|

시장보고서

상품코드

2061705

환각제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Psychedelic Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

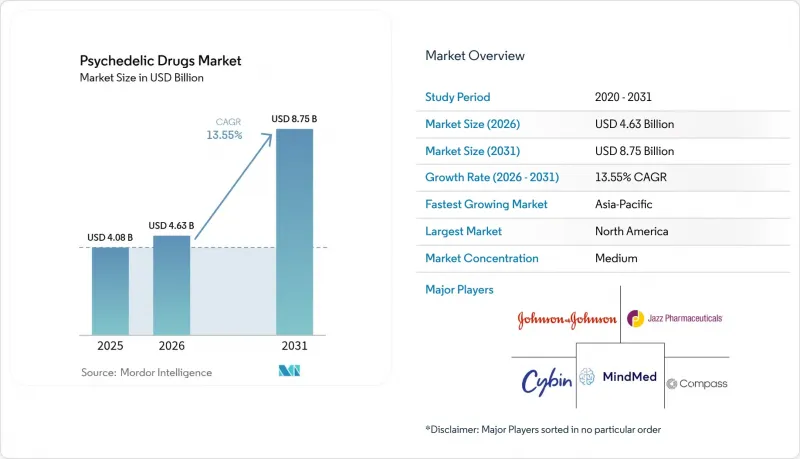

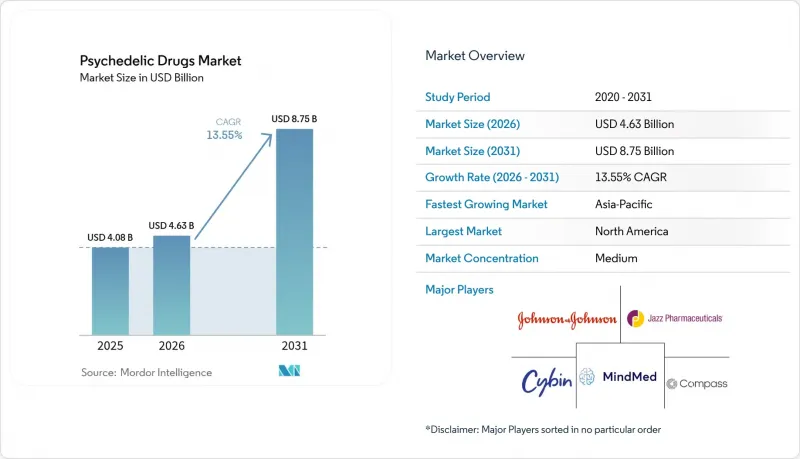

Mordor Intelligence에 의하면, 환각제 시장 규모는 2025년에 40억 8,000만 달러로 평가되었습니다. 2026년 46억 3,000만 달러에서 2031년까지 87억 5,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 13.55%를 나타낼 전망입니다.

본 보고서는 약제의 유형(케타민, 실로시빈 등), 원료(천연 유래 및 합성), 용도(치료 저항성 우울증 등), 투여 경로(경구 등), 유통 채널(병원 약국 등), 최종 용도(병원 등), 지역(북미 등)에 따라 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 환각제 시장 동향 및 인사이트

전 세계 정신질환 유병률 증가와 미충족 의료 수요

치료 저항성 우울증 및 불안 장애의 발생률 증가는 대상 환자층을 확대함으로써 환각제 의약품 시장 규모를 키우고 있습니다. 2회 투여로 실로시빈에 의한 75%의 관해율을 보인 2상 임상시험은 지속적인 반응이 연간 총 치료 시간을 단축할 수 있다는 점에서 임상의들의 관심을 높이고 있습니다. 정신과 의사 부족에 직면한 의료 시스템에서는 효과가 높고 빈도가 낮은 중재가 외래 진료의 병목 현상을 해소할 수 있을 것으로 추정됩니다. 인지도가 높아짐에 따라 환자 지원 단체들은 보험사 측에 장기적인 항우울제 복용 순응도에 의존하는 비용 대비 효과 모델을 재검토할 것을 강력히 요구하고 있습니다.

환각제의 의료적 활용 및 규제 해제를 향한 규제 동향

임상시험 설계 및 획기적 치료제 지정에 관한 FDA의 지침이 더욱 명확해짐에 따라 개발 기간이 단축되었으며, 이는 후기 임상시험 단계에 있는 후원사가 환각제 시장에서 점유율을 확보하는 데 직접적인 영향을 미치고 있습니다. 오리건주와 콜로라도주는 감독 하에 시로시빈을 제공하는 서비스에 대한 면허를 발급하고, 연방 기관이 검토할 수 있는 데이터 세트를 구축했습니다. 이로 인해 전미 차원의 규제 변경이 가속화될 가능성이 있습니다. 여기서 시사하는 바는 지역 한정 정책 실험이 사실상 4상 안전성 시험의 역할을 수행하고 있으며, 전국적인 확대에 앞서 규제 당국에 실증적인 확신을 심어주고 있다는 점입니다. 호주의 사례는 의료 목적의 사용과 엄격한 공급망 관리가 공존할 수 있음을 보여주고 있으며, 전 세계적으로 이러한 정책이 확산되는 데 기여하고 있습니다.

제한적인 보험 적용 및 환급 절차

표준 지급자 코드가 존재하지 않기 때문에 환자의 본인 부담금이 높은 수준을 유지하고 있어, 보급이 지연될 가능성이 있습니다. 그러나 한편으로는 이는 의료 제공업체가 약물, 치료법 및 사후 관리를 하나의 패키지로 묶은 종합적 지불 모델을 시도하도록 유도하는 요인이 되고 있습니다. 초기 의료경제 분석에 따르면, 실로시빈을 이용한 2회의 세션으로 1년 치 항우울제 비용을 상쇄할 수 있는 것으로 나타났으며, 이 데이터는 의료비 억제 위원회에 있어 설득력 있는 근거가 됩니다. 이로부터 도출되는 결론은 대규모 공적 보험사가 단 한 번이라도 환각제 치료를 보장하기 시작하면, 효과적인 치료를 거부한다는 인상을 피하기 위해 민간 보험사들도 곧바로 뒤따를 것이라는 점입니다. 그러나 관할 구역마다 차이가 있으므로, 스폰서는 국가별로 특화된 약제경제학적 자료를 준비해야 합니다.

부문별 분석

2025년 기준으로 케타민은 환각제 시장의 44.70%를 차지했습니다. 새로운 경구용 서방형 정제로 인해 해리 증상이 완화되어, 이로 인해 정신과 분야에서 더 광범위하게 채택되고 있습니다. 이를 바탕으로 볼 때, 투여의 편의성으로 인해 케타민은 유지 요법으로 전환될 것이며, 재처방에 따른 수익원이 증가할 것으로 예측됩니다. 실로시빈은 연평균 17.85%의 성장률을 기록하고 있으며, 두 건의 획기적 치료법 지정을 통해 혜택을 누리고 있어, 환각제 의약품 업계의 파이프라인에서 가장 빠르게 성장하는 제품으로 자리매김하고 있습니다.

실로시빈의 합성 유사체는 환각 작용의 지속 시간을 단축하는 것을 목표로 하며, 입원 없이 지역 클리닉에서 이를 도입할 수 있게 해줍니다. MDMA의 PTSD 적응증 승인이 임박함에 따라, 보험사의 관심이 우울증에서 트라우마 치료로 이동하고, 수익 구조가 다각화될 가능성이 있습니다. 이 부문의 경쟁 압력은 소규모 개발 기업들이 희귀질환 적응증으로 방향을 전환하도록 유도하여, 희귀질환 치료제 지정을 통해 얻을 수 있는 이점을 확보하도록 하고 있습니다. 새로운 화학물질이 등장함에 따라, 제형 유형의 다양화로 인해 단일 자산의 성공에 대한 의존도가 낮아지고, 시장 전체의 회복력이 강화됩니다.

2025년에는 합성 화합물이 환각제 시장의 63.80%를 차지했습니다. 이는 GMP 제조가 규제 당국의 승인을 받는 기반이 되기 때문입니다. 즉, 배치 간 일관성 덕분에 제품의 편차로 인한 임상시험 지연 위험이 줄어든다는 추론입니다. 제품의 편차는 종종 간과되기 쉬운 비용 요인입니다. 그러나 ‘천연’ 정신 건강 지원 제품에 대한 소비자의 신뢰가 높아짐에 따라 식물 유래 실로시빈에 대한 수요가 증가하고 있으며, 이 틈새 시장의 성장률은 14.2%를 나타낼 것으로 예측됩니다.

반합성 하이브리드 제품은 특허 유효 기간을 유지하면서 ‘진품’이라는 스토리성을 활용하고 있어, 제약 업계의 엄격함과 소비자의 인식 사이를 연결하는 가교 역할을 하고 있습니다. 추출 및 정제 기술의 발전으로 인해, 현재는 약전 기준을 충족하는 불순물 프로파일을 가진 미세결정성 사이로신을 얻을 수 있게 되었으며, 기존의 ‘천연’ 대 ‘합성’이라는 이분법은 점차 모호해지고 있습니다. 전략적 관점에서 볼 때, 정제 기술에 관한 지적재산권 출원은 새로운 분자에 관한 출원과 동등한 가치를 갖게 될 가능성이 있으며, 이러한 추세는 대마 시장에서도 관찰됩니다.

지역별 분석

2025년 사이키델릭 의약품 시장의 51.60%를 차지한 북미는 선진적인 주 정부 정책, 풍부한 벤처 캐피털, 그리고 일류 학술 연구 거점을 모두 갖추고 있습니다. 매사추세츠주가 매출세의 15%를 재원으로 삼아 ‘천연 환각 물질 위원회’를 설립한 것은 주 정부가 수익 창출과 규제를 동시에 추진하는 좋은 사례입니다. 존스 홉킨스 대학교는 실로시빈 관련 프로그램 확대를 위해 5,500만 달러의 기부금을 확보했습니다. 이는 주목도가 높은 조사에 대해서는 희석 효과를 수반하지 않는 자금이 풍부하게 존재함을 보여줍니다. 또한, 이 지역에는 전문 클리닉 체인의 대부분이 집중되어 있어, 환자 유치 수를 늘리는 데 기여하는 긴밀한 의뢰 네트워크가 형성되어 있습니다. 전략적 관점에서 볼 때, 이러한 높은 밀도가 성과 연계형 상환 시범 사업을 뒷받침하는 요인으로 볼 수 있습니다. 왜냐하면 환자 수가 많을수록 통계적으로 신뢰도가 높은 데이터를 얻을 수 있기 때문입니다.

유럽은 매출액 기준 2위를 차지하고 있으며, 이를 주도하고 있는 곳은 유럽 최초의 상업용 환각제 임상시험 거점인 영국의 Clerkenwell Health 시설입니다. 독일의 제약 생태계는 현지 기업들에게 환각제 원료의 GMP 제조 분야에서 경쟁 우위를 제공하고 있는 반면, 스위스는 환각제 화학 분야의 오랜 전문 지식을 활용하여 국경을 초월한 임상시험을 유치하고 있습니다. 유럽의약품청(EMA)은 적응형 임상시험 설계에 대한 참여에 긍정적인 태도를 보이고 있으며, 이를 통해 소규모 바이오테크 기업의 예산과 조화를 이루고 있습니다. 이러한 점에서 범유럽적 임상시험 네트워크가 윤리 심의 승인을 통일함으로써 데이터 수집을 가속화하고, 규제 환경이 느리다는 인식을 불식시킬 가능성이 있다고 볼 수 있습니다.

아시아태평양은 연평균 성장률(CAGR) 14.75%로 성장하고 있으며, 이를 주도하고 있는 것은 해당 지역에서 선구자적 역할을 확고히 한 호주 연방 정부의 약물 분류 재검토 결정입니다. 초기 단계 임상시험에서 발생하는 고액의 치료비는 경제적으로 여유가 있는 환자들이 본인 부담으로 치료를 받고 있음을 보여주며, 보험 적용이 시작되기 전에 민간 부담에 의한 수요가 임상 인프라 구축을 뒷받침할 수 있음을 시사합니다. 중국에서 부상하고 있는 사이키델릭 리트리트 시장은 전통 의학의 개념과 현대적인 마음챙김을 융합하고 있으며, 서양의 의료 모델과는 다른 문화적 적응의 길을 제시하고 있습니다. 일본은 동향을 주시하면서도, 국가 정신건강 이니셔티브의 일환으로 기초 연구에 대한 자금 지원을 지속하고 있으며, 향후 임상 적용을 위한 기반을 마련하고 있습니다. 이러한 점에서 볼 때, 아시아·태평양 지역의 성장은 의료 관광과 국내에서의 점진적인 규제 완화가 결합되는 데 달려 있을 것으로 추정됩니다. 이는 과거 대마 시장에서 나타났던 양상과 유사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the psychedelic drugs market size was valued at USD 4.08 billion in 2025 and estimated to grow from USD 4.63 billion in 2026 to reach USD 8.75 billion by 2031, at a CAGR of 13.55% during the forecast period (2026-2031).

This report is Segmented by Drug Type (Ketamine, Psilocybin, and More), Source (Naturally-Derived and Synthetic), Application (Treatment-Resistant Depression, and More), Route of Administration (Oral, and More), Distribution Channel (Hospital Pharmacy, and More), End-Use Setting (Hospitals, and More), and Geography (North America, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Psychedelic Drugs Market Trends and Insights

Rising Global Prevalence of Mental-Health Disorders and Unmet Therapeutic Needs

The escalating incidence of treatment-resistant depression and anxiety is expanding the psychedelic drugs market size by increasing the addressable patient pool. Phase 2 studies showing 75 % remission with psilocybin after two doses have amplified clinician interest because durable responses can lower total therapy hours per year. Health systems facing psychiatrist shortages are inferring that high-impact, low-frequency interventions could relieve bottlenecks in outpatient care. As awareness rises, patient advocacy groups are urging payers to reassess cost-effectiveness models that rely on long-term antidepressant adherence.

Progressive Regulatory Shifts Toward Medicalization and De-Scheduling of Psychedelics

More explicit FDAguidance on clinical trial design and breakthrough designations is shortening development timelines, directly influencing psychedelic drugs market share capture by late-stage sponsors. Oregon and Colorado have issued licenses for supervised psilocybin services, creating data sets that federal agencies can review, which may speed national rescheduling. The inference here is that localized policy experiments are effectively functioning as phase 4 safety studies, giving regulators empirical assurance before national roll-outs. Australia's precedent supports global policy diffusion because it shows that medicalized use can coexist with stringent supply-chain controls.

Limited Insurance Coverage and Reimbursement Pathways

The absence of standard payer codes keeps patient out-of-pocket costs high and may delay widespread uptake. Yet, it also incentivizes providers to experiment with bundled-payment models that package drug, therapy, and follow-up. Early health economic analyses indicate that two psilocybin sessions can offset a year's worth of antidepressant spend, a data point that resonates with cost-containment committees. The inference is that once a single large public insurer covers a psychedelic intervention, private insurers will quickly follow to avoid the perception of denying effective care. Jurisdictional variability, however, means sponsors must prepare country-specific pharmacoeconomic dossiers.

Other drivers and restraints analyzed in the detailed report include:

- Escalating Institutional and Strategic Investment Fueling R&D and Commercial Infrastructure

- Expansion of Health-Care Delivery Models Enabling Psychedelic-Assisted Therapy

- Persisting Societal Stigma and Patient Acceptance Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ketamine holds 44.70% psychedelic drugs market share in 2025. Novel oral extended-release tablets are reducing dissociation events, which supports broader psychiatric adoption. A logical inference is that dosing convenience will pivot ketamine toward maintenance therapy regimes, increasing repeat-prescription revenue streams. Psilocybin, growing at 17.85% annually, benefits from double breakthrough therapy designations, positioning it as the fastest mover in the psychedelic drugs industry pipeline.

Psilocybin's synthetic analogs aim to shorten hallucinogenic duration, enabling community clinic roll-out without overnight stays. MDMA's pending PTSD approval could shift payer focus from depression to trauma care, diversifying the revenue mix. The segment's competitive pressure is steering smaller developers toward ultra-rare indications to secure orphan designation advantages. As new chemical entities emerge, drug-type diversification reduces reliance on single-asset success and strengthens overall market resilience.

Synthetic compounds command 63.80% psychedelic drugs market size in 2025 because GMP manufacturing underpins regulatory acceptance. The inference is that batch consistency reduces the risk of trial delays due to product variability, an often-overlooked cost driver. Growing consumer trust in "natural" mental health aids, however, lifts demand for botanically derived psilocybin, granting that niche a 14.2% growth rate.

Semi-synthetic hybrids are capitalizing on the authenticity narrative while retaining patent life, creating a bridge between pharmaceutical rigor and consumer perception. Extraction-purification advances now yield micro-crystalline psilocin with impurity profiles that satisfy pharmacopeia standards, blurring the old natural-versus-synthetic divide. A strategic inference is that IP filings around purification technology could become as valuable as those for new molecules, a trend mirrored in cannabis markets.

Geography Analysis

North America, with a 51.60% psychedelic drugs market share in 2025, combines progressive state policy, substantial venture capital, and premier academic centers. Massachusetts' creation of a Natural Psychedelic Substances Commission, funded via a 15% sales tax, exemplifies how states monetize and regulate simultaneously. Johns Hopkins secured USD 55 million in philanthropy to expand psilocybin programs, illustrating that non-dilutive funding is abundant for high-profile research. The region also houses most specialty clinic chains, yielding dense referral networks that drive patient throughput. A strategic inference is that this density will support outcome-based reimbursement pilots because large patient volumes yield statistically robust data.

Europe ranks second by revenue, paced by the United Kingdom's Clerkenwell Health facility, the continent's first commercial psychedelic trials hub. Germany's pharmaceutical ecosystem gives local firms an edge in GMP manufacturing of psychedelic APIs, while Switzerland leverages historical expertise in psychedelic chemistry to attract cross-border trials. The European Medicines Agency has signaled its willingness to engage in adaptive trial designs, creating alignment with smaller biotech budgets. An inference is that pan-European clinical trial networks could accelerate data collection by harmonizing ethics approvals, countering the perception of a slow regulatory environment.

Asia-Pacific grows at 14.75% CAGR, led by Australia's federal rescheduling decision that entrenches its role as regional trailblazer. High treatment costs in early clinics demonstrate that affluent patients will self-fund, hinting that private-pay demand can bootstrap clinical infrastructure before insurance arrives. China's emerging psychedelic retreat market blends traditional medicine concepts with modern mindfulness, suggesting cultural adaptation pathways distinct from Western medical models. Japan monitors developments but continues to fund basic research under its state mental-health initiative, laying the groundwork for future clinical translation. The inference is that Asia-Pacific growth will hinge on a mix of medical tourism and gradual domestic liberalization, a pattern earlier seen in cannabis markets.

- Janssen (Johnson & Johnson)

- Jazz Pharmaceuticals

- Pfizer

- Hikma Pharmaceuticals

- Fresenius

- B. Braun

- Teva Pharmaceutical Industries

- Sun Pharma (Taro)

- Accord Healthcare

- Sandoz Group

- Mylan (Viatris)

- Baxter

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Prevalence of Mental-Health Disorders and Unmet Therapeutic Needs

- 4.2.2 Progressive Regulatory Shifts Toward Medicalization and De-Scheduling of Psychedelics

- 4.2.3 Escalating Institutional & Strategic Investment Fuelling R&D and Commercial Infrastructure

- 4.2.4 Expansion of Health-Care Delivery Models Enabling Psychedelic-Assisted Therapy

- 4.2.5 Strategic Pharma-Biotech Alliances Targeting Novel Psychedelics

- 4.2.6 Liberalization of Controlled-Substance Laws and Expansion of Ketamine Clinic Networks

- 4.3 Market Restraints

- 4.3.1 Limited Insurance Coverage and Reimbursement Pathways

- 4.3.2 Persisting Societal Stigma and Patient Acceptance Barriers

- 4.3.3 Adverse-Event Management Requiring Certified Psychotherapists

- 4.3.4 High Assisted-Therapy Session Costs Hindering Payer Reimbursement

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Type

- 5.1.1 Gamma-Hydroxybutyric Acid (GHB)

- 5.1.2 Ketamine

- 5.1.3 Psilocybin

- 5.1.4 Lysergic Acid Diethylamide (LSD)

- 5.1.5 3,4-Methylenedioxymethamphetamine (MDMA)

- 5.1.6 Dimethyltryptamine (DMT)

- 5.1.7 Ibogaine

- 5.1.8 Mescaline

- 5.1.9 Other Drug Types

- 5.2 By Source

- 5.2.1 Naturally-Derived

- 5.2.2 Synthetic

- 5.3 By Application

- 5.3.1 Treatment-Resistant Depression

- 5.3.2 Major Depressive Disorder

- 5.3.3 Post-Traumatic Stress Disorder (PTSD)

- 5.3.4 Substance & Opiate Addiction

- 5.3.5 Anxiety & Panic Disorders

- 5.3.6 Narcolepsy & Sleep Disorders

- 5.3.7 Alcohol Use Disorder

- 5.3.8 Other Applications

- 5.4 By Route of Administration

- 5.4.1 Oral

- 5.4.2 Intranasal

- 5.4.3 Intravenous

- 5.4.4 Sublingual / Buccal

- 5.4.5 Transdermal & Others

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacy

- 5.5.2 Retail Pharmacy

- 5.5.3 Online & Telehealth Platforms

- 5.5.4 Other Distribution Channels

- 5.6 By End-use Setting

- 5.6.1 Specialized Psychedelic Clinics

- 5.6.2 Hospitals

- 5.6.3 Research & Academic Institutes

- 5.6.4 Homecare Settings

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Janssen (Johnson & Johnson)

- 6.3.2 Jazz Pharmaceuticals

- 6.3.3 Pfizer

- 6.3.4 Hikma Pharmaceuticals

- 6.3.5 Fresenius Kabi

- 6.3.6 B. Braun Medical

- 6.3.7 Teva Pharmaceutical Industries

- 6.3.8 Sun Pharma (Taro)

- 6.3.9 Accord Healthcare

- 6.3.10 Sandoz

- 6.3.11 Mylan (Viatris)

- 6.3.12 Baxter International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment