence에 의하면, 실크 단백질 시장 규모는 2025년 12억 4,000만 달러에서 2026년에는 13억 3,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 7.01%로 성장을 지속하여, 2031년까지 18억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 단백질의 유형(피브로인, 세리신 등), 형태(분말, 액체, 나노 제제), 용도(퍼스널케어 및 화장품, 바이오메디컬·의약품 등), 최종 사용자 산업(섬유 및 의류 기업 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 실크 단백질 시장 동향 및 분석

화장품 분야에서 천연 및 기능성 성분에 대한 수요 증가

클린 뷰티 브랜드들이 더 짧은 시험 주기로 입증된 효과에 주력함에 따라, 널리 알려진 단백질의 중요성이 커지고 있습니다. 2024년에 출시된 비건 발효 유래 실크는 15분 이내에 눈에 보이는 모공 면적을 7분의 1로 축소시켜 합성 폴리머를 능가하며, 유럽연합(EU)의 효능 표시 입증 규정을 충족했습니다. 기존에 누에고치에서 추출되던 세리신은 주름 방지 필름 형성제로 재도입되고 있습니다. 30밀리리터당 98달러인 이 프리미엄 브랜드는 2026년 전자상거래 데이터에서 40%가 넘는 재구매율을 기록했습니다. 일본과 한국에서 외용 및 내복용 형태 모두 승인됨에 따라, 단일 추출 캠페인을 통해 두 가지 수익원을 모두 확보할 수 있어 가치 극대화가 이루어지고 있습니다. 금지된 미세 플라스틱의 대체재를 찾는 소매업체들은 설비 변경을 최소화하면서 기존 제품 라인에 실크 펩타이드를 도입하고 있으며, 이를 통해 전환 비용을 절감하고 규정 준수 절차를 가속화하고 있습니다. 유효성 데이터와 지속가능성 관련 스토리가 결합되면서, 실크 단백질은 아시아의 틈새 시장 SKU(재고 관리 단위)에서 유럽과 미국의 주류 제품 라인업으로 그 영역을 넓혔습니다.

상처 덮개재 및 약물 전달 분야의 생체의료용도 급증

병원 구매 담당자는 폴리프로필렌 메쉬에서 실크 피브로인 스캐폴드로의 전환을 추진하고 있습니다. 이러한 실크 스캐폴드는 과민 반응이 전혀 없음을 입증했으며, 인공 관절 치환술 1건당 465.91달러의 비용 절감으로 이어집니다. 일본에서 실시된 제3상 임상시험에서는 2주 이내에 90%의 창상 기저면 형성을 달성하여 하이드로콜로이드 제품보다 우수한 성과를 거두었으며, 이는 보험 급여 승인을 뒷받침하는 계기가 되었습니다. 실험실 연구 결과, 은으로 처리된 실크가 대장균의 수를 95% 감소시키는 것으로 나타났으며, 은 이온의 독성 없이 감염 관리 지침을 충족했습니다. 피브로인 필름의 분해 속도는 조절이 가능하기 때문에 항생제나 성장 인자를 상처 부위에 직접 전달할 수 있어 전신 투여의 필요성을 줄여줍니다. 또한, 식용 실크 코팅이 미국 식품의약국(FDA)으로부터 ‘일반적으로 안전하다고 인정되는(GRAS)’ 것으로 인정됨에 따라, 경구 약물 전달 시스템에 관한 임상시험 신청 전(pre-IND) 협의가 시작되었으며, 실크를 기반으로 한 치료제의 가능성이 시사되고 있습니다.

높은 추출 및 정제 비용

탈검 폐수에서 세리신을 정제하려면 투석이나 동결건조와 같은 에너지 집약적인 공정이 필요하며, 이로 인해 비용은 1kg당 15-88달러로 상승하여 상품 가격을 상회하고 있습니다. 소규모 추출 업체들은 인장 강도를 50% 향상시키는 저온 알칼리 처리를 위한 자금 확보에 어려움을 겪고 있습니다. 2025년부터 가동 중인 에보닉의 슬로바키아 자동 생산 라인은 단위당 경제성을 공개하지 않고 있어, 프리미엄 시장에서의 입지를 계속해서 확립해야 함을 시사하고 있습니다. 매년 약 5만 톤의 세리신이 폐기되고 있습니다. 비용 대비 효과가 높은 정제 방법의 기술적 진전이 이루어진다면, 공급량을 대폭 늘리고 가격을 낮출 수 있을 것입니다. 추출법은 아직 리터당 1,112밀리그램(mg/L)이라는 기준치를 초과하지 않는 발효법보다 비용 효율이 높은 상태이지만, 아시아 이외 지역에서의 추출법 확산은 동등한 인건비 우위가 없기 때문에 제약을 받고 있습니다.

부문별 분석

2025년, 피브로인은 실크 단백질 시장의 33.89%를 차지했으며, 주로 섬유용 실과 생체 이식용 스캐폴드로 활용되었습니다. 가수분해 실크 펩타이드 시장은 연평균 성장률(CAGR) 7.78%를 나타낼 것으로 예측되며, 혈청이나 음료에 쉽게 분산되는 수용성 형태라는 장점이 있습니다. 보호 코팅 분야에서 높은 분자 무결성으로 평가받고 있는 순수 실크 단백질은 비용 문제로 인해 생산량이 적습니다. 이전에는 폐기되던 세리신은 DSM-Firmenich와의 라이선스 계약을 통해 현재 안티에이징 필름 분야에서 상업적인 용도로 활용되고 있습니다. 피부의 더 깊은 층까지 침투하는 실크 아미노산은 라인 케어 제품 분야에서 프리미엄 위치를 확고히 하고 있습니다.

재조합 기술은 경계를 재정의하고 있으며, 인실리코에서 분자량을 미리 설정할 수 있게 되었습니다. AMSilk사의 139.9킬로달톤(kDa) 생체 모방형 변이체는 캐시미어와 같은 부드러움을 제공하는 반면, Spiber사의 라이브러리는 사출 성형이 가능한 수지에 대응합니다. 펩타이드의 활용은 하루 7.5g 섭취 시 자연살해(NK) 세포의 활성이 증가했다는 것을 보여준 한국의 임상시험을 계기로 더욱 주목받고 있습니다. 따라서 단백질 유형을 선택할 때는 추출 방법보다 기능적 성능이 점점 더 중요한 요소가 될 것입니다.

2025년에는 분말이 전체의 58.02%를 차지하며 주류가 되었습니다. 이는 중국과 인도에 확립된 분무 건조 인프라를 입증하는 것입니다. 분말은 수년까지 보관 기간과 운반의 용이성을 자랑하지만, 미세 입자에 비해 생체 이용률 면에서는 뒤떨어집니다. 연평균 성장률(CAGR) 8.02%를 나타낼 것으로 예측되는 나노 제제는 정밀한 일렉트로스피닝 기술의 혜택을 받고 있으며, 100나노미터(nm) 미만의 섬유를 생성하여 상처 치유를 촉진합니다. 반면, 일괄 처리의 편리함 덕분에 자체 브랜드나 OEM 채널에서 선호되는 액상 제품은 방부제 사용으로 인해 ‘천연 유래’ 표기에 제약을 받습니다.

일렉트로스피닝의 처리 능력은 시간당 수 Kg을 넘기는 경우가 드물어 나노폼공급을 제한하고 있지만, 그 뛰어난 성능 덕분에 특정 부위의 접착을 필요로 하는 생체의학 기업들의 관심을 끌고 있습니다. 분말은 여전히 벌크 텍스타일 시장의 주력 제품으로 자리매김하고 있는 반면, 나노폼은 신흥 의료 분야와 고급 화장품 시장에서 주도적인 위치를 차지할 것으로 예상되어, 공급망의 양극화를 시사하고 있습니다.

지역별 분석

2025년 현재, 아시아태평양은 시장 점유율의 41.03%를 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 8.32%로 성장할 것으로 전망됩니다. 이러한 성장은 주로 세계 생사 시장의 53%를 차지하는 중국과 연방 정부의 자금 지원을 받은 인도의 현대화 계획에 의해 주도되고 있습니다. 태국, 일본, 한국 등의 국가들은 발효 공장을 건설하고 있으며, 바이오의약품 및 화장품 산업을 위한 지역 공급망을 강화하고 있습니다. 북미에서는 수입 의존에서 국내 생산으로의 전환이 두드러지게 나타나고 있으며, 주 정부의 인센티브 지원에 힘입어 캐논 버지니아사의 새로운 생산 라인이 2026년에 가동을 시작할 예정입니다. 유럽에서는 규제 체계가 중요한 역할을 하고 있습니다. 예를 들어, 슬로바키아에 위치한 에보닉의 시설에서는 매달 수 톤의 방적용 분말을 생산하여 현지 프리미엄 섬유 시장 수요를 충족시키고 있습니다.

북미 시장 점유율은 아직 작지만, 각 브랜드가 국내산이며 동물성 원료가 아닌 원료를 우선적으로 사용함에 따라 점차 확대되고 있습니다. 캐논 버지니아사의 새로운 생산 라인은 이 업계 전반에 걸친 관심을 여실히 보여주고 있습니다. 또한, 캘리포니아주 대학에서 창업한 벤처 기업은 리터당 900밀리그램(mg L?¹)에 가까운 발효 수율을 달성했습니다. 지방 고용 창출을 목적으로 하는 미국의 주 정부 보조금 덕분에, 실크 바이오기술은 경제 발전의 주요 원동력으로 자리매김하고 있습니다. 캐나다 온타리오주의 시범 공장은 옥수수 유래 원료와 친환경 수력발전을 결합하여 탄소 중립적인 비단 원료를 생산하고 있습니다.

유럽에서는 엄격한 환경 규제와 산업 역량 간의 균형을 맞추고 있습니다. 유럽연합(EU)의 미세 플라스틱 금지 조치로 인해 생분해성 필름 형성제에 대한 수요가 증가하고 있으며, 에보닉의 슬로바키아 공장은 장기 위탁 생산 계약을 통해 지역 화장품 제조업체에 제품을 공급함으로써 이러한 수요에 대응하고 있습니다. 100입방미터(m³) 규모의 반응조를 갖춘 프랑스의 아지노모토 발효 허브는 아시아의 전문 지식을 유럽 시장에 접목하고 있습니다. 또한, 동유럽 각국 정부는 추가 투자를 유치하기 위해 바이오테크놀러지 파크에 세제 혜택을 제공합니다.

남미와 중동에서는 뽕나무 재배 면적이 제한적이라는 점과 바이오리액터 도입을 위한 자금 부족과 같은 과제에 직면해 있습니다. 그러나 아시아태평양은 누에고치 양잠과 산업적 발효를 결합함으로써 다른 지역보다 더 높은 수준의 지속적인 성장이 예상됩니다. 다만, 보호주의적인 조달 규제로 인해 유럽 및 미국 시장에서는 생산 과잉이 발생할 가능성이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the silk protein market size is expected to grow from USD 1.24 billion in 2025 to USD 1.33 billion in 2026 and is forecast to reach USD 1.86 billion by 2031 at 7.01% CAGR over 2026-2031.

This report is Segmented by Protein Type (Fibroin, Sericin, and More), Form (Powder, Liquid, Nano-Formulation), Application (Personal Care and Cosmetics, Biomedical and Pharmaceutical, and More), End-User Industry (Textile & Apparel Companies and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Silk Protein Market Trends and Insights

Growing Demand for Natural and Functional Ingredients in Cosmetics

Recognizable proteins are gaining importance as clean-beauty labels focus on proven performance in shorter testing cycles. A vegan fermentation-derived silk, launched in 2024, achieved a sevenfold reduction in visible pore area within fifteen minutes, surpassing synthetic polymers and meeting European Union (EU) claims substantiation rules. Legacy sericin, traditionally sourced from cocoons, is being reintroduced as an anti-wrinkle film former. Premium brands, priced at USD 98 per 30 milliliters, reported a replenishment rate exceeding 40% in 2026 e-commerce data. The dual approval of both topical and ingestible formats in Japan and South Korea enhances value capture, as a single extraction campaign services two profit centers. Retailers replacing banned microplastics are integrating silk peptides into existing formulation lines with minimal equipment changes, reducing conversion costs and accelerating compliance. The combination of efficacy data and sustainability narratives has expanded silk proteins from niche Asian stock-keeping units (SKUs) to mainstream Western assortments.

Surging Biomedical Use in Wound Dressings and Drug Delivery

Hospital buyers are transitioning from polypropylene meshes to silk fibroin scaffolds. These silk scaffolds demonstrate zero hypersensitivity reactions and result in savings of USD 465.91 per arthroplasty case. A Phase III trial in Japan achieved 90% wound-bed preparation within two weeks, outperforming hydrocolloids and supporting reimbursement approval. Laboratory studies showed that silver-treated silk reduced Escherichia coli counts by 95%, meeting infection-control protocols without silver-ion toxicity. The tunable degradation profiles of fibroin films enable direct delivery of antibiotics or growth factors to wounds, reducing the need for systemic dosing. Additionally, the U.S. Food and Drug Administration's (FDA) "Generally Recognized as Safe" status for edible silk coatings has initiated pre-Investigational New Drug (pre-IND) discussions for oral drug carriers, indicating potential for silk-based therapeutics.

High Extraction and Purification Costs

Purifying sericin from degumming wastewater involves energy-intensive processes such as dialysis and freeze-drying, which increase costs to USD 15-88 per kilogram, exceeding commodity pricing. Small-scale extractors face challenges in securing capital for low-temperature alkali treatments that enhance tensile strength by 50%. Evonik's automated production line in Slovakia, operational since 2025, has not disclosed unit economics, indicating the continued need for premium market positioning. Approximately 50,000 tons of sericin are discarded annually. A technological advancement in cost-effective purification methods could significantly increase supply and reduce prices. While extraction remains more cost-efficient than fermentation, which has yet to surpass the 1,112 milligrams per liter (mg/L) benchmark, scaling extraction outside Asia is constrained by the lack of comparable labor cost advantages.

Other drivers and restraints analyzed in the detailed report include:

- Rising Interest in Sustainable and Biodegradable Textiles

- Regulatory Push for Microplastic Alternatives in Personal Care

- Variability in Raw-Silk Quality and Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, fibroin captured 33.89% of the silk protein market, primarily in textile yarns and implantable scaffolds. Hydrolyzed silk peptide, projected to grow at a 7.78% compound annual growth rate (CAGR), benefits from its soluble formats that easily disperse in serums and beverages. Whole silk protein, valued for its high molecular integrity in protective coatings, sees modest volumes due to its cost. Sericin, previously discarded, now finds commercial use in anti-aging films, supported by licensing from DSM-Firmenich. Silk amino acids, penetrating deeper skin layers, secure a premium position in lineage-care products.

Recombinant technologies are redefining boundaries, allowing preset molecular weights in silico. AMSilk's 139.9-kilodalton (kDa) biomimetic variant offers cashmere-like softness, while Spiber's library caters to injection-moldable resins. Peptide adoption gains traction from a Korean trial, highlighting elevated natural killer (NK)-cell activity at a daily dose of 7.5 grams. Thus, the choice of protein type will increasingly hinge on functional performance over extraction methods.

In 2025, powders dominated with 58.02% of the volume, a testament to the established spray-dry infrastructure in China and India. While powders boast a multi-year shelf life and easy freight, they fall short on bioavailability compared to finer particles. Nano-formulations, projected to grow at an 8.02% CAGR, benefit from precision electrospinning, producing fibers below 100 nanometers (nm) that expedite wound closure. Liquids, favored in private-label original equipment manufacturer (OEM) channels for their batching simplicity, face limitations in natural-label claims due to preservatives.

Despite electrospinning throughput rarely exceeding kilograms per hour, capping nano-form supply, the performance premium draws biomedical firms seeking targeted adhesion. While powders will remain a staple for bulk textiles, nano-forms are poised to dominate emerging medical and high-end cosmetic niches, indicating a bifurcated supply chain.

Geography Analysis

In 2025, Asia-Pacific accounted for a 41.03% market share and is projected to grow at an 8.32% compound annual growth rate (CAGR) through 2031. This growth is primarily driven by China, which represents 53% of the global raw silk market, and by India's modernization initiatives supported by federal funding. Countries such as Thailand, Japan, and South Korea are establishing fermentation plants, strengthening the region's supply chain for the biomedical and cosmetic industries. In North America, the transition from import reliance to domestic production is evident, with Canon Virginia's new production line set to launch in 2026, supported by state incentives. In Europe, regulatory frameworks play a significant role; for example, Evonik's facility in Slovakia produces several tons of spinning-grade powder monthly, meeting the demand of the local premium textile market.

North America's market share, though smaller, is increasing as brands prioritize onshore, animal-free supplies. Canon Virginia's new production line highlights this cross-sector interest. Additionally, academic spin-outs in California are achieving fermentation yields nearing 900 milligrams per liter (mg L-1). U.S. state subsidies aimed at rural job creation are positioning silk biotechnology as a key economic development driver. In Canada, pilot plants in Ontario are combining corn-based feedstocks with green hydroelectricity to produce zero-carbon silk inputs.

Europe is balancing stringent environmental regulations with its industrial capabilities. The European Union's (EU) microplastic ban is driving demand for biodegradable film-formers, and Evonik's Slovak facility is addressing this need by supplying regional cosmetics manufacturers through long-term tolling agreements. France's Ajinomoto fermentation hub, equipped with 100 cubic meter (m3) reactors, integrates Asian expertise into the European market. Additionally, Eastern European governments are offering tax holidays for biotech parks to attract further investments.

South America and the Middle East face challenges such as limited mulberry cultivation and insufficient capital for bioreactors. However, Asia-Pacific's combination of cocoon farming and industrial fermentation positions it for sustained growth, surpassing other regions. Protectionist sourcing regulations, however, may lead to redundant capacity in Western markets.

- AMSilk GmbH

- Bolt Threads Inc.

- Croda International Plc

- dsm-firmenich

- Evolved By Nature Inc.

- Evonik Industries AG

- Givaudan

- Huzhou Aotesi Biochemical

- JRS Pharma

- LANXESS

- Lonza

- MATEXCEL

- PlanAdv S.r.l.s.

- SEIWA KASEI Co., Ltd.

- Spiber Inc.

- Suzhou Suhao BioTech

- Wuxi Boton Technology

- Zhejiang Jiaxin Silk Corp., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for natural and functional ingredients in cosmetics

- 4.2.2 Surging biomedical use (wound dressings, drug delivery)

- 4.2.3 Rising interest in sustainable and biodegradable textiles

- 4.2.4 Regulatory push for micro-plastic alternatives in personal-care

- 4.2.5 Breakthroughs in recombinant / microbial silk-protein production

- 4.2.6 Expansion of plant-based recombinant silk platforms lowering CAPEX

- 4.3 Market Restraints

- 4.3.1 High extraction and purification costs

- 4.3.2 Variability in raw-silk quality and supply constraints

- 4.3.3 Allergenicity and regulatory uncertainty for ingestible silk peptides

- 4.3.4 Limited scalability of sericulture outside Asia-Pacific

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Protein Type

- 5.1.1 Fibroin

- 5.1.2 Sericin

- 5.1.3 Whole Silk Protein

- 5.1.4 Hydrolyzed Silk Peptide

- 5.1.5 Silk Amino Acids

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Liquid

- 5.2.3 Nano-formulation

- 5.3 By Application

- 5.3.1 Personal Care and Cosmetics

- 5.3.2 Biomedical and Pharmaceutical

- 5.3.3 Textiles and Fabrics

- 5.3.4 Food and Dietary Supplements

- 5.3.5 Coatings and Adhesives

- 5.4 By End-user Industry

- 5.4.1 Cosmetics & Personal-Care Manufacturers

- 5.4.2 Healthcare & Medical-Device Companies

- 5.4.3 Textile & Apparel Companies

- 5.4.4 Food & Nutrition Companies

- 5.4.5 Other Industrial Users (Packaging, Coatings)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AMSilk GmbH

- 6.4.2 Bolt Threads Inc.

- 6.4.3 Croda International Plc

- 6.4.4 dsm-firmenich

- 6.4.5 Evolved By Nature Inc.

- 6.4.6 Evonik Industries AG

- 6.4.7 Givaudan

- 6.4.8 Huzhou Aotesi Biochemical

- 6.4.9 JRS Pharma

- 6.4.10 LANXESS

- 6.4.11 Lonza

- 6.4.12 MATEXCEL

- 6.4.13 PlanAdv S.r.l.s.

- 6.4.14 SEIWA KASEI Co., Ltd.

- 6.4.15 Spiber Inc.

- 6.4.16 Suzhou Suhao BioTech

- 6.4.17 Wuxi Boton Technology

- 6.4.18 Zhejiang Jiaxin Silk Corp., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment