|

시장보고서

상품코드

2063717

당뇨병성 신증 치료제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Diabetic Nephropathy Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

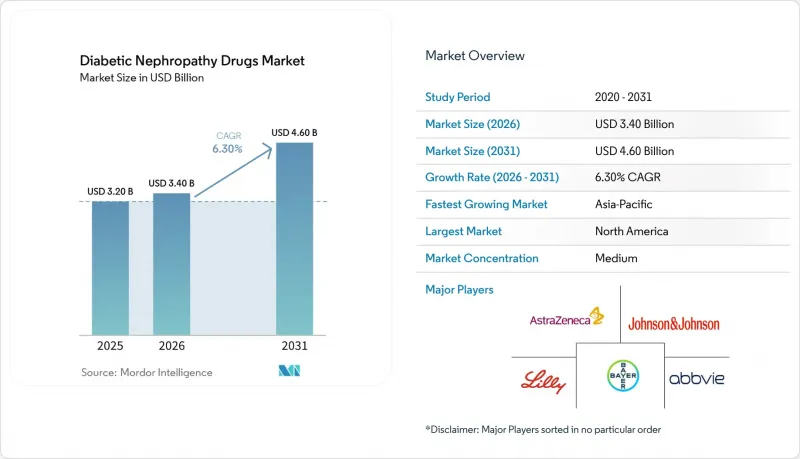

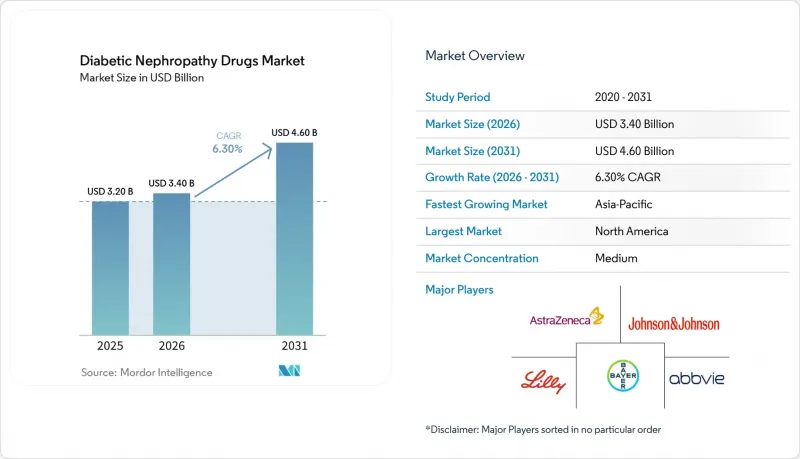

Mordor Intelligence에 의하면, 당뇨병성 신증 치료제 시장 규모는 2025년에 32억 달러, 2026년에 34억 달러, 2031년까지 46억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 6.30%로 성장할 것으로 전망됩니다.

본 보고서는 약물 분류별(ACE 억제제, 안지오텐신 II 수용체 길항제, SGLT2 억제제 등), 당뇨병 유형별(제1형, 제2형), 유통 채널(병원 약국, 소매/지역 약국, 온라인 약국), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 당뇨병성 신증 치료제 시장 동향 및 인사이트

당뇨병 유병률 증가와 고령화

당뇨병 유병률의 급증, 특히 2045년까지 아시아에서 2형 당뇨병이 68% 증가할 것으로 예상에 따라, 당뇨병성 신증 치료제 시장의 잠재 고객 기반이 확대되고 있습니다. BMI가 낮은 경우의 유전적 감수성은 신장 합병증을 가속화시키며, NGAL 및 KIM-1과 같은 바이오마커에 기반한 조기 선별 프로그램의 도입을 촉진하고 있습니다. 고령화는 추가적인 부담을 초래하고 있으며, 신장 기능의 자연스러운 저하로 인해 미량 알부민뇨에서 명백한 신증으로의 진행이 빨라지고 있습니다. 의료 제도에서는 예방 캠페인과 병행하여 전 인구를 대상으로 한 선별검사를 실시했습니다. 이러한 인구동학적 요인들이 서로 얽히면서, 당뇨병성 신증 치료제 시장의 장기적인 성장이 지속될 것으로 예측됩니다.

CREDENCE 및 EMPA-REG 임상시험 이후 SGLT2 억제제의 임상 도입

CREDENCE 및 EMPA-REG와 같은 획기적인 임상시험을 통해, 혈당 조절과는 별개로 신장 및 심혈관 보호 효과가 입증됨에 따라, SGLT2 억제제가 1차 선택 약물이 되도록 지침이 개정되었습니다. 실제 데이터에 따르면, SGLT2 억제제를 지속적으로 복용하는 환자의 경우 입원 중 병원 내 사망률이 45% 낮습니다. 최근 미국에서 만성 신증에 동반된 심부전에 대한 소타글리플로진의 승인이 이루어짐에 따라 적응증이 확대되었습니다. 그러나 적격 환자 중에서도 이러한 약물을 처방받는 경우는 극히 일부에 불과하여, 처방 격차는 여전히 존재하고 있습니다. 따라서 당뇨병성 신증 치료제 시장은 여전히 더 성장할 여지가 남아 있습니다. 의료비 총액 절감 효과에 대한 보험사의 인식이 높아지고 있는 만큼, 도입이 가속화될 것으로 기대됩니다.

신약(예: 피네레논)의 높은 정가

하루 약 19달러에 달하는 피네레논의 가격은 특히 예산 상한선이 있는 의료 제도 하에서 경제적 부담의 허용 범위를 한계에 몰아넣고 있습니다. 보험사는 단계별 치료 프로토콜을 적용함으로써, 최적의 치료에 도달하기까지의 과정을 길게 만들고, 도입 속도를 늦추고 있습니다. 평생에 걸친 치료는 급성 질환의 치료에 비해 누적 지출을 증가시킵니다. 2026년부터 시작되는 메디케어(미국 의료보험 제도)의 가격 협상에서는 기존의 당뇨병 치료제에 대해 대폭적인 가격 인하가 적용되지만, 신약은 이러한 협상의 대상에서 제외됩니다. 따라서 여러 가지 고가 약물을 병용하는 병용 요법의 경우 비용 부담이 커지고, 경제적 부담이 중첩되면서 당뇨병성 신증 치료제 시장의 단기적인 성장이 둔화될 것입니다.

부문별 분석

2025년 기준으로, ACE 억제제는 당뇨병성 신증 치료제 시장에서 33.1%라는 최대 점유율을 유지했습니다. 그러나 SGLT2 억제제는 비당뇨성 만성 신증 및 심부전 환자군으로의 적응증 확대를 배경으로, 2031년까지 연평균 성장률(CAGR) 12.5%를 기록하며 성장을 주도하고 있습니다. ACE 억제제가 금기인 경우, ARB는 1차 선택 약물의 대체제가 됩니다. 피네레논과 같은 MRA는 잔존하는 염증 및 섬유화를 치료함으로써, RAS 차단 요법에 내성을 보이는 단백뇨 환자들 사이에서 지지를 넓혀가고 있습니다. 이뇨제는 여전히 체액 관리에 중요한 역할을 하고 있는 반면, GLP-1 수용체 작용제 및 DPP-4 억제제는 부수적인 신장 효과를 통해 새롭게 부상한 ‘기타’라는 틈새 시장을 차지하고 있습니다.

CONFIDENCE 임상시험 데이터에 따르면, 피네레논과 엠파글리플로진의 병용 요법이 단일 요법보다 우수한 효과를 보였으며, 단일 요법 위주에서 요법 기반 치료로 전환될 것으로 예측됩니다. 또한, 아트라센탄이나 이프타코판과 같은 엔도세린 수용체 길항제 및 보체 억제제가 신속 승인을 획득함에 따라, 병용 요법을 중시하는 당뇨병성 신증 치료제 시장 규모는 확대될 것으로 예측됩니다. 임상의들이 다제 병용 프로토콜에 대한 이해를 깊게 함에 따라, 보험 적용 목록에 등재되는 사례가 늘어나면서 도입 속도가 가속화되고 있습니다.

지역별 분석

2025년, 북미는 당뇨병성 신증 치료제 시장의 37.4%를 차지하며 시장을 주도했습니다. 이는 성숙한 보험 제도, 광범위한 임상시험 네트워크, 그리고 동종 최초의 치료법의 급속한 보급에 힘입은 결과입니다. 메디케어의 ‘신장 관리 선택 모델’은 초기 단계의 관리를 장려하고 있으며, 이로 인해 처방량이 증가하고 있습니다. 기존 당뇨병 치료제에 대한 파트 D 68% 할인 혜택이 곧 시행됨에 따라, 절감된 자금이 새로운 신장 보호제로 재투자되어 수요를 더욱 공고히할 것으로 보입니다.

아시아태평양은 가장 성장세가 두드러지는 지역으로, 2031년까지 연평균 성장률(CAGR) 9.3%를 나타낼 것으로 전망됩니다. 아시아 2형 당뇨병 환자에서 미량 알부민뇨(39.8%) 및 다량 알부민뇨(18.8%)의 유병률은 공중보건상의 긴급 상황을 여실히 보여주고 있습니다. 각국 정부는 조기 검진에 자금을 지원하고 있으며, 보험 적용 범위의 확대는 고부가가치 치료법으로 가는 길을 열어주고 있습니다.

유럽에서는 국민건강보험 제도와 체계적인 의료 기술 평가를 통해 꾸준한 판매량을 유지하고 있습니다. 피네레논과 아트라센탄에 대한 EMA의 승인은 규제 당국이 혁신성과 안전성 사이에서 균형 잡힌 입장을 취하고 있음을 보여줍니다. 한편, 중동 및 아프리카 및 남미에서는 당뇨병 유병률 증가와 보험 지급 제도의 단계적 개혁을 배경으로 새로운 가능성이 보이지만, 가격에 대한 민감성이 단기적인 보급을 저해할 가능성이 있습니다. 이러한 지역별 동향이 복합적으로 작용하여, 당뇨병성 신증 치료제 시장에서 다양한 수요 구조를 형성하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the diabetic nephropathy drugs market size is projected to be USD 3.20 billion in 2025, USD 3.40 billion in 2026, and reach USD 4.60 billion by 2031, growing at a CAGR of 6.30% from 2026 to 2031.

This report is Segmented by Drug Class (ACE Inhibitors, Angiotensin II Receptor Blockers, SGLT2 Inhibitors, and More), Diabetes Type (Type-1, Type-2), Distribution Channel (Hospital Pharmacies, Retail/Community Pharmacies, Online Pharmacies), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Diabetic Nephropathy Drugs Market Trends and Insights

Rising Diabetes Prevalence & Ageing Population

Escalating diabetes prevalence, particularly the 68% surge in type 2 diabetes projected for Asia by 2045, is enlarging the addressable base for the diabetic nephropathy drugs market. Genetic susceptibility at lower body-mass indices accelerates kidney complications, prompting earlier screening programs reliant on biomarkers such as NGAL and KIM-1. Ageing adds further strain, as natural declines in renal function hasten the transition from microalbuminuria to overt nephropathy. Health systems are rolling out population-wide screening alongside prevention campaigns. These intertwined demographic pressures are expected to sustain long-run growth for the diabetic nephropathy drugs market.

Clinical Adoption of SGLT2 Inhibitors Post-CREDENCE & EMPA-REG Trials

Landmark trials such as CREDENCE and EMPA-REG demonstrated renal and cardiovascular protection independent of glucose control, driving guideline upgrades that elevate SGLT2 inhibitors to first-line status. Real-world evidence indicates a 45% lower in-hospital mortality for continuous SGLT2 inhibitor users during admissions. The recent U.S. approval of sotagliflozin for heart failure in chronic kidney disease broadens applicability. Adoption gaps persist, with only a minority of eligible patients prescribed these agents, leaving headroom for the diabetic nephropathy drugs market to expand. Growing payer recognition of total-cost-of-care savings is expected to accelerate uptake.

High List-Price of Novel Agents (e.g., Finerenone)

At roughly USD 19 daily, finerenone stretches affordability thresholds, particularly under budget-capped health systems. Insurers impose step-therapy protocols, lengthening the path to optimal care and dampening the velocity of uptake. Lifelong therapy magnifies cumulative expenditure versus acute indications. U.S. price negotiations under Medicare starting in 2026 will heavily discount older diabetes drugs, yet novel agents stay outside those bargains, maintaining cost pressure when combination regimens pair multiple premium agents, affordability barriers compound, muting near-term growth for the diabetic nephropathy drugs market.

Other drivers and restraints analyzed in the detailed report include:

- Guideline Shift Toward Early RAS-Blockade Intensification

- AI-Based Urinary Biomarker Panels Enabling Pre-Emptive Therapy

- Stringent Renal-Safety Regulatory Endpoints Prolonging Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ACE inhibitors retained the largest 33.1% diabetic nephropathy drugs market share in 2025. SGLT2 inhibitors, however, headline growth with a 12.5% CAGR through 2031, buoyed by approvals that now extend to non-diabetic chronic kidney disease and heart failure cohorts. ARBs provide first-line alternatives when ACE inhibitors are contraindicated. MRAs such as finerenone address residual inflammation and fibrosis, gaining traction for proteinuric patients resistant to RAS blockade. Diuretics retain a role in fluid management, while GLP-1 receptor agonists and DPP-4 inhibitors occupy an emerging "Others" niche owing to ancillary renal effects.

Clinical data from the CONFIDENCE trial showed that dual finerenone-empagliflozin therapy outperforms monotherapy, foreshadowing a pivot from single-drug dominance to regimen-based care. Furthermore, the diabetic nephropathy drugs market size for combination-oriented approaches is expected to escalate as endothelin receptor antagonists and complement inhibitors, such as atrasentan and iptacopan, secure accelerated approvals. Growing clinician familiarity with multidrug protocols is reinforcing formulary placement and supporting adoption curves.

Geography Analysis

North America dominated with 37.4% share of the diabetic nephropathy drugs market in 2025, underpinned by mature insurance frameworks, extensive clinical trial networks, and rapid adoption of first-in-class therapies. Medicare's Kidney Care Choices Model incentivizes early-stage management, boosting prescription volumes. Upcoming 68% Part D discounts on legacy diabetes drugs will redirect savings toward novel nephroprotective agents, further fortifying demand.

Asia-Pacific represents the fastest-growing region, projected at a 9.3% CAGR through 2031. Prevalence of microalbuminuria (39.8%) and macroalbuminuria (18.8%) among Asian type 2 diabetes patients underscores the public-health emergency. Governments are funding early screening, while expanding insurance pools open doors for high-value therapies.

Europe maintains solid volume through universal healthcare and structured health-technology assessments. EMA approvals of finerenone and atrasentan illustrate regulators' balanced stance on innovation and safety. Meanwhile, the Middle East, Africa, and South America exhibit emerging potential amid rising diabetes incidence and incremental reimbursement reforms, although price sensitivity may temper near-term uptake. Together, regional dynamics shape a diversified demand profile for the diabetic nephropathy drugs market.

- AstraZeneca

- Bayer

- Boehringer Ingelheim & Eli Lilly (Alliance)

- Johnson & Johnson

- Abbvie

- Novartis

- Pfizer

- Merck

- Novo Nordisk

- GlaxoSmithKline

- Sanofi

- CSL Vifor Pharma

- Fresenius Medical Care AG

- Baxter

- DaVita

- Medtronic plc (renal therapies)

- Otsuka Pharmaceutical Co.

- Ardelyx Inc.

- Chinook Therapeutics

- Ionis Pharmaceuticals

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diabetes Prevalence & Ageing Population

- 4.2.2 Clinical Adoption Of SGLT2 Inhibitors Post-CREDENCE & EMPA-REG Trials

- 4.2.3 Guideline Shift Towards Early RAS-Blockade Intensification

- 4.2.4 AI-Based Urinary Biomarker Panels Enabling Pre-Emptive Therapy

- 4.2.5 Value-Based Kidney-Care Payment Bundles In Developed Countries

- 4.2.6 Emergence Of Combination Therapy Strategies

- 4.3 Market Restraints

- 4.3.1 High List-Price Of Novel Agents (E.G., Finerenone)

- 4.3.2 Stringent Renal-Safety Regulatory Endpoints Prolonging Approvals

- 4.3.3 Low Nephropathy Awareness In Low- & Mid-Income Countries

- 4.3.4 Venture Capital Shift Toward Multi-Organ Metabolic Drugs

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Drug Class

- 5.1.1 ACE Inhibitors

- 5.1.2 Angiotensin II Receptor Blockers (ARBs)

- 5.1.3 SGLT2 Inhibitors

- 5.1.4 Mineralocorticoid Receptor Antagonists (MRAs)

- 5.1.5 Diuretics

- 5.1.6 Others (GLP-1 RAs, DPP-4, etc.)

- 5.2 By Diabetes Type

- 5.2.1 Type-1 Diabetes

- 5.2.2 Type-2 Diabetes

- 5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail/Community Pharmacies

- 5.3.3 Online Pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AstraZeneca plc

- 6.3.2 Bayer AG

- 6.3.3 Boehringer Ingelheim & Eli Lilly (Alliance)

- 6.3.4 Johnson & Johnson (Janssen)

- 6.3.5 AbbVie Inc.

- 6.3.6 Novartis AG

- 6.3.7 Pfizer Inc.

- 6.3.8 Merck & Co. Inc.

- 6.3.9 Novo Nordisk A/S

- 6.3.10 GSK plc

- 6.3.11 Sanofi S.A.

- 6.3.12 CSL Vifor Pharma

- 6.3.13 Fresenius Medical Care AG

- 6.3.14 Baxter International Inc.

- 6.3.15 DaVita Inc.

- 6.3.16 Medtronic plc (renal therapies)

- 6.3.17 Otsuka Pharmaceutical Co.

- 6.3.18 Ardelyx Inc.

- 6.3.19 Chinook Therapeutics

- 6.3.20 Ionis Pharmaceuticals

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment