|

시장보고서

상품코드

2061897

글루포시네이트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Glufosinate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

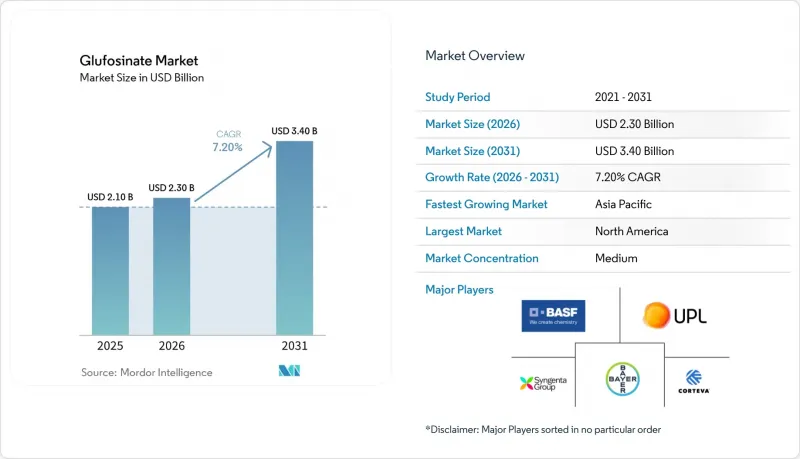

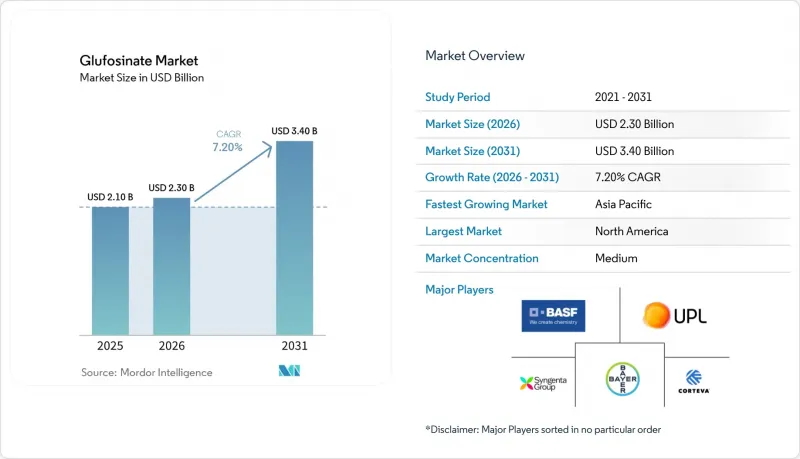

Mordor Intelligence에 의하면, 글루포시네이트 시장 규모는 2025년 21억 달러로 평가되었습니다. 2026년 23억 달러로 확대되어 2031년까지 34억 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 7.2%를 나타낼 전망입니다.

본 보고서는 작물 유형별(곡물 등), 제형별(수현탁액 농축제 등), 처리 단계별(발아 전 등), 유통 채널별(온라인 플랫폼 등) 및 지역별(북미, 유럽, 아시아태평양, 남미, 아프리카, 중동)로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 글루포시네이트 시장 동향 및 분석

글루포시네이트 내성 잡초의 확산이 시장에 미치는 영향

현재, 팔머 아마란스는 미국 내 31개 주에서 워터헴프는 25개 주에서 확산되고 있으며, 두 종 모두 글루포시네이트 내성이 확인되었습니다. 이러한 문제를 방치하면 대두 수확량이 최대 90%까지 감소합니다. 글루포시네이트 내성 잡초 증가는 글루포시네이트 시장의 주요 성장 동력이 되고 있습니다. 내성 잡초 군락에 대처하는 농가들은 효과적인 대체 제초제로 글루포시네이트에 주목하고 있습니다. 글루포시네이트는 더 이상 글루포시네이트에 반응하지 않는 다양한 유형의 잡초를 방제할 수 있습니다. 이러한 추세는 글루포시네이트 사용량이 많은 지역에서 특히 두드러지며, 이러한 지역에서는 작물의 수확량과 품질을 유지하기 위해 내성 관리 전략이 필수적입니다.

글루포시네이트 내성 생명공학 작물의 확대

글루포시네이트 내성 유전자 변형 작물의 보급이 시장 수요를 견인하고 있습니다. 대두, 옥수수, 면화 등 이러한 생명공학 작물 덕분에 농가는 작물에 피해를 주지 않고 글루포시네이트를 살포할 수 있습니다. 이러한 내성 품종의 도입은 효과적인 잡초 방제를 가능하게 하고, 생산성 향상 및 작물 관리 방식의 유연성을 높이기 위해, 특히 북미와 남미를 중심으로 전 세계적으로 확대되고 있습니다. 또한, 생명공학 연구 개발에 대한 투자가 증가함에 따라 새로운 글루포시네이트 내성 작물 품종의 도입이 진행되고 있으며, 이는 시장 성장을 더욱 촉진할 것으로 예측됩니다. 또한, 글루포시네이트는 지속 가능한 농업 관행과도 잘 어울리기 때문에 생산성과 환경 보전의 균형을 맞추고자 하는 농가에게 바람직한 선택지가 되고 있습니다.

차세대 하이드록시페닐피루브산 디옥시게나제(HPPD) 억제제 및 바이오 제초제의 등장

차세대 하이드록시페닐피루브산 디옥시게나제(HPPD) 억제제 및 바이오 제초제의 등장으로 글루포시네이트 시장의 경쟁이 치열해지고 있습니다. 하이드록시페닐피루브산 디옥시게나제(HPPD) 억제제는 광엽 잡초 방제에 효과적인 반면, 미생물이나 식물 추출물 등 천연 유래의 바이오 제초제는 환경적으로 지속 가능한 잡초 방제 방법을 우선시하는 농가들로부터 지지를 받고 있습니다. 이러한 첨단 대체제가 특히 유기농업, 정밀농업 또는 지속 가능한 농업의 실천 분야에서 보급됨에 따라, 특정 작물에 대한 적용 시 글루포시네이트를 부분적으로 대체할 가능성이 있습니다. 이에 대해 각 제조업체는 시장 점유율을 유지하기 위해 제형 개선, 탱크 믹스(혼합 살포)의 호환성 향상, 그리고 타겟을 명확히 한 마케팅 전략의 실행에 주력하고 있습니다.

부문별 분석

곡물 및 곡류 부문이 가장 큰 비중을 차지했으며, 2025년에는 글루포시네이트 시장 점유율의 44%를 차지했습니다. 이러한 선도적 지위는 밀, 쌀, 옥수수 등 주요 식량 작물의 광범위한 재배에서 비롯된 것으로, 이러한 작물의 경우 잡초를 관리하고 수확량을 높이기 위해 효과적인 제초제 솔루션이 요구되고 있습니다. 글루포시네이트의 광범위한 제초 효과와 낮은 잔류 활성은 곡물 재배에 특히 적합합니다. 또한, 이 부문은 확립된 재배 관행과 대규모 곡물 생산자들의 광범위한 도입의 혜택을 누리고 있어, 최대 작물 유형 부문으로서의 입지를 공고히 하고 있습니다.

유지종자 및 콩류는 가장 빠르게 성장하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 9.8%로 확대되고 있습니다. 이러한 성장은 식물성 유지 및 단백질이 풍부한 콩류에 대한 전 세계적 수요 증가와 더불어, 아시아·태평양 지역 및 남미 등지에서 재배 면적이 확대됨에 따라 주도되고 있습니다. 농가들은 특히 유지종자나 콩과 작물을 포함한 윤작 체계에서 잡초 관리 효율을 높이고 작물 손실을 최소화하기 위해 글루포시네이트의 사용을 확대되고 있습니다. 또한, 지속 가능한 농업 및 무경운 재배로의 전환이 이러한 작물에서 글루포시네이트 사용을 촉진하고 있습니다. 이는 효과적인 잡초 방제를 보장하는 동시에 토양 보전을 지원하기 위함입니다.

수현탁액 농축제는 기존의 탱크 혼합 및 살포 인프라에 원활하게 통합될 수 있기 때문에 2025년에는 글루포시네이트 시장 점유율의 52%를 차지하며 최대 부문으로 부상했습니다. 이러한 장점은 취급의 용이성, 물에 대한 균일한 분산성, 그리고 신뢰할 수 있는 제초 효과에 기인합니다. 수현탁액 농축제는 일관된 효능과 표준 살포 장비와의 호환성 덕분에 곡물, 잡곡, 유지종자 작물 재배에 있어 농가에서 널리 사용되고 있습니다.

건조 제제(수분산성 과립)는 가장 빠르게 성장하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 11.2%를 나타낼 것으로 전망됩니다. 이는 대규모 농장에서 선호하는 전자상거래 배송 모델과 일치합니다. 이러한 성장은 저장 기간의 연장, 운송의 용이성, 그리고 정밀 살포 시스템 및 기계화 살포 시스템과의 호환성에 힘입어 이루어지고 있습니다. WDG는 액상 제제와 비교해 유출을 최소화하고 내우성을 높이기 때문에 강우량이 많은 지역이나 관개 조건이 불안정한 지역에서 도입이 확대되고 있습니다. 또한, 건조 제제 기술의 발전으로 용해성과 효능이 향상되어, 대규모이며 자원 효율이 높은 농업 실천에서 선호되는 선택지가 되고 있습니다.

지역별 분석

2025년에도 북미는 글루포시네이트 시장에서 32.5%의 점유율을 차지하며, 최대 지역 시장으로서의 위상을 유지했습니다. 이러한 우위는 제초제 내성 작물의 광범위한 도입, 선진적인 농업 인프라, 그리고 확립된 농약 공급망에 기인합니다. 미국과 캐나다의 농가들은 광범위한 잡초 방제 효과, 글루포시네이트 내성 잡초에 대한 효능, 그리고 생명공학 작물 시스템과의 호환성을 이유로 글루포시네이트를 사용하고 있습니다. 또한, 탄탄한 유통망과 견고한 규제 체계를 통해 지역 전체에서 글루포시네이트 제품공급 안정성과 지속적인 사용이 보장되고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 11.2%를 나타낼 것으로 전망됩니다. 이러한 성장은 중국, 인도, 동남아시아 등 여러 국가에서 곡물, 잡곡, 유지종자, 콩류의 재배가 확대된 데 더해, 글루포시네이트 내성 작물 품종의 도입과 현대적인 농업 기술의 급속한 보급에 힘입어 이루어지고 있습니다. 농업 소매 인프라 확충, 디지털 농업 솔루션 도입, 그리고 정밀 살포 기술의 발전이 글루포시네이트의 보급을 더욱 촉진하고 있습니다.

남미의 글루포시네이트 시장은 파라콰트의 공백을 메운 브라질의 사탕수수·커피·대두 부문과 아르헨티나의 다제내성 잡초에 대한 ‘더블 히트’ 프로그램에 힘입어 성장하고 있습니다. 환율 변동과 중국공급 과잉으로 인해 투입 자재 비용은 급등락하고 있지만, 형질 도입과 스택형 프로그램이 가격에 따른 망설임을 상쇄하고 있습니다. 독일과 프랑스 등 유럽 국가들은 여전히 옥수수 및 곡물 분야의 주요 소비국이지만, 내분비계 교란 물질에 대한 규제가 강화될 경우 고부가가치 과수 재배 농가들은 방침을 전환할 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the glufosinate market size is projected to increase from USD 2.1 billion in 2025 to USD 2.3 billion in 2026 and reach USD 3.4 billion by 2031, growing at a CAGR of 7.2% over 2026-2031.

This report is Segmented by Crop Type (Cereals and Grains, and More), by Formulation (Aqueous Suspension Concentrate, and More), by Treatment Stage (Pre-Emergence, and More), by Distribution Channel (Online Platforms and More), and by Geography (North America, Europe, Asia-Pacific, South America, Africa, and Middle East). The Market and Forecasts are Provided in Terms of Value (USD).

Global Glufosinate Market Trends and Insights

Impact of Glyphosate-Resistant Weed Proliferation on the Market

Palmer amaranth nowadays infests 31 United States states and waterhemp 25 states, both showing confirmed glyphosate resistance that slashes soybean yields by up to 90% when unmanaged. The increasing prevalence of glyphosate-resistant weeds is a significant driver for the glufosinate market. Farmers dealing with resistant weed populations are turning to glufosinate as an effective alternative herbicide. It offers control over a broad spectrum of weeds that no longer respond to glyphosate. This trend is particularly prominent in regions with high glyphosate usage, where resistance management strategies are essential to maintaining crop yield and quality.

Expansion of Glufosinate-Tolerant Biotech Crops

The growth of glufosinate-tolerant genetically modified crops is driving market demand. These biotech crops, such as soybeans, maize, and cotton, enable farmers to apply glufosinate without harming the crop. The adoption of these tolerant varieties is expanding globally, particularly in North and South America, as they facilitate effective weed control while supporting higher productivity and flexibility in crop management practices. Furthermore, the increasing investments in biotechnology research and development are leading to the introduction of new glufosinate-tolerant crop varieties, which is projected to further boost market growth. The compatibility of glufosinate with sustainable farming practices also makes it a preferred choice for farmers aiming to balance productivity with environmental stewardship.

Emergence of Next-gen Hydroxyphenylpyruvate Dioxygenase (HPPD) and Bio-Herbicides

The introduction of next-generation Hydroxyphenylpyruvate Dioxygenase (HPPD) inhibitors and bio-herbicides is intensifying competition in the glufosinate market. Hydroxyphenylpyruvate Dioxygenase (HPPD) inhibitors are effective at controlling broadleaf weeds, while bioherbicides derived from natural sources, such as microbes or plant extracts, appeal to farmers prioritizing environmentally sustainable weed control methods. As these advanced alternatives gain popularity, particularly in organic, precision, or sustainable agricultural practices, they may partially replace glufosinate in certain crop applications. In response, manufacturers are focusing on improving formulations, enhancing tank-mix compatibility, and implementing targeted marketing strategies to retain market share.

Other drivers and restraints analyzed in the detailed report include:

- Impact of Paraquat and Dicamba Regulatory Exit on the Market

- Precision-Spraying Adoption Boosting Post-Emergence Demand

- Rainfastness Concerns Under Increasingly Erratic Rainfall Patterns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cereals and grains led the largest segment, with 44% of the glufosinate market share in 2025, this leadership is attributed to the extensive cultivation of staple crops such as wheat, rice, and maize, which require effective herbicidal solutions to manage weeds and enhance yield. Glufosinate's broad-spectrum weed control and low residual activity make it particularly suitable for cereal and grain farming. Furthermore, the segment benefits from established application practices and widespread adoption among large-scale cereal producers, solidifying its position as the largest crop-type segment.

Oilseeds and pulses are the fastest growing, advancing at a 9.8% CAGR through 2026-2031. This growth is driven by increasing global demand for plant-based oils and protein-rich pulses, coupled with expanded cultivation in regions such as Asia-Pacific and South America. Farmers are increasingly adopting glufosinate to enhance weed management efficiency and minimize crop losses, particularly in rotation systems involving oilseeds and legumes. Additionally, the transition toward sustainable and no-till farming practices is boosting glufosinate usage in these crops, as it supports soil conservation while ensuring effective weed control.

Aqueous suspension concentrate led largest segment, with 52% of glufosinate market share in 2025, because they integrate smoothly into existing tank mixes and distribution infrastructure. This dominance is attributed to their ease of handling, uniform dispersion in water, and reliable weed control performance. Suspension concentrates are widely utilized by farmers for cereal, grain, and oilseed crops due to their consistent efficacy and compatibility with standard spraying equipment.

Dry formulation (water-dispersible granules) is fastest growing, projected to grow at an 11.2% CAGR to 2026-2031, aligning with e-commerce shipping models favored by large farms. This growth is driven by their extended shelf life, ease of transport, and compatibility with precision and mechanized spraying systems. WDGs are increasingly adopted in regions with high rainfall or irrigation variability, as they minimize runoff and enhance rainfastness compared to liquid formulations. Additionally, advancements in dry formulation technology are improving solubility and efficacy, making them a preferred choice for large-scale and resource-efficient farming practices.

Geography Analysis

North America remains the largest regional contributor in 2025, with a 32.5% share of the glufosinate market. This dominance is attributed to the widespread adoption of herbicide-tolerant crops, advanced agricultural infrastructure, and a well-established agrochemical supply chain. Farmers in the United States and Canada utilize glufosinate for its broad-spectrum weed control, effectiveness against glyphosate-resistant weeds, and compatibility with biotech crop systems. Additionally, robust distribution networks and strong regulatory frameworks ensure the availability and consistent use of glufosinate products across the region.

Asia-Pacific is the fastest-growing region, with a 11.2% CAGR through 2026-2031. This growth is driven by the increasing cultivation of cereals, grains, oilseeds, and pulses, alongside the adoption of glufosinate-tolerant crop varieties and the rapid implementation of modern farming techniques in countries such as China, India, and Southeast Asia. The expansion of agri-retail infrastructure, adoption of digital farming solutions, and advancements in precision spraying technologies further support the uptake of glufosinate.

South America glufosinate market growing propelled by Brazilian sugarcane, coffee and soybean segments that filled the paraquat void and by Argentine double-hit programs for multi-resistant weeds. Currency swings and Chinese oversupply create input-cost rollercoasters, but trait adoption and stacked programs counterbalance price-induced hesitancy. Europe countries like Germany and France remain core users in corn and cereals, yet high-value fruit growers may pivot if endocrine-disruptor rules tighten.

- BASF SE

- Bayer AG

- UPL Limited

- Syngenta AG

- Nufarm Limited

- Jiangsu Seven-continent Green Chemical Co., Ltd.

- Zhejiang Yongnong Chemical Co., Ltd.

- Fuhua Tongda Chemical Co., Ltd.

- Sumitomo Chemical Co., Ltd.

- Albaugh, LLC

- Limin Chemical Co., Ltd. (Limin Group Co., Ltd.)

- FMC Corporation

- Corteva, Inc.

- Shandong Weifang Rainbow Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Impact of glyphosate-resistant weed proliferation on the market

- 4.2.2 Expansion of glufosinate-tolerant biotech crops

- 4.2.3 Impact of paraquat and dicamba regulatory exit on the market

- 4.2.4 Precision-spraying adoption boosting post-emergence demand

- 4.2.5 Rapid uptake of nano-microencapsulated glufosinate formulations

- 4.2.6 Stacked-trait seed mixes enabling dual-mode herbicide programs

- 4.3 Market Restraints

- 4.3.1 Price volatility driven by Chinese oversupply affects the market

- 4.3.2 Stringent toxicology reviews in the European Union

- 4.3.3 Hydroxyphenylpyruvate Dioxygenase (HPPD) impact on the market

- 4.3.4 Rainfastness concerns under increasingly erratic rainfall patterns

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Crop Type

- 5.1.1 Cereals and Grains

- 5.1.2 Oilseeds and Pulses

- 5.1.3 Fruits and Vegetables

- 5.1.4 Other Crop Types

- 5.2 By Formulation

- 5.2.1 Aqueous Suspension Concentrate

- 5.2.2 Liquid (Soluble) Concentrate

- 5.2.3 Dry Formulation (Water-Dispersible Granules)

- 5.3 By Treatment Stage

- 5.3.1 Pre-Emergence

- 5.3.2 Post-Emergence

- 5.4 By Distribution Channel

- 5.4.1 Agri-Retailers and Cooperatives

- 5.4.2 Online Platforms

- 5.4.3 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Russia

- 5.5.3.5 Italy

- 5.5.3.6 Spain

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Japan

- 5.5.4.5 Thailand

- 5.5.4.6 Vietnam

- 5.5.4.7 Philippines

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products And Services, And Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 UPL Limited

- 6.4.4 Syngenta AG

- 6.4.5 Nufarm Limited

- 6.4.6 Jiangsu Seven-continent Green Chemical Co., Ltd.

- 6.4.7 Zhejiang Yongnong Chemical Co., Ltd.

- 6.4.8 Fuhua Tongda Chemical Co., Ltd.

- 6.4.9 Sumitomo Chemical Co., Ltd.

- 6.4.10 Albaugh, LLC

- 6.4.11 Limin Chemical Co., Ltd. (Limin Group Co., Ltd.)

- 6.4.12 FMC Corporation

- 6.4.13 Corteva, Inc.

- 6.4.14 Shandong Weifang Rainbow Chemical Co., Ltd.