|

시장보고서

상품코드

2061838

당뇨병성 신증 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Diabetic Nephropathy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

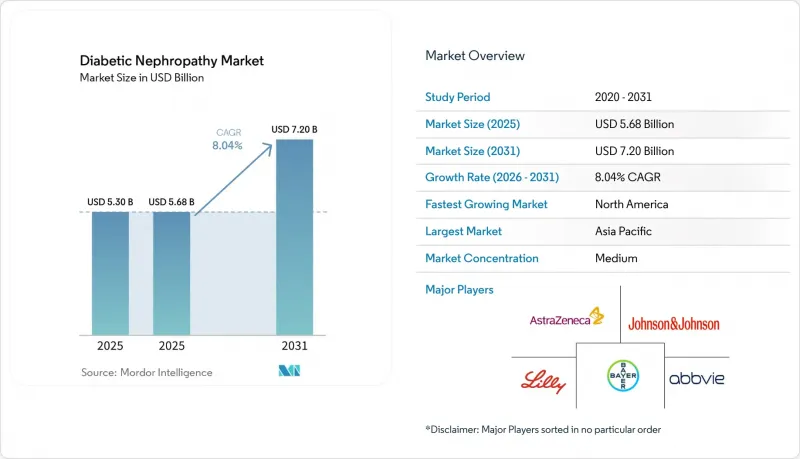

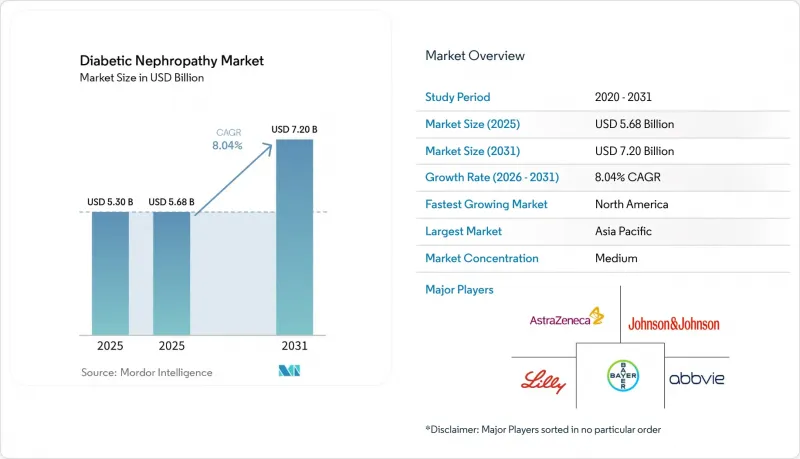

Mordor Intelligence에 의하면, 당뇨병성 신증 시장 규모는 2025년 53억 달러에서 2025년에는 56억 8,000만 달러로 확대되어 2031년까지 72억 달러에 이를 것으로 예측되며, 2025년부터 2031년에 걸쳐 CAGR은 8.04%를 나타낼 전망입니다.

본 보고서는 제품 유형(치료제, 진단제), 질환 진행 단계(고여과, 미량 알부민뇨, 다량 알부민뇨, CKD 3-4기, ESRD), 최종 사용자(병원, 전문 클리닉, 투석 센터, 진단실험실, 학술 기관), 투여 경로(경구, 주사), 지역(북미, 유럽, 아시아태평양, 기타)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 당뇨병성 신증 시장 동향 및 인사이트

전 세계 당뇨병 유병률 증가

2024년, 전 세계 당뇨병 환자 수는 성인 5억 8,900만 명에 달했으며, 2021년 대비 16% 증가했습니다. 이 중 90%가 2형 당뇨병이며, 환자의 20-40%는 진단 후 10년 이내에 당뇨병성 신증을 발병합니다. 이러한 증가는 특정 지역에 집중되어 있으며, 중국과 인도에서만 총 2억 4,100만 명의 당뇨병 환자가 있습니다. 그러나 이들 국가의 농촌 지역에서는 알부민뇨 선별 검사 실시율이 30% 미만에 그치고 있으며, 국민건강보험을 통한 UACR 검사 및 SGLT-2 억제제의 적용 범위가 확대됨에 따라 더욱 커질 것으로 예상되는 막대한 미충족 수요가 부각되고 있습니다. 중동 및 북아프리카에서는 비만이나 앉아 있는 시간이 많은 생활 습관 등의 요인으로 인해, 걸프협력회의(GCC) 회원국들의 당뇨병 유병률이 20%를 초과하고 있습니다. 그러나 이 지역들의 의료 시스템은 바이오마커 검사 측면에서 어려움을 겪고 있으며, 대부분의 경우 혈청 크레아티닌 수치에 의존하고 있는데, 이는 초기 신장 손상을 발견하기에는 불충분합니다. 이러한 시장의 성장은 규제적 개입보다는 주로 역학적 동향에 의해 주도되고 있습니다.

고령화가 진행되면서 만성 신증(CKD)으로 인한 부담이 커지고 있습니다.

세계 65세 이상 인구는 2024년 7억 7,100만 명에서 2050년까지 16억 명으로 증가할 것으로 예측됩니다. 일본, 이탈리아, 독일 등에서는 이미 연령 중앙값이 47세를 넘어섰습니다. 노화에 따른 네프론 손실은 당뇨병의 영향을 증폭시키며, 당뇨병이 없는 사람도 40세 이후부터 10년마다 사구체의 약 10%를 잃게 됩니다. 고혈압을 동반한 당뇨병 환자의 경우, 네프론 손실이 더욱 심해지며, 같은 기간 동안 기능 용량이 30-50% 감소합니다. 이러한 인구 동향은 특히 북미와 유럽에서 두드러지게 나타나며, 이들 지역의 의료 시스템에서는 고령 당뇨병 환자를 대상으로 연 1회 eGFR 모니터링을 통해 조기 발견이 일상적인 진료 과정에 포함되어 있습니다. 반면, 아시아·태평양 지역 국가들에서는 한국이나 태국 등지에서 급속한 고령화가 진행되는 한편, 만성질환 관리 시스템이 미비하다는 과제에 직면해 있습니다. 이로 인해 중앙 검사실에서의 지연을 피할 수 있는 현장 진단형 UACR 기기에 대한 수요가 발생하고 있습니다. 또한, ISO 15189와 같은 규정 준수 체계가 해당 지역에서 점차 확산되고 있어, 진단 품질 기준이 확보되고 있습니다.

성과 연계형 신장 관리 모델

2024년, CMS는 ‘종합적 신장 치료 계약(CKCC)’ 이니셔티브를 도입했으며, 재정적 위험을 감수한 4,200명의 신장 전문의가 참여했습니다. 투석률이 벤치마크를 초과할 경우, 의료 제공업체는 정액 지급액의 최대 5%에 해당하는 벌금을 부과받지만, 기준을 상회할 경우에는 공동 절감분을 얻을 수 있습니다. 2024년 초의 데이터에 따르면, CKCC 참가자들은 ESRD(말기 신부전)의 진행을 늦추기 위한 인센티브에 힘입어, 사용량 기반 보상 모델과 비교했을 때 SGLT-2 억제제 처방량을 31%, UACR 검사를 18% 증가시켰습니다. 호주에서는 Kidney Health Australia가 유사한 개혁을 제안하고 있지만, 주별로 자금 조달 체계가 분산되어 있어 시행이 지연되고 있습니다. 성과 연계형 보상 모델에서는 복약 순응도 모니터링이 용이하고 비용도 저렴하기 때문에 SGLT-2나 GLP-1 등의 경구약이 유리합니다. 반면, 엔도세린 길항제와 같이 철저한 안전성 감시가 필요한 정맥 내 투여 약물은 불리한 입장에 놓이게 됩니다. 가치 기반 의료를 준수하는 것이 경쟁 우위로 자리 잡고 있는 가운데, 각 기업은 CKCC의 성과에 부합하기 위해 조직 내에 실세계 데이터(REW) 팀을 구성하고 있습니다.

부문별 분석

2025년에는 고정 용량 복합제 형태의 경구용 SGLT-2 억제제 및 GLP-1 수용체 작용제의 도입에 힘입어, 치료제가 시장 점유율의 66.90%를 차지했습니다. 이러한 복합제는 복용 부담을 줄이면서 eGFR을 유지하는 것을 목적으로 합니다. 33.10%의 시장 점유율을 차지하는 진단약 시장은 2031년까지 연평균 성장률(CAGR) 8.15%로 성장하고 있으며, 시스타틴 C, NGAL, KIM-1 등의 바이오마커 패널의 상용화가 이를 뒷받침하고 있습니다. 이러한 기술들은 연구용 도구에서 임상 등급의 검사 방식으로 점차 전환되고 있습니다. 치료제 분야에서는 SGLT-2 억제제가 주류를 이루고 있으며, 2021년과 2023년에 각각 CKD(만성 신장병) 적응증으로 FDA 승인을 획득한 Farxiga 및 Jardiance 등의 제품이 시장을 주도하고 있습니다. GLP-1 수용체 작용제는 2025년 당뇨병성 신증에 대한 세마글루티드의 승인을 계기로 연평균 성장률(CAGR) 9.5%를 기록하며 가장 빠르게 성장하고 있는 부문입니다. 엔도세린 수용체 길항제와 칼슘 채널 차단제는 틈새 시장에서 역할을 하고 있지만, ACE 억제제와 ARB는 SGLT-2 억제제의 뛰어난 치료 성과로 인해 그 존재감이 점차 약해지고 있습니다. 다만, 비용을 중시하는 시장에서는 여전히 널리 사용되고 있습니다.

2025년에는 만성 신장병 3-4기가 시장 점유율의 42.35%를 차지했습니다. 이는 eGFR이 60 mL/min/1.73m² 미만으로 떨어진 후에 증상이 나타나 의료기관에서 검사를 받게 되는 진단 경향을 반영한 것입니다. 고여과 부문은 적극적인 선별 검사 및 치료를 장려하는 조기 개입 모델에 힘입어 연평균 성장률(CAGR) 9.40%로 가장 빠르게 성장하고 있습니다. 미량 알부민뇨(1기)와 다량 알부민뇨(2기)를 합치면 시장의 약 35%를 차지하며, 조기 선별 검사를 권장하는 지침에 힘입어 시장이 성장하고 있습니다. 말기 신증(5기)은 환자가 투석이나 이식으로 전환되기 때문에 시장 점유율은 작지만, ESRD 환자를 대상으로 한 진단 서비스는 여전히 중요한 수익원입니다.

지역별 분석

2025년, 북미는 시장 점유율의 39.67%를 차지했습니다. 이는 메디케어 파트 B에 따라 당뇨병성 신증에 대한 SGLT-2 억제제 및 GLP-1 작용제의 보험 적용을 시행하는 CMS(미국 의료보험 및 의료보조 서비스 센터)의 정책에 따른 것입니다. 이러한 정책들은 종합적 신장 관리 계약 모델과 결합되어 초기 단계에서의 개입을 지원하고 있습니다. 3,480만 명의 당뇨병 환자가 있는 미국에서는 37%가 신장 기능 장애를 보이고 있음에도 불구하고, 해당 환자 중 연간 1회 UACR 선별 검사를 받는 비율은 고작 48%에 불과하여 의료 서비스 제공에 큰 격차가 발생하고 있습니다. 의료 시스템에서는 전자 차트를 통한 알림이나 약사가 주도하는 아웃리치 활동을 통해 이러한 격차 해소에 힘쓰고 있습니다. 캐나다에서는 SGLT-2 억제제가 주 정부의 처방약 목록에 포함되어 있지만, 시스타틴 C와 같은 정교한 바이오마커에 대한 보험 적용은 여전히 일관성이 부족합니다. 이로 인해 온타리오주나 브리티시컬럼비아주와 같은 지역에서는 정밀 검사가 제공되는 반면, 지방에서는 혈청 크레아티닌 검사에 의존할 수밖에 없는 등 양극화된 진단 체계가 형성되고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2031년까지의 연평균 성장률(CAGR)은 8.50%로 예측됩니다. 이러한 성장은 중국 내 1억 4,000만 명의 당뇨병 환자(이 중 20%가 미세알부민뇨증을 보이고 있습니다)에 의해 주도되고 있습니다. SGLT-2 억제제를 각 주의 필수 의약품 목록에 포함하도록 의무화하는 국가 정책에 따라, 병원에서의 접근성이 보장되고, 대량 구매를 통한 50-70%의 가격 인하가 촉진되고 있습니다. 인도에서는 상황이 양극화되어 있습니다. 델리, 뭄바이, 방갈로르 등 주요 도시에 위치한 사립 병원에서는 첨단 바이오마커를 포함한 종합적인 당뇨병성 신증 치료를 제공합니다. 그러나 소규모 도시에 위치한 정부 산하 1차 보건 센터에서는 기본적인 UACR 검사조차 실시되지 않고 있어, 환자들은 자비로 진단을 받기 위해 민간 검사 기관을 찾아갈 수밖에 없는 실정입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the diabetic nephropathy market size is expected to increase from USD 5.30 billion in 2025 to USD 5.68 billion in 2025 and reach USD 7.20 billion by 2031, growing at a CAGR of 8.04% over 2025-2031.

This report is Segmented by Product Type (Therapeutics, Diagnostics), Stage of Disease (Hyperfiltration, Micro-Albuminuria, Macro-Albuminuria, CKD Stage 3-4, ESRD), End User (Hospitals, Specialty Clinics, Dialysis Centres, Diagnostic Laboratories, Academic Institutes), Route of Administration (Oral, Injectable), and Geography (North America, Europe, Asia-Pacific, and More). Market Forecasts are in Value (USD).

Global Diabetic Nephropathy Market Trends and Insights

Escalating Global Diabetes Prevalence

In 2024, the global diabetic population reached 589 million adults, marking a 16% increase compared to 2021. Type 2 diabetes represents 90% of these cases, with 20-40% of patients developing diabetic nephropathy within a decade of diagnosis. This growth is concentrated in specific regions, with China and India collectively accounting for 241 million diabetics. However, rural areas in these countries report less than 30% screening penetration for albuminuria, highlighting a significant unmet demand that is expected to grow as national health insurance expands coverage for UACR testing and SGLT-2 inhibitors. In the Middle East and North Africa, diabetes prevalence exceeds 20% in Gulf Cooperation Council nations, driven by factors such as obesity and sedentary lifestyles. However, healthcare systems in these regions face challenges in biomarker testing, often relying on serum creatinine, which is insufficient for detecting early-stage kidney damage. Growth in these markets is primarily driven by epidemiological trends rather than regulatory interventions.

Ageing Population Accelerating CKD Burden

The global population aged 65 and older is expected to grow from 771 million in 2024 to 1.6 billion by 2050. Countries such as Japan, Italy, and Germany already report median ages above 47 years. Age-related nephron loss compounds the impact of diabetes, with non-diabetic individuals losing approximately 10% of glomeruli per decade after age 40. Diabetics with hypertension experience even greater nephron loss, reducing functional capacity by 30-50% over the same period. This demographic trend is particularly evident in North America and Europe, where healthcare systems have integrated early detection into routine care through annual eGFR monitoring for older diabetic patients. In contrast, Asia-Pacific nations face challenges as rapidly aging populations in countries like South Korea and Thailand coincide with underdeveloped chronic disease management systems. This has created demand for point-of-care UACR devices that bypass centralized laboratory delays. Compliance frameworks such as ISO 15189 are gaining traction in the region, ensuring quality standards for diagnostics.

Pay-for-Performance Nephrology Care Models

In 2024, CMS introduced the Comprehensive Kidney Care Contracting (CKCC) initiative, engaging 4,200 nephrologists who accepted financial risk. Providers face penalties of up to 5% of capitated payments if dialysis rates exceed benchmarks, while outperformers gain shared savings. Early 2024 data shows CKCC participants increased SGLT-2 inhibitor prescriptions by 31% and UACR testing by 18% compared to fee-for-service models, driven by incentives to delay ESRD progression. In Australia, Kidney Health Australia is advocating for comparable reforms, though fragmented state-level funding has delayed implementation. Pay-for-performance models favor oral therapeutics like SGLT-2 and GLP-1 due to simpler adherence monitoring and lower costs, disadvantaging IV-administered drugs like endothelin antagonists that require intensive safety oversight. Compliance with value-based care is becoming a competitive edge, with companies embedding real-world evidence teams to align with CKCC outcomes.

Other drivers and restraints analyzed in the detailed report include:

- Guideline-Mandated Annual Microalbumin Testing

- Rise of Urinary Multi-Omics Biomarker Panels

- Low Physician Awareness in Primary Care

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, therapeutics captured 66.90% of the market share, driven by the adoption of oral SGLT-2 inhibitors and GLP-1 receptor agonists in fixed-dose combinations. These combinations aim to enhance eGFR preservation while reducing the pill burden. Diagnostics, with a 33.10% share, are growing at an 8.15% CAGR through 2031, supported by the commercialization of biomarker panels like Cystatin-C, NGAL, and KIM-1, transitioning from research tools to clinical-grade assays. Within therapeutics, SGLT-2 inhibitors dominate, led by products like Farxiga and Jardiance, which gained FDA approval for CKD indications in 2021 and 2023, respectively. GLP-1 receptor agonists are the fastest-growing segment, with a 9.5% CAGR, fueled by the approval of semaglutide for diabetic kidney disease in 2025. Endothelin receptor antagonists and calcium-channel blockers serve niche roles, while ACE inhibitors and ARBs are losing prominence due to the superior outcomes of SGLT-2 inhibitors, though they remain prevalent in cost-sensitive markets.

Chronic Kidney Disease Stages 3-4 accounted for 42.35% of the market share in 2025, reflecting the trend of diagnoses occurring after eGFR drops below 60 mL/min/1.73m2, when symptoms prompt medical evaluation. The hyperfiltration segment is the fastest-growing, with a 9.40% CAGR, driven by early intervention models that reward proactive screening and treatment. Microalbuminuria (Stage 1) and macroalbuminuria (Stage 2) together represent about 35% of the market, with growth supported by guidelines promoting earlier screenings. End-stage renal disease (Stage 5) holds a smaller share as patients transition to dialysis or transplantation, though diagnostic services for ESRD patients remain a significant revenue driver.

Geography Analysis

In 2025, North America accounted for 39.67% of the market share, driven by CMS policies that reimburse SGLT-2 inhibitors and GLP-1 agonists for diabetic kidney disease under Medicare Part B. These policies, combined with Comprehensive Kidney Care Contracting models, support early-stage interventions. The U.S., with 34.8 million diabetics, faces a significant gap in care as only 48% of eligible patients receive annual UACR screenings, despite 37% showing kidney impairment. Health systems are addressing this gap through electronic health record alerts and pharmacist-led outreach. In Canada, while SGLT-2 inhibitors are covered under provincial formularies, reimbursement for advanced biomarkers like Cystatin-C remains inconsistent. This creates a two-tier diagnostic system, with provinces like Ontario and British Columbia offering advanced testing, while rural areas rely on serum creatinine methods.

Asia-Pacific is the fastest-growing region, with an 8.50% CAGR projected through 2031. Growth is fueled by China's 140 million diabetics, 20% of whom exhibit microalbuminuria. National policies mandating the inclusion of SGLT-2 inhibitors in provincial essential medicine lists ensure hospital access and drive price reductions of 50-70% through volume-based procurement. In India, the landscape is fragmented. Private hospitals in major cities like Delhi, Mumbai, and Bangalore provide comprehensive diabetic nephropathy care, including advanced biomarkers. However, government primary health centers in smaller cities lack basic UACR testing, pushing patients to private laboratories for self-funded diagnostics.

- Abbott Laboratories

- Abbvie

- AstraZeneca

- Bayer

- Beckton Dickinson

- Boehringer Ingelheim

- Chinook Therapeutics

- Eli Lilly and Company

- Roche

- GlaxoSmithKline

- Johnson & Johnson (Janssen / Invokana)

- Kyowa Kirin

- Merck

- Novo Nordisk

- Ortho Clinical Diagnostics

- Pfizer

- Quest Diagnostics

- Randox Laboratories

- Reata Pharmaceuticals

- Sanofi

- Siemens Healthineers

- Sysmex

- Thermo Fisher Scientific

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Diabetes Prevalence

- 4.2.2 Ageing Population Accelerating CKD Burden

- 4.2.3 Guideline-Mandated Annual Microalbumin Testing

- 4.2.4 Rise of Urinary Multi-Omics Biomarker Panels

- 4.2.5 Pay-for-Performance Nephrology Care Models

- 4.3 Market Restraints

- 4.3.1 Low Physician Awareness in Primary Care

- 4.3.2 Adverse-Event Concerns with Endothelin Antagonists

- 4.3.3 Limited Reimbursement for Novel Biomarker Tests

- 4.3.4 AI Diagnostic Algorithms Facing Regulatory Delay

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Therapeutics

- 5.1.1.1 ACE Inhibitors

- 5.1.1.2 Angiotensin II Receptor Blockers (ARBs)

- 5.1.1.3 SGLT-2 Inhibitors

- 5.1.1.4 Endothelin Receptor Antagonists

- 5.1.1.5 GLP-1 Receptor Agonists

- 5.1.1.6 Calcium-Channel Blockers

- 5.1.1.7 Others

- 5.1.2 Diagnostics

- 5.1.2.1 Urine Albumin-to-Creatinine Ratio (UACR)

- 5.1.2.2 24-h Urine Albumin

- 5.1.2.3 Serum Creatinine

- 5.1.2.4 Estimated GFR (eGFR) Algorithms

- 5.1.2.5 Imaging (Ultrasound, MRI)

- 5.1.2.6 Novel Biomarkers (Cystatin-C, NGAL, KIM-1, etc.)

- 5.1.2.7 Others

- 5.1.1 Therapeutics

- 5.2 By Stage of Disease

- 5.2.1 Hyperfiltration (Pre-clinical)

- 5.2.2 Micro-albuminuria (Stage 1)

- 5.2.3 Macro-albuminuria (Stage 2)

- 5.2.4 Chronic Kidney Disease (Stage 3-4)

- 5.2.5 End-Stage Renal Disease (Stage 5)

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics

- 5.3.3 Dialysis Centres

- 5.3.4 Diagnostic Laboratories

- 5.3.5 Academic & Research Institutes

- 5.4 By Route of Administration (Therapeutics)

- 5.4.1 Oral

- 5.4.2 Injectable

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of MEA

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 AbbVie Inc.

- 6.3.3 AstraZeneca plc

- 6.3.4 Bayer AG

- 6.3.5 Beckman Coulter

- 6.3.6 Boehringer Ingelheim GmbH

- 6.3.7 Chinook Therapeutics

- 6.3.8 Eli Lilly and Company

- 6.3.9 F. Hoffmann-La Roche Ltd

- 6.3.10 GSK plc

- 6.3.11 Johnson & Johnson (Janssen / Invokana)

- 6.3.12 Kyowa Kirin

- 6.3.13 Merck KGaA

- 6.3.14 Novo Nordisk A/S

- 6.3.15 Ortho Clinical Diagnostics

- 6.3.16 Pfizer Inc.

- 6.3.17 Quest Diagnostics

- 6.3.18 Randox Laboratories

- 6.3.19 Reata Pharmaceuticals

- 6.3.20 Sanofi S.A.

- 6.3.21 Siemens Healthineers AG

- 6.3.22 Sysmex Corporation

- 6.3.23 Thermo Fisher Scientific Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment