|

시장보고서

상품코드

2061761

프랑스의 히트펌프 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)France Heat Pump - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

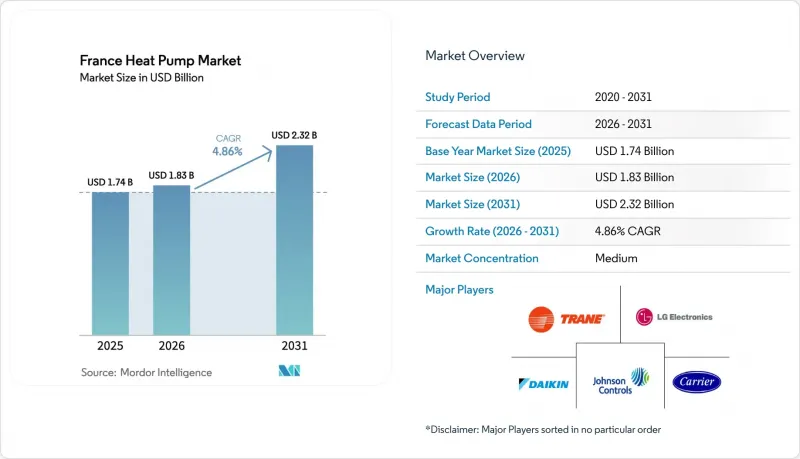

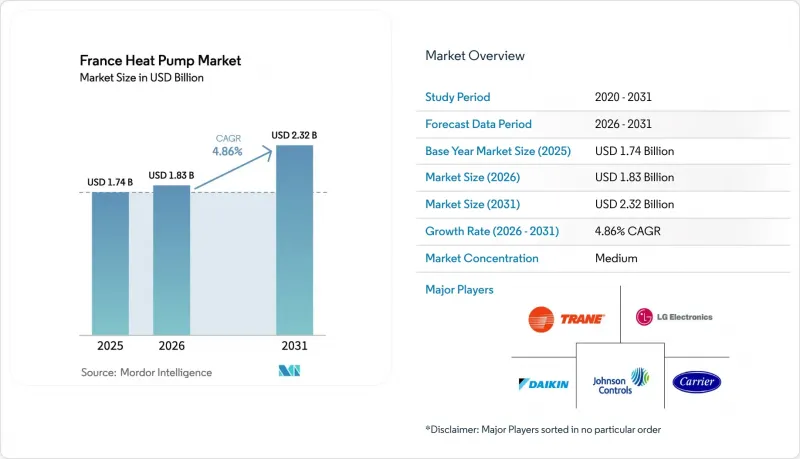

Mordor Intelligence에 의하면, 프랑스의 히트펌프 시장 규모는 2025년 17억 4,000만 달러로 평가되었고, 2026년에는 18억 3,000만 달러로 추정되고, 2026-2031년 CAGR 4.86%로 성장할 전망이며, 2031년에는 23억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 열원 유형별(공기원, 수원 등), 기술별(공기-공기, 공기-물 등), 용량별(10kW 미만, 10-50kW 등), 용도별(공간 난방, 산업 및 공정 가열 등), 최종 사용자별(주택, 상업시설 등), 설치 형태별(신규 설치, 개보수), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

프랑스의 히트펌프 시장 동향 및 인사이트

‘MaPrimeRenov’ 보조금, 대상 시장 확대

프리미엄 등급 보조금을 받기 위해서는 유럽산이어야 한다는 요건이 있으며, 연간 약 20억 유로(22억 4,000만 달러)의 자금이 현지 브랜드로 유입되고 있습니다. 저소득 가구의 지방 지역에서 공기-물식 시스템으로 개조할 경우, 투자 회수 기간이 8년에서 5년으로 단축됩니다. 지열 시스템의 보조금 상한액이 5,000유로(5,600달러)로 인상됨에 따라, 공기열식 설비와의 비용 격차가 줄어들어 2026년에는 판매 대수가 18% 증가할 것으로 전망됩니다. 10kW 미만 부문에서 그동안 25%의 점유율을 차지하던 아시아계 수입업체가 철수함에 따라, 애틀랜틱사와 보쉬사에 즉시 시장 확대의 여지가 생깁니다. EHPA 데이터베이스를 통한 검증을 통해 승인까지 소요되는 기간이 3주 늘어납니다만, 공급망의 투명성은 향상됩니다.

RE2020 건축 에너지 기준, 저탄소 난방 의무화

4 kg CO2e/m²·년의 상한선으로 인해 가스 보일러는 기준을 충족하지 못하게 되어, 2023년에 준공되는 단독주택의 86%가 히트펌프를 선택할 것으로 예측됩니다. 개발업체들은 평생 4만 유로(4만 4,800달러)를 초과할 가능성이 있는 탄소 벌금을 피하기 위해 8,000-1만 2,000유로(8,960-1만 3,440달러)의 추가 외장 비용을 감수하고 있습니다. 옥상 태양광 발전과 히트펌프를 결합함으로써 1차 에너지 계수를 최대 40%까지 절감할 수 있어, 다른 시스템에 할당될 탄소 예산을 확보할 수 있을 뿐만 아니라, 남부 지역에서는 리버서블 유닛의 도입이 촉진되고 있습니다.

냉매 규제가 기술 전환을 가속화

EU 규정 2024/573에 따라 2030년까지 HFC 할당량이 79% 감축되므로, 가연성인 R290 또는 R454B 혼합 가스로의 전환이 시급합니다. R290은 압력이 높기 때문에 더 두꺼운 배관과 새로운 압축기 하우징이 필요하며, 이로 인해 대당 300-500유로(336-560달러)의 추가 비용이 발생합니다. 미쓰비시 전기의 ‘Ecodan 2026’ 시리즈는 이러한 상충 관계를 여실히 보여주고 있습니다. -7℃에서 효율은 15% 향상되지만, 설치 가능한 실내 면적은 20제곱미터 이상으로 제한됩니다.

부문별 분석

2025년, 프랑스의 히트펌프 시장에서 공기원 방식이 매출 점유율 74.78%를 차지하며 시장을 주도했습니다. 설치 비용이 8,000-1만 2,000유로(8,960-1만 3,440달러)로 저렴하기 때문에 기존 라디에이터가 40-55℃의 급수 온도를 지원하는 개조 프로젝트의 경우, 공기원 유닛은 여전히 매력적인 선택지입니다. 지열 이용 프로젝트는 시장 규모는 작지만, 산업 폐열의 통합 및 시추 비용의 감소로 인해 연평균 5.31%의 성장이 예상됩니다. 수열 이용 장치는 ‘물 프레임워크 지침’에 따른 허가 절차가 복잡하여 틈새 시장에 머물러 있지만, 하이브리드형(가스+히트펌프) 시스템은 탄소 배출 벌금이 부과됨에도 불구하고 보일러 철거를 주저하는 가구들로부터 지지를 받고 있습니다.

화강암 지질, 얕은 대수층, 그리고 넉넉한 보조금 덕분에 브르타뉴는 프랑스 내 지열 이용의 거점으로 자리매김하고 있으며, 북부의 퇴적암 지대와 비교해 시추 비용을 20-30% 절감하고 있습니다. 오베르뉴-론-알프 지역의 산업 관계자들은 염수-물 순환 시스템을 도입하여, 주변 공기 열원 시스템이 3.2에서 한계에 도달하는 반면, 계절 성능 계수 4.5 이상을 달성함으로써, 더 깊은 지열 이용 도입에 대한 경제적 타당성을 입증하고 있습니다.

2025년 매출의 65.86%를 공기-물 시스템이 차지하고 있으며, 이는 기존 물 순환 시스템 및 RE2020 기준에 부합하는 공급 온도와의 호환성을 입증하고 있습니다. 지열 지하-수 시스템은 규모는 작지만, 시추 비용이 1미터당 48유로(54달러)까지 하락했고, RE2020의 1차 에너지 계수 0.6이 초저탄소 열에 우대 조치를 적용하고 있기 때문에 연평균 성장률(CAGR) 5.14%로 가장 빠르게 확대되고 있습니다. 매출의 28%를 차지하는 공기 대 공기 유닛은 남부 지역에서 증가하는 냉방 부하에 대응하고 있지만, MaPrimeRenov의 프리미엄 보조금 대상에서 제외되어 있어 개보수 추세가 주춤하고 있습니다. 물-물 시스템은 여전히 특정 호숫가 지역이나 지역 난방 시범 사업에 국한되어 있습니다.

2026년 1월에 발표된 비스만(Weismann)의 ‘Vitocal 350-G’는 R290 인버터 압축기를 지열 이용에 도입하여, 0℃의 브라인 입구 온도에서 COP 5.2를 달성했으며, 동급의 공기원 유닛보다 35% 뛰어난 성능을 보여주고 있습니다. 이에 대해 보쉬는 ‘Compress 7800i LW’로 맞서고 있습니다. 이는 300리터 용량의 탱크와 기본 제공되는 수요 반응 인터페이스를 내장한 공기-물 방식 플랫폼으로, 효율성 및 전력망 서비스 양 측면에서 경쟁력을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the france heat pump market size is valued at USD 1.83 billion in 2026, up from USD 1.74 billion in 2025, and is projected to reach USD 2.32 billion by 2031, growing at a 4.86% CAGR over 2026-2031.

This report is Segmented by Source Type (Air Source, Water Source, and More), Technology (Air-To-Air, Air-To-Water, and More), Capacity (Below 10 KW, 10-50 KW, and More), Application (Space Heating, Industrial and Process Heating, and More), End User (Residential, Commercial, and More), Installation (New Installation, and Retrofit), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

France Heat Pump Market Trends and Insights

MaPrimeRenov' Subsidies Expand Addressable Market

Premium-tier rebates now require European factory origin, steering roughly EUR 2 billion (USD 2.24 billion) of annual funding toward local brands. Payback periods for rural air-to-water retrofits fall from eight to five years for low-income households. The raised EUR 5,000 (USD 5,600) cap on geothermal systems narrows the cost gap with air-source equipment, supporting an 18% unit-sales bump in 2026. Market share vacated by Asian importers, previously 25% in the sub-10 kW tier, creates immediate runway for Atlantic and Bosch. Verification through the EHPA database adds three-week approval lags but improves supply-chain transparency.

RE2020 Building Energy Code Mandates Low-Carbon Heating

The 4 kg CO2e m-2-year ceiling makes gas boilers non-compliant, prompting 86% of single-family completions in 2023 to choose heat pumps. Developers accept EUR 8,000-12,000 (USD 8,960-13,440) extra envelope cost to avoid lifetime carbon penalties that can exceed EUR 40,000 (USD 44,800). Pairing rooftop photovoltaics with heat pumps cuts primary-energy factors by up to 40%, freeing carbon budget for other systems and tilting specification toward reversible units in the south.

Refrigerant Regulations Accelerate Technology Transition

EU Regulation 2024/573 reduces HFC quotas 79% by 2030, forcing a pivot to flammable R290 or R454B blends. R290's higher pressure demands thicker tubing and new compressor housings, adding EUR 300-500 (USD 336-560) per unit. Mitsubishi Electric's Ecodan 2026 range illustrates the trade-off: 15% higher efficiency at -7 °C but indoor placement limited to rooms above 20 m2.

Other drivers and restraints analyzed in the detailed report include:

- Heat-as-a-Service Models Lower Up-Front Costs

- Smart-Grid Demand Response Revenues Improve ROI

- Shortage of Certified Installers Limits Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air-source configurations led the France heat pump market with 74.78% revenue share in 2025. Favorable capex of EUR 8,000-12,000 (USD 8,960-13,440) installed keeps air units attractive for retrofit scenarios where existing radiators match 40 °C-55 °C water supply. Ground-source projects commanded a smaller base but show 5.31% annual growth potential thanks to industrial waste-heat integration and drilling-cost declines. Water-source units remain niche, bound by Water Framework permitting complexity, while hybrid gas-plus-heat-pump systems appeal to households reluctant to decommission boilers despite carbon penalties.

Granite geology, shallow aquifers, and supportive subsidies make Brittany the national stronghold for ground-source, lowering borehole expenditures 20-30% relative to northern sedimentary zones. Industrial actors in Auvergne-Rhone-Alpes deploy brine-to-water loops achieving seasonal performance factors above 4.5 when ambient air-source rivals stall at 3.2, validating the economic thesis for deeper geothermal adoption.

Air-to-water systems controlled 65.86% of 2025 sales, underscoring their fit with legacy hydronic circuits and RE2020 compliant supply temperatures. Geothermal ground-to-water solutions, although smaller, are the fastest expanding at 5.14% CAGR as drilling prices fall to EUR 48 (USD 54) per meter and RE2020's primary-energy factor of 0.6 rewards ultra-low-carbon heat. Air-to-air units, accounting for 28% of revenue, meet rising cooling loads in the south but lose out on premium MaPrimeRenov' subsidies, curbing retrofit momentum. Water-to-water remains confined to select lakeside or district-heating pilots.

Viessmann's Vitocal 350-G, unveiled January 2026, puts a R290 inverter compressor in geothermal service, posting a 5.2 COP at 0 °C brine inlet, 35% better than air-equivalent units. Bosch counters with the Compress 7800i LW, an air-to-water platform embedding a 300-liter tank and native demand-response interface, signaling competition on both efficiency and grid service.

List of Companies Covered in this Report:

- Trane Inc., Trane Technologies Plc

- LG Electronics Inc.

- Daikin Industries Ltd.

- Johnson Controls International Plc

- Carrier Corporation

- Atlantic Group

- Vaillant Group

- Intuis Inc.

- Bosch Thermotechnology GmbH

- NIBE Energy Systems

- Thermor

- De Dietrich Thermique

- Saunier Duval

- Aldes Corporation

- CIAT Corporation

- Frisquet S.A.

- Viessmann Climate Solutions SE

- Stiebel Eltron GmbH and Co. KG

- Glen Dimplex Thermal Solutions

- Aermec S.p.A.

- Hoval Group

- Baxi Heating, BDR Thermea

- Wolf GmbH

- Ariston Thermo Group

- Panasonic Corporation

- Mitsubishi Electric Corporation

- Hitachi Air Conditioning

- ETT, Energie Transfert Thermique

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 MaPrimeRenov' Subsidies Expand Addressable Market

- 4.2.2 RE2020 Building Energy Code Mandates Low-Carbon Heating

- 4.2.3 Heat-as-a-Service Models Lower Up-Front Costs

- 4.2.4 Smart-Grid Demand Response Revenues Improve ROI

- 4.2.5 Cold-Climate R290 Units Boost Seasonal Performance

- 4.2.6 Industrial Waste-Heat Recovery via High-Temp HPs

- 4.3 Market Restraints

- 4.3.1 Refrigerant Phase-Down Drives Costly Redesigns

- 4.3.2 Shortage of Certified Installers Limits Deployments

- 4.3.3 Grid Congestion Fees in Rural Areas Raise Opex

- 4.3.4 Used-Equipment Grey Market Undercuts OEM Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source Type

- 5.1.1 Air Source

- 5.1.2 Water Source

- 5.1.3 Ground Source

- 5.1.4 Hybrid

- 5.2 By Technology

- 5.2.1 Air-to-Air

- 5.2.2 Air-to-Water

- 5.2.3 Water-to-Water

- 5.2.4 Ground-to-Water

- 5.3 By Capacity

- 5.3.1 Below 10 kW

- 5.3.2 10-50 kW

- 5.3.3 50-200 kW

- 5.3.4 Above 200 kW

- 5.4 By Application

- 5.4.1 Space Heating

- 5.4.2 Space Cooling

- 5.4.3 Domestic and Sanitary Hot Water

- 5.4.4 Industrial and Process Heating

- 5.4.5 Other Applications

- 5.5 By End User

- 5.5.1 Residential

- 5.5.2 Commercial

- 5.5.3 Industrial

- 5.6 By Installation

- 5.6.1 New Installation

- 5.6.2 Retrofit

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Trane Inc., Trane Technologies Plc

- 6.4.2 LG Electronics Inc.

- 6.4.3 Daikin Industries Ltd.

- 6.4.4 Johnson Controls International Plc

- 6.4.5 Carrier Corporation

- 6.4.6 Atlantic Group

- 6.4.7 Vaillant Group

- 6.4.8 Intuis Inc.

- 6.4.9 Bosch Thermotechnology GmbH

- 6.4.10 NIBE Energy Systems

- 6.4.11 Thermor

- 6.4.12 De Dietrich Thermique

- 6.4.13 Saunier Duval

- 6.4.14 Aldes Corporation

- 6.4.15 CIAT Corporation

- 6.4.16 Frisquet S.A.

- 6.4.17 Viessmann Climate Solutions SE

- 6.4.18 Stiebel Eltron GmbH and Co. KG

- 6.4.19 Glen Dimplex Thermal Solutions

- 6.4.20 Aermec S.p.A.

- 6.4.21 Hoval Group

- 6.4.22 Baxi Heating, BDR Thermea

- 6.4.23 Wolf GmbH

- 6.4.24 Ariston Thermo Group

- 6.4.25 Panasonic Corporation

- 6.4.26 Mitsubishi Electric Corporation

- 6.4.27 Hitachi Air Conditioning

- 6.4.28 ETT, Energie Transfert Thermique

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment