|

시장보고서

상품코드

2061633

그람 양성 감염증 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Gram-positive Bacterial Infections - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

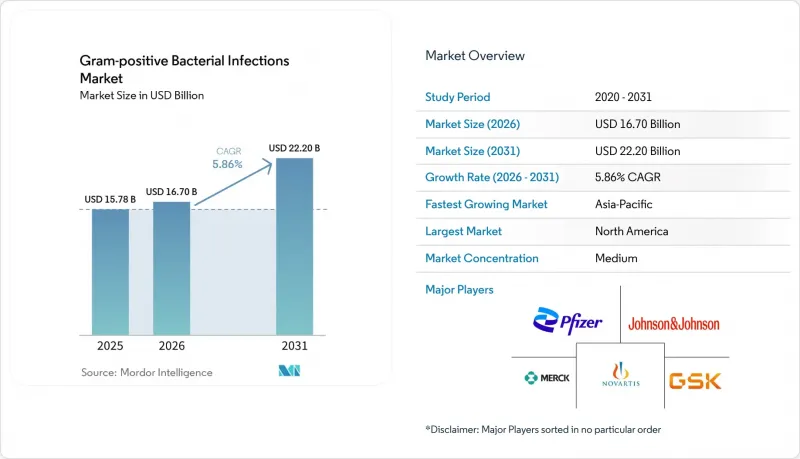

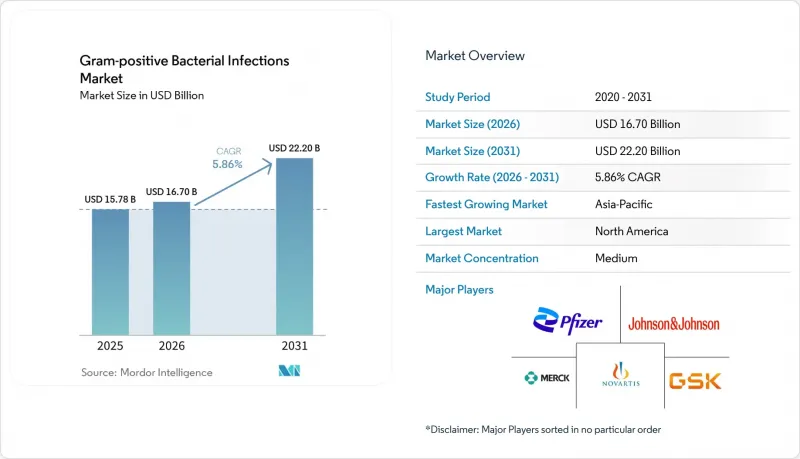

Mordor Intelligence에 의하면, 그람 양성 감염증 시장 규모는 2025년 157억 8,000만 달러로 평가되었고, 2026년에는 167억 달러로 추정되고, 2026-2031년 CAGR 5.86%로 성장을 지속할 전망이며, 2031년까지 222억 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 카테고리별(치료제, 진단제 등), 병원체별(황색포도상구균 등), 질환 적응증별(폐렴, 패혈증 및 혈류 감염, 피부 및 연부조직 감염, 인두염 등), 최종 사용자별(병원, 검사 기관 등), 지역별(북미, 남미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 그람양성균 감염증 시장 동향 및 인사이트

그람 양성 감염증의 유병률 증가

2024년, EU/EEA 국가에서 침습성 황색포도상구균(S. aureus) 혈류 감염의 발생률은 인구 10만 명당 37.9건에 달했으며, 대장균(E. coli) 균혈증에 이어 두 번째로 높은 수치를 기록했습니다. 팬데믹 기간 중 수술 지연으로 인해 인공관절 치환술이 증가함에 따라, 이러한 의료기기의 수명 기간 동안 지연성 포도상구균 감염의 위험이 높아지고 있습니다. 2020-2024년 호흡기 병원체의 유행이 확대됨에 따라, 침습성 폐렴구균 감염증의 발생률은 2배로 증가했습니다. 클로스트리디오이데스 디피실(Clostridioides difficile)은 여전히 의료 관련 설사의 주요 원인이며, 미국에서는 매년 22만 3,900명의 입원과 1만 2,800명의 사망을 초래하고 있습니다. 게다가, 반코마이신 치료 후 재발률은 여전히 30%에 달하고 있습니다.

승인된 의약품 및 후기 개발 파이프라인 증가

2025년 항균제 파이프라인에는 90개의 임상 단계 후보 약물이 포함되어 있으며, 그중 절반은 그람양성균을 표적으로 하고 있습니다. 인간 단일클론 항체인 토스타톡시마브는 중증 황색포도상구균 폐렴을 대상으로 한 3상 임상시험을 성공적으로 완료했으며, 고령 환자에게서 유의미한 유효성을 보였기 때문에 이 환자군에 초점을 맞춘 확인 임상시험이 실시될 예정입니다. 항바이오필름 항체 TRL1068은 인공관절 감염을 대상으로 한 1상 임상시험에서 유망한 결과를 보였으며, 활막으로의 침투와 세균 부하 감소를 달성함으로써 기존과는 다른 치료 접근법의 유효성이 입증되었습니다.

그람 양성 병원체에서 항생제 내성의 확산

리네졸리드 내성은 현재 23S rRNA의 변이 및 cfr 유전자의 획득을 통해 여러 지역에서 확인되고 있으며, 이로 인해 치료 기간이 단축되고 치료 성공률이 낮아지고 있습니다. 캄보디아의 감시 조사 결과, 2023년에 광범위 내성 임질균(XDR-Neisseria gonorrhoeae) 분리주가 12.5%를 기록했으며, 항생제 사용량이 적은 환경에서도 내성 형질이 급속히 확산되고 있는 실태가 드러났습니다. 전 세계 항생제 소비량은 2016-2023년 16.3% 증가했으며, 이대로 방치할 경우 2030년까지 52.3% 증가할 것으로 예측되어 선택압이 가속화되고 있습니다. 이러한 경향은 현재 개발 중인 약물에 위협이 되고 있으며, 예방, 진단 및 새로운 작용기전에 대한 병행 투자가 요구되고 있습니다.

부문별 분석

2025년 시점에서 진단 분야의 수익 기반은 비교적 소규모였으나, 2031년까지 연평균 성장률(CAGR) 6.79%를 나타낼 것으로 예측되며, 이는 제품 카테고리 중 가장 빠른 성장세를 보일 것입니다. 당일 내 병원체 검출을 권장하는 항생제 적정 사용 의무화로 인해, 다중 PCR 패널 및 신속한 표현형 검사 시스템에 대한 병원 수요가 증가하고 있습니다. 글리코펩타이드계 항생제는 치료제 매출의 18%를 차지했으나, 임상 지침에 따라 치료제 모니터링이 필요한, 더 단기간에 고용량을 투여하는 요법이 채택됨에 따라 이익률에 대한 압박이 커지고 있습니다.

신속 검사는 경구용 약물로 단계적으로 전환하는(스텝다운) 요법의 보급을 뒷받침하고 있으며, 옥사졸리디논 계열 약물 수요를 끌어올리고 있습니다. 다중 검사 시스템을 통해 배양 검사에 수반되는 업무 부담이 줄어들어 병원의 업무 효율이 향상되는 한편, 보험사는 치료의 조기 단계 전환을 입원 기간 단축의 수단으로 보고 있습니다. 이러한 운영 비용 절감이 분자 검사의 높은 초기 비용을 상쇄하기 시작하면서, 진단법의 보급 곡선을 더욱 확대시키고, 그람 양성 감염증 시장을 성장시키고 있습니다.

메티실린 내성 균주를 포함한 황색포도상구균 감염증은 2025년 병원체 관련 매출의 28.5%를 차지했으며, 이는 수술 부위 감염 및 삽입형 의료기기 관련 감염에서 이 균주가 차지하는 핵심적인 역할을 반영하고 있습니다. EU 전체에서 MRSA 혈류 감염 발생률이 20.4% 감소했음에도 불구하고, 병원 네트워크에서는 여전히 고위험군 환자에게 항-MRSA 세팔로스포린계 항생제나 리포글리코펩타이드계 항생제를 우선적으로 사용하고 있습니다.

클로스트리디오이데스 디피실(Clostridioides difficile)은 2031년까지 연평균 성장률(CAGR) 6.96%를 나타낼 것으로 예측되며, 이는 병원체 중 가장 빠른 성장 궤도입니다. 이는 장내 미생물 군집을 보존하고 재발을 대폭 억제하는 CRS3123이나 이베자폴스타트 등의 약물에 힘입은 결과입니다. 규제 당국은 지속적인 치유를 중시하는 복합 평가 지표를 수용할 의향을 시사하고 있으며, 이러한 추세는 3상 임상시험 데이터가 공개되는 대로 승인까지의 기간을 단축하고 시장 내 보급을 확고히 할 가능성이 높다고 여겨집니다.

지역별 분석

북미는 2025년 매출의 41.25%를 차지했으며, 미국 내 6,200개 병원 검사실과 신속 분자진단 시스템에 대한 지속적인 설비 투자 예산이 이를 뒷받침하고 있습니다. 도시 지역의 시설에서는 Accelerate Pheno나 BioFire FilmArray와 같은 플랫폼이 선호되고 있습니다. 그러나 지방의 의료기관에서는 여전히 수동 배양 워크플로우에 의존하고 있어, 결과가 나오기까지 96시간 이상 걸리는 경우도 있어, 설치 공간이 적게 필요한 채혈 직후 검사 솔루션에 여전히 기회가 남아 있습니다. 연방 정부의 의약품 적정 사용 목표에 따르면, 현재 환급 보너스를 적절한 시기에 의약품 단계적 증량 조치를 해제하는 지표와 연계하고 있으며, 이를 통해 신속 진단이 더욱 정착되고 있습니다.

유럽에서는 2019-2024년 MRSA 혈류 감염의 발생률이 20.4% 감소했으나, 8개국에서는 반코마이신 내성 엔테로코커스 페시움의 유병률이 50% 이상의 것으로 보고되었습니다. 독일의 2025년 기술 평가에서 AST(항생제 감수성 검사) 소요 시간을 최소 12시간 단축하는 시스템에 대한 보험 급여가 승인되었습니다. QuickMIC의 검증은 이 기준을 충족했으며, 이는 조달 컨소시엄이 수량 연동형 계약 협상을 시작하는 계기가 되었습니다. 폐렴구균에서 페니실린과 마크로라이드에 대한 복합 내성 비율이 11.1%에 달함에 따라, 지침 제정 위원회는 현재 지역사회 획득성 폐렴에 대해 고용량의 β-락탐계 항생제 또는 플루오로퀴놀론계 항생제 중 하나를 포함하는 경험적 치료 요법을 권장하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 8.25%를 나타낼 것으로 예측되며, 이는 지역별 성장률 중 가장 높은 수치입니다. 중국에서는 2020-2025년 의료비가 연평균 8.2% 증가했으며, 이에 따라 자동 혈액 배양 및 MALDI-TOF 동정을 위한 조달 예산이 확대되고 있습니다. 인도의 ‘아유슈만 바라트’ 계획이 확대됨에 따라, 지방 병원들은 증후군에 기반한 관리에서 배양 검사에 기반한 치료로 전환할 수 있게 되었습니다. 중국, 인도, 브라질에서 EUCAST 기준치와의 조화를 통해 글리코펩타이드계 및 옥사졸리디논계 약제의 감수성 판정이 엄격해짐에 따라, 감수성으로 위장된 치료 실패 사례가 감소하고 있습니다. 남미는 2025년 전 세계 매출의 6%를 차지했으며, 브라질에서 이 기준치가 채택됨에 따라 병원들은 이미 난치성 VRE 및 MRSA 감염증에 대한 예비 약물을 사용하게 되었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the gram-positive bacterial infections market size is expected to grow from USD 15.78 billion in 2025 to USD 16.70 billion in 2026 and is forecast to reach USD 22.20 billion by 2031 at 5.86% CAGR over 2026-2031.

This report is Segmented by Product Category (Therapeutics, Diagnostics, and More), Pathogen (Staphylococcus Aureus, and More), Disease Indication (Pneumonia, Sepsis/BSI, SSTI, Pharyngitis, and More), End User (Hospitals, Reference Laboratories, and More), and Geography (North America, South America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Gram-positive Bacterial Infections Market Trends and Insights

Rising Prevalence of Gram-Positive Infections

In 2024, invasive S. aureus bloodstream infections reached 37.9 per 100,000 population in EU/EEA countries, ranking second only to E. coli bacteremia. The backlog of surgeries during the pandemic has led to an increase in prosthetic joint implantations, raising the risk of late-onset staphylococcal infections over the lifespan of these devices. Between 2020 and 2024, the incidence of invasive S. pneumoniae disease doubled as respiratory pathogens began circulating more widely. Clostridioides difficile remains the leading cause of healthcare-associated diarrhea, resulting in 223,900 hospitalizations and 12,800 deaths annually in the U.S. Additionally, recurrence rates after vancomycin therapy remain as high as 30%.

Increasing Number of Drug Approvals & Late-Stage Pipelines

The 2025 antibacterial pipeline includes 90 clinical-stage assets, with half targeting gram-positive organisms. Tostatoxumab, a human monoclonal antibody, successfully completed Phase 3 trials for severe S. aureus pneumonia, demonstrating significant benefits for elderly patients and prompting a confirmatory study focused on this demographic. The anti-biofilm antibody TRL1068 showed promising results in Phase 1 trials for prosthetic joint infections, achieving synovial penetration and bacterial load reduction, thereby validating non-traditional treatment approaches.

Escalating Antibiotic Resistance Among Gram-Positive Pathogens

Linezolid resistance now appears in multiple regions via 23S rRNA mutation and cfr gene uptake, curbing therapy length and success. Cambodia's surveillance logged 12.5% extensively drug-resistant Neisseria gonorrhoeae isolates in 2023, underscoring how resistance traits spread quickly even in lower-use settings. Global antibiotic consumption climbed 16.3% between 2016 and 2023, with forecasts of 52.3% growth by 2030 if unchecked, accelerating selection pressure. These patterns threaten current pipelines and require simultaneous investment in prevention, diagnostics, and novel mechanisms.

Other drivers and restraints analyzed in the detailed report include:

- Growing Healthcare Spending in Emerging Economies

- Adoption Of Rapid Molecular Diagnostics Enabling Targeted Therapy

- Patent Expiries Driving Generic Erosion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostics represented the smaller revenue base in 2025, yet they are set to post a 6.79% CAGR through 2031, the swiftest growth among product categories. Stewardship mandates that favor same-day organism detection reinforce hospital demand for multiplex PCR panels and rapid phenotypic systems. Glycopeptides retained an 18% slice of therapeutic revenue, but margin pressure is accelerating as clinical guidance adopts shorter, higher-dose courses requiring therapeutic drug monitoring.

Rapid testing also underpins greater use of oral step-down regimens, boosting oxazolidinone demand. Hospitals gain workflow efficiencies when multiplex systems reduce ancillary culture labor, while payers view faster de-escalation as a lever to trim length of stay. These operational savings are beginning to offset the higher upfront cost of molecular tests, further widening the diagnostics adoption curve and enlarging the gram-positive bacterial infections market.

Staphylococcus aureus infections, including methicillin-resistant strains, delivered 28.5% of 2025 pathogen revenue, reflecting their central role in surgical site and indwelling device infection. Despite a 20.4% decline in MRSA bloodstream incidence across the EU, hospital networks still reserve anti-MRSA cephalosporins and lipoglycopeptides for high-risk cohorts.

Clostridioides difficile is projected to grow at 6.96% CAGR to 2031, the fastest pathogen trajectory, fueled by agents such as CRS3123 and ibezapolstat that spare gut microbiota and sharply cut recurrence. Regulatory agencies are signaling acceptance of composite endpoints that emphasize sustained cure, a development likely to accelerate approval timelines and solidify commercial uptake once Phase 3 data read out.

Geography Analysis

North America delivered 41.25% of 2025 revenue, anchored by 6,200 U.S. hospital laboratories and sustained capital budgets for rapid molecular systems. Urban facilities favor platforms such as Accelerate Pheno and BioFire FilmArray; however, rural centers still rely on manual culture workflows that can exceed 96 hours before result release, leaving opportunity for low-footprint direct-from-blood solutions. Federal stewardship targets now link reimbursement bonuses to timely de-escalation metrics, further entrenching rapid diagnostics.

Europe recorded a 20.4% decline in MRSA bloodstream incidence from 2019 to 2024, yet eight countries documented vancomycin-resistant Enterococcus faecium prevalence above 50%. Germany's 2025 technology assessment endorsed reimbursement for systems that trim AST turnaround by at least 12 hours. QuickMIC validation met this threshold, prompting procurement consortia to negotiate volume-linked contracts. With combined penicillin and macrolide resistance in S. pneumoniae at 11.1%, guideline panels now recommend empiric regimens containing either higher-dose beta-lactams or fluoroquinolones in community-acquired pneumonia.

Asia-Pacific is poised for an 8.25% CAGR through 2031, the highest regional pace. China's 8.2% annual healthcare spending expansion between 2020 and 2025 has lifted procurement budgets for automated blood culture and MALDI-TOF identification. India's Ayushman Bharat scale-up enables district hospitals to transition from syndromic management to culture-based therapy. Harmonization with EUCAST breakpoints across China, India, and Brazil tightens susceptibility interpretation for glycopeptides and oxazolidinones, reducing treatment failure masquerading as susceptibility. South America contributes 6% of global 2025 revenue; Brazil's breakpoint adoption is already steering hospitals toward reserve agents for refractory VRE and MRSA infections.

- Abbott Laboratories

- AstraZeneca

- Basilea Pharmaceutica Ltd.

- Becton Dickinson & Co.

- bioMerieux

- Cepheid (Danaher)

- Cumberland Pharmaceuticals

- Dr Reddy's Laboratories Ltd.

- GlaxoSmithKline

- Hikma Pharmaceuticals

- Johnson & Johnson

- Lupin

- Melinta Therapeutics

- Merck

- Novartis

- Paratek Pharmaceuticals

- Pfizer

- Roche

- Sanofi

- Shionogi & Co., Ltd.

- Sun Pharma Industries Ltd.

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Gram-Positive Infections

- 4.2.2 Increasing Number of Drug Approvals & Late-Stage Pipelines

- 4.2.3 Growing Healthcare Spending in Emerging Economies

- 4.2.4 Adoption of Rapid Molecular Diagnostics Enabling Targeted Therapy

- 4.2.5 Bundled-Payment Rules Boosting Prophylactic Narrow-Spectrum Use

- 4.2.6 Climate-Driven Geographic Expansion of Gram-Positive Pathogens

- 4.3 Market Restraints

- 4.3.1 Escalating Antimicrobial Resistance Among Gram-Positive Bacteria

- 4.3.2 Patent Expiries Driving Generic Erosion

- 4.3.3 Diagnostic Stewardship Curbing Unnecessary Test Ordering

- 4.3.4 VC Pullback for Narrow-Spectrum Antibiotic Start-Ups

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Category

- 5.1.1 Therapeutics

- 5.1.1.1 ?-lactam antibiotics

- 5.1.1.2 Cephalosporins

- 5.1.1.3 Penicillins

- 5.1.1.4 Fluoroquinolones

- 5.1.1.5 Lipopeptides

- 5.1.1.6 Oxazolidinones

- 5.1.1.7 Glycopeptides

- 5.1.1.8 Vaccines & mAbs

- 5.1.2 Diagnostics

- 5.1.2.1 Culture & susceptibility testing

- 5.1.2.2 Rapid molecular (PCR, isothermal)

- 5.1.2.3 Immunoassays

- 5.1.2.4 Point-of-care lateral-flow

- 5.1.3 Adjunctive Prevention Products

- 5.1.1 Therapeutics

- 5.2 By Pathogen

- 5.2.1 Staphylococcus aureus (incl. MRSA)

- 5.2.2 Streptococcus pneumoniae

- 5.2.3 Enterococcus faecalis/faecium (incl. VRE)

- 5.2.4 Clostridioides difficile

- 5.2.5 Listeria monocytogenes

- 5.3 By Disease Indication

- 5.3.1 Pneumonia

- 5.3.2 Sepsis / BSI

- 5.3.3 Skin & Soft-Tissue Infections

- 5.3.4 Pharyngitis (Strep throat)

- 5.3.5 Endocarditis

- 5.3.6 Meningitis

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Reference Laboratories

- 5.4.3 Ambulatory Surgery Centers

- 5.4.4 Retail & Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East & Africa

- 5.5.5.1 GCC

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East & Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Overview, Market Level Overview, Core Segments, Financials as available, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 AstraZeneca plc

- 6.3.3 Basilea Pharmaceutica Ltd.

- 6.3.4 Becton Dickinson & Co.

- 6.3.5 bioMerieux SA

- 6.3.6 Cepheid (Danaher)

- 6.3.7 Cumberland Pharmaceuticals

- 6.3.8 Dr Reddy's Laboratories Ltd.

- 6.3.9 GlaxoSmithKline plc

- 6.3.10 Hikma Pharmaceuticals plc

- 6.3.11 Johnson & Johnson (Janssen)

- 6.3.12 Lupin Ltd.

- 6.3.13 Melinta Therapeutics

- 6.3.14 Merck & Co., Inc.

- 6.3.15 Novartis AG

- 6.3.16 Paratek Pharmaceuticals

- 6.3.17 Pfizer Inc.

- 6.3.18 Hoffmann-La Roche Ltd

- 6.3.19 Sanofi SA

- 6.3.20 Shionogi & Co., Ltd.

- 6.3.21 Sun Pharma Industries Ltd.

- 6.3.22 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment