|

시장보고서

상품코드

2061812

시어버터 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Shea Butter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

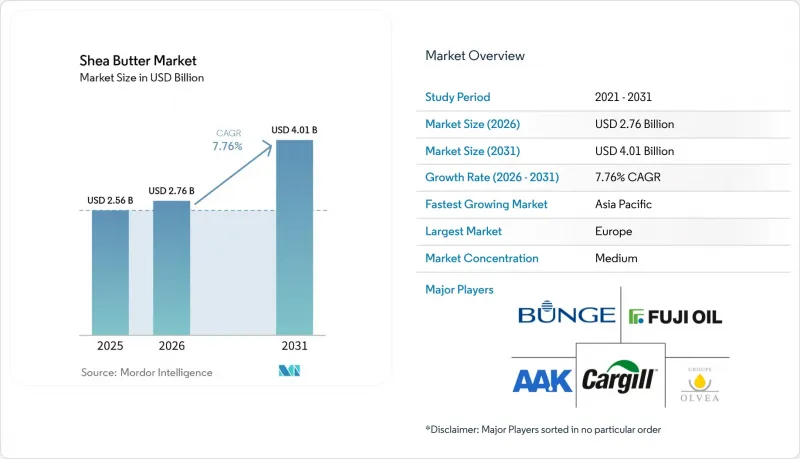

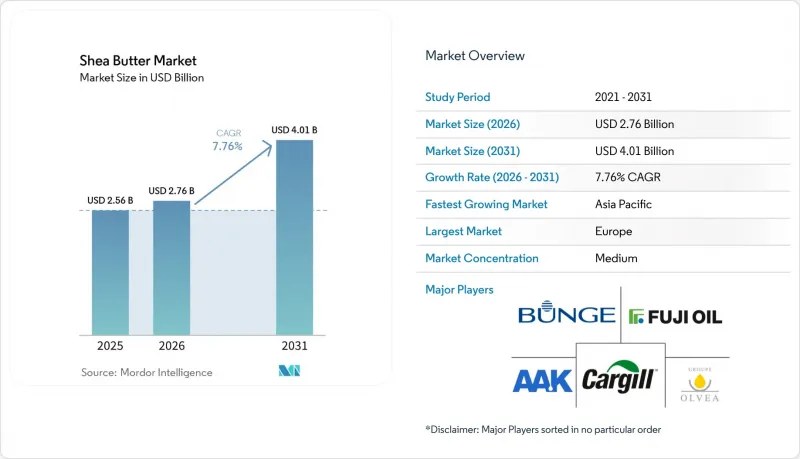

Mordor Intelligence에 의하면, 시어버터 시장 규모는 2025년 25억 6,000만 달러로 평가되었습니다. 2026년 27억 6,000만 달러에서 2031년까지 40억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR은 7.76%를 나타낼 것으로 예측됩니다.

본 보고서는 원료 유형(생·미정제, 정제, 분획), 용도(퍼스널케어 및 화장품, 식품 및 음료, 의약품·영양보조식품, 산업용) 및 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 및 수량(톤)으로 제시되어 있습니다.

세계의 시어버터 시장 동향과 분석

클린 라벨, 유기농, 식물 유래 퍼스널케어 원료에 대한 수요 증가

클린 라벨, 유기농, 식물 유래 퍼스널케어 원료에 대한 소비자 수요가 제품 개발 전략을 재편하고 있으며, 시어버터는 스킨케어 및 헤어케어 제품의 배합에서 중요한 성분으로 부상하고 있습니다. 투명성과 천연 유래 성분에 대한 선호도가 높아짐에 따라, 각 브랜드는 합성 화학 물질을 클린 라벨의 기대에 부응하는 시어버터와 같이 최소한의 가공만 거친 대체 성분으로 대체하고 있습니다. 또한, 식물 유래라는 특성은 확대되고 있는 비건 및 크루얼티 프리 뷰티 트렌드와도 부합하며, 프리미엄 제품부터 대중 시장 제품에 이르기까지 폭넓은 제품 라인에서 활용도가 높은 원료로 자리 잡고 있습니다. 2024년 미국위생재단(NSF)의 데이터에 따르면, 소비자의 74%가 퍼스널케어 제품에서 유기농 원료를 중요하게 여겼으며, 이는 소비자의 선호도가 원료 조달 및 배합 결정에 미치는 영향이 얼마나 큰지를 여실히 보여주었습니다. 이러한 추세를 반영하여, 각 제조업체들은 추적 가능성과 윤리적 조달, 특히 시어버터 생산이 집중된 서아프리카공급망에서의 조달을 중시하고 있습니다. AAK AB나 Ghana Nuts Company Limited와 같은 공급업체들은 변화하는 시장 수요에 부응하기 위해, 인증받은 유기농 및 공정무역 시어버터를 제품 라인업에 추가하는 방식으로 대응하고 있습니다. 또한, 클린 뷰티 트렌드, 지속가능성에 대한 요구, 규제 압력 등의 요인이 맞물리면서 다기능 천연 성분의 사용이 확대되고 있으며, 시어버터의 보습 효과와 피부 장벽 회복 작용이 부가가치를 창출하고 있습니다. 인디 브랜드와 D2C(Direct-to-Consumer) 브랜드들은 경쟁 우위로서 ‘클린 라벨’을 내세워 수요를 더욱 확대하고 있으며, 이는 전 세계 퍼스널케어 시장에서 시어버터의 입지를 확고히 하고 있습니다.

미국 및 유럽연합 내 식품 용도 확대를 뒷받침하는 GRAS/FDA 승인

미국과 유럽연합에서 최근 이루어진 규제 승인은 오랫동안 지속되어 온 규제상의 과제를 해결함으로써 식품 제조 분야에서 시어버터의 사용에 큰 영향을 미치고 있습니다. 미국 FDA가 시아올레인(GRN 850, 2020년) 및 시아스테아린(GRN 1116, 2024년)에 대해 ‘일반적으로 안전하다고 인정되는(GRAS)’ 인증을 부여함에 따라, 이를 구운 과자, 과자 코팅, 유제품 대체품 등의 제품에 배합할 수 있게 되었으며, 총 지방 함량의 최소 10%까지 사용이 허용되고 있습니다. 이러한 추세는 특히 코코아 가격 변동 및 공급 제약에 대응하기 위해 식품 업계가 코코아 버터를 대체할 수 있는 비용 효율이 높으면서 기능적으로 동등한 대체재를 모색하고 있는 움직임과 일치합니다. 마찬가지로, 유럽식품안전청(EFSA)이 규정(EC) No 258/97에 따라 실시한 2024년 재평가에서는 시어버터의 안전성이 재확인되었으며, 그 적용 범위가 유아용 조제분유 및 의료용 영양식품 등 규제가 엄격한 분야로까지 확대되었습니다. 이러한 발전은 제조업체 간의 신뢰를 높이고, 기호식품 및 기능성 식품 분야 전반에 걸쳐 시아를 주성분으로 하는 배합에 대한 연구 개발 투자를 촉진하고 있습니다. Bunge Loders Croklaan 등공급업체들은 증가하는 수요에 대응하기 위해 시아 원료 포트폴리오를 확대했습니다. 한편, 미국과 EU 간의 규제 조화를 통해 국경을 넘는 무역이 원활해지고 있으며, 다국적 제조업체를 위한 기준이 점차 통일되고 있습니다. 추적 가능성과 품질 보증 요건의 강화는 표준화되고 규제를 준수하는 공급망을 더욱 촉진하고 있으며, 시어버터는 식품 산업에서 활용도가 높고 규제의 검증을 받은 원료로서의 입지를 확고히 하고 있습니다.

기후와 계절에 따라 달라지는 시아넛 공급의 변동성

시어버터 시장은 기후 및 계절적 요인에 크게 좌우되는 시어 너트공급 변동으로 인해 중대한 과제에 직면해 있습니다. 생산은 주로 서아프리카의 야생 시어 나무에 의존하고 있으며, 관리된 재배의 가능성은 제한적입니다. 불규칙한 강우 패턴, 장기화되는 가뭄, 계절적인 수확 주기가 견과류 수확량에 직접적인 영향을 미치며, 원자재 공급량과 가격 변동을 초래하고 있습니다. 정책상의 혼란이 이러한 문제들을 더욱 악화시키고 있습니다. 그 예로, 2026년 2월에 발표된 나이지리아의 1년간 수출 금지 조치가 2027년 2월까지 연장된 것을 들 수 있습니다. 아프리카 무역회의소(African Trade Chamber)에 따르면, 이로 인해 연간 약 35만-50만 톤의 견과류 공급이 차질을 빚게 되며, 이는 세계 생산량의 40%에 가까운 규모입니다. 이러한 공급 감소로 인해, 국제 바이어들은 가나, 부르키나파소, 코트디부아르 등의 국가에서 대체 공급원을 찾아야만 하는 상황에 처해 있습니다. 이들 국가에서는 2024년부터 2025년에 걸친 수출 규제로 인해 이미 공급이 부족해져, 조달에 있어 추가적인 어려움이 발생하고 있습니다. 대규모 식품 및 개인 위생 용품 생산에 안정적인 공급량에 의존하고 있는 제조업체들은 원자재 비용의 변동성 확대와 공급망의 불확실성에 직면해 있습니다. 기업들은 이러한 과제에 대응하기 위해 조달 전략의 다각화와 산지별 파트너십 구축을 추진하고 있지만, 이러한 전환에는 물류상의 복잡성과 시간이 소요됩니다. IOI Loders Croklaan과 같은 B2B 기업들은 지역적 위험을 완화하기 위해 다원산지 조달 네트워크를 확대하고 있지만, 기후 변화에 취약하고 지리적으로 집중된 생산에 대한 의존도가 이러한 전략의 효과를 계속해서 제한하고 있으며, 이는 장기적인 가격 책정 및 재고 계획에 영향을 미치고 있습니다.

부문별 분석

2025년 기준으로 생·비정제 시어버터가 시장 점유율 1위를 차지하며 매출의 58.13%를 차지했습니다. 이러한 우위는 프리미엄 천연·유기농 화장품 분야에서 여전히 중요한 위치를 차지하고 있는 전통적이고 장인 정신이 깃든 사용 기반에서 비롯됩니다. 비정제 시어버터는 정제 제품의 불비누화물 함량이 3-5%인 데 비해 최대 17%라는 높은 함량을 가지고 있으며, 이는 생물학적 활성과 최소한의 가공이라는 주장을 뒷받침하여 천연 및 유기농 성분을 선호하는 소비자들에게 어필하고 있습니다. 한편, 정제 시어버터는 표준화된 색상, 향, 지방산 구성을 저비용으로 중시하는 중견 화장품 및 퍼스널케어 브랜드를 대상으로 계속해서 공급되고 있습니다. 이 부문은 기본적인 안전성 및 유효성 기준을 충족하는 비용 효율적인 처방이 높은 수요를 보이고 있는 아시아태평양 시장 수요 증가에 힘입어 특히 큰 혜택을 보고 있습니다.

스테아린산 및 올레산과 같은 분획 시어버터 유도체는 가장 빠르게 성장하는 부문으로 부상하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.44%로 확대될 것으로 전망됩니다. 산업용 구매자들은 식품 및 화장품 분야의 용도 수요 변화에 대응하기 위해, 정확한 용해 프로파일, 안정성 향상, 그리고 배합의 일관성을 이유로 이러한 유도체로의 전환을 가속화하고 있습니다. 2024년 AAK AB가 시아스테아린에 대해 획득한 GRAS 승인(GRN 1116)과 같은 규제 측면의 진전과, 초콜릿의 유통기한을 연장하는 Bunge Limited의 ‘Coberine 206’과 같은 제품 혁신이 이러한 전환을 더욱 가속화하고 있습니다. 이러한 발전 덕분에, 분획 시어버터 유도체는 산업용도로 활용 가능성이 높고 고성능인 솔루션으로서의 입지를 확고히 하는 동시에, 다양한 최종 용도 분야에 걸쳐 타겟을 명확히 한 제품 개발을 가능하게 하고 있습니다.

지역별 분석

유럽은 세계 시어버터 시장에서 가장 큰 점유율을 차지하고 있으며, 2025년 수요의 33.91%를 차지했습니다. 이러한 우위는 추적성과 지속가능성을 우선시하는 엄격한 규제 체계에서 비롯된 것입니다. 2024년 12월에 발효된 EU의 산림 파괴 규제 및 정책, 그리고 기업의 지속가능성 실사 지침 등의 조치에 따라, 수입업체는 구획 단위의 추적 가능성 및 산림 파괴가 없는 조달처 검증 등을 포함하여 공급망의 완전한 투명성을 확보해야 할 의무가 있습니다. 이러한 조치들은 특히 고급 퍼스널케어 및 화장품 분야에서 윤리적이고 친환경적인 제품을 원하는 소비자들 수요 증가와 부합합니다. 독일, 프랑스, 영국이 수입을 주도하고 있으며, 그 배경에는 고품질 제품 개발을 위해 인증된 시어버터에 의존하는 로레알, 바이엘스도르프, 클라랑스 같은 다국적 화장품 기업들의 존재가 있습니다. 또한, 이탈리아와 스페인은 시어버터를 원료로 하는 식품 분야에서 주요 주자로 부상하고 있으며, 규제 당국의 승인을 바탕으로 클린 라벨 기준을 충족하는 과자 및 제과 제품에 시어 스테아린을 배합하고 있습니다. 반면 러시아에서는 소비자들의 인지도가 낮고, 고급 천연 유래 퍼스널케어 제품의 보급률도 낮아 수요가 미미한 임베디드니다.

아시아태평양은 가장 빠르게 성장하는 시장으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 7.76%로 확대될 것으로 전망됩니다. 이러한 성장은 가처분 소득 증가와 클린 뷰티 및 기능성 성분의 채택 확대에 힘입어 이루어지고 있습니다. 중국과 인도에서는 식물 유래 및 천연 개인 위생 용품 시장이 꾸준한 성장세를 보이고 있습니다. 이는 식품 용도를 확대한 중국에서 2021년 시아 오일이 함유된 코코아 버터 대체품이 승인되는 등 규제 측면의 진전에 힘입은 결과입니다. 또한, 특수 유지 분야에서의 혁신도 이러한 추세를 뒷받침하고 있으며, Bunge Limited와 같은 기업들은 온난한 기후 조건에서 초콜릿의 안정성과 관련된 문제를 해결하기 위해 ‘Coberine 206’과 같은 제품을 도입하고 있습니다. 일본과 한국은 영양보조식품 시장, 특히 관절 건강을 지원하는 시아 비비누화물 보충제 분야의 틈새 시장으로 부상하고 있습니다. 호주에서는 클린 라벨 및 윤리적으로 조달된 화장품에 대한 수요가 시장을 주도하고 있으며, 소매업체들은 환경에 대한 의식이 높은 소비자들의 공감을 얻기 위해 공정무역 및 지속가능성 인증을 강조하고 있습니다.

북미는 유리한 규제 환경과 클린 라벨 및 식물 유래 제품에 대한 소비자의 높은 선호도에 힘입어 중요한 시장으로 자리매김하고 있습니다. 미국 식품의약국(FDA)이 시아올레인과 스테아린에 대해 GRAS(일반적으로 안전하다고 인정되는 물질) 승인을 내림에 따라, 이들의 용도는 제과, 제빵, 유제품 대체품 분야로 확대되고 있습니다. 지역별로는 미국이 소비를 주도하고 있으며, 각 브랜드는 추적 가능성과 윤리적 조달에 점점 더 주력하고 있고, AAK AB의 ‘Kolo Nafaso’ 프로그램과 같은 체계적인 공급망과의 협력도 확대되고 있습니다. 캐나다와 멕시코는 시장 규모는 작지만, 천연 화장품이나 지속가능성을 중시하는 제품 라인에서 꾸준한 성장이 나타나고 있습니다. 남미에서는 브라질과 아르헨티나가 점차 고급 퍼스널케어 제품을 도입하고 있지만, 수입 비용이나 낮은 인지도와 같은 과제는 여전히 남아 있습니다. 중동 및 아프리카에서는 남아프리카공화국과 아랍에미리트(UAE) 등 시장이 식품 및 화장품용 정제 시어버터의 주요 수입국으로 자리 잡고 있습니다. 가나, 부르키나파소, 나이지리아, 말리, 코트디부아르 등의 생산국들은 현지 산업의 참여 강화를 목적으로 한 수출 규제와 개발 금융 이니셔티브의 지원을 받아, 부가가치가 높은 가공에 점점 더 주력하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.19According to Mordor Intelligence, the shea butter market size is projected to expand from USD 2.56 billion in 2025 and USD 2.76 billion in 2026 to USD 4.01 billion by 2031, registering a 7.76% CAGR between 2026 and 2031.

This report is Segmented by Ingredient Type (Raw/Unrefined, Refined, Fractionated), Application (Personal-Care and Cosmetics, Food and Beverage, Pharmaceuticals and Nutraceuticals, Industrial), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Shea Butter Market Trends and Insights

Rising demand for clean-label, organic, and plant-based personal care ingredients

Consumer demand for clean-label, organic, and plant-based personal care ingredients is reshaping product development strategies, with shea butter emerging as a key component in skincare and haircare formulations. The growing preference for transparency and naturally derived ingredients is driving brands to replace synthetic chemicals with minimally processed alternatives like shea butter, which aligns with clean-label expectations. Its plant-based origin also supports the expanding vegan and cruelty-free beauty movement, making it a versatile ingredient across premium and mass-market product lines. Data from the National Sanitation Foundation in 2024 indicates that 74% of consumers prioritize organic ingredients in personal care products, underscoring the impact of consumer preferences on procurement and formulation decisions . This trend has led manufacturers to emphasize traceability and ethical sourcing, particularly from West African supply chains, where shea butter production is concentrated. Suppliers such as AAK AB and Ghana Nuts Company Limited are responding by enhancing their portfolios with certified organic and fair-trade shea butter to meet evolving market demands. Additionally, the convergence of clean beauty trends, sustainability requirements, and regulatory pressures is driving the adoption of multifunctional natural ingredients, with shea butter's moisturizing and skin barrier-repair properties offering added value. Indie and direct-to-consumer brands are further amplifying demand by leveraging clean-label claims as a competitive advantage, solidifying shea butter's role in the global personal care market.

GRAS/FDA approvals supporting broader food applications in the United States and European Union

Recent regulatory approvals in the United States and European Union are significantly influencing the adoption of shea butter in food manufacturing by addressing long-standing regulatory challenges. The U.S. FDA's Generally Recognized as Safe (GRAS) determinations for shea olein (GRN 850, 2020) and shea stearin (GRN 1116, 2024) have enabled their inclusion in products such as baked goods, confectionery coatings, and dairy alternatives, with usage levels permitted up to a minimum 10% of total fat content . This development aligns with the food industry's pursuit of cost-efficient and functionally comparable alternatives to cocoa butter, particularly in response to volatile cocoa prices and supply constraints. Similarly, the European Food Safety Authority's 2024 re-evaluation under Regulation (EC) No 258/97 has reaffirmed the safety of shea butter and extended its application to high-regulation categories, including infant formula and medical nutrition. These advancements are fostering confidence among manufacturers and driving investments in research and development for shea-based formulations across indulgent and functional food categories. Suppliers such as Bunge Loders Croklaan expanded their shea ingredient portfolios to meet growing demand, while regulatory alignment between the U.S. and EU is facilitating smoother cross-border trade and harmonizing standards for multinational producers. Enhanced traceability and quality assurance requirements are further encouraging standardized and compliant supply chains, positioning shea butter as a versatile and regulation-backed ingredient in the food industry.

Volatility in shea nut supply due to climatic and seasonal dependencies

The shea butter market faces significant challenges due to the volatility in shea nut supply, which is heavily influenced by climatic and seasonal factors. Production depends largely on wild-grown shea trees in West Africa, with limited potential for controlled cultivation. Irregular rainfall patterns, prolonged dry periods, and seasonal harvesting cycles directly impact nut yields, causing fluctuations in raw material availability and pricing. Policy disruptions further compound these issues, as demonstrated by Nigeria's extension of its one-year export ban through February 2027, announced in February 2026, which removed an estimated 350,000-500,000 tonnes of annual nut supply, nearly 40% of global output, as per the African Trade Chamber. This supply contraction has forced international buyers to seek alternative sources in countries like Ghana, Burkina Faso, and Cote d'Ivoire, where prior export restrictions in 2024-2025 had already tightened supply, creating additional procurement challenges. Manufacturers reliant on consistent volumes for large-scale food and personal care production are grappling with increased input cost volatility and supply chain uncertainty. Companies are diversifying sourcing strategies and forming origin-specific partnerships to address these challenges, though such transitions involve logistical complexities and time. B2B players like IOI Loders Croklaan are expanding multi-origin sourcing networks to mitigate regional risks, but the reliance on climate-sensitive and geographically concentrated production continues to limit the effectiveness of these strategies, impacting long-term pricing and inventory planning.

Other drivers and restraints analyzed in the detailed report include:

- Growing consumer awareness of therapeutic and nutritional benefits

- Increasing preference for sustainably sourced and fair-trade ingredients

- Quality inconsistency and adulteration risks in unrefined supply chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Raw/unrefined shea butter accounted for the largest share of the market in 2025, contributing 58.13% of revenue. Its dominance is attributed to its traditional and artisanal usage base, which remains significant in premium natural and organic cosmetics. The high unsaponifiable content of raw shea butter, up to 17% compared to 3-5% in refined variants, supports claims of bioactivity and minimal processing, appealing to consumers seeking natural and organic formulations. At the same time, refined shea butter continues to serve mid-tier cosmetic and personal care brands that prioritize standardized color, odor, and fatty acid composition at a lower cost. This segment is particularly benefiting from rising demand in Asia-Pacific markets, where cost-effective formulations that meet baseline safety and efficacy standards are in high demand.

Fractionated shea butter derivatives, such as stearin and olein, are emerging as the fastest-growing segment, projected to expand at a CAGR of 8.44% from 2026 to 2031. Industrial buyers are increasingly shifting toward these derivatives due to their precise melting profiles, improved stability, and formulation consistency, which align with evolving application needs in food and cosmetics. Regulatory developments, such as AAK AB's GRAS approval (GRN 1116) for shea stearin in 2024, and product innovations like Bunge Limited's Coberine 206, which extends chocolate shelf life, are further accelerating this transition. These advancements position fractionated shea derivatives as scalable, high-performance solutions for industrial applications, while enabling targeted product development across diverse end-use categories.

Geography Analysis

Europe holds the largest share of the global shea butter market, accounting for 33.91% of demand in 2025. This dominance is attributed to stringent regulatory frameworks that prioritize traceability and sustainability. Policies such as the EU Deforestation Regulation and the Corporate Sustainability Due Diligence Directive, effective December 2024, mandate importers to ensure full supply chain transparency, including plot-level traceability and verification of deforestation-free sourcing. These measures align with growing consumer demand for ethical and environmentally responsible products, particularly in premium personal care and cosmetics. Germany, France, and the United Kingdom lead imports, driven by multinational cosmetic companies like L'Oreal, Beiersdorf, and Clarins, which rely on certified shea butter for high-quality formulations. Additionally, Italy and Spain are emerging as key players in shea-based food applications, leveraging regulatory approvals to incorporate shea stearin into confectionery and bakery products that meet clean-label standards. Conversely, Russia shows modest demand due to limited consumer awareness and lower penetration of premium natural personal care products.

The Asia-Pacific region is the fastest-growing market, projected to expand at a CAGR of 7.76% from 2026 to 2031. This growth is fueled by rising disposable incomes and increasing adoption of clean beauty and functional ingredients. China and India are experiencing robust growth in plant-based and natural personal care products, supported by regulatory developments such as China's 2021 approval of cocoa butter equivalents containing shea, which has broadened food applications. Innovation in specialty fats is also driving adoption, with companies like Bunge Limited introducing products such as Coberine 206 to address challenges in chocolate stability under warm climatic conditions. Japan and South Korea are emerging as niche markets for nutraceutical applications, particularly shea unsaponifiable supplements for joint health. In Australia, demand is driven by clean-label and ethically sourced cosmetics, with retailers emphasizing fair-trade and sustainability certifications that resonate with environmentally conscious consumers.

North America represents a significant market, supported by favorable regulatory frameworks and strong consumer preference for clean-label and plant-based products. The U.S. Food and Drug Administration's GRAS approvals for shea olein and stearin have expanded their use across confectionery, bakery, and dairy-alternative segments. The United States leads regional consumption, with brands increasingly focusing on traceability and ethical sourcing, often collaborating with structured supply chains such as AAK AB's Kolo Nafaso program. Canada and Mexico, while smaller markets, are witnessing steady growth in natural cosmetics and sustainability-driven product lines. In South America, Brazil and Argentina are gradually adopting premium personal care products, though challenges such as import costs and limited awareness persist. In the Middle East and Africa, markets like South Africa and the United Arab Emirates are key importers of refined shea for food and cosmetics. Producing nations, including Ghana, Burkina Faso, Nigeria, Mali, and Cote d'Ivoire, are increasingly focusing on value-added processing, supported by export restrictions and development finance initiatives aimed at strengthening local industry participation.

- AAK AB

- Bunge Global SA

- Cargill, Incorporated

- Olvea Group

- Savannah Fruits Company

- BASF SE

- Ghana Nuts Company Ltd.

- Fuji Oil Holdings

- Gombella Integrated Services

- Manorama Industries Ltd.

- All Organic Treasures GmbH

- Shea Radiance LLC

- SOPHIM

- Suru Chemicals & Pharmaceuticals Pvt. Ltd.

- Croda International Plc

- Natural Sourcing, LLC

- Bulk Apothecary

- Right Shea

- Hallstar (Biochemica)

- Clariant AG

- DDW The Color House (GNT Group)

- Synthite Industries Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for clean-label, organic, and plant-based personal care ingredients

- 4.2.2 Expanding application as a functional lipid and cocoa butter alternative in food formulations

- 4.2.3 GRAS/FDA approvals supporting broader food applications in the United States and European Union

- 4.2.4 Growing consumer awareness of therapeutic and nutritional benefits

- 4.2.5 Increasing preference for sustainably sourced and fair-trade ingredients

- 4.2.6 Advancements in processing technologies improving yield and quality consistency

- 4.3 Market Restraints

- 4.3.1 Volatility in shea nut supply due to climatic and seasonal dependencies

- 4.3.2 Quality inconsistency and adulteration risks in unrefined supply chains

- 4.3.3 High price sensitivity among industrial and B2B buyers

- 4.3.4 Intense competition from alternative natural butters and oils

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Ingredient Type

- 5.1.1 Raw/Unrefined

- 5.1.2 Refined

- 5.1.3 Fractionated (stearin, olein)

- 5.2 By Application

- 5.2.1 Personal-Care and Cosmetics

- 5.2.2 Food and Beverage

- 5.2.3 Pharmaceuticals and Nutraceuticals

- 5.2.4 Industrial (bio-lubes, candles, etc.)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AAK AB

- 6.4.2 Bunge Global SA

- 6.4.3 Cargill, Incorporated

- 6.4.4 Olvea Group

- 6.4.5 Savannah Fruits Company

- 6.4.6 BASF SE

- 6.4.7 Ghana Nuts Company Ltd.

- 6.4.8 Fuji Oil Holdings

- 6.4.9 Gombella Integrated Services

- 6.4.10 Manorama Industries Ltd.

- 6.4.11 All Organic Treasures GmbH

- 6.4.12 Shea Radiance LLC

- 6.4.13 SOPHIM

- 6.4.14 Suru Chemicals & Pharmaceuticals Pvt. Ltd.

- 6.4.15 Croda International Plc

- 6.4.16 Natural Sourcing, LLC

- 6.4.17 Bulk Apothecary

- 6.4.18 Right Shea

- 6.4.19 Hallstar (Biochemica)

- 6.4.20 Clariant AG

- 6.4.21 DDW The Color House (GNT Group)

- 6.4.22 Synthite Industries Pvt. Ltd.