|

시장보고서

상품코드

2061940

미디어, 엔터테인먼트 및 컨텐츠 작성용 에이전트 AI 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agentic AI In Media, Entertainment, And Content Creation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

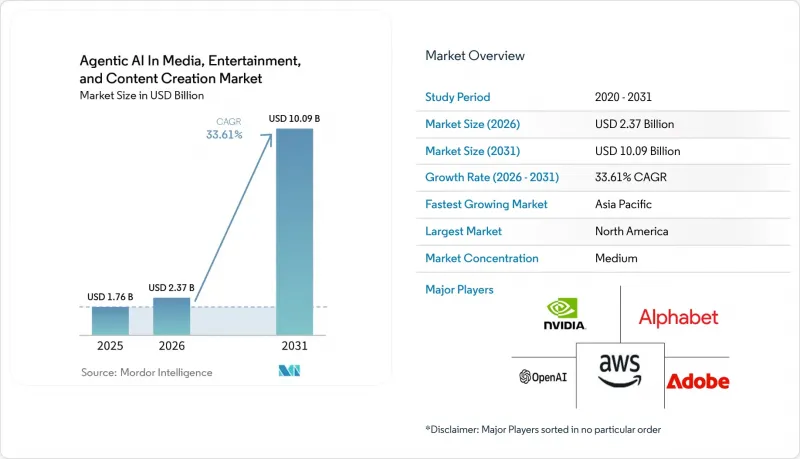

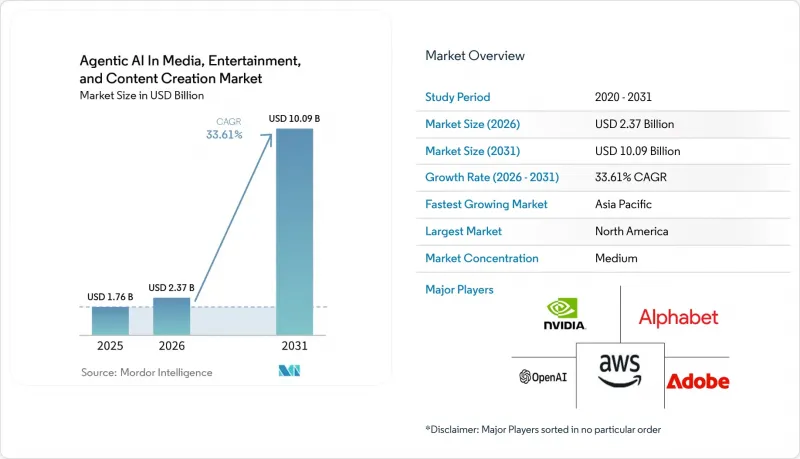

미디어, 엔터테인먼트 및 컨텐츠 작성용 에이전트 AI 시장 규모는 2025년 17억 6,000만 달러로 평가되었고, 2026년에는 23억 7,000만 달러로 추정되고, 2026-2031년 CAGR 33.61%로 성장을 지속할 전망이며, 2031년까지 100억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 용도별(제작 및 컨텐츠 제작, 포스트 프로덕션 및 VFX, 기타), AI 자율 수준별(지원형 AI, 기타), 도입 모델별(온프레미스, 클라우드, 하이브리드), 최종 사용자별(영화 및 TV 스튜디오, 기타), 컴포넌트별(소프트웨어 플랫폼, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미디어, 엔터테인먼트 및 컨텐츠 작성용 에이전트 AI 시장 동향 및 인사이트

생성형 AI의 비용 감소로 인해 인디 크리에이터들 시장 진입이 가능해졌습니다.

2024년 초부터 2025년 말까지 추론 비용이 70% 감소함에 따라 진입 장벽이 낮아져, YouTube 제작자들은 50달러 미만의 비용으로 1분 분량의 동영상을 제작할 수 있게 되었습니다. 자금은 시나리오 작성, 스토리보드 제작, 에셋 생성을 자동화하는 Sozee나 Channel Farm과 같은 AI 네이티브 기업들로 유입되었습니다. OpenAI, Anthropic, Cohere의 각 모델을 연동하는 노코드 오케스트레이션 툴 덕분에 엔지니어링 인력이 더 이상 필요하지 않게 되었습니다. OpenAI의 GPT-4 Turbo 가격은 2024년 1월 1,000 토큰당 0.03달러에서 2025년 12월까지 0.01달러로 인하되었습니다. 한편, Midjourney나 Stability AI와 같은 플랫폼의 이미지 생성 비용은 프레임당 0.01달러 미만으로, 크리에이터들은 완성된 동영상 1분당 50달러 미만의 비용으로 숏폼 동영상 컨텐츠를 제작할 수 있게 되었습니다. 비용이 더욱 낮아짐에 따라, 독립 크리에이터들은 대형 스튜디오가 간과했던 롱테일 틈새 시장을 공략하며 신작의 양과 다양성을 새롭게 바꾸고 있습니다.

스트리밍 플랫폼에서의 초개인화 컨텐츠에 대한 수요

현재 시청 시간의 4분의 3 이상은 추천 엔진의 영향을 받고 있으며, Disney+나 Spotify와 같은 서비스에서는 생성형 AI를 도입해 지역에 맞춘 예고편, 썸네일, 팟캐스트 인트로, 나아가 대체 스토리 전개까지 제작하고 있습니다. 조사에 따르면, 맞춤형 경험은 재이용률을 최대 25%까지 높일 수 있으며, 이는 수십억 달러 규모의 추가적인 반복 수익으로 이어집니다. 이러한 경제적 논리에 따라, 플랫폼은 문화적 뉘앙스와 지역 규정을 준수하면서도 대규모로 컨텐츠를 생성하고 태그를 부여하는 반자율형 시스템의 도입을 추진하고 있습니다.

합성 배우 및 딥페이크를 둘러싼 윤리적 우려

미국 영화 텔레비전 배우 조합(SAG)은 2025년, 디지털 초상 사용 시 동의와 2차 사용료 지급을 의무화하는 계약 조항을 포함시켜 스튜디오의 규정 준수 비용을 절감했습니다. 유명 배우의 무단 AI 복제를 둘러싼 500만 달러 규모의 화해를 포함해, 많은 관심을 모았던 이 소송은 법적 위험을 여실히 드러냈습니다. 조사에 따르면, 대다수의 소비자는 합성 미디어에 대한 더 엄격한 규제를 지지하고 있으며, 현재 EU 규정에서는 워터마크 표시가 의무화되어 있습니다. 기업은 업무 절차에 동의 관리 및 정보 공개를 포함시켜야 하며, 그렇지 않을 경우 평판 하락이나 법적 제재의 위험을 감수하게 됩니다.

부문별 분석

미디어, 엔터테인먼트 및 컨텐츠 작성용 에이전트 AI 시장은 2025년 제작 및 컨텐츠 제작 분야에서 38.31%의 점유율을 기록했습니다. 이는 생성형 동영상 편집 도구와 AI 지원형 에셋 빌더의 광범위한 도입을 반영한 것입니다. 각 스튜디오는 편집 주기를 수주에서 수일로 단축하고, 콘셉트 아트 비용을 최대 40% 절감했습니다. 반면, 현지화 및 번역 시장은 2031년까지 연평균 성장률(CAGR) 34.81%를 나타낼 것으로 전망됩니다. 이는 기존 재더빙 비용의 불과 몇 분의 일 수준에 불과하며, 힌디어, 포르투갈어, 아랍어 시청자를 위해 아카이브 라이브러리를 활용할 수 있게 해주는 다국어 보이스 클로닝 기술에 힘입은 결과입니다.

현재 현지화 기술은 32개 언어에 걸쳐 어조와 리듬을 95%의 정확도로 재현하고 있으며, 이를 통해 플랫폼은 기존 컨텐츠를 새롭게 단장하고 대상 시장을 신속하게 확대할 수 있게 되었습니다. 그 결과, 미디어, 엔터테인먼트, 컨텐츠 제작 분야의 현지화 업무와 관련된 에이전트형 AI 시장 규모는 컬러 그레이딩 등 기존 업무보다 훨씬 빠른 속도로 확대될 전망입니다. 또한 스튜디오에서는 마스크 제거, 프레임 보간, 4K 업스케일링을 위해 포스트 프로덕션 AI를 활용하고 있으며, 이를 통해 기존에는 대규모 VFX 팀이 담당하던 작업 부담을 더욱 줄이고 있습니다.

크리에이터들이 수작업 워크플로를 보완하기 위해 텍스트 프롬프트 편집기나 이미지 생성 도구에 의존함에 따라, 어시스턴트 AI는 2025년 지출의 51.24%를 차지했습니다. 세미 에이전트형 솔루션은 의사결정의 주요 단계에서 사용자의 승인을 필요로 하면서도, 하위 작업을 연쇄적으로 연결함으로써 구조화된 자율성을 더했습니다. 향후 완전 자율 주행 시스템 시장은 2031년까지 연평균 성장률(CAGR) 34.21%를 나타낼 것으로 전망됩니다. 이는 데이터베이스 쿼리 실행, 렌더링 일정 설정, 자산 공개를 사람의 개입 없이 수행할 수 있는 함수 호출형 대규모 언어 모델에 의해 주도되는 것입니다.

컨텐츠 검토 및 실시간 자막 생성 분야에서 완전 자율형 시스템의 도입으로 처리 시간이 이미 수 시간에서 수 분으로 단축되었습니다. 그러나 각본 집필이나 촬영 기술 분야에서는 여전히 인간의 감각이 매우 높은 가치를 지니고 있기 때문에 지원적인 역할에 그치고 있습니다. 작업의 복잡성에 맞추어 자율성 수준을 조정할 수 있는 제공업체는 최적의 생산성을 실현하고, 크리에이티브 팀을 소외시키지 않으면서 미디어, 엔터테인먼트, 컨텐츠 제작 분야에서 완전 자율형 AI 시장 점유율을 더욱 확대할 것입니다.

지역별 분석

북미는 할리우드의 LED 볼륨에 대한 조기 투자와 실리콘밸리의 기반 모델 연구소 집적 덕분에 2025년 매출의 37.72%를 차지했습니다. 미국의 스튜디오들은 업계에 특화된 유연한 규제의 혜택을 누리고 있지만, 합성 초상에 관한 새로운 노조 조항으로 인해 허용되는 사용 범위는 좁아지고 있습니다. 캐나다의 58%에 달하는 VFX 세액 공제는 밴쿠버로 해외 포스트 프로덕션 업무를 유치하고 있는 반면, 멕시코의 니어쇼어 시설은 연속 드라마 촬영에 있어 비용 면에서 우위를 제공합니다. 이에 따라 해당 지역의 에이전틱 AI 시장은 안정세를 유지하면서도 미디어, 엔터테인먼트, 컨텐츠 제작 등 각 분야로 분산되고 있습니다.

아시아태평양은 중국의 대중용 'Douyin' 동영상 아바타, 숙련된 노동력 부족을 보완하는 일본의 AI 지원 애니메이션 중간 작화, 그리고 현지 언어 텍스트를 활용한 동영상 생성을 활용하는 인도의 2억 명 규모 크리에이터 기반에 힘입어, 2031년까지 연평균 성장률(CAGR) 34.59%를 나타낼 것으로 전망됩니다. 바이트댄스가 2025년 도우인(Douyin)에 선보인 AI 생성 동영상 아바타는 사용자가 직접 촬영하지 않고도 맞춤형 컨텐츠를 제작할 수 있는 기능으로, 출시 6개월 만에 1억 명 이상의 사용자에게 도달했습니다. 이는 중국 플랫폼이 에이전트형 시스템을 구축할 수 있을 만큼 규모가 크다는 것을 보여줍니다. 한국의 주요 모바일 게임 기업들은 AI 자산을 통합해 레벨 디자인 시간을 약 40% 단축함으로써, 해당 지역의 성장세를 더욱 공고히 하고 북미와의 수익 격차를 좁히고 있습니다.

유럽에서는 영국의 혁신적인 가상 무대나 독일의 고도로 전문화된 VFX 스튜디오를 중심으로 첨단 기술 도입이 계속해서 활발히 이루어지고 있습니다. 그러나 해당 지역은 성장 궤도에 영향을 미칠 수 있는 과제에 직면해 있으며, 특히 EU AI법에 따른 규정 준수 비용과 의무화된 워터마크 표시 요건이 그 예로 꼽힙니다. 이러한 규제 조치는 보다 역동적인 북미 및 아시아태평양 시장과 비교할 때 성장을 둔화시킬 가능성이 있습니다. 한편, 남미와 중동 및 아프리카는 현재 규모는 작지만 유망한 잠재력을 보여주고 있습니다. 브라질의 게임 산업에 대한 5억 달러 규모의 투자는 큰 진전을 가져올 것으로 기대됩니다. 한편, 아랍에미리트(UAE)는 국가 주도의 AI 인센티브를 통해 성장을 적극적으로 촉진하고 있습니다. 이러한 인센티브는 아부다비나 두바이와 같은 주요 지역에 포스트 프로덕션 허브를 구축하는 것을 목표로 하고 있으며, 2031년까지 해당 지역 시장 점유율 확대에 기여할 가능성이 있는 새로운 거점의 출현을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the agentic aI market size in media, entertainment, and content creation is expected to grow from USD 1.76 billion in 2025 to USD 2.37 billion in 2026, and is forecast to reach USD 10.09 billion by 2031 at a 33.61% CAGR over 2026-2031.

This report is Segmented by Application (Production and Content Creation, Post-Production and VFX, and More), AI Autonomy Level (Assistive AI, and More), Deployment Model (On-Premises, Cloud, and Hybrid), End-User (Film and TV Studios, and More), Component (Software Platforms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In Media, Entertainment, And Content Creation Market Trends and Insights

Generative AI Cost Declines Enabling Indie Creators

A 70% drop in inference pricing between early 2024 and late 2025 lowered entry barriers and allowed YouTube producers to complete minute-long videos for under USD 50. Funding flowed to AI-native outfits such as Sozee and Channel Farm, which automate scripting, storyboard creation, and asset generation. No-code orchestration tools that chain OpenAI, Anthropic, and Cohere models removed the need for engineering talent. OpenAI's pricing for GPT-4 Turbo dropped from USD 0.03 per 1,000 tokens in January 2024 to USD 0.01 by December 2025, while image-generation costs on platforms like Midjourney and Stability AI fell below USD 0.01 per frame, enabling creators to produce short-form video content for under USD 50 per minute of finished output. As costs fall further, independent creators seize long-tail niches that large studios overlook, reshaping the volume and diversity of new releases.

Streaming Platforms' Demand for Hyper-Personalized Content

Recommendation engines now influence more than four out of five viewing hours, and services like Disney+ and Spotify embed generative AI to craft localized trailers, thumbnails, podcast intros, and even alternate story arcs. Research indicates that tailored experiences can increase retention by up to 25%, translating into billions in additional recurring revenue. This economic logic drives platforms to adopt semi-agentic systems that generate and tag content at scale while adhering to cultural nuance and regional rules.

Ethical Concerns Over Synthetic Actors and Deepfakes

The Screen Actors Guild secured contract clauses in 2025 that require consent and residuals for the use of digital likeness, reducing compliance costs for studios. High-profile lawsuits, including a USD 5 million settlement involving an unauthorized AI replica of a major actor, highlighted legal exposure. Surveys show most consumers favor stricter rules on synthetic media, and EU regulations now mandate watermarking. Companies must embed consent management and disclosure into workflows or risk reputational damage and enforcement penalties.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Virtual Production Stages in Film-Making

- Cloud-GPU Price Wars Among Hyperscalers

- High IP Licensing Costs for Model Training

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Agentic AI market in media, entertainment, and content creation recorded a 38.31% share in production and content creation in 2025, reflecting widespread adoption of generative video editors and AI-assisted asset builders. Studios shortened editing cycles from weeks to days and cut concept-art costs by up to 40%. In contrast, localization and translations are projected to post a 34.81% CAGR through 2031, fueled by multilingual voice cloning that unlocks archival libraries for Hindi, Portuguese, and Arabic audiences at a fraction of prior re-dubbing costs.

Localization technology now replicates tone and cadence across 32 languages with 95% fidelity, enabling platforms to refresh back catalogs and expand addressable markets quickly. As a result, the Agentic AI market size in media, entertainment, and content creation, tied to localization roles, is poised to expand far faster than legacy tasks such as color grading. Studios also harness post-production AI for mask removal, frame interpolation, and 4K upscaling, further compressing workloads previously handled by large VFX teams.

Assistive AI maintained 51.24% of 2025 spending as creators relied on text-prompt editors and image generators to augment manual workflows. Semi-agentic solutions added structured autonomy, chaining subtasks while still requiring user approval at decision nodes. Looking ahead, fully agentic systems should log a 34.21% CAGR to 2031, driven by function-calling large language models that query databases, schedule renders, and publish assets without human mediation.

In content moderation and real-time subtitle creation, fully agentic deployments already shrink turnaround from hours to minutes. Yet scriptwriting and cinematography remain assistive domains where human taste carries premium value. Providers that map autonomy levels to task complexity will achieve optimal productivity, pushing the Agentic AI market share of full agents in media, entertainment, and content creation higher without alienating creative teams.

Geography Analysis

North America delivered 37.72% of 2025 revenue thanks to Hollywood's early investment in LED volumes and Silicon Valley's concentration of foundation-model labs. U.S. studios benefit from flexible, sector-specific regulation, although new union clauses on synthetic likenesses tighten permissible use. Canada's 58% VFX tax credit has attracted overseas post-production work to Vancouver, while Mexico's nearshore facilities offer cost advantages for episodic shoots, keeping the regional Agentic AI market stable yet distributed across media, entertainment, and content creation.

Asia-Pacific is projected to register a 34.59% CAGR through 2031, fueled by China's mass-market Douyin video avatars, Japan's AI-assisted anime in-betweening that offsets skilled-labor shortages, and India's 200 million-strong creator base leveraging local-language text-to-video generation. ByteDance's 2025 rollout of AI-generated video avatars on Douyin, which allows users to create personalized content without filming, reached over 100 million users within six months, demonstrating the scale at which Chinese platforms can deploy agentic systems. South Korea's mobile game leaders are integrating AI assets to reduce level design time by roughly 40%, reinforcing the region's upward trajectory and closing the revenue gap with North America.

Europe continues to demonstrate strong adoption of advanced technologies, driven by the United Kingdom's innovative virtual stages and Germany's highly specialized VFX studios. However, the region faces challenges that could impact its growth trajectory, particularly due to the compliance costs associated with the EU AI Act and the mandatory watermarking requirements. These regulatory measures may slow down growth when compared to the more dynamic markets of North America and Asia-Pacific. On the other hand, South America, the Middle East, and Africa, while currently smaller markets, are showing promising potential. Brazil's USD 500 million investment in the gaming sector is expected to drive significant advancements, while the United Arab Emirates is actively fostering growth through sovereign AI incentives. These incentives aim to establish post-production hubs in key locations such as Abu Dhabi and Dubai, signaling the emergence of budding hotspots that could help increase regional market share by 2031.

- Adobe Inc.

- OpenAI, L.L.C.

- NVIDIA Corporation

- Amazon Web Services, Inc.

- Alphabet Inc.

- Meta Platforms, Inc.

- Microsoft Corporation

- Stability AI Ltd.

- Runway AI, Inc.

- Synthesia Ltd.

- Epic Games, Inc.

- Unity Software Inc.

- IBM Corporation

- SoundHound AI, Inc.

- Descript, Inc.

- ElevenLabs, Inc.

- Shutterstock, Inc.

- DeepMind Technologies Limited

- WetaFX Ltd.

- Cinesite Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Generative AI Cost Declines Enabling Indie Creators

- 4.2.2 Streaming Platforms' Demand for Hyper-Personalised Content

- 4.2.3 Rise of Virtual Production Stages in Film-Making

- 4.2.4 Cloud-GPU Price Wars Among Hyperscalers

- 4.2.5 Generative Voice and Dubbing Tools Localising Back-Catalogs

- 4.2.6 Foundation Model Fine-Tuning Marketplaces

- 4.3 Market Restraints

- 4.3.1 Ethical Concerns Over Synthetic Actors and Deepfakes

- 4.3.2 High IP Licensing Costs for Model Training

- 4.3.3 Regulatory Uncertainty Around AI-Generated Content

- 4.3.4 Compute Supply Bottlenecks for Agentic Orchestration

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application

- 5.1.1 Production and Content Creation

- 5.1.2 Post-Production and VFX

- 5.1.3 Marketing and Advertising

- 5.1.4 Gaming and Interactive Media

- 5.1.5 Broadcast and Streaming Operations

- 5.1.6 Localisation and Translations

- 5.2 By AI Autonomy Level

- 5.2.1 Assistive AI

- 5.2.2 Semi-Agentic AI

- 5.2.3 Fully Agentic AI

- 5.3 By Deployment Model

- 5.3.1 On-Premises

- 5.3.2 Cloud

- 5.3.3 Hybrid

- 5.4 By End-User

- 5.4.1 Film and TV Studios

- 5.4.2 Publishers and Media Houses

- 5.4.3 Advertising and Creative Agencies

- 5.4.4 Game Studios

- 5.4.5 Independent Creators and SMEs

- 5.5 By Component

- 5.5.1 Software Platforms

- 5.5.2 Services

- 5.5.3 Hardware Accelerators

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Adobe Inc.

- 6.4.2 OpenAI, L.L.C.

- 6.4.3 NVIDIA Corporation

- 6.4.4 Amazon Web Services, Inc.

- 6.4.5 Alphabet Inc.

- 6.4.6 Meta Platforms, Inc.

- 6.4.7 Microsoft Corporation

- 6.4.8 Stability AI Ltd.

- 6.4.9 Runway AI, Inc.

- 6.4.10 Synthesia Ltd.

- 6.4.11 Epic Games, Inc.

- 6.4.12 Unity Software Inc.

- 6.4.13 IBM Corporation

- 6.4.14 SoundHound AI, Inc.

- 6.4.15 Descript, Inc.

- 6.4.16 ElevenLabs, Inc.

- 6.4.17 Shutterstock, Inc.

- 6.4.18 DeepMind Technologies Limited

- 6.4.19 WetaFX Ltd.

- 6.4.20 Cinesite Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment