|

시장보고서

상품코드

2061924

드라이브 바이 와이어(DBW) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Drive-by-Wire - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

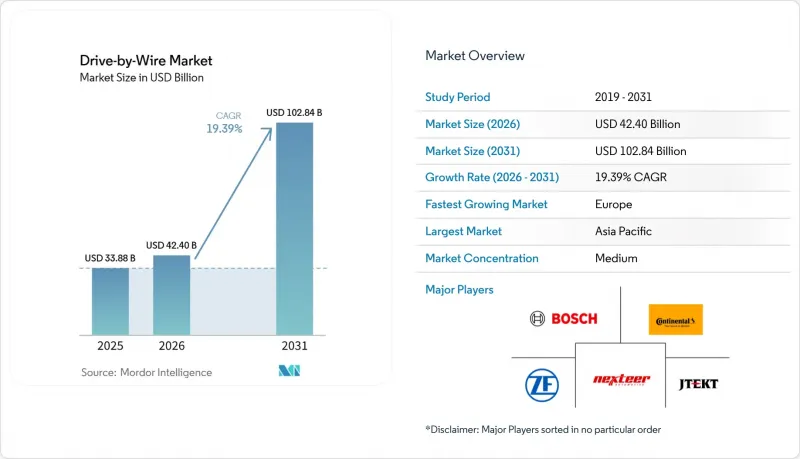

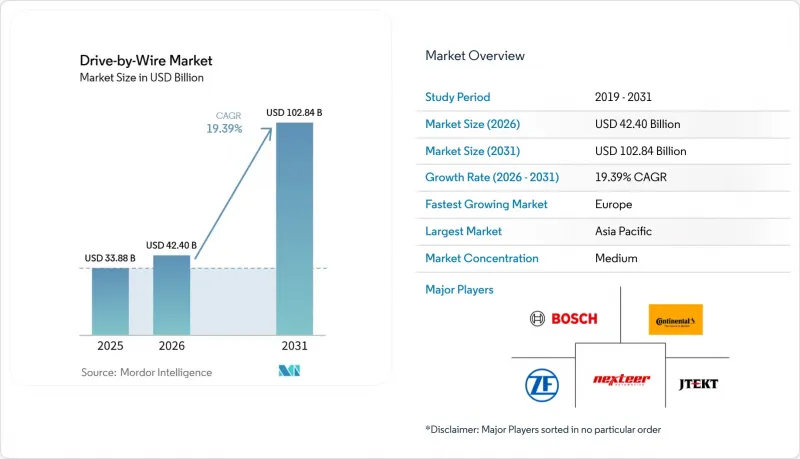

드라이브 바이 와이어 시장 규모는 2025년에 338억 8,000만 달러로 평가되었고, 2026년에 424억 달러로 추정되고, 2031년까지 1,028억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 19.39%로 성장할 전망입니다.

본 보고서는 용도별(스로틀 바이 와이어, Brake by wire 등), 차종별(승용차, 소형 상용차 등), 추진 방식별(내연기관 차량, 하이브리드 전기차 등), 컴포넌트별(액추에이터, 센서 등), 작동 기술별 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 드라이브 바이 와이어 시장 동향 및 분석

ADAS 및 자율주행의 보급 확대

레벨 3 이상의 자율주행에는 기계적 연결 구조로는 달성할 수 없는 10밀리초 미만의 결정론적 제어 루프가 필요하며, 이를 통해 드라이브 바이 와이어는 미래 무인 주행 기능의 기반이 됩니다. 메르세데스-벤츠는 2026년 EQS에 스티어 바이 와이어 시스템을 탑재하여 도심 주행 시 조향 조작력을 대폭 줄였습니다. 중국의 GB 17675-2025 규격은 이중화 기능을 의무화하고 스티어링 컬럼을 폐지함으로써 세계적인 선례가 되고 있습니다. NIO ET9와 XPENG GX는 라이다(LiDAR) 기반의 경로 계획과 자동 차선 변경 기능을 결합하여, 운전자의 조작 없이 이를 수행합니다. UNECE는 스티어 바이 와이어의 이중화 기능을 조건으로 한 미러리스 규정을 마련 중이며, 이에 따라 BEV의 1회 충전당 주행 거리는 최대 12km 연장될 전망입니다.

전기차 플랫폼의 보급 확대

BEV 아키텍처는 유압 및 공압 부품을 배제하고, Brake-by-wire, 스로틀 바이 와이어, 통합형 파워 일렉트로닉스의 도입을 가능하게 함으로써 차량 중량을 줄입니다. BYD는 회생 효율을 높이고 브레이크 먼지 배출을 대폭 줄이는 전기 기계식 Brake-by-wire 시스템을 선보였습니다. 도요타의 2026년형 RAV4는 시프트 바이 와이어 기술과 전자 제어 브레이크를 통합하여 도심 주행 시 에너지 회수 효율을 높였습니다. ZF는 2025년, 수백만 대 규모의 차량을 대상으로 한 통합 제동 제어 시스템 계약을 수주하며, 각 OEM 업체들의 기성 BEV 섀시 모듈에 대한 수요가 증가하고 있음을 입증하고 있습니다. 중국의 4단계 연비 규제는 회생 제동을 장려하고 있으며, 특히 미국이나 EU에서도 유사한 인센티브가 도입될 전망인 만큼, 현지 OEM 각사는 Brake-by-wire 시스템으로의 전환을 서두르고 있습니다.

높은 시스템 비용과 검증의 복잡성

스티어 바이 와이어 시스템은 차량당 비용을 크게 증가시키며, Brake-by-wire 시스템 역시 마찬가지로 비용을 증가시킵니다. 이러한 비용은 전 세계 자동차 생산 대수의 대부분을 차지하는 A부문 및 B부문 차종에서 가격 상승의 주요 요인이 됩니다. ISO 26262 ASIL-D 규격을 준수하려면 고장 주입 시험 및 수백만 킬로미터에 달하는 평가를 포함한 광범위한 테스트가 필요하며, 그 결과 차량 플랫폼 하나당 막대한 엔지니어링 비용이 발생합니다. IPG Automotive는 액추에이터의 동적 특성을 가상화하여 시험 시간을 단축했으나, 이러한 접근 방식의 도입은 여전히 최상위 공급업체로 한정되어 있습니다. 인피니언의 원칩 센서는 부품 비용 절감에 성공했으며, ZF의 모듈형 플랫폼은 서로 다른 차종 간 부품 공통화율이 높아 중기적으로 비용 절감 가능성이 시사되고 있습니다.

부문별 분석

2025년에는 스로틀 바이 와이어가 드라이브 바이 와이어 시장의 39.25%를 차지하며 시장을 독점했습니다. 스티어 바이 와이어는 드라이브 바이 와이어 시장에서 점유율을 확대하고 있으며, 각 OEM 업체들이 레벨 3 자율 주행을 위해 스티어링 칼럼이 없는 운전실을 필요로 하고 있어, 2031년까지 연평균 성장률(CAGR) 21.33%를 나타낼 것으로 전망됩니다. 주요 움직임으로, 메르세데스-벤츠는 2026년 출시 EQS 모델에 이 기술을 적용했습니다. 한편, 여러 중국 자동차 제조업체들은 2026-2027년 대규모 생산 능력 확충을 계획하고 있습니다. Brake-by-wire 기술의 도입이 가속화되는 가운데, ZF는 대규모 수주를 확보했으며, 이는 해당 공급업체가 장기적인 수요 지속에 대해 강한 자신감을 가지고 있음을 보여줍니다.

시프트 바이 와이어나 파크 바이 와이어와 같은 기술은 이미 일반 차량에 적용되고 있습니다. 예를 들어, 2026년 출시 예정인 토요타 RAV4는 터널 높이를 낮춤으로써 승객의 발밑 공간을 넓혔습니다. 서스펜션 바이 와이어는 여전히 틈새 시장 기술이지만, BYD가 그 성능적 우위를 입증함에 따라 비용 절감과 함께 더 광범위한 도입이 이루어질 가능성이 시사되고 있습니다. 앞으로 스티어링과 브레이크 시스템을 통합하는 통합 섀시 제어 기술이 업계에 혁명을 가져올 것으로 보입니다. 이러한 혁신은 하드웨어의 수를 줄일 뿐만 아니라, 2020년대 말까지 중형 세단이 레벨 3 자율 주행을 실현할 수 있는 길을 열어줄 것입니다.

2025년 기준으로 승용차는 드라이브 바이 와이어 시장의 69.11%를 차지했습니다. 그러나 전기 트럭이 회생 제동을 통한 주행 거리 연장을 추구하는 가운데, 중형 및 대형 상용차 시장은 연평균 성장률(CAGR) 20.15%로 성장할 전망입니다. 볼보와 다임러의 프로토타입은 스티어링 컬럼을 제거함으로써 최소 회전 반경을 줄이고, 추가 배터리를 탑재할 공간을 확보했습니다.

소형 상용차는 차량 대여 업체들이 저렴한 구입 비용을 중요시하기 때문에 비교적 저속으로 주행합니다. 그러나 포드의 E-트랜짓과 메르세데스의 e스프린터에는 정지 및 재출발 주행 시 에너지를 회수하기 위한 Brake-by-wire 시스템이 탑재되어 있습니다. 오프로드 차량의 경우, 장시간 교대 근무 중 원격 조종을 지원하기 위해 스티어 바이 와이어(Steer-by-Wire) 시험이 진행되고 있으며, 2027년 유럽에서 기계 지침이 시행되면 기능 안전에 관한 의무적 규제 대상이 됩니다.

지역별 분석

아시아태평양은 2025년 매출의 38.06%를 차지했으며, 중국이 이를 주도했습니다. 중국에서는 GB 17675-2025 규정에 따라 2026년 7월부터 스티어링 컬럼이 폐지됨에 따라, 현지에서 스티어 바이 와이어(Steer-by-Wire) 시스템의 도입이 가속화되고 있습니다. 일본은 '모빌리티 DX 전략'에 따라 막대한 자금을 투입하여, 국내 브랜드를 드라이브 바이 와이어 기술에 기반한 소프트웨어 정의 차량으로 전환하고 있습니다. 2024년, 한국의 현대모비스는 통합 섀시 컨트롤러의 ASIL-D 인증을 획득하며 수출 및 국내 시장 확대의 길을 열었습니다. 인도는 아직 초기 단계에 있지만, AIS-189 사이버 보안 규정에 따라 각 OEM 업체들은 2027년 신차 출시를 목표로 Brake-by-wire 시스템 도입을 검토하고 있습니다.

유럽에서는 중요 원자재법이 희토류 미사용 액추에이터 사용을 의무화하고 페라이트 모터 및 스위치드 릴랙턴스 모터에 대한 투자를 촉진하고 있어, 2031년까지의 연평균 성장률(CAGR)이 20.81%를 나타낼 것으로 예측되며, 지역별로는 가장 빠른 성장세를 보일 전망입니다. 메르세데스-벤츠는 EQS에 스티어 바이 와이어를 최초로 탑재했으며, 폭스바겐의 E3 2.0 아키텍처는 ECU를 통합함으로써 향후 설치를 간소화하고 있습니다. 에코디자인 규제로 인해 추적성 관련 비용이 증가함에 따라, 각 OEM 업체들은 간접비를 분산시키기 위해 조기에 생산 규모를 확대하도록 촉구하고 있습니다.

북미는 시장 점유율 면에서는 뒤처져 있지만, 전자식 구동 시스템을 통해 가장 효과적으로 실현할 수 있는 경량화를 의무화하는 NHTSA의 CAFE 규정의 혜택을 누리고 있습니다. GM의 Ultifi 존 컨트롤러 계획과 포드의 E-Transit에 Brake-by-wire가 표준화된 것은 이 기술이 주류로 자리 잡아가고 있음을 보여줍니다. 캐나다는 MVSS 효율 규제를 미국의 정책과 조화시키고 있는 반면, 브라질의 PROCONVE L8 배기가스 기준이나 UAE의 자율주행 택시 구상은 규모는 작지만 성장세가 두드러지는 수요 거점을 창출하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the drive-by-wire market size is projected to be USD 33.88 billion in 2025, USD 42.40 billion in 2026, and reach USD 102.84 billion by 2031, growing at a CAGR of 19.39% from 2026 to 2031.

This report is Segmented by Application (Throttle-By-Wire, Brake-By-Wire, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Propulsion Type (Internal-Combustion Engine Vehicles, Hybrid Electric Vehicles, and More), Component (Actuators, Sensors, and More), Actuation Technology, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Drive-by-Wire Market Trends and Insights

Growing Adoption of ADAS and Autonomous Driving

Level 3+ automation needs deterministic sub-10-millisecond control loops that mechanical linkages cannot meet, making drive-by-wire foundational for future driverless capability. Mercedes-Benz embedded steer-by-wire in the EQS in 2026 and cut urban steering effort significantly. China's GB 17675-2025 mandates redundancy and deletes the steering column, creating a global precedent . NIO ET9 and XPENG GX marry LiDAR-based path planning with autonomous lane changes, executing them without driver input. UNECE is drafting mirrorless regulations contingent on steer-by-wire redundancy, which would extend BEV driving range by up to 12 kilometers per charge.

Rising EV Platform Penetration

BEV architectures eliminate hydraulic and pneumatic components, making way for brake-by-wire, throttle-by-wire, and integrated power electronics, thereby reducing curb weight. BYD showcased an electro-mechanical brake-by-wire system that improves energy recuperation and significantly reduces brake dust emissions. Toyota's 2026 RAV4 integrates shift-by-wire technology with electronically controlled brakes, enhancing energy recovery during city driving . ZF secured a contract in 2025 for integrated brake control spanning millions of vehicles, underscoring OEM demand for prefabricated BEV chassis modules. China's Phase IV fuel-consumption regulations incentivize regenerative braking, steering local OEMs towards brake-by-wire systems, especially ahead of similar incentives set to roll out in the United States and EU.

High System Cost and Validation Complexity

Steer-by-wire systems add a significant premium per vehicle, while brake-by-wire systems also increase costs. These expenses represent a notable markup on A- and B-class cars, which account for a substantial share of global automotive output. Compliance with ISO 26262 ASIL-D standards requires extensive testing, including fault injection and multi-million-kilometer evaluations, resulting in considerable engineering costs per vehicle platform. While IPG Automotive has reduced testing time by virtualizing actuator dynamics, adoption of this approach remains limited to top-tier suppliers. Infineon's one-chip sensors have successfully reduced the bill of materials, and ZF's modular platform shares a high percentage of parts across different vehicle classes, indicating a potential cost reduction in the medium term.

Other drivers and restraints analyzed in the detailed report include:

- Weight-Reduction and Fuel-Efficiency Mandates

- Cyber-Secure Fail-Operational E/E Architectures

- Functional-Safety Certification Barriers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Throttle-by-wire dominated the drive-by-wire market with 39.25% share in 2025. Steer-by-wire accounted for a rising share of the drive-by-wire market and is projected to post a 21.33% CAGR through 2031, as OEMs need column-free cabins for Level 3 automation. In a significant move, Mercedes-Benz integrated the technology into its EQS model set for release in 2026. Meanwhile, several Chinese automakers have planned substantial production capacity for the years 2026-2027. As the adoption of brake-by-wire technology gains momentum, ZF has secured a major order, signaling strong supplier confidence in sustained long-term volumes.

Technologies like shift-by-wire and park-by-wire have already found their way into mainstream vehicles. For instance, Toyota's RAV4, scheduled for 2026, features a reduced tunnel height, enhancing legroom for passengers. While suspension-by-wire remains a niche offering, BYD's demonstration of its performance advantages suggests a potential for wider adoption as costs decrease. Looking ahead, integrated chassis control is set to revolutionize the industry by merging steering and braking systems. This innovation not only reduces the hardware count but also paves the way for mid-priced sedans to achieve Level 3 autonomy by the end of the decade.

Passenger cars accounted for 69.11% of the drive-by-wire market share in 2025. Yet, medium- and heavy-duty commercial vehicles will expand at a 20.15% CAGR as electric trucks pursue regenerative braking range boosts. Volvo and Daimler prototypes cut turning circles and clear room for extra batteries once columns vanish.

Light commercial vehicles operate at slower speeds because fleets prize low acquisition costs. However, the Ford E-Transit and Mercedes eSprinter now include brake-by-wire to recover energy during stop-and-go duty. Off-highway vehicles are testing steer-by-wire to support remote control during long shifts and will face mandatory functional-safety rules after Europe enacts its Machinery Regulation in 2027.

Geography Analysis

Asia-Pacific held 38.06% of 2025 revenue, led by China, where GB 17675-2025 removes the steering column from July 2026 and accelerates local steer-by-wire adoption. Japan allocates significant funding under its Mobility DX Strategy, steering domestic brands towards software-defined vehicles reliant on drive-by-wire technology. In 2024, South Korea's Hyundai Mobis secured ASIL-D certification for its integrated chassis controller, paving the way for both export and domestic expansion. While India is still in the nascent stages, the AIS-189 cybersecurity regulations are prompting OEMs to consider brake-by-wire systems for their 2027 launches.

Europe is projected to record a 20.81% CAGR through 2031, the fastest regional pace, as the Critical Raw Materials Act demands rare-earth-free actuators and sparks investment in ferrite and switched-reluctance motors. Mercedes-Benz debuted steer-by-wire in the EQS, and Volkswagen's E3 2.0 architecture consolidates ECUs to simplify future installations. The Ecodesign regulation adds traceability costs, nudging OEMs to scale volumes sooner to spread overhead.

North America trails in share yet gains from NHTSA CAFE rules that compel weight reductions best delivered by electronic actuation. GM's Ultifi zone-controller plan and Ford's E-Transit brake-by-wire standardization illustrate mainstream uptake. Canada aligns its MVSS efficiency rules with U.S. policy, while Brazil's PROCONVE L8 emission standard and the UAE autonomous taxi initiative create smaller but growing demand pockets.

- Robert Bosch GmbH

- Continental AG

- ZF Friedrichshafen AG

- Nexteer Automotive

- JTEKT Corporation

- Curtiss-Wright Corporation

- Astemo, Ltd.

- DENSO Corporation

- NSK Ltd.

- Nissan Motor Co., Ltd.

- SKF Group

- Mobil Elektronik GmbH

- Schaeffler AG

- Hyundai Mobis

- Ficosa International

- Infineon Technologies AG

- Kongsberg Automotive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Market Definition

- 1.3 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of ADAS and Autonomous Driving

- 4.2.2 Rising EV Platform Penetration

- 4.2.3 Weight-Reduction and Fuel-Efficiency Mandates

- 4.2.4 Cyber-Secure Fail-Operational E/E Architectures

- 4.2.5 Zonal Architectures Reducing Wiring Harness Length

- 4.2.6 EU Rare-Earth-Free Motor Directives Spurring SBW

- 4.3 Market Restraints

- 4.3.1 High System Cost and Validation Complexity

- 4.3.2 Functional-Safety Certification Barriers

- 4.3.3 Scarcity of ISO-26262 Engineers

- 4.3.4 Limited Aftermarket Service Readiness

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Throttle-by-Wire

- 5.1.2 Brake-by-Wire

- 5.1.3 Steer-by-Wire

- 5.1.4 Shift-by-Wire

- 5.1.5 Park-by-Wire

- 5.1.6 Suspension-by-Wire

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.2.4 Off-highway Vehicles

- 5.3 By Propulsion Type

- 5.3.1 Internal-Combustion Engine Vehicles

- 5.3.2 Hybrid Electric Vehicles

- 5.3.3 Battery Electric Vehicles

- 5.4 By Component

- 5.4.1 Actuators

- 5.4.2 Sensors

- 5.4.3 Electronic Control Units (ECU)

- 5.4.4 Software and Middleware

- 5.4.5 Wiring-Harness and Connectors

- 5.4.6 Others

- 5.5 By Actuation Technology

- 5.5.1 Electro-Mechanical

- 5.5.2 Electro-Hydraulic

- 5.5.3 Electro-Pneumatic

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 GCC

- 5.6.5.2 Turkey

- 5.6.5.3 South Africa

- 5.6.5.4 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Nexteer Automotive

- 6.4.5 JTEKT Corporation

- 6.4.6 Curtiss-Wright Corporation

- 6.4.7 Astemo, Ltd.

- 6.4.8 DENSO Corporation

- 6.4.9 NSK Ltd.

- 6.4.10 Nissan Motor Co., Ltd.

- 6.4.11 SKF Group

- 6.4.12 Mobil Elektronik GmbH

- 6.4.13 Schaeffler AG

- 6.4.14 Hyundai Mobis

- 6.4.15 Ficosa International

- 6.4.16 Infineon Technologies AG

- 6.4.17 Kongsberg Automotive

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment