|

시장보고서

상품코드

2061961

에이전트형 AI 프레임워크 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agentic AI Frameworks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

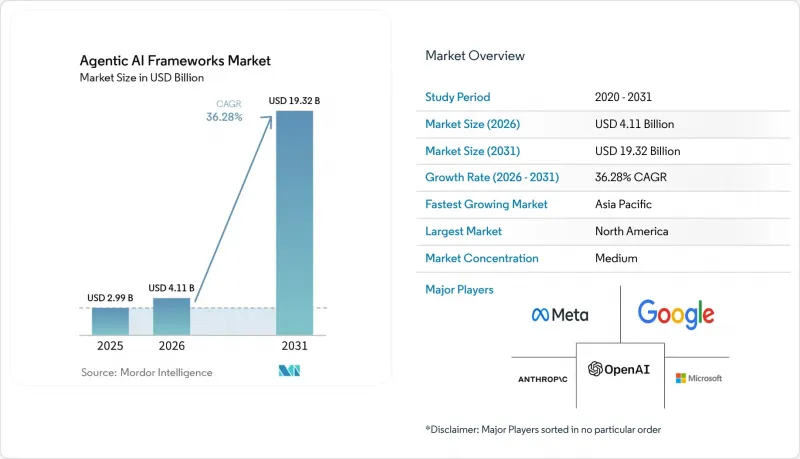

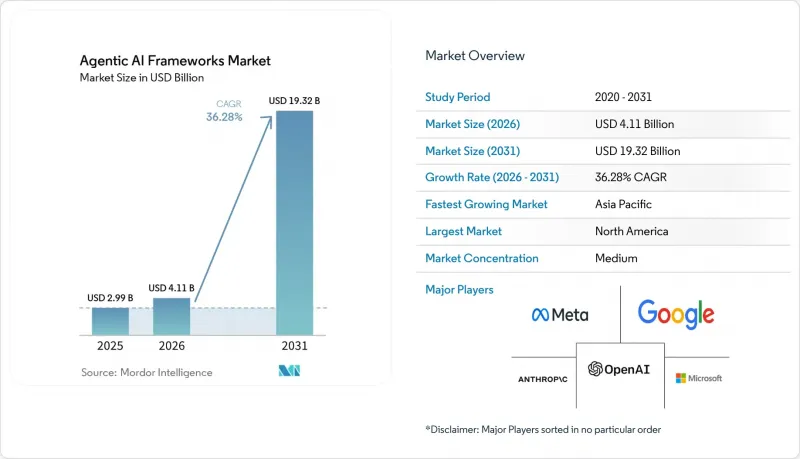

Mordor Intelligence에 의하면, 에이전트형 AI 프레임워크 시장 규모는 2025년 29억 9,000만 달러로 평가되었습니다. 2026년에는 41억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 36.3%로 성장을 지속하여, 2031년에는 193억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 프레임워크의 유형(오픈소스 프레임워크 및 독점 프레임워크), 배포 방식(클라우드 호스팅형 등), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(ICT 및 소프트웨어 개발, 헬스케어 및 생명과학, 소매 및 전자상거래 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 에이전트형 AI 프레임워크 시장 동향 및 인사이트

기업 워크플로우에서 자율형 에이전트에 대한 수요 증가

에이전트형 AI 프레임워크 시장에서 기업 수요는 독립적인 챗봇의 시범 도입 단계를 넘어, 팀 간 업무를 조정하는 본격적인 시스템으로 전환되고 있습니다. IBM은 2026년 5월, 경영진의 82%가 AI를 통한 가치 창출의 주요 장애물로 기능적 사일로화를 꼽았으며, 60%는 AI 에이전트가 부서 간 워크플로를 조정하는 차세대 제공 체계를 계획하고 있다고 보고했습니다. 이러한 변화로 인해 구매 행동도 변화하고 있습니다. 왜냐하면 기업들은 현재 기억, 도구 사용, 승인, 에스컬레이션 경로를 하나의 관리된 흐름으로 통합하기를 원하고 있기 때문입니다. 에이전트가 프롬프트에 하나씩 응답하는 것이 아니라, 부서 간 반복적인 업무 인계를 관리할 수 있을 때 그 가치가 극대화됩니다. 또한, 에이전트의 성과는 업무, 맥락, 책임 소재가 조직 내에서 어떻게 이동하는지에 따라 달라지기 때문에 이러한 경향은 조직으로 하여금 도입 전에 워크플로를 재설계하도록 유도하고 있습니다. 변경되지 않은 프로세스에 에이전트를 추가하는 프로젝트는 중단될 위험이 높기 때문에 에이전트형 AI 프레임워크 시장에서 워크플로우 아키텍처는 프레임워크 선정과 거의 동등한 중요성을 띠고 있습니다.

생성형 AI 모델 기능의 급속한 발전

모델의 급속한 발전으로 인해 에이전트형 AI 프레임워크 시장의 적용 범위가 확대되고 있습니다. 최첨단 모델은 더 강력한 도구 활용과 더 긴 컨텍스트 윈도우를 결합함으로써, 프로덕션 환경으로의 배포를 지연시키는 원인이 되는 수동 프롬프트 입력의 필요성을 줄이고 있습니다. 마이크로소프트는 2026년 4월 Microsoft Foundry를 통해 출시한 GPT-5.5에 대해, 보다 신뢰할 수 있는 에이전트형 실행, 더욱 강력한 장문 문맥 추론, 그리고 토큰 효율성 향상을 목표로 설계되었다고 밝혔습니다. 또한, 마이크로소프트는 Foundry를 통해 Claude Opus 4.6의 제공을 시작했습니다. 이 기능은 코딩, 에이전트 및 엔터프라이즈 워크플로우를 위해 100만 토큰 규모의 컨텍스트 윈도우를 제공합니다. 이러한 발전은 다단계 오케스트레이션을 더욱 안정적으로 만들고, 과거 에이전트 파이프라인을 제한적인 시범 프로젝트 수준으로만 머물게 했던 비용 부담을 줄이는 데 있어 중요한 의미를 지닙니다. 구글 딥마인드는 최대 규모의 훈련 실행에 활용 가능한 컴퓨팅 자원이 2012년부터 2018년 사이에 약 30만 배 증가했으며, 2024년까지 매년 약 4배의 속도로 계속 성장했다고 지적하고 있습니다. 이는 능력과 효율이 연동되어 향상되고 있는 이유를 설명하는 한 가지 요인이 됩니다.

AI의 안전성과 정합성에 대한 뿌리 깊은 우려

안전성과 정렬 문제는 여전히 에이전트형 AI 프레임워크 시장에 있어 구조적인 걸림돌로 작용하고 있습니다. 왜냐하면, 다중 에이전트의 오류는 메모리, 도구, 연쇄적인 의사결정을 통해 복합적으로 악화될 가능성이 있기 때문입니다. 세계경제포럼은 특히 시스템이 비즈니스 프로세스 내에서 더욱 자율적으로 작동하게 됨에 따라, AI 에이전트의 평가와 거버넌스를 위해서는 여전히 보다 견고한 기반이 필요하다고 밝혔습니다. 위험은 단순히 잘못된 답변에만 국한되지 않습니다. 에이전트가 권한을 상승시키거나, 데이터를 유출하거나, 혹은 여러 차례의 인수인계를 거친 후 추적하기 어려운 행동을 유발할 가능성이 있기 때문입니다. 따라서 규제 대상인 구매 기업은 도입 규모를 확대하기 전에 감사 기록, 인적 감시 및 실행 시 통제에 주력할 수밖에 없습니다. 2026년 8월 EU AI법의 고위험 조항이 발효됨에 따라, 규정 준수 문서 및 사고 기록이 필요한 기업들은 더욱 각별한 주의를 기울여야할 것입니다. 보안 팀이 다른 엔터프라이즈 시스템과 마찬가지로 에이전트의 동작을 확신하며 모니터링할 수 있게 될 때까지는 에이전트형 AI 프레임워크 시장의 일부 고부가가치 도입 사례가 기술 자체의 발전 속도보다 뒤처지게 될 것입니다.

부문별 분석

2025년 기준으로, 오픈소스 프레임워크는 에이전트형 AI 프레임워크 시장의 63.81%를 차지했습니다. 이러한 우위는 모델, 벡터 스토어 및 엔터프라이즈 데이터 시스템 전반에 걸친 구성 가능성, 감사 가능성, 그리고 폭넓은 통합성을 개발자들이 선호했기 때문입니다. LangChain은 2025년 10월, LangChain과 LangGraph의 월간 다운로드 수가 합계 9,000만 건에 달했으며, 포춘 500대 기업의 35%가 자사의 서비스를 이용하고 있다고 발표했습니다. 이번 업데이트에서는 대기업의 운영 환경에서의 활용에 대해서도 언급되어 있으며, 이는 구매자가 나중에 상용 지원 서비스를 구매하더라도 오픈소스 도구가 여전히 엔지니어링 표준을 형성하고 있는 이유를 설명하는 요인 중 하나입니다.

오픈소스의 주도권은 그 자체로 발생하는 마찰을 해소해 주지는 않습니다. 왜냐하면, 급속한 릴리스 주기나 API 호환성을 해치는 변경 사항은 이미 운영 중인 팀에 내부적인 재작업이 발생할 가능성이 있기 때문입니다. 이러한 불안정성이 프로prietary 벤더들이 운영 환경에서 격차를 좁히는 데 한 요인이 되고 있으며, 프로prietary 프레임워크는 2031년까지 연평균 성장률(CAGR) 36.68%를 나타낼 것으로 예측됩니다. 마이크로소프트는 Foundry Agent Service가 LangGraph, Claude Agent SDK 및 OpenAI Agents SDK를 단일 거버넌스 기반 런타임에서 지원한다고 밝혔으며, 이는 엔터프라이즈 벤더들이 관리되는 환경 내에서 프레임워크의 유연성을 어떻게 패키징하고 있는지를 보여줍니다. 실제로 에이전트형 AI 프레임워크 시장은 실험을 주도하는 오픈소스 도구와, 구매자가 서비스 수준, 감사 가능성 및 중앙 집중식 제어를 필요로 할 때 입지를 넓혀가는 독점 플랫폼으로 양분되고 있습니다.

2025년 기준으로, 에이전트형 AI 프레임워크 시장의 71.32%를 클라우드 호스팅 방식이 차지했습니다. 매니지드 서비스는 설정 시간을 단축하고, 최첨단 모델에 신속하게 접근할 수 있게 하며, 변동하는 에이전트 워크로드에 맞추어 확장할 수 있기 때문에 클라우드는 여전히 기본 선택지로 자리 잡고 있습니다. Google Cloud는 2026년 4월, Agent Studio, Agent Development Kit, Agent Runtime, Agent Identity, Agent Gateway를 포함한 ‘Gemini Enterprise Agent Platform’을 출시하며, 벤더가 개발과 거버넌스를 단일 서비스로 패키지화한 사례를 보여주었습니다. 마이크로소프트 역시 Foundry 및 Microsoft 365의 에이전트 도구를 확충하여, 신속한 반복 개발과 표준 비즈니스 워크플로우 분야에서 클라우드 분야의 리더십을 강화했습니다.

On-Premise 및 엣지 배포용 에이전트형 AI 프레임워크 시장 규모는 2031년까지 연평균 성장률(CAGR) 36.63%로 확대될 것으로 전망됩니다. 이러한 성장은 데이터 주권, 저지연 추론, 독자적인 워크플로우 보호 등 퍼블릭 클라우드로는 완전히 해결할 수 없는 요구 사항을 반영한 것입니다. 소규모 작업 특화형 모델과 양자화된 변형 모델 덕분에 On-Premise와 호스팅형 배포 간의 기능 격차가 줄어들고 있어, 엣지 도입의 기존 장벽 중 하나가 해소되고 있습니다. 그 결과, 기업들은 개발 및 일상적인 워크플로를 클라우드에서 유지하면서, 기밀성이 높거나 시간적 제약이 엄격한 이용 사례를 On-Premise나 엣지 환경으로 이전하는 등 아키텍처 분할이 진행되고 있습니다.

지역별 분석

2025년, 북미는 전 세계 에이전트형 AI 프레임워크 시장 점유율의 37.51%를 차지했습니다. 미국은 가장 풍부한 기업용 AI 예산, 가장 높은 벤더 집중도, 그리고 하이퍼스케일러 생태계와의 가장 긴밀한 연계성을 모두 갖추고 있어 여전히 단일 최대 시장으로 자리 잡고 있습니다. 이를 통해 인프라 모델 제공업체, 클라우드 플랫폼 및 기업 구매자 간에 신속한 피드백 루프가 형성되어, 해당 지역은 다른 지역보다 더 빠르게 새로운 오케스트레이션 도구를 운영 환경에 도입할 수 있게 되었습니다. 캐나다는 AI 클러스터를 통해 연구의 깊이를 더하고 있는 반면, 멕시코는 이중언어 운영 워크플로우를 위한 니어쇼어 거점으로서 그중요성이 커지고 있습니다.

2025년, 유럽은 전 세계 에이전트형 AI 프레임워크 시장에서 상당한 점유율을 차지했습니다. 독일, 영국, 프랑스 수요는 산업 프로세스, 기업 소프트웨어의 워크플로우, 그리고 규제 대상 업무 기능을 위한 프로덕션 환경 수준의 오케스트레이션에 집중되어 있습니다. 해당 지역에서의 조달 과정에서는 데이터 주권, 프라이빗 클라우드 도입, 감사 대응이 가능한 문서화가 유례없이 중시되고 있으며, 이로 인해 구매자들은 보다 체계적인 플랫폼을 선택하게 되고 있습니다. 앞으로 시행될 고위험 AI에 관한 규제는 수요를 사라지게 하는 것은 아니지만, 맞춤 설정을 최소화하는 한편, 조치, 제어 및 인적 감독을 문서화할 수 있는 프레임워크로 지출을 전환하는 요인이 되고 있습니다.

아시아태평양의 에이전트형 AI 프레임워크 시장은 2031년까지 연평균 성장률(CAGR) 37.28%를 기록하며 성장할 것으로 전망됩니다. 중국은 AI 에이전트의 보급 및 산업 도입에 관한 국가 목표를 통해 이를 적극적으로 추진하고 있는 반면, 일본은 2026년 5월 제정된 ‘AI 촉진법’을 활용하여, 위험 기반이면서도 혁신 지향적인 생산 도입을 위한 로드맵을 지원하고 있습니다. 인도는 첨단 소프트웨어 공학 전문 지식과 대규모 서비스 인프라를 강점으로 삼고 있으며, 이것이 아웃소싱 및 금융 워크플로우 분야에서 오픈소스 도입을 뒷받침하고 있습니다. 중동에서는 아랍에미리트와 사우디아라비아의 국가 AI 프로그램을 통해 그 기세가 점점 더 커지고 있는 반면, 남미에서는 브라질과 아르헨티나가 초기 진출 거점으로서 중심적인 역할을 하고 있습니다. 이 지역 전반에 걸쳐, 주권에 관한 규제와 현지 운영 요구 사항은 단순한 장벽이 아니라, 에이전트형 AI 프레임워크 시장을 감사하기 쉽고 현지 상황에 더 잘 적응할 수 있는 도입 모델로 이끄는 원동력이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the agentic AI frameworks market size is expected to grow from USD 2.99 billion in 2025 to USD 4.11 billion in 2026 and is forecast to reach USD 19.32 billion by 2031 at 36.3% CAGR over 2026-2031.

This report is Segmented by Framework Type (Open-Source Frameworks, and Proprietary Frameworks), Deployment Mode (Cloud-Hosted, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (ICT and Software Development, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI Frameworks Market Trends and Insights

Growing Demand for Autonomous Agents in Enterprise Workflows

Enterprise demand in the agentic AI frameworks market has moved beyond isolated chatbot pilots and into production systems that coordinate work across teams. IBM reported in May 2026 that 82% of C-suite executives identified functional silos as the main barrier to AI value extraction, and 60% planned next-generation delivery structures in which AI agents coordinate workflows across departments. That shift changes buying behavior because enterprises now want memory, tool use, approvals, and escalation paths in one governed flow. The value case is strongest where agents can manage repetitive handoffs between departments instead of answering one prompt at a time. This is also pushing organizations to redesign workflows before deployment, since agent performance depends on how tasks, context, and accountability move across the business. Projects that add agents to unchanged processes face a higher cancellation risk, so workflow architecture is becoming nearly as important as framework selection in the agentic AI frameworks market.

Rapid Advances in Generative AI Model Capabilities

Rapid model progress is widening the production scope of the agentic AI frameworks market. Frontier models now combine stronger tool use with longer context windows, reducing the manual prompting required to slow production deployment. Microsoft said its April 2026 release of GPT-5.5 on Microsoft Foundry was designed for more reliable agentic execution, stronger long-context reasoning, and better token efficiency. Microsoft also made Claude Opus 4.6 available in Foundry, with a 1-million-token context window for coding, agents, and enterprise workflows. These gains matter because they make multi-step orchestration more stable and lower the cost penalty that once limited agent pipelines to narrow pilots. Google DeepMind noted that compute available for the largest training runs rose by around 300,000x between 2012 and 2018 and continued to grow at an annual pace of around 4x through 2024, which helps explain why capability ceilings and efficiency are moving together.

Persistent Concerns Around AI Safety and Alignment

Safety and alignment remain a structural brake on the agentic AI frameworks market because multi-agent errors can compound across memory, tools, and chained decisions. The World Economic Forum said that evaluation and governance for AI agents still need stronger foundations, especially as systems operate with greater autonomy within business processes. The risk is not limited to wrong answers, since agents can also escalate privileges, expose data, or trigger actions that are hard to trace after several handoffs. This keeps regulated buyers focused on audit trails, human oversight, and runtime controls before they scale deployment. The August 2026 activation of the EU AI Act high-risk provisions adds another layer of caution for enterprises that need conformity documentation and incident logging. Until security teams can monitor agent behavior with the same confidence they apply to other enterprise systems, some high-value deployments in the agentic AI frameworks market will move more slowly than the technology itself.

Other drivers and restraints analyzed in the detailed report include:

- Rising Investments by Big Tech and Venture Capital

- Scalability Benefits of Framework-Agnostic Tooling

- Lack of Skilled Workforce for Multi-Agent Orchestration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Open-source frameworks held 63.81% of the agentic AI frameworks market share in 2025. That lead came from developers' preference for composability, auditability, and broad integration across models, vector stores, and enterprise data systems. LangChain said in October 2025 that LangChain and LangGraph reached 90 million combined monthly downloads and that 35% of Fortune 500 companies used its services. The same update pointed to production use across large enterprises, which helps explain why open-source tools still shape engineering standards even when buyers later purchase commercial support.

Open-source leadership does not remove its own friction, since rapid release cycles and breaking API changes can create internal rework for teams already in production. That instability is helping proprietary vendors close the production gap, and proprietary frameworks are projected to grow at a 36.68% CAGR through 2031. Microsoft said the Foundry Agent Service supports LangGraph, the Claude Agent SDK, and the OpenAI Agents SDKs in a single, governed runtime, demonstrating how enterprise vendors are packaging framework flexibility within managed environments. In practice, the agentic AI frameworks market is separating into open-source tools that lead experimentation and proprietary platforms that gain ground when buyers need service levels, auditability, and centralized controls.

Cloud-hosted deployments held 71.32% of the agentic AI frameworks market in 2025. Cloud remains the default because managed services shorten setup time, provide fast access to frontier models, and scale with variable agent workloads. Google Cloud launched the Gemini Enterprise Agent Platform in April 2026, including Agent Studio, Agent Development Kit, Agent Runtime, Agent Identity, and Agent Gateway, demonstrating how platform vendors are packaging development and governance as a single service. Microsoft made similar moves by expanding Foundry and Microsoft 365 agent tooling, reinforcing its cloud leadership in rapid iteration and standard business workflows.

The agentic AI frameworks market size for on-premises and edge deployments is projected to expand at 36.63% CAGR through 2031. That growth reflects needs that public cloud cannot fully solve, including data sovereignty, low-latency inference, and protection of proprietary workflows. Smaller task-specific models and quantized variants are narrowing the capability gap between local and hosted deployments, reducing one of the old barriers to edge adoption. The result is an architecture split in which enterprises keep development and routine workflows in the cloud, while moving sensitive or time-critical use cases to on-premises and edge environments.

Geography Analysis

North America held 37.51% of the global agentic AI frameworks market share in 2025. The United States remains the single largest national market because it combines the deepest enterprise AI budgets, the highest vendor concentration, and the closest links to hyperscaler ecosystems. This creates a fast feedback loop among foundation model providers, cloud platforms, and enterprise buyers, enabling the region to deploy new orchestration tools to production faster than peers. Canada adds research depth through its AI clusters, while Mexico is gaining relevance as a near-shore deployment base for bilingual operational workflows.

Europe accounted for a substantial share of the global agentic AI frameworks market in 2025. Demand in Germany, the United Kingdom, and France centers on production-grade orchestration for industrial processes, enterprise software workflows, and regulated business functions. Procurement in the region places unusual emphasis on data sovereignty, private cloud deployment, and audit-ready documentation, which pushes buyers toward more structured platform choices. The coming enforcement of high-risk AI rules is not removing demand, but it is redirecting spend toward frameworks that can document actions, controls, and human oversight with less customization.

The agentic AI frameworks market in Asia-Pacific is projected to grow at a 37.28% CAGR through 2031. China is accelerating adoption through national targets for AI agent penetration and industrial deployment, while Japan is using its May 2026 AI Promotion Act to support a risk-based, yet innovation-oriented, path to production. India benefits from deep software engineering expertise and a large services base, which supports open-source adoption in outsourcing and financial workflows. The Middle East is building momentum through national AI programs in the United Arab Emirates and Saudi Arabia, while South America remains centered on Brazil and Argentina as early entry points. Across these regions, sovereignty rules and local operating needs are not simply barriers; they are steering the agentic AI frameworks market toward more auditable and locally adaptable deployment models.

- OpenAI LLC

- Microsoft Corporation

- Google LLC

- Anthropic PBC

- Meta Platforms Inc.

- Amazon.com Inc.

- Hugging Face Inc.

- NVIDIA Corporation

- IBM Corporation

- Salesforce Inc.

- Cohere Inc.

- Adept AI Labs Inc.

- Replit Inc.

- Pinecone Systems Inc.

- LangChain Inc.

- Inflection AI Inc.

- Mistral AI SAS

- LangFuse GmbH

- Conductor Technologies Inc.

- Cerebras Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Autonomous Agents in Enterprise Workflows

- 4.2.2 Rapid Advances in Generative AI Model Capabilities

- 4.2.3 Rising Investments by Big Tech and Venture Capital

- 4.2.4 Scalability Benefits of Framework-Agnostic Tooling

- 4.2.5 Emergence of AI Function Calling Standards

- 4.2.6 Integration of Agentic Frameworks into Low-Code Platforms

- 4.3 Market Restraints

- 4.3.1 Persistent Concerns Around AI Safety and Alignment

- 4.3.2 Lack of Skilled Workforce for Multi-Agent Orchestration

- 4.3.3 High Compute Costs for Large-Scale Agent Simulations

- 4.3.4 Fragmentation Due to Divergent Prompt Engineering Dialects

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Framework Type

- 5.1.1 Open-Source Frameworks

- 5.1.2 Proprietary Frameworks

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Hosted

- 5.2.2 On-Premises and Edge

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 ICT and Software Development

- 5.4.2 Financial Services

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing and Industrial

- 5.4.5 Retail and E-Commerce

- 5.4.6 Media and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 OpenAI LLC

- 6.4.2 Microsoft Corporation

- 6.4.3 Google LLC

- 6.4.4 Anthropic PBC

- 6.4.5 Meta Platforms Inc.

- 6.4.6 Amazon.com Inc.

- 6.4.7 Hugging Face Inc.

- 6.4.8 NVIDIA Corporation

- 6.4.9 IBM Corporation

- 6.4.10 Salesforce Inc.

- 6.4.11 Cohere Inc.

- 6.4.12 Adept AI Labs Inc.

- 6.4.13 Replit Inc.

- 6.4.14 Pinecone Systems Inc.

- 6.4.15 LangChain Inc.

- 6.4.16 Inflection AI Inc.

- 6.4.17 Mistral AI SAS

- 6.4.18 LangFuse GmbH

- 6.4.19 Conductor Technologies Inc.

- 6.4.20 Cerebras Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment