|

시장보고서

상품코드

2061960

사이버 보안 에이전트형 AI : 시장 점유율 분석, 업계 동향 및 통계, 성장 전망(2026-2031년)Cybersecurity Agentic AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

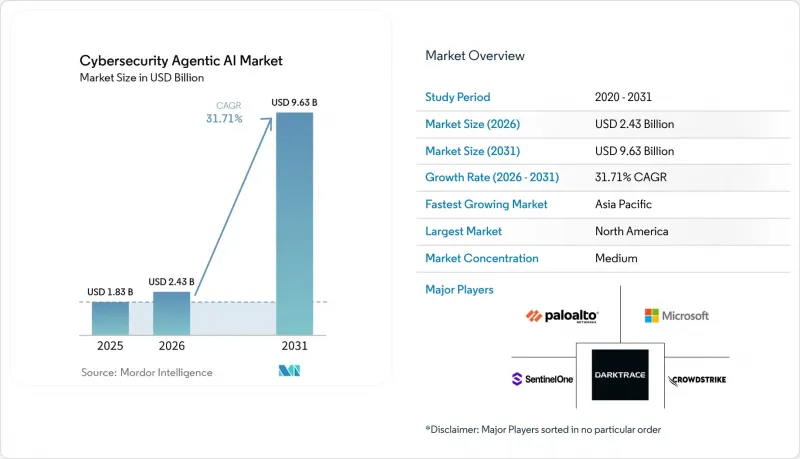

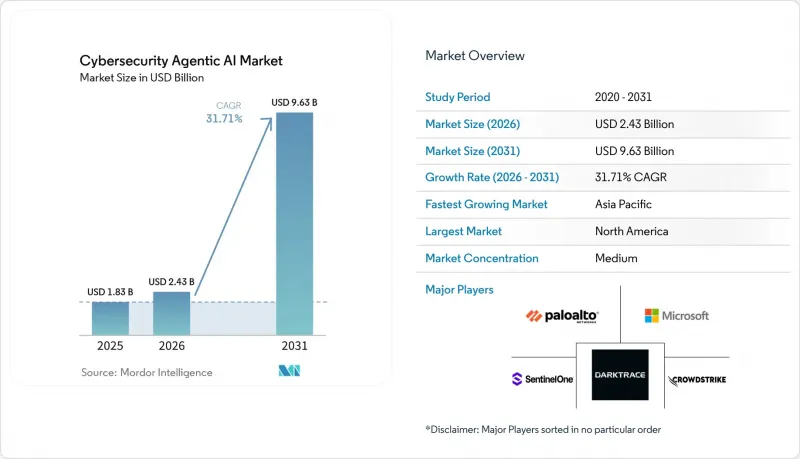

Mordor Intelligence에 따르면, 사이버 보안 에이전트형 AI 시장 규모는 2025년에 18억 3,000만 달러, 2026년에 24억 3,000만 달러, 2031년까지 96억 3,000만 달러에 이를 것으로 전망됩니다.

또한 2026년부터 2031년까지 연평균 성장률(CAGR) 31.71%를 기록할 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 플랫폼 등), 보안 수준(네트워크 보안, 엔드포인트 보안 등), 배포 방식(클라우드 네이티브, On-Premise, 하이브리드), 조직 규모(대기업, 중소기업), 산업 분야(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 사이버 보안 에이전트형 AI 시장 동향과 인사이트

자율적인 대응 루프를 통한 실시간 위협 완화

위협 활동의 확대가 수동 방식의 분류 모델을 능가함에 따라, 사이버 보안 에이전트형 AI 시장이 성장하고 있습니다. CrowdStrike는 2026년 3월, 공격자가 탈출 시간을 29분까지 단축함에 따라 분석가가 주도하는 봉쇄 조치를 취할 여지가 거의 없어졌습니다고 보고했습니다. 자율적인 대응 루프는 조사, 우선순위 지정, 확산 방지를 단일 프로세스로 통합하고, 팀 간 업무 인계에 따른 지연을 방지하기 때문에 매우 중요합니다. 2025년 4월에 출시된 IBM의 ‘Autonomous Threat Operations Machine’은 다중 에이전트 워크플로우와 도메인별 모델을 활용하여, 최소한의 인적 개입으로 위협 분류 및 복구를 수행함으로써 이러한 변화를 입증하고 있습니다. 이러한 루프는 피드백 효과를 만들어내며, 향후 감지 및 대응을 강화하기 위한 데이터를 생성합니다.

멀티 클라우드 환경에서 기계 생성형 공격 표면의 폭발적인 증가

AI 기반 워크로드 증가에 따라 보안 팀의 공격 표면이 확대되는 가운데, 사이버 보안 에이전트형 AI 시장이 성장하고 있습니다. 시스코는 2026년 2월, 에이전트 기반 워크로드가 클라우드 전반으로 확산됨에 따라 기업들이 AI 기반 정책 적용을 요구하고 있으며, 자율적인 보안 제어에 대한 수요가 증가하고 있다고 지적했습니다. Palo Alto Networks의 2025년 조사에 따르면, 운영 환경에서 AI를 활용하고 있는 조직의 99%가 AI 시스템에 대한 공격을 적어도 한 번은 경험한 바 있으며, 41%는 API 공격이 증가했다고 보고했습니다. Orca Security의 조사에 따르면, 2025년에는 조직의 55%가 2개 이상의 클라우드 공급업체를 이용할 것으로 예상되며, 이는 2024년의 12%에서 증가한 수치로, ID 관리 및 정책 환경의 분산 문제가 두드러지게 나타나고 있습니다. 이에 따라 컨텍스트를 해석하고, 클라우드, API, 트러스트 존을 아우르며 조치를 조정하는 보안 시스템에 대한 수요가 증가하고 있습니다.

적대적 AI와 모델 포이즌링의 위험

사이버 보안 분야의 에이전트형 AI 시장은 방어 능력을 높이는 자율성이, 모델이나 데이터 파이프라인이 침해될 경우 피해를 확대시킬 가능성이 있다는 과제에 직면해 있습니다. OWASP는 백도어 삽입, 출력 변조, 서비스 거부 공격 등 데이터 및 모델 포이즌링을 중대한 위험 요소로 지목하고 있습니다. ICLR 2025의 연구에 따르면, 사전 학습 중 0.1%라는 미미한 포이즌링 비율이라도, 그것이 훈련된 모델에 지속될 가능성이 있는 것으로 밝혀졌습니다. 구글의 위협 인텔리전스 그룹은 2025년에 위협 행위자들이 AI를 악용한 사례를 보고했으며, 이는 사이버 공격에서 AI가 실제로 어떻게 활용될 수 있는지를 보여줍니다. 규제가 엄격한 분야에서는 구매자가 더 엄격한 권한 설정이나 제한된 적용 범위를 요구하거나,本番 시스템에서 자율적인 작동을 허용하기 전에 광범위한 검증을 요구하기 때문에 이러한 위험 요소들이 도입 지연으로 이어질 가능성이 있습니다.

부문별 분석

2025년, 소프트웨어 플랫폼은 39.71%의 점유율을 차지했습니다. 이는 기업이 엔드포인트, 클라우드, ID, 네트워크 텔레메트리 전반에 걸친 통합적인 에이전트 기반 오케스트레이션을 선호하는 경향을 반영하고 있습니다. 이 부문은 공유 정책, 메모리 및 통합된 대응 로직의 이점을 활용하여 대규모 자율적 조치를 간소화하고 있습니다. 에이전트의 분산형 배포는 의사 결정의 불일치나 조치의 중복을 초래할 수 있으므로 위험 요인으로 간주됩니다. 많은 조직이 전개, 워크플로우 재설계, 정책 매핑, 모델 거버넌스 분야에서 외부 지원이 필요하기 때문에 서비스는 여전히 두 번째로 중요한 구성 요소로 남아 있습니다.

구매자가 일회성 구현에서 지속적인 튜닝 및 모니터링으로 전환함에 따라, 서비스에 대한 수요는 점점 더 지속적인 성격을 띠고 있습니다. GitLab이 2025년에 공개한 Duo Agent Platform의 공개 베타 버전은 오케스트레이션이 개발 및 보안 워크플로우로까지 확대되면서, 자문 및 통합에 대한 수요가 증가하고 있음을 여실히 보여주었습니다. 하드웨어 가속기는 지연 시간에 민감한 환경에서의 로컬 추론 수요에 힘입어 2031년까지 연평균 성장률(CAGR) 32.31%를 기록하며 성장할 것으로 전망됩니다. 이러한 변화로 인해 하드웨어는 엣지 환경 및 고속 환경에서 실시간 자율 방어의 핵심 기반이 되며, 지연 시간이 긴 클라우드 왕복 시간에 대한 의존도를 줄여줍니다.

2025년, 사이버 보안 에이전트형 AI 시장에서 네트워크 보안이 28.23%의 점유율을 차지했습니다. 이는 네트워크 텔레메트리가 여전히 동서 방향 트래픽, 횡방향 권한 상승, 정책 위반에 대해 가장 광범위한 실시간 가시성을 제공하기 때문입니다. 많은 기업에게 있어 네트워크 계층은 여전히 에이전트 기반 시스템이 자산과 환경을 넘나들며 행동을 상호 연관지어 분석할 수 있게 해주는 핵심 기반이 되고 있습니다. 엔드포인트 보안 역시 기존 보안 스택에 자율적인 조사 및 안내형 복구를 도입하기에 가장 용이한 분야이기 때문에 확고한 입지를 유지했습니다. 이에 따라 엔드포인트 플랫폼은 사이버 보안 에이전트형 AI 시장에서 에이전트형 기술 도입의 일반적인 진입점이 되고 있습니다.

SentinelOne은 2026년 3월, 자사의 자율 조사 기능인 ‘Purple AI’가 2026 회계연도 4분기에 판매된 라이선스의 50% 이상에 포함되었다고 보고했으며, 이는 엔드포인트 벤더들이 기존 고객 기반을 활용해 에이전트형 기능을 보급하고 있는 실태를 여실히 보여주고 있습니다. 또한, 조직이 다루는 비인간 정체성 및 API 기반 액세스 경로가 증가함에 따라 클라우드 및 SaaS 보안, 그리고 IAM 분야도 성장하고 있습니다. 2031년까지 연평균 성장률(CAGR)이 33.31%로 가장 빠르게 성장하고 있는 OT 및 IoT 보안 시장은 디지털 인프라와 물리적 인프라의 급속한 융합에 힘입어 성장하고 있습니다. 사이버 보안 에이전트형 AI 시장은 단순히 이상 징후를 감지하는 데 그치지 않고, 네트워크의 의도와 운영 맥락을 모두 해석하는 플랫폼으로 전환되고 있습니다.

지역별 분석

북미는 강력한 벤더 기반과 기업들의 조기 도입에 힘입어 2025년 사이버 보안 에이전트형 AI 시장의 34.86%를 차지했습니다. 규제 대상 부문에 대한 지속적인 모니터링과 사이버 복원력을 촉진하는 정책이 추가적인 성장을 뒷받침하고 있습니다. ISC2는 2025년 12월, 해당 지역의 심각한 사이버 보안 인력 부족이 수작업 부담을 줄여주는 플랫폼에 대한 수요를 촉진하고 있다고 보고했습니다. 시장의 성장은 기업의 계약 확대와도 관련이 있으며, 고객은 개별 구매가 아닌 보다 광범위한 플랫폼과의 관계를 통해 에이전트 기능을 도입하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 32.71%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 지역 시장이 될 전망입니다. 이러한 성장은 급속한 디지털화의 확산, 멀티 클라우드 도입, 그리고 AI를 활용한 공격에 대한 우려에 힘입어 이루어지고 있습니다. 이 지역의 조직들은 숙련된 보안 팀을 확충하는 속도를 앞지르는 속도로 사이버 방어 체계를 강화하고 있습니다. 중요 인프라의 현대화 및 분산 환경의 모니터링도 수요를 견인하고 있지만, 데이터 현지화 규제 및 규제의 성숙도에 따라 기회의 불균형이 발생할 가능성이 있습니다.

유럽은 2025년에 3위를 차지할 전망이며, 수요는 금융 서비스, 제조업, 핵심 인프라 분야에 집중되어 있습니다. 이러한 분야에서는 감지와 마찬가지로 거버넌스와 문서화가 중요하게 여겨지고 있습니다. 2026년 『AI and Ethics』지에 게재된 조사 결과에 따르면, 유럽이 투명성과 설명 가능성을 중시하고 있음이 드러났으며, 이는 감사 가능한 자율 시스템에 대한 수요를 뒷받침하고 있습니다. 중동 및 아프리카은 디지털 전환(DX) 프로그램을 통해 소규모 기반에서 성장하고 있는 반면, 남미는 랜섬웨어 위협 증가와 금융 부문의 디지털화를 배경으로 서서히 확대되고 있습니다. 두 지역 모두 발전의 초기 단계에 있지만, 확장성이 있는 감시 및 대응 모델에 대한 수요가 높아지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 요약

제4장 시장 동향

- 시장 개요

- 시장 성장 촉진요인

- 자율 대응 루프를 통한 실시간 위협 완화

- 멀티 클라우드 환경에서 기계 생성형 공격 표면의 급증

- AI를 활용한 지속적인 통제 모니터링에 관한 규제 요건

- 만성적인 사이버 보안 인력 부족이 AI 보안 도입을 가속화하고 있다

- DevSecOps 파이프라인에 LLM 에이전트 통합

- 전문적인 AI 보안 스타트업에 대한 벤처 자금 조달 증가

- 시장 성장 억제요인

- 적대적 AI와 모델 포이즌링의 위험

- 에이전트형 AI의 의사결정에서 설명 가능성의 한계

- 보안 특화형 인프라 모델 훈련에 소요되는 높은 계산 비용

- 관할 구역별로 분할된 데이터 출처 기준

- 거시경제 요인이 시장에 미치는 영향

- 업계 가치사슬 분석

- 규제 동향

- 기술 전망

- Portre's Five Forces 분석

제5장 시장 규모 및 성장 전망

- 구성 요소별

- 소프트웨어 플랫폼

- 서비스(MDR, 자문, 통합)

- 하드웨어 가속기(AI 최적화 칩, 센서)

- 보안 수준별

- 네트워크 보안

- 엔드포인트 보안

- 애플리케이션 보안

- 클라우드 및 SaaS 보안

- ID 및 접근 관리

- OT/IoT 보안

- 모드별

- 클라우드 네이티브

- On-Premise

- 하이브리드

- 조직 규모별

- 대기업

- 중소기업

- 산업 분야별

- BFSI

- 헬스케어 및 생명과학

- 정부·국방

- IT 및 통신

- 제조업

- 소매 및 전자상거래

- 에너지 및 유틸리티

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 그 밖의 남미 국가들

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 그 밖의 유럽 국가들

- 아시아태평양 지역

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양 국가들

- 중동 및 아프리카

- 중동

- 아랍에미리트

- 사우디아라비아

- 그 밖의 중동 국가들

- 아프리카

- 남아프리카

- 이집트

- 그 밖의 아프리카 국가들

- 중동

- 북미

제6장 경쟁 현황

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 개요

- CrowdStrike Holdings Inc.

- Palo Alto Networks Inc.

- Darktrace plc

- SentinelOne Inc.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- Rapid7 Inc.

- Arctic Wolf Networks Inc.

- Sophos Ltd.

- Elastic N.V.

- Google LLC

- Amazon Web Services Inc.

- Accenture plc

- Noma Security

- Vectra AI

- Okta Inc.

제7장 시장 기회와 미래 전망

LSH 26.06.30자주 묻는 질문

According to Mordor Intelligence, the cybersecurity agentic AI market size is projected to be USD 1.83 billion in 2025, USD 2.43 billion in 2026, and reach USD 9.63 billion by 2031, growing at a CAGR of 31.71% from 2026 to 2031.

This report is Segmented by Component (Software Platforms, and More), Security Level (Network Security, Endpoint Security, and More), Deployment (Cloud-Native, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cybersecurity Agentic AI Market Trends and Insights

Real-Time Threat Mitigation Via Autonomous Response Loops

The cybersecurity agentic AI market is growing as threat activity outpaces manual triage models. CrowdStrike reported in March 2026 that adversaries reduced breakout time to 29 minutes, leaving little room for analyst-led containment. Autonomous response loops are crucial because they integrate investigation, prioritization, and containment into a single process, avoiding delays caused by team handoffs. IBM's Autonomous Threat Operations Machine, launched in April 2025, demonstrates this shift by using multi-agent workflows and domain-specific models for triage and remediation with minimal human input. These loops create a feedback effect, generating data to enhance future detection and response.

Explosion of Machine-Generated Attack Surfaces in Multi-Cloud Environments

The cybersecurity agentic AI market is expanding as AI-enabled workloads increase the attack surface for security teams. Cisco noted in February 2026 that enterprises seek AI-aware policy enforcement as agentic workloads spread across clouds, driving demand for autonomous security controls. Palo Alto Networks' 2025 research found that 99% of organizations using AI in production experienced at least one attack on their AI systems, with 41% reporting increased API attacks. Orca Security found 55% of organizations used two or more cloud providers in 2025, up from 12% in 2024, highlighting a fragmented identity and policy environment. This strengthens demand for security systems that interpret context and coordinate actions across clouds, APIs, and trust zones.

Adversarial AI and Model Poisoning Risks

The cybersecurity agentic AI market faces challenges as the same autonomy that enhances defense can amplify damage if models or data pipelines are compromised. OWASP identifies data and model poisoning as critical risks, including backdoor insertion, output manipulation, and denial-of-service attacks. Research at ICLR 2025 revealed that even a 0.1% poisoning rate during pre-training can persist into deployed models. Google's Threat Intelligence Group documented AI misuse by threat actors in 2025, showing its practical application in cyberattacks. These risks may slow adoption in regulated sectors, as buyers impose stricter permissions, narrower deployment scopes, or demand extensive validation before allowing autonomous actions in production systems.

Other drivers and restraints analyzed in the detailed report include:

- Chronic Cyber Workforce Shortage Accelerating AI Security Adoption

- Regulatory Mandates for AI-Driven Continuous Controls Monitoring

- Limited Explainability of Agentic AI Decisions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms held a 39.71% share in 2025, reflecting enterprise preference for integrated agentic orchestration across endpoint, cloud, identity, and network telemetry. This segment benefits from shared policy, memory, and unified response logic, simplifying autonomous actions at scale. Fragmented agent deployments are seen as a risk due to inconsistent decisions and duplicate actions. Services remained the second-largest component as many organizations require external support for deployment, workflow redesign, policy mapping, and model governance.

Service demand is increasingly recurring as buyers shift from one-time implementation to ongoing tuning and oversight. GitLab's 2025 public beta of the Duo Agent Platform highlighted how orchestration extends into development and security workflows, driving advisory and integration needs. Hardware accelerators are projected to grow at a 32.31% CAGR through 2031, driven by the need for local inference in latency-sensitive environments. This shift positions hardware as a key enabler of real-time autonomous defense in edge and high-speed settings, reducing reliance on slower cloud round-trip times.

Network security commanded a 28.23% share of the cybersecurity agentic AI market in 2025 because network telemetry still provides the broadest real-time view of east-west movement, lateral escalation, and policy violations. For many enterprises, the network layer remains the backbone that allows agentic systems to correlate behavior across assets and environments. Endpoint security also retained a strong position because it is often the easiest place to introduce autonomous investigation and guided remediation into an existing security stack. This has made endpoint platforms a common entry point for agentic adoption in the cybersecurity agentic AI market.

SentinelOne reported in March 2026 that its Purple AI autonomous investigation capability was included in over 50% of licenses sold in Q4 FY26, highlighting how endpoint vendors leverage their installed base to distribute agentic features. Cloud and SaaS security and IAM are also growing as organizations handle an increasing number of non-human identities and API-driven access paths. OT and IoT security, the fastest-growing segment at a 33.31% CAGR through 2031, is driven by the rapid convergence of digital and physical infrastructure. The cybersecurity agentic AI market is shifting toward platforms that interpret both network intent and operational context, rather than just detecting anomalies.

Geography Analysis

North America accounted for 34.86% of the cybersecurity agentic AI market in 2025, driven by its strong vendor base and early enterprise adoption. Policies promoting continuous monitoring and cyber resilience in regulated sectors further support growth. ISC2 reported in December 2025 that critical cybersecurity skill gaps in the region are boosting demand for platforms that reduce manual effort. Market growth is also tied to enterprise contract expansions, with customers adopting agentic functions through broader platform relationships rather than stand-alone purchases.

Asia-Pacific is projected to grow at a 32.71% CAGR through 2031, making it the fastest-growing regional market. This growth is fueled by rapid digital expansion, multi-cloud adoption, and concerns over AI-enabled attacks. Organizations in the region are scaling cyber defenses faster than they can expand skilled security teams. Critical infrastructure modernization and distributed environment monitoring also drive demand, though data localization rules and regulatory maturity may create uneven opportunities.

Europe ranked third in 2025, with demand focused on financial services, manufacturing, and critical infrastructure, where governance and documentation are as important as detection. Research published in AI and Ethics in 2026 highlighted Europe's emphasis on transparency and explainability, supporting demand for auditable autonomous systems. The Middle East and Africa are growing from a smaller base through digital transformation programs, while South America is gradually expanding amid rising ransomware threats and financial sector digitization. Both regions are in an early development stage,s but show increasing demand for scalable monitoring and response models.

- CrowdStrike Holdings Inc.

- Palo Alto Networks Inc.

- Darktrace plc

- SentinelOne Inc.

- IBM Corporation

- Microsoft Corporation

- Cisco Systems Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- Rapid7 Inc.

- Arctic Wolf Networks Inc.

- Sophos Ltd.

- Elastic N.V.

- Google LLC

- Amazon Web Services Inc.

- Accenture plc

- Noma Security

- Vectra AI

- Okta Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Real-Time Threat Mitigation via Autonomous Response Loops

- 4.2.2 Explosion of Machine-Generated Attack Surfaces in Multi-Cloud Environments

- 4.2.3 Regulatory Mandates for AI-Driven Continuous Controls Monitoring

- 4.2.4 Chronic Cyber Workforce Shortage Accelerating AI Security Adoption

- 4.2.5 Integration of LLM Agents in DevSecOps Pipelines

- 4.2.6 Growing Venture Funding for Specialized AI Security Startups

- 4.3 Market Restraints

- 4.3.1 Adversarial AI and Model Poisoning Risks

- 4.3.2 Limited Explainability of Agentic AI Decisions

- 4.3.3 High Computational Costs of Training Security-Specific Foundation Models

- 4.3.4 Fragmented Data Provenance Standards Across Jurisdictions

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software Platforms

- 5.1.2 Services (MDR, Advisory, Integration)

- 5.1.3 Hardware Accelerators (AI-Optimized Silicon, Sensors)

- 5.2 By Security Level

- 5.2.1 Network Security

- 5.2.2 Endpoint Security

- 5.2.3 Application Security

- 5.2.4 Cloud and SaaS Security

- 5.2.5 Identity and Access Management

- 5.2.6 OT / IoT Security

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Native

- 5.3.2 On-Premises

- 5.3.3 Hybrid

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Mid-Sized Enterprises

- 5.5 By Industry Vertical

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Government and Defense

- 5.5.4 IT and Telecom

- 5.5.5 Manufacturing

- 5.5.6 Retail and E-Commerce

- 5.5.7 Energy and Utilities

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 CrowdStrike Holdings Inc.

- 6.4.2 Palo Alto Networks Inc.

- 6.4.3 Darktrace plc

- 6.4.4 SentinelOne Inc.

- 6.4.5 IBM Corporation

- 6.4.6 Microsoft Corporation

- 6.4.7 Cisco Systems Inc.

- 6.4.8 Fortinet Inc.

- 6.4.9 Check Point Software Technologies Ltd.

- 6.4.10 Trend Micro Incorporated

- 6.4.11 Rapid7 Inc.

- 6.4.12 Arctic Wolf Networks Inc.

- 6.4.13 Sophos Ltd.

- 6.4.14 Elastic N.V.

- 6.4.15 Google LLC

- 6.4.16 Amazon Web Services Inc.

- 6.4.17 Accenture plc

- 6.4.18 Noma Security

- 6.4.19 Vectra AI

- 6.4.20 Okta Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment