|

시장보고서

상품코드

2061707

유럽의 군용 무인 차량 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2031년)Europe Military Unmanned Vehicles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

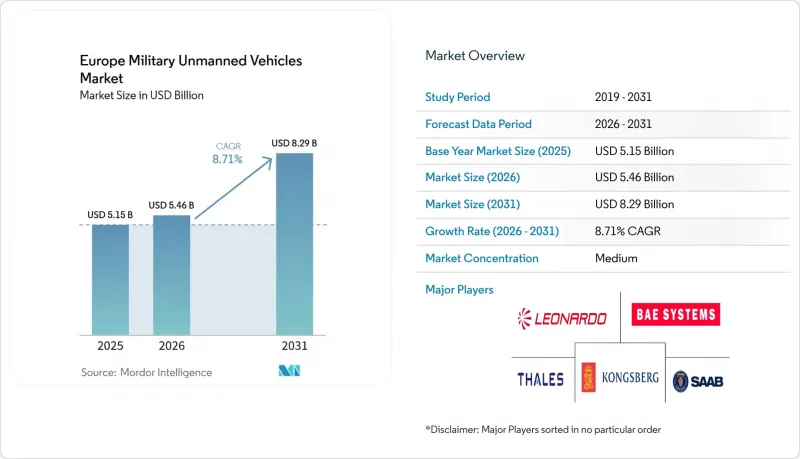

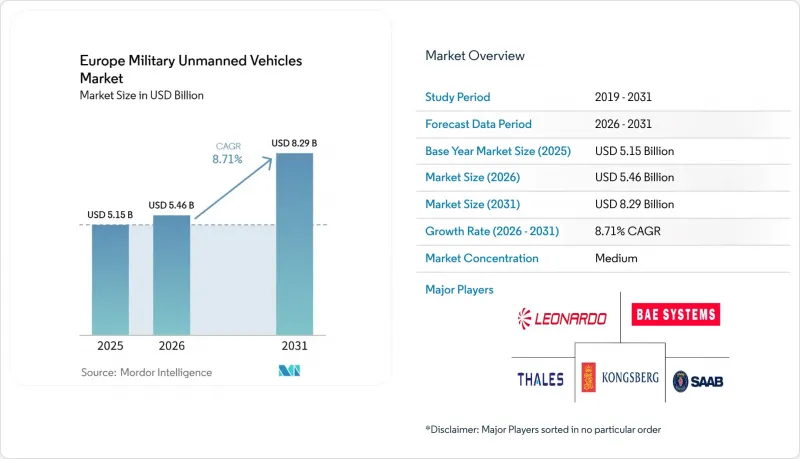

Mordor Intelligence에 의하면, 유럽의 군용 무인 차량 시장 규모는 2025년 51억 5,000만 달러로 평가되었습니다. 2026년에는 54억 6,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 8.71%를 나타내, 2031년에는 82억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 플랫폼 유형(무인 항공기, 무인 지상 차량 등), 운용 모드(원격 조종, 반자율형 등), 용도(정보·감시·정찰 등), 차량 크기(소형, 중형, 대형) 및 지역(영국, 독일 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 군용 무인 차량 시장 동향과 인사이트

국방 예산 증액이 다중 도메인 무인 시스템의 조달을 가속화

2025년에 유럽의 국방비는 증가할 전망이며, 육상, 항공, 해상 임무에 사용되는 무인 플랫폼을 지속적으로 우선시하고 있어, 유럽의 군용 무인 차량 시장 전체에 걸쳐 대규모의 지속적인 조달 주기를 뒷받침하고 있습니다. 독일은 수백 대의 협업형 항공기 개발 계획의 일환으로, 2026년에 예정된 공동 회전익 탄약 조달을 포함해 무인 체계에 막대한 자금을 배정했습니다. 폴란드의 국방 지출은 높은 요격 성공률을 자랑하는 대UAS(무인항공기 시스템) 체계와 국내 UAV(무인항공기) 생산 라인 확장에 중점을 두고 있습니다. 프랑스는 향후 10년 동안 무인 시스템에 막대한 자원을 투입하고 있으며, 국내 생산 및 소프트웨어 주도형 아키텍처를 추진하기 위해 AI 탑재 드론 개발에 추가 투자를 단행함으로써 장기적인 기술적·운용적 목표를 뒷받침하고 있습니다. 이러한 예산 배분은 단계적인 업그레이드가 아닌 전 함대의 현대화를 목표로 하고 있으며, 각 군종 간 상호 운용이 가능한 제어 시스템과 공통 페이로드 규격을 중시하고 있습니다.

EU 및 NATO의 현대화 프로그램이 자율 기술의 도입을 확대되고 있습니다.

유럽 방위 기금은 2021년부터 2027년까지 70억 유로(81억 4,000만 달러)를 출연하기로 결정했으며, 이 막대한 자금을 AI 및 디지털 기술에 배정하고 있습니다. 이러한 요소들은 2026년 2월 프랑스, 독일, 이탈리아, 폴란드, 영국이 출범시킨 LEAP와 같은 상호 운용 가능한 프로그램을 뒷받침하는 기반이 되고 있습니다. 2025년 10월에 채택된 스웨덴의 LUUV 프로그램은 GPS를 사용할 수 없는 해상 임무를 위해 AI 항법 시스템을 통합했으며, 2026년 여름에 시험 단계로 넘어갈 예정으로, 한랭 수역 환경에서의 조만간 실용화를 시사하고 있습니다. LEAP 이니셔티브는 공통 데이터 링크 규격의 도입을 가속화하여 각국 함대 간의 중복을 줄이고, 합동 작전을 가능하게 합니다. 유럽의 군용 무인 차량 시장은 NATO 작전 부대와의 통합을 용이하게 하고, ISR(정보·감시·정찰), 병참, 대기뢰 임무에서 국경을 초월한 즉각 대응 태세를 촉진하는 통합 규격의 혜택을 누리고 있습니다.

EU 회원국 간의 조달 규제 및 항공 적합성 인증의 분절화

인증 절차는 국가와 범주에 따라 다르며, 이로 인해 유럽의 군용 무인 차량 시장의 국경을 초월한 확장에 차질이 발생하고 있습니다. 전자기 호환성 및 분리 공역 내 충돌 회피를 포함한 각국의 시험 요건은 관할 구역을 넘나드는 공급업체의 비용을 증가시킵니다. 이러한 차이는 수명 주기 비용을 증가시키고, 다국적 여단 내 혼성 함대의 유지 계획을 복잡하게 만들며, 나아가 운용 효율과 장기적인 자원 배분에 영향을 미칩니다. NATO의 STANAG 4586에 따른 표준화는 지상 및 해상 관제 장비에 대해서는 아직 종합적이지 않아, 그 결과 통합 시에는 다중 공급업체 팀이 직접 인터페이스 작업을 처리해야 합니다. EU 사이버보안법은 산업용 제어 시스템에 대한 IEC 62443 인증을 장려하고 있으며, 많은 플랫폼에서는 연결성 및 자율성 구성 요소에 필요한 보증 수준을 충족하기 위해 여전히 개조가 필요합니다.

부문별 분석

2025년에는 무인항공기(UAV)가 76.86%의 점유율로 1위를 차지했으나, 나토(NATO)가 북해 및 발트해 전구에서의 기뢰 대책과 해저 안보를 우선시함에 따라, 무인수중정(UMV) 시장은 2031년까지 연평균 성장률(CAGR) 13.99%로 확대될 것으로 전망됩니다. 벨기에·네덜란드의 rMCM 프로그램(총액 22억 유로/25억 6,000만 달러)는 2026년 3월에 첫 번째 함정을 인도하고, 고위험 기뢰 제거 임무를 유인 함정에서 무인 수상·수중 차량으로 전환함으로써 임무당 비용을 50-60% 절감하는 것을 목표로 하고 있습니다. 스웨덴 크로나 6,000만 크로나(630만 달러) 규모의 LUUV 계약은 AI 기반 소나 분류 기술을 활용해 GPS를 사용할 수 없는 환경을 대상으로 하며, 2026년 3분기 시험에서는 한랭 해역에서의 장시간 초계 및 저지연 운영자 감시가 검증될 예정입니다. UGV(수상 무인정)은 시장 점유율의 10% 중반대를 차지하고 있으며, 물류 및 폭발물 처리(EOD) 분야에서 성장이 기대되고 있습니다. 이는 각 부대가 개방형 인터페이스를 통해 페이로드를 통합하는 표준화된 플랫폼을 도입함으로써, 유지보수 및 훈련 부담을 줄이고 있기 때문입니다. 유럽의 군용 무인 차량 시장에서 UAV는 여전히 판매량 증가를 주도하고 있습니다. 이는 특히 BVLOS(시야 외 비행)가 필요하지 않은 경우, 그룹 1 및 그룹 2 시스템이 상용 부품이나 이중 용도 공급망을 활용하여 신속하게 규모를 확대할 수 있기 때문입니다. 무인 해양 시스템은 기뢰 감지 및 제거를 위한 NATO 인증 임무 패키지의 혜택을 받고 있으며, 해상 요충지의 위험도가 높아짐에 따라 자본 예산에서 차지하는 비중이 확대되고 있습니다.

UMV의 도입으로 무인 모함과 자율형 기뢰 감지 차량을 결합함으로써, 승무원을 추가적인 IED 위험에 노출시키지 않고도 수색 범위를 확대하여 함대 구성이 재편되고 있습니다. 항공 분야에서는 영국의 ‘프로텍터 RG Mk1’이 AI 지원 기반 계획 수립, 멀티센서 앙상블, 그리고 STANAG 4586 준수를 통해 ISR의 현대화를 주도하고 있으며, NATO 자산과의 연계를 가능하게 하고 있습니다. 지상 로봇은 기지 병참 지원 및 폭발물 처리(EOD) 분야에서 여전히 필수적이며, 유럽의 프로그램에서는 현재 투자를 보호하고 공급업체에 대한 종속을 피하기 위해 여러 섀시에 재장착이 가능한 자율 주행 키트가 선호되고 있습니다. 유럽의 군용 무인 차량 시장에서는 공통된 지휘통제 및 관제 스테이션 규격이 채택되어 있어, NATO의 요청에 따라 ISR, 후방 지원, 공병 임무 간에 차량을 유연하게 재배치할 수 있습니다. 조달 팀은 플랫폼에 구애받지 않는 자율 레이어를 원하고 있습니다. 이는 유럽의 군용 무인 차량 시장에서 소프트웨어 재사용 및 부대 간 훈련 공유를 통해 장기적인 비용 절감이 실현되기 때문입니다.

2025년에는 원격 조종 시스템이 46.24%의 점유율을 차지했으나, 대항적 전자전(EW) 환경의 확대에 따라, 상시 제어 링크에 의존하지 않는 차량 내 의사결정 루프의 필요성이 높아짐에 따라, 완전 자율형 플랫폼은 2031년까지 연평균 성장률(CAGR) 11.24%로 확대될 것으로 예측됩니다. 헬싱사의 CA-1 Europa는 사이클 타임을 단축한 협력적 다중 플랫폼 작전을 입증하고 있으며, 이는 NATO가 추진하는 강력한 킬 체인 구상과 부합합니다. 스웨덴에서 실시된 100대 규모의 무인항공기(UAS) 스웜 실증 실험을 통해, 한 명의 운영자가 광범위한 지역의 복잡한 수색 및 배치 패턴을 감독할 수 있음이 입증되어, 출격당 필요한 인원을 줄일 수 있게 되었습니다. 반자율 주행 모드는 유럽의 군용 무인 차량 시장에서 속도와 감시의 균형을 유지하면서, 주요 단계에 대해 사람의 승인을 받은 후 사전에 프로그래밍된 경로를 주행할 수 있게 해주기 때문에 30% 중반대 시장 점유율을 차지하고 있습니다. 완전 자율 모드의 발전은 교전 규칙상 즉각적인 인적 승인이 필요하지 않으며, 엄격한 시간 제한이나 열악한 통신 환경 하에서도 작전을 수행할 수 있도록 지원하는 ISR(정보·감시·정찰) 및 병참 분야에 중점을 두고 있습니다. EU의 AI 법은 군사적 용도를 적용 대상에서 제외하고 있지만, 각국 군은 윤리적·안전상의 관행을 표준화하기 위한 NATO 차원의 지침을 기다리는 한편, 운용상의 안전 조치를 계속해서 마련하고 있습니다.

각 공급업체는 운전자가 개입할 수 있음을 보장하는 ‘감시 모드’를 핵심으로 하는 자율 주행 시스템을 구축하고 있으며, 이를 통해 유럽 무인 차량 업계에서 지휘관 및 조달 당국의 수용도를 높이고 있습니다. 전파 간섭이 우려되는 지역에서는 원격 제어 모드에서 자율 주행 모드로의 제어 이관을 표준화하는 것이 설계 요건으로 자리 잡고 있으며, 항공 당국은 다수 차량에 의한 운용과 관련된 안전성 검증을 지속적으로 진행하고 있습니다. 이 훈련 프로그램에는 운영자가 보다 안전하게 감시할 수 있도록 인간과 기계의 팀 훈련이 포함되어 있으며, 교전 결정에 관한 교리는 유의미한 인적 통제 기준과 일치합니다. 예측 기간 동안 유럽의 군용 무인 차량 시장에서 자율 기술의 도입은 ISR(정보·감시·정찰) 및 병참 분야에서 시작하여, 기내 처리 및 결정론적 동작을 통해 임무 수행 시점이 개선되는 공병 및 대지뢰 임무 분야로 확대될 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the europe military unmanned vehicles market size is expected to grow from USD 5.15 billion in 2025 to USD 5.46 billion in 2026 and is forecast to reach USD 8.29 billion by 2031 at 8.71% CAGR over 2026-2031.

This report is Segmented by Platform Type (Unmanned Aerial Vehicles, Unmanned Ground Vehicles, and More), Mode of Operation (Remotely Piloted, Semi-Autonomous, and More), Application (Intelligence, Surveillance, and Reconnaissance, and More), Vehicle Size (Small, Medium, and Large), and Geography (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Military Unmanned Vehicles Market Trends and Insights

Rising Defense Budgets Accelerate Multi-Domain Unmanned Procurement

European defense spending increased in 2025 and continues to prioritize unmanned platforms in land, air, and maritime missions, supporting scale and recurring procurement cycles across the Europe military unmanned vehicles market. Germany allocated significant funding for unmanned capabilities, including a joint loitering-munition award planned for 2026, as part of efforts to develop hundreds of collaborative aircraft. Poland's defense spending emphasizes counter-UAS systems with high interception success rates and the expansion of domestic UAV production lines. France has committed substantial resources to unmanned systems through the next decade, with additional investments in AI-enabled drone development to advance domestic manufacturing and software-driven architectures, supporting long-term technological and operational objectives. These allocations target full-fleet modernization rather than incremental upgrades, which favors interoperable control systems and common payload standards across services.

EU And NATO Modernization Programs Expand Autonomous Adoption

The European Defence Fund committed EUR 7 billion (USD 8.14 billion) for 2021-2027 and has allocated a significant amount to AI and digital technologies, which underpin interoperable programs such as LEAP, launched by France, Germany, Italy, Poland, and the UK in February 2026. Sweden's LUUV program, awarded in October 2025, integrates AI navigation for GPS-denied maritime missions and is set to move to summer 2026 trials, signaling near-term operationalization in cold-water environments. The LEAP initiative accelerates the adoption of common data-link standards to reduce duplication across national fleets and enable combined operations. The Europe military unmanned vehicles market benefits from aligned standards that ease integration into NATO task groups and facilitate cross-border readiness for ISR, logistics, and counter-mine missions.

Fragmented Procurement Regulations and Airworthiness Certification Across EU Member States

Certification pathways vary by country and category, introducing friction that slows cross-border deployments in the Europe military unmanned vehicles market. National testing requirements, including electromagnetic compatibility and collision-avoidance in segregated airspace, increase supplier costs across jurisdictions. These variations increase lifecycle costs and complicate sustainment planning for mixed fleets in multinational brigades, thereby impacting operational efficiency and long-term resource allocation. NATO's STANAG 4586 harmonization is not yet comprehensive for ground and maritime controllers, which leaves multi-vendor teams to handle interface work themselves during integration. The EU Cybersecurity Act drives IEC 62443 certification for industrial controls, and many platforms still need retrofits to meet required assurance levels for connectivity and autonomy components.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Autonomy Improves Mission Efficiency and Reduces Risk

- EU Action Plans on Drone and Counter-Drone Security Unlock New Programs

- Cybersecurity and EW Vulnerabilities In C2 Links And GNSS-Dependent Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

UAVs led with a 76.86% share in 2025, while UMVs are projected to expand at a 13.99% CAGR through 2031 as NATO prioritizes mine countermeasures and undersea security in the North Sea and Baltic theaters. The Belgian-Dutch rMCM program, valued at EUR 2.2 billion (USD 2.56 billion), delivered the first vessels in March 2026 and aims to cut per-mission costs by 50-60% by shifting high-risk clearance tasks from crewed hulls to unmanned surface and underwater vehicles. Sweden's LUUV contract for SEK 60 million (USD 6.3 million) targets GPS-denied environments with AI-based sonar classification, and third-quarter 2026 trials will test longer patrol durations and low-latency operator oversight in cold waters. UGVs hold a mid-teen share, with growth in logistics and EOD roles, as units field standardized platforms that integrate payloads via open interfaces to reduce maintenance and training burdens. The Europe military unmanned vehicles market continues to see UAVs as the volume driver because Group 1 and Group 2 systems scale quickly with commercial components and dual-use supply chains, especially where BVLOS is not required. Unmanned marine systems benefit from NATO-certified mission packages for mine detection and neutralization, and now receive a larger share of capital budgets as maritime choke points elevate risk profiles.

UMV adoption reshapes fleet composition by combining unmanned mother ships with autonomous mine-hunting vehicles to expand coverage without exposing crews to more IEDs. In the air domain, the United Kingdom's Protector RG Mk1 anchors ISR modernization through AI-assisted planning, multi-sensor ensembles, and STANAG 4586 compatibility, enabling collaboration with NATO assets. Ground robotics remains essential for base logistics and EOD, and European programs now favor autonomy kits that can be refitted across multiple chassis to protect investment and avoid lock-in. The Europe military unmanned vehicles market supports common command-and-control and control station standards so teams can reallocate vehicles between ISR, logistics, and engineering missions as needed NATO. Procurement teams seek platform-agnostic autonomy layers because long-term cost savings derive from software reuse and shared training across formations in the Europe military unmanned vehicles market.

Remotely piloted systems held a 46.24% share in 2025, while fully autonomous platforms are projected to expand at a 11.24% CAGR through 2031 as contested EW environments increase the need for on-board decision loops that do not depend on constant control links. Helsing's CA-1 Europa demonstrates coordinated multi-platform engagements with faster cycle times, aligning with NATO's push for resilient kill chains. Sweden's 100-UAS swarm demonstration showed that one operator can supervise complex search-and-allocation patterns across large areas, reducing manpower requirements per sortie. Semi-autonomous modes hold a mid-30s share because they allow pre-programmed routes with human authorization for key steps, balancing speed and oversight in the Europe military unmanned vehicles market. Fully autonomous growth focuses on ISR and logistics, where rules of engagement do not require immediate human authority, and autonomy supports tight timelines and sparse communications. The EU AI Act exempts military applications, but militaries continue to define operational guardrails while awaiting NATO-level guidance to standardize ethical and safety practices.

Suppliers build autonomy stacks around supervised modes that ensure an operator can intervene, thereby improving acceptance among commanders and procurement authorities in the European unmanned vehicles industry. Standardized handoff of control from remote to autonomous modes is becoming a design requirement in RF-contested areas, and airworthiness authorities continue to address safety cases for multi-vehicle operations. Training pipelines include human-machine team drills so operators can safely supervise more safely, and doctrine aligns with meaningful human control standards for engagement decisions. Over the forecast period, autonomy adoption is likely to expand from ISR and logistics to engineering and mine-countermeasure roles where on-board processing and deterministic behaviors improve mission timing in the Europe military unmanned vehicles market.

List of Companies Covered in this Report:

- Airbus SE

- Leonardo S.p.A.

- Dassault Aviation SA

- Rheinmetall AG

- BAE Systems plc

- Thales Group

- Saab AB

- Milrem AS

- QinetiQ Group

- Kongsberg Gruppen ASA

- Exail Technologies SA

- Elbit Systems Ltd.

- Israel Aerospace Industries Ltd.

- Lockheed Martin Corporation

- General Atomics

- Northrop Grumman Corporation

- Textron Inc.

- L3Harris Technologies, Inc.

- AeroVironment, Inc.

- Anduril Industries, Inc.

- DroneShield Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Operational success of low-cost attritable drone swarms in Ukraine influencing European defense strategies

- 4.2.2 Large EU and NATO modernization programs driving adoption of autonomous and unmanned systems

- 4.2.3 Rising defense budgets in Europe accelerating procurement of multi-domain unmanned platforms

- 4.2.4 Advancements in AI-enabled autonomy improving mission efficiency and reducing manpower risks

- 4.2.5 EU action plans on drone and counter-drone security unlocking new funding and development initiatives

- 4.2.6 Emergence of European tier-2 and tier-3 suppliers strengthening the regional unmanned systems ecosystem

- 4.3 Market Restraints

- 4.3.1 Cybersecurity and EW vulnerabilities in C2 links and GNSS-dependent platforms

- 4.3.2 Fragmented procurement regulations and airworthiness certification across EU member states

- 4.3.3 Dependence on non-European semiconductor and RF component supply chains subject to export controls

- 4.3.4 Rising lifecycle and sustainment costs of advanced autonomous unmanned systems

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 Unmanned Aerial Vehicles (UAVs)

- 5.1.2 Unmanned Ground Vehicles (UGVs)

- 5.1.3 Unmanned Marine Vehicles (UMVs)

- 5.2 By Mode of Operation

- 5.2.1 Remotely Piloted

- 5.2.2 Semi-Autonomous

- 5.2.3 Fully Autonomous

- 5.3 By Application

- 5.3.1 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.3.2 Combat

- 5.3.3 Logistics and Resupply

- 5.3.4 Explosive Ordnance Disposal (EOD)

- 5.3.5 Mine Counter-Measures (MCM)

- 5.3.6 Others

- 5.4 By Vehicle Size

- 5.4.1 Small

- 5.4.2 Medium

- 5.4.3 Large

- 5.5 By Geography

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 Spain

- 5.5.4 Italy

- 5.5.5 France

- 5.5.6 Russia

- 5.5.7 Norway

- 5.5.8 Poland

- 5.5.9 Sweden

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Airbus SE

- 6.4.2 Leonardo S.p.A.

- 6.4.3 Dassault Aviation SA

- 6.4.4 Rheinmetall AG

- 6.4.5 BAE Systems plc

- 6.4.6 Thales Group

- 6.4.7 Saab AB

- 6.4.8 Milrem AS

- 6.4.9 QinetiQ Group

- 6.4.10 Kongsberg Gruppen ASA

- 6.4.11 Exail Technologies SA

- 6.4.12 Elbit Systems Ltd.

- 6.4.13 Israel Aerospace Industries Ltd.

- 6.4.14 Lockheed Martin Corporation

- 6.4.15 General Atomics

- 6.4.16 Northrop Grumman Corporation

- 6.4.17 Textron Inc.

- 6.4.18 L3Harris Technologies, Inc.

- 6.4.19 AeroVironment, Inc.

- 6.4.20 Anduril Industries, Inc.

- 6.4.21 DroneShield Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment