|

시장보고서

상품코드

2061914

선반 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Lathe Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

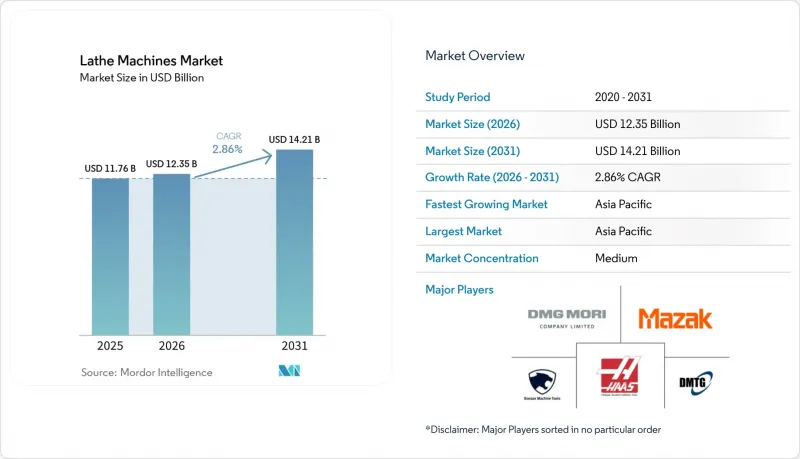

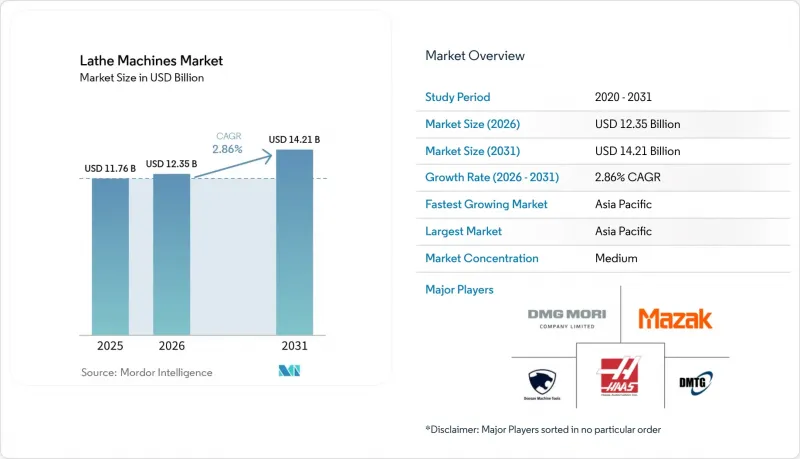

선반 시장 규모는 2025년 117억 6,000만 달러로 평가되었고, 2026년에는 123억 5,000만 달러로 추정되고, 2026-2031년 CAGR 2.86%로 성장을 지속할 전망이며, 2031년까지 142억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(CNC, 기존 등), 기계 구성별(수평형, 수직형 등), 자동화 수준별(수동, 반자동, 완전 자동), 최종 사용자 산업별(자동차, 항공우주 등) 및 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액 기준(10억 달러)으로 제시되어 있습니다.

세계의 선반 시장 동향 및 인사이트

항공우주 부품 제조 수요의 확대

항공우주 분야 수요는 민간 항공기 생산 증가, 국방 프로그램의 현대화, 그리고 우주 경제의 성장에 힘입어 첨단 선반 플랫폼에 구조적인 호재로 작용하고 있습니다. 최근 업계 분석에 따르면, 2035년까지 상당한 성장이 예상되며, 민간 항공이 큰 비중을 차지하고, 방위 관련 사업이 경기 순환 전반에 걸쳐 회복력을 높일 것이라는 점이 강조되고 있습니다. 영국에서는 ‘세계 전투 항공 프로그램(GCAP)’과 같은 장기적인 국방 이니셔티브가 정밀 제조 및 민간 항공우주 공급망에도 파급되는 군민 겸용(듀얼 유스) 연구개발을 촉진할 것으로 예측됩니다. 가법(애디티브)과 감법(서브트랙티브)을 결합한 하이브리드 워크플로는 많은 비행에 필수적인 부품에서 표준으로 자리 잡고 있으며, EASA(유럽항공안전청)의 지침에서는 인증된 인터페이스와 마감을 실현하기 위해 기계 가공이 필수적인 후공정임을 강조하고 있습니다. 이러한 품질 및 인증 기준에 따라, 소량 생산에서 무결함을 실현하는 데 기여하는 다축 선반, 선반 및 밀링 머신 복합기, 그리고 통합 계측 시스템에 대한 수요가 증가하고 있습니다. 감가상각비 우대 조치를 확대하는 재정 정책은 주요 시장의 항공우주 공급업체들 사이에서 자동화 및 디지털화된 선반 센터로의 교체를 더욱 촉진하고 있습니다.

자동차 산업에서의 엔진 및 변속기 부품 수요

전동화로 인해 부품 구성이 변화하고 있음에도 불구하고, 자동차 파워트레인 가공은 여전히 CNC 선반 및 다축 선반의 주요 적용 분야로 남아 있습니다. 독일에서는 2025년에 415만 대의 승용차가 생산되어 전년 대비 2% 증가했으나, 2019년의 생산 대수에는 아직 미치지 못했으며, 2026년 초의 수치는 정체 추세를 보이고 있어, 공급업체들은 생산량뿐만 아니라 생산성과 복잡성에도 계속해서 주력하고 있습니다. 미국에서는 2025년 자동차 생산 대수가 평균 1,018만 대에 달했으며, 그 대부분을 소형 트럭이 차지하고 있어, 이에 따라 차축, 크랭크샤프트, 구동계 하우징을 위한 중절삭 가공이 유지되고 있습니다. EV 아키텍처는 다단 기어의 수를 줄이는 한편, 로터 샤프트, 단단 기어박스 하우징, 열 관리 부품 등 새로운 선삭 수요를 창출하여 선반의 작업 부하에 변화를 가져오고 있습니다. 이러한 변화로 인해, 동일한 설비로 톱니 가공, 측정, 연삭을 통합하는 디지털 사이클을 갖춘 유연성이 높은 선반·밀링 복합 가공기나 5축 대응 플랫폼이 유리해집니다. 제품 수명 주기가 단축되고 부품의 다양성이 높아지는 가운데, 선반 시장은 리드 타임을 늘리지 않고도 설계 변경에 대응할 수 있는 플랫폼으로 자본이 이동하는 혜택을 누리고 있습니다.

첨단 CNC 선반에 대한 막대한 설비 투자

자본 집약성은 도입의 장벽이 됩니다. 특히, 수주 상황이 불안정하고 투자 회수 기간이 짧은 중소기업의 경우 더욱 그렇습니다. 엔트리급 CNC 선반으로도 기본적인 요구 사항은 충족할 수 있지만, 규제가 엄격한 시장이나 고부가가치 부품의 경우, 리니어 구동, 높은 강성, 통합 측정 기능을 갖춘 프리미엄 다축 플랫폼이 요구되므로 도입 비용이 높아집니다. 공구, 공작물 고정, 통합 및 검증은 총 소유 비용(TCO)을 증가시키며, 가동 초기 단계에서 인력 부족으로 인해 가동률이 떨어지면 투자 수익성 판단이 복잡해집니다. 공장이 반자동화에서 무인 셀로 규모를 확대해 나가는 가운데, 용도 엔지니어링 및 단계적 자동화를 포함하는 공급업체 생태계는 이제 투자 타당성을 입증하는 데 있어 핵심적인 역할을 하고 있습니다. 첨단 가공 플랫폼의 공시 가격대는 투자 프로파일을 보여주며, 표면적인 사이클 타임뿐만 아니라 수율, 가동률, 에너지 절감 효과를 고려한 수명 주기 ROI 분석의 필요성을 뒷받침하고 있습니다.

부문별 분석

CNC 선반은 2025년에 61.23%의 시장 점유율을 차지한 것으로 평가되었고, 이는 시제품, 다품종 소량 생산, 그리고 공정 제어가 인증 공급에 필수적인 규제 대상 부품 분야에서 이 장비의 범용성을 반영한 것입니다. 또한, 구매자들이 병렬 가공을 통해 복잡한 회전 부품의 사이클 타임 단축을 추구하는 가운데, 다축 플랫폼은 연평균 성장률(CAGR) 6.23%를 나타낼 것으로 전망됩니다. 첨단 기계는 한 번의 세팅으로 선삭, 밀링, 톱니 가공, 인컷 측정, 에너지 절약 모드를 결합하여 항공우주 및 의료용 부품의 리드타임을 단축하므로, 통합성이 차별화 요소가 됩니다. 기존의 엔진용 선반은 여전히 수리 및 유지보수 분야에서 사용되고 있는 반면, 수직 터렛 선반은 에너지 장비 및 중장비 분야의 대구경·단축 공작물을 가공하는 데 활용되고 있습니다. 특수 용도 선반은 특이한 형상이나 규제가 엄격한 틈새 시장에 대응하며, 맞춤형 제작을 통해 프리미엄 가격을 유지할 수 있는 분야를 담당하고 있습니다. 선반 시장에서는 2차 공정을 생략할 수 있는 플랫폼이 호평을 받고 있습니다. 이는 노동력 부족으로 인해 금속의 절삭 속도뿐만 아니라 공정 단축의 가치도 높아지고 있기 때문입니다.

또한, 선반과 밀링 머신의 하이브리드 기계가 최종 형상에 이르기까지 단일한 공작물 고정 경로를 제공함으로써, 여러 개의 지그 사용에 따른 취급 위험을 줄여주어, 카테고리 간의 경계도 점차 모호해지고 있습니다. 이러한 변화는 추적 가능성과 공정 내 검증이 이제 필수 요건이 된 규제 산업 분야에서 검증된 제조 방식과 부합합니다. 구매자들은 최고 주축 회전수뿐만 아니라, 라이프사이클 지원 및 용도 분야에 대한 전문 지식을 우선시하고 있습니다. 이러한 수요에 따라 선반 업계는 기존의 제품 라벨보다 최종 사용자의 평가를 더 정확하게 반영하는 ‘기능 클러스터’를 기준으로 제품을 분류하고 있습니다. 그 결과, CNC 플랫폼 시장 점유율은 유지되고 있으며, 복잡한 부품군과 설계 주기 단축에 대응하는 다축 선반 및 하이브리드 시스템의 성장이 가속화되고 있습니다.

수평 선반은 바 피더를 활용한 생산과 로봇을 통한 공작물 처리 능력을 바탕으로, 2025년에는 52.87%의 시장 점유율을 차지했습니다. 또한, 구매자들이 더 엄격한 공차와 대기 시간 단축을 목표로 생산 체제를 통합함에 따라, 다축 선반 센터 시장은 연평균 성장률(CAGR) 5.41%로 성장할 것으로 전망됩니다. 수직형 구성은 플랜지, 로터, 터빈 디스크 등 대구경 공작물에서 여전히 필수적이며, 이 경우 중력을 이용한 안정성과 견고한 공작물 고정력이 매우 중요합니다. 스위스형 선반은 기존의 틈새 시장을 넘어, 1000분의 1 mm 미만의 공차와 소형 폼 팩터가 주류를 이루는 의료기기 및 정밀 패스너 분야로 그 영역을 넓혀가고 있습니다. 고사양 기종의 경우, 디지털 사이클 및 열 제어 기능의 추가가 표준적인 요건으로 자리 잡고 있습니다. 그 결과, 선반 시장에서는 장시간 무인 운전 시에도 공차 범위를 확실하게 유지할 수 있는 플랫폼이 높이 평가받고 있습니다.

공급업체의 역할이 확대되어 OEM을 위한 잉여 생산 능력 대응부터 신제품의 신속한 도입 지원에 이르기까지 포괄하게 되면서, 구성 비율은 유연하고 통합된 시스템으로 전환되고 있습니다. 부품 설계의 반복 주기가 빨라지는 가운데, 구매자들은 안정적인 에너지 소비량으로 처리량을 향상시키면서도 품질을 유지하기 위한 시뮬레이션, 폐쇄 루프 측정 및 미리 구축된 가공 사이클을 요구하고 있습니다. 선반 업계는 정밀도나 스핀들의 가동 시간을 희생하지 않으면서도 부품 구성의 변화에 대응할 수 있는 다축 솔루션으로 계속해서 전환하고 있습니다. 디지털화의 진전으로 기존 프로그래밍의 장벽이 낮아지는 가운데, 이러한 추세에 따라 예측 기간 동안 다축 솔루션의 선반 시장 점유율이 확대될 것으로 전망됩니다.

지역별 분석

아시아태평양은 2025년에 48.12%를 차지한 것으로 평가되었으며, 2031년까지 연평균 6.91%의 성장률을 보일 것으로 전망되어 선반 시장의 지역적 견인차 역할을 할 것으로 보입니다. 한편, 다각적인 제조 활동과 정책 지원에 힘입어 자동차, 전자기기, 항공우주 분야공급업체 전반에 걸쳐 생산 능력 확대가 촉진되고 있습니다. 일본과 한국은 성능 벤치마크가 되는 첨단 다축 및 하이브리드 솔루션의 수출을 지속하고 있으며, 인도의 유력 기업들은 리쇼어링 및 공급업체 다각화에 대응하기 위해 제품 포트폴리오를 확대되고 있습니다. 동남아시아의 정밀 산업 클러스터는 바 피더 방식의 선반 가공 및 소형 정밀 부품에 대한 수요를 끌어올리고 있습니다. 해당 지역은 기존 설비의 기반과 역량 향상이 균형을 이루고 있어, 신규 설비 도입에 있어 계속해서 주도적인 입지를 유지할 것으로 보입니다. 자본 배분이 전자 및 모빌리티 공급망에 맞추어 재편되는 가운데, 선반 시장은 아시아태평양 전반에 걸친 자동화 및 디지털 워크플로우의 확산으로 인해 혜택을 보고 있습니다.

북미 시장 전망은 안정적이며, 자동차, 항공우주, 의료 분야의 밸류체인에서는 고부가가치 부품과 라이프사이클 서비스의 확충이 우선시되고 있습니다. 2025년 미국의 자동차 생산 대수는 높은 수준을 유지할 것으로 보이며, 경트럭 생산에 편중되는 추세가 나타나고 있어 드라이브트레인 및 섀시 부품용 대형 선반 가공 수요가 뒷받침될 것으로 보입니다. 민관 협력 프로그램과 정책의 현대화에 따라 통합형 공장 기술과 인재 육성이 중시되고 있으며, 이에 따라 중소기업 사이에서 커넥티드 선반 플랫폼 및 모듈식 자동화에 대한 수요가 증가하고 있습니다. 연방 정부의 인재 양성 이니셔티브는 숙련된 기술 인력 공급원을 확대하는 것을 목표로 하고 있으며, 인력 부족이 완화됨에 따라 잠재적인 설비 수요가 창출될 가능성이 있습니다. 이러한 요인들로 인해 선반 시장은 가동률과 규정 준수를 향상시키는 기능 업그레이드와 밀접하게 연관되어 있습니다.

유럽은 자동차 업계의 선도 기업, 항공우주 분야의 주요 제조업체, 의료 클러스터를 기반으로 여전히 중요한 생산 거점을 유지하고 있습니다. 독일에서는 2025년에 415만 대의 승용차가 생산되었으며, 전동화로 인해 부품 요구 사항이 변화하는 상황 속에서도 파워트레인 가공에 대한 핵심적인 수요를 뒷받침했습니다. 영국의 장기 방위 프로그램에 대한 투자는 민간 항공우주 공급업체와 그 가공 파트너들에게까지 파급되는 정밀 제조 생태계를 뒷받침하고 있습니다. 이탈리아와 스페인은 대형 및 수직 선반 가공 분야에서 생산력을 유지하고 있는 반면, 북유럽 국가들은 선박 및 에너지 관련 부품 분야에서 틈새 시장 역량을 제공합니다. 세계 기타 지역에서는 중동의 산업화 계획과 남미에서의 선택적 확장이 추가적인 성장 기회를 가져오고 있습니다. 이러한 동향들이 맞물려 선반 시장을 지탱하고 있으며, 유럽에서는 고부가가치 부문과 수명 주기 지원이 중시되는 반면, 기타 지역에서는 대량 도입이 추진되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the lathe machines market size is expected to grow from USD 11.76 billion in 2025 to USD 12.35 billion in 2026 and is forecast to reach USD 14.21 billion by 2031 at 2.86% CAGR over 2026-2031.

This report is Segmented by Product Type (CNC, Conventional, and More), by Machine Configuration (Horizontal, Vertical, and More), by Automation Level (Manual, Semi-Automatic, Fully Automatic), by End-User Industry (Automotive, Aerospace, and More), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts in Value (USD Billion).

Global Lathe Machines Market Trends and Insights

Growing Aerospace Component Manufacturing Demand

Aerospace demand is a structural tailwind for advanced turning platforms, supported by rising commercial aviation output, defense program modernization, and a growing space economy. Recent industry analysis highlights substantial growth potential through 2035, with commercial aviation taking the larger share and defense initiatives adding resilience across cycles. In the United Kingdom, long-horizon defense initiatives such as the Global Combat Air Program are expected to stimulate precision manufacturing and dual-use R&D that spills into civilian aerospace supply chains. Additive to subtractive hybrid workflows have become standard for many flight-critical parts, with EASA guidance underscoring machining as a required post-process to achieve certified interfaces and finishes. These quality and certification norms reinforce demand for multi-axis lathes, turn mill centers, and integrated metrology that support zero defect execution at small batch sizes. Fiscal policies that improve capital allowances further catalyze upgrades to automation-ready, digitally enabled turning centers among aerospace suppliers in key markets.

Automotive Industry Demand for Engine and Transmission Components

Automotive powertrain machining remains a key use case for CNC and multi-spindle lathes, even as electrification reshapes component mixes. Germany produced 4.15 million passenger cars in 2025, which was a 2% year over year increase, though still below 2019 volumes, and early 2026 readings point to a near flat trajectory that keeps suppliers focused on productivity and complexity rather than volume alone. In the United States, motor vehicle assemblies averaged 10.18 million units in 2025, with light trucks comprising the bulk, which sustains heavy-duty turning for axles, crankshafts, and drivetrain housings. EV architectures change the lathe workload by reducing multi-speed gear counts while adding new turning needs such as rotor shafts, single-speed gearbox housings, and thermal management components. These shifts favor flexible turn mill centers and 5-axis capable platforms with digital cycles that integrate gear cutting, measuring, and grinding in the same setup. As model cycles shorten and part variety rises, the lathe machines market benefits from capital that moves toward platforms able to absorb design churn without extending lead times.

Extremely High Capital Investment for Advanced CNC Lathes

Capital intensity impedes adoption, especially for small and mid sized firms that face uneven order books and short payback thresholds. Entry level CNC turning can meet basic needs, yet regulated markets and high value parts push buyers toward premium multi axis platforms with linear drives, higher rigidity, and integrated measurement that raise acquisition costs. Tooling, workholding, integration, and validation add to the total cost of ownership, which complicates the business case when labor constraints reduce attainable utilization in the early ramp period. Supplier ecosystems that include application engineering and phased automation are now central to justify spend as shops scale from semi automatic to lights out cells. Published pricing ranges for advanced machining platforms illustrate the investment profile and reinforce the need for lifecycle ROI analysis that captures yield, uptime, and energy savings in addition to headline cycle time.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of General Engineering and Job Shop Operations

- Medical Device Manufacturing Growth

- Critical Shortage of Skilled Lathe Operators and CNC Programmers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CNC lathes held 61.23% of 2025, reflecting their versatility for prototypes, high mix batches, and regulated parts where process control is critical to qualified supply, and multi spindle platforms are projected to record a 6.23% CAGR as buyers chase cycle time reduction on complex rotational parts through parallel operations. Integration is the differentiator as advanced machines combine turning, milling, gear cutting, in cut measurement, and energy saving modes within a single setup to compress lead times for aerospace and medical components. Conventional engine lathes persist in repair and maintenance, while vertical turret lathes serve large diameter, short length work in energy and heavy equipment. Special purpose lathes address outlier geometries and regulated niches that can sustain customization premiums. The lathe machines market favors platforms that can remove secondary steps because workforce scarcity elevates the value of process elimination in addition to raw metal removal rate.

The category lines are also blurring as turn mill hybrids present a single workholding path to final geometry and reduce handling risks tied to multiple fixtures. This shift aligns with validated manufacturing in regulated sectors, where traceability and in process confirmation are now table stakes. Buyers prioritize lifecycle support and application expertise rather than peak spindle ratings alone. These demands help the lathe machine industry segment its offerings by capability clusters, which more closely mirror end user evaluations than traditional product labels. The result is continued share for CNC platforms and faster growth for multi spindle and hybrid systems that align with complex part families and shorter design cycles.

Horizontal lathes accounted for 52.87% in 2025 on the strength of bar-fed production and compatibility with robotic loading, and multi-axis turning centers are forecast to grow at 5.41% CAGR as buyers consolidate operations for tighter tolerances and shorter queues. Vertical configurations remain essential for large diameter workpieces such as flanges, rotors, and turbine disks, where gravity-assisted stability and rigid workholding are critical. Swiss-type lathes are expanding beyond legacy niches to serve medical devices and precision fasteners where sub-thousandth tolerances and small form factors dominate. Digital cycles and thermal control additions are now standard expectations in the upper tier. As a result, the lathe machines market rewards platforms that can reliably hold tolerance bands through long unattended runs.

The configuration mix is shifting toward flexible and integrated systems because supplier roles have broadened to cover overflow capacity and rapid new product introduction support for OEMs. As part designs iterate faster, buyers require simulation, closed-loop measurement, and pre-built machining cycles that preserve quality while pushing throughput at stable energy draw. The lathe machine industry continues to move toward multi-axis solutions that accept volatility in part mix without giving up accuracy or spindle uptime. This tilt helps multi-axis solutions lift their share of the lathe machines market over the forecast period as digital adoption lowers historical programming barriers.

Geography Analysis

Asia Pacific accounted for 48.12% in 2025 and is projected to grow at 6.91% through 2031, making it the regional engine of the lathe machines market, while diversified manufacturing and policy support reinforce capacity expansion across automotive, electronics, and aerospace suppliers. Japan and South Korea continue to export advanced multi-axis and hybrid solutions that set performance benchmarks, and domestic champions in India expand their portfolios to address reshoring and vendor diversification. Precision clusters in Southeast Asia add demand for bar-fed turning and small-form precision parts. The region's balance of installed base and capability upgrades positions it to continue leading new equipment placements. As capital allocation follows electronics and mobility supply chains, the lathe machines market gains from the broader adoption of automation and digital workflows across APAC.

North America's outlook is stable as automotive, aerospace, and medical supply chains prioritize higher value parts and lifecycle service depth. U.S. motor vehicle assemblies remained elevated in 2025, with a light truck skew that supports heavy-duty turning for drivetrain and chassis components. Public-private programs and policy modernization emphasize integrated factory technologies and workforce development, which raise the appeal of connected turning platforms and modular automation among small and mid-sized firms. Federal workforce initiatives aim to expand the skilled trade pipeline, which can unlock latent equipment demand as staffing constraints ease. These drivers keep the lathe machines market tied to capability upgrades that enhance utilization and compliance.

Europe retains a significant base anchored by automotive leaders, aerospace primes, and medical clusters. Germany produced 4.15 million passenger cars in 2025, which sustained core demand for powertrain machining even as electrification changes part requirements. The United Kingdom's long-run defense program investment supports precision manufacturing ecosystems that ripple across civil aerospace suppliers and their machining partners. Italy and Spain maintain production strengths in heavy-duty and vertical turning, while the Nordics contribute niche capabilities in marine and energy parts. Across the rest of the world, industrialization agendas in the Middle East and selective expansions in South America provide incremental growth opportunities. Together, these trends support a lathe machines market where Europe emphasizes high-value segments and lifecycle support, while other regions drive volume placements.

- DMG Mori Co., Ltd.

- Yamazaki Mazak Corporation

- Haas Automation, Inc.

- Doosan Machine Tools Co., Ltd.

- Dalian Machine Tool Group Co., Ltd.

- Okuma Corporation

- Hyundai WIA Corporation

- JTEKT Corporation

- Hardinge Inc.

- Emco Group

- INDEX-Traub

- Citizen Machinery

- Spinner Maschinenbau

- Ace Micromatic Group

- Victor Taichung Machinery

- Hartford Machining Centres

- Maschinenfabrik Berthold Hermle

- Gildemeister Italiana

- Beijing Jingdiao Group

- Arrow Machine Tools

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Aerospace Component Manufacturing Demand

- 4.2.2 Automotive Industry Demand for Engine and Transmission Components

- 4.2.3 Expansion of General Engineering and Job Shop Operations

- 4.2.4 Medical Device Manufacturing Growth

- 4.2.5 Oil and Gas Equipment Manufacturing Requirements

- 4.2.6 Rising Adoption of Multi-Axis and Turn-Mill Centers

- 4.3 Market Restraints

- 4.3.1 Extremely High Capital Investment for Advanced CNC Lathes

- 4.3.2 Critical Shortage of Skilled Lathe Operators and CNC Programmers

- 4.3.3 Long Lead Times for Custom Machine Configurations

- 4.3.4 High Tooling and Maintenance Cost Structure

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value-In USD Billion)

- 5.1 By Product Type

- 5.1.1 CNC Lathe Machines

- 5.1.2 Conventional (Engine) Lathes

- 5.1.3 Multi-Spindle Lathes

- 5.1.4 Vertical Turret / Turning Lathes (VTLs)

- 5.1.5 Special-Purpose Lathes

- 5.1.6 Others - Capstan & Turret Lathes, Bench & Speed Lathes

- 5.2 By Machine Configuration

- 5.2.1 Horizontal Lathes

- 5.2.2 Vertical Lathes

- 5.2.3 Multi-Axis Turning Centres

- 5.2.4 Swiss-Type / Sliding-Head Lathes

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automatic

- 5.3.3 Fully Automatic

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Aerospace & Defence

- 5.4.3 General Machinery Manufacturing

- 5.4.4 Electronics & Electrical

- 5.4.5 Medical Devices

- 5.4.6 Oil & Gas

- 5.4.7 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DMG Mori Co., Ltd.

- 6.4.2 Yamazaki Mazak Corporation

- 6.4.3 Haas Automation, Inc.

- 6.4.4 Doosan Machine Tools Co., Ltd.

- 6.4.5 Dalian Machine Tool Group Co., Ltd.

- 6.4.6 Okuma Corporation

- 6.4.7 Hyundai WIA Corporation

- 6.4.8 JTEKT Corporation

- 6.4.9 Hardinge Inc.

- 6.4.10 Emco Group

- 6.4.11 INDEX-Traub

- 6.4.12 Citizen Machinery

- 6.4.13 Spinner Maschinenbau

- 6.4.14 Ace Micromatic Group

- 6.4.15 Victor Taichung Machinery

- 6.4.16 Hartford Machining Centres

- 6.4.17 Maschinenfabrik Berthold Hermle

- 6.4.18 Gildemeister Italiana

- 6.4.19 Beijing Jingdiao Group

- 6.4.20 Arrow Machine Tools

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment