|

시장보고서

상품코드

2064514

엣지 AI 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Edge AI Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

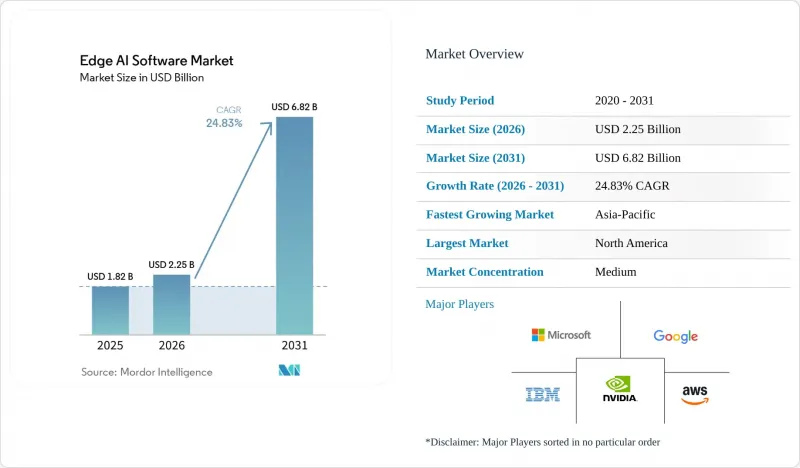

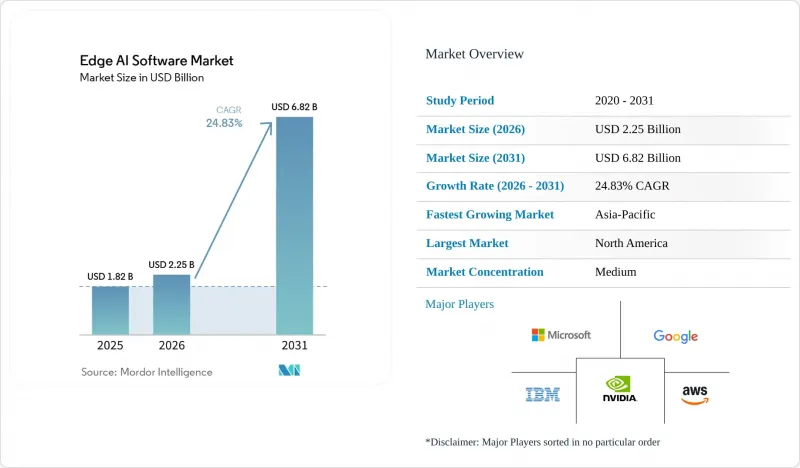

Mordor Intelligence에 의하면, 엣지 AI 소프트웨어 시장 규모는 2025년에 18억 2,000만 달러로 평가되었습니다. 2026년에 22억 5,000만 달러에서 2031년까지 68억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 24.83%를 나타낼 전망입니다.

본 보고서는 제공 형태(솔루션 및 서비스), 데이터 모달리티(시각 데이터, 청각 데이터, 텍스트 및 언어 데이터, 환경 및 위치 정보 데이터, 멀티모달 데이터), 도입 형태(클라우드, On-Premise 등), 최종 사용자 산업(제조, 의료, 소매 및 소비재, 에너지 및 유틸리티 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 엣지 AI 소프트웨어 시장 동향 및 인사이트

IoT 엔드포인트 데이터의 급증

산업 및 기업의 엔드포인트에서 생성되는 기계 데이터의 양이 방대해지면서, 클라우드 중계 아키텍처로는 이를 효율적으로 처리할 수 없게 되자 엣지 AI 소프트웨어 시장이 성장세를 보이고 있습니다. 2026년 5월 『Discover Computing』지에 게재된 ELARA 프레임워크에 관한 연구에 따르면, 대규모 IoT 네트워크 전체에서 종단 간 지연 시간이 39-52밀리초, 대역폭 감소율이 최대 48%, 작업 완료율이 93-98%인 것으로 나타났습니다. 이는 시간적 제약이 있는 워크로드에 대한 로컬 처리를 직접 지원하는 기능입니다. 이 결과는 중요한 의미를 지닙니다. 왜냐하면 산업용 시스템은 수천 개의 노드에 걸쳐 1Hz 이상의 빈도로 센서 스트림을 전송할 가능성이 있으며, 배포 규모가 확대됨에 따라 원시 텔레메트리 데이터를 집계형 인프라로 전송하는 비용이 급격히 증가하기 때문입니다. 또한, 시스코의 『State of Wireless Report 2026』에 따르면, IoT의 성장은 사용자의 이동성 및 고대역폭 용도 도입을 앞지르며, 기업의 무선 투자에 있어 가장 큰 촉진요인으로 꼽혔습니다. 이는 네트워크에 대한 지출이 단순한 연결성 확장이 아니라 엔드포인트의 지능에 의해 형성되고 있음을 보여줍니다. 이러한 상황에서 엣지 AI 소프트웨어 시장이 수혜를 입는 이유는 기업들이 어떤 데이터를 업스트림로 전송해야 할지 결정하기 전에 로컬에서 데이터를 필터링하고, 맥락을 파악하며, 조치를 취할 수 있는 소프트웨어를 필요로 하기 때문입니다. 또한, 네트워크의 순용량만으로는 해당 요건을 충족할 수 없습니다.

엣지 환경에서의 저지연 의사결정에 대한 수요

엣지 AI 소프트웨어 시장은 제조, 자율 시스템, 공공 서비스, 공공 안전 등 각 분야에서 실시간 의사 결정이 필요한 이용 사례에 힘입어 성장하고 있습니다. 지연 시간의 허용 범위가 50밀리초 미만으로 떨어지거나, 사이트의 텔레메트리 데이터가 하루에 1테라바이트에 달하면, 로컬 추론은 설계상의 선택지가 아니라 실용적인 필수 요건이 됩니다. NVIDIA와 T-Mobile은 2026년 3월, NVIDIA Metropolis 플랫폼을 활용해 분산형 5G 엣지 네트워크 상에서 물리적 AI 용도를 통합할 것이라고 발표했습니다. 여기에는 스마트 시티 운영, 유틸리티의 자동 점검, 그리고 운영상 응답 속도가 매우 중요한 산업 안전 워크로드 등이 포함됩니다. 또한, 휴렛팩커드 엔터프라이즈(HPE)도 2026년 3월에 ‘HPE AI Grid’를 출시하여 분산된 추론 사이트 전반에 걸쳐 예측 가능한 저지연 성능을 제공했습니다. 또한, 컴캐스트는 소형 언어 모델을 활용한 자사 네트워크 상에서의 실시간 엣지 추론 현장 테스트를 시작했습니다. 따라서 엣지 AI 소프트웨어 시장은 제한적인 연산 환경에서도 추론 성능을 안정적으로 유지할 수 있는 플랫폼으로 전환되고 있습니다. 벤치마크용 하드웨어에서의 평균 처리량보다, 실제 사용 시점에서의 결정론적 동작이 더 중요하게 여겨지기 때문입니다.

서로 다른 에지 환경의 통합에 수반되는 복잡성

엣지 AI 소프트웨어 시장은 여전히 큰 운영상의 장벽에 직면해 있습니다. 그 이유는 대부분의 기업 도입 환경이 서로 다른 프로세서 유형, 운영 체제, 연결 환경을 아우르고 있기 때문입니다. 2026년 『Sensors』지에 게재된 MIGS 아키텍처에 관한 조사에 따르면, 이종 디바이스의 통합을 위해서는 Modbus, OPC UA, MQTT를 동시에 처리할 수 있는 프로토콜 독립형 미들웨어가 필요하다는 사실이 밝혀졌습니다. 이는 실제 산업 환경에서 상호 운용성이 여전히 얼마나 어려운지를 보여줍니다. ZEDEDA의 2026년 조사 결과에서도 유사한 문제가 지적되었으며, 기업의 41%가 분산 워크로드 관리를 주요 과제로 꼽았고, 47%는 서로 다른 하드웨어 환경 전반에 걸쳐 일관된 거버넌스가 필요한 하이브리드 클라우드·엣지 아키텍처를 채택하고 있다고 보고했습니다. 이로 인해 엣지 AI 소프트웨어 시장에서는 양극화가 나타나고 있습니다. 표준화된 장비군을 보유한 대기업은 신속하게 규모를 확대할 수 있는 반면, 구식 운영 기술을 보유한 인수 기업은 도입 주기가 길어지고 통합 비용이 높아지는 경향이 있기 때문입니다. 이 분야에서 보다 범용적인 하드웨어 추상화 계층이 개발되기 전까지는 상호 운용성이 도입 속도와 소프트웨어 표준화에 있어 구조적인 걸림돌로 남아 있을 것입니다.

부문별 분석

2025년, 솔루션은 엣지 AI 소프트웨어 시장 점유율의 62.72%를 차지하며, 기업들이 모듈형 계약 모델보다 통합 플랫폼을 선호함에 따라 계속해서 주도적인 위치를 유지했습니다. 이러한 경향은 제조업체, 통신 사업자 및 기타 대규모 사용자들이 추론 런타임, 압축 도구, 배포 오케스트레이션을 하나의 제품에 통합한 검증된 패키지를 원하고 있다는 실질적인 구매 경향을 반영하고 있습니다. 구매자들이 일반적으로 이러한 접근 방식을 선호하는 이유는 에지 환경에서의 상호 운용성에 대한 불확실성을 줄이고, 서로 다른 공급업체의 도구를 조합해야 하는 부담을 덜 수 있기 때문입니다. 엣지 AI 소프트웨어 시장에서 이러한 추세는 플랫폼 제공업체들에게 초기 수익 면에서 우위를 안겨주었습니다. 왜냐하면 그들은 제한적인 기능뿐만 아니라 완전한 운영 레이어를 판매할 수 있기 때문입니다. 또한, 이러한 동향은 엣지 AI 소프트웨어 시장이 시범 도입 단계를 벗어났음을 보여줍니다. 왜냐하면 조달 팀은 대개 사내 팀이 장기적인 운영을 위한 명확한 방향을 확정한 후에야 번들 솔루션을 표준화하기 때문입니다.

서비스 시장은 2031년까지 연평균 성장률(CAGR) 25.64%로 확대될 것으로 예상되며, 그 성장 속도는 엣지 AI 소프트웨어 시장 전체를 상회하고 있습니다. 이러한 차이는 초기 소프트웨어 스택 도입 이후의 배포 관리 방식에 변화가 생기고 있음을 보여줍니다. 많은 기업은 분산된 자산 전반에 걸친 모델 드리프트를 관리하는 데 필요한 사내 엔지니어링 팀을 보유하고 있지 않기 때문에 엣지 MLOps, 모델 최적화, 라이프사이클 관리 및 전체 자산에 걸친 가시성을 외부에 위탁하는 경향이 강해지고 있습니다. 지멘스는 2026년 4월, 여러 공장 거점에 걸친 모델 훈련, 배포, 재훈련 및 AI 모델 관리를 포괄하는 ‘Industrial AI Suite on Siemens Industrial Edge’의 제공 범위를 확대하겠다고 발표하며, 이러한 전환을 보다 구체적으로 제시했습니다. 2026년에 구글이 iOS Swift, JavaScript, Android API 전반에 걸쳐 LiteRT-LM 지원을 확대한 것은 모바일 환경에서도 동일한 방향성을 보여주고 있습니다. 그곳에서는 런타임이 독립형 소프트웨어 제품이라기보다는 내장형 관리 계층처럼 작동하는 경향이 점점 더 강해지고 있습니다.

따라서 엣지 AI 소프트웨어 시장에서는 제품 및 서비스의 경제성이 점차 융합되고 있지만, 이 두 가지 범주는 여전히 별도로 보고되고 있습니다. 많은 기업에게 통합 솔루션은 여전히 가장 먼저 구매하는 대상이지만, 도입이 시범 운영 단계에서 본격적인 운영 단계로 넘어가면 서비스 계층의 중요성이 커집니다. 이는 특히 2023년과 2024년에 엣지 하드웨어를 도입한, 사내 AI 인력이 아직 부족한 중견 산업 사용자들 사이에서 두드러지게 나타납니다. 그 결과, 엣지 AI 소프트웨어 업계는 단순한 라이선스 기반의 소프트웨어 제공을 넘어, 패키지화된 소프트웨어와 지속적인 운영 지원을 결합한 라이프사이클 플랫폼으로 발전하고 있습니다.

2025년에는 비주얼 데이터가 매출의 29.98%를 차지하며, 엣지 AI 소프트웨어 시장에서 가장 큰 모달리티가 되었습니다. 이러한 우위는 공장 검사, 보안 감시, 자동차용 인식 시스템 분야에서 수년에 걸쳐 컴퓨터 비전을 도입해 온 결과로 구축된 것입니다. 많은 엔드포인트에서 여전히 실시간으로 분석되지 않은 영상이 수집되고 있기 때문에 전 세계에 설치된 카메라 기반 시설은 계속해서 큰 수요의 원천이 되고 있습니다. NVIDIA는 2026년 전 세계에 15억 대 이상의 카메라가 설치될 것으로 예상되는 반면, 그중 1% 미만에서만 의미 있는 실시간 분석이 이루어지고 있다고 지적했습니다. 이는 로컬 시각 추론 프레임워크에 여전히 큰 기회가 남아 있음을 시사합니다. 엣지 AI 소프트웨어 시장의 경우, 이는 시각적 워크로드가 여전히 현재 수익의 기반을 이루고 있음을 의미합니다. 왜냐하면, 이러한 항목들은 품질 관리, 안전 감시, 자동 검사 등 기업에서 이미 정립된 지출 항목과 직접적으로 연결되어 있기 때문입니다.

최종 사용자가 로컬에서 처리하고자 하는 정보의 유형이 다양해짐에 따라, 다른 데이터 모달리티도 확대되고 있습니다. 텍스트 및 언어 데이터는 인간-기계 인터페이스와 로컬 대화 기능을 지원하며, 환경 데이터 및 위치 데이터는 모니터링, 경로 안내, 인프라 활용 사례와 관련이 있습니다. 각 데이터 스트림마다 개별 모델에 의존하지 않고 여러 입력을 동시에 해석할 수 있는 단일 스택을 추구하는 기업이 늘어나고 있어, 멀티모달 AI는 전략적으로 중요해지고 있습니다. 2026년 5월에 출시된 NVIDIA의 ‘Nemotron 3 Nano Omni’ 모델은 시각, 언어, 음성 인식 기능을 하나의 소형 모델에 통합했으며, 에이전트형 엣지 워크로드를 위해 설계되었는데, 이는 더욱 통합된 추론 아키텍처로의 전환을 반영한 것입니다. 엣지 AI 소프트웨어 시장은 이러한 혜택을 누리고 있습니다. 이는 고객이 더욱 풍부한 지역적 맥락을 필요로 하는 반면, 리소스가 제한된 기기에서 여러 개의 완전한 소프트웨어 스택을 지원할 수 없는 경우, 멀티모달 모델이 운영상의 복잡성을 단순화할 수 있기 때문입니다.

음성 데이터 시장은 2031년까지 연평균 성장률(CAGR) 26.88%로 확대될 것으로 예상되며, 엣지 AI 소프트웨어 시장에서 가장 빠르게 성장하는 분야로 자리매김하고 있습니다. 가장 큰 수요는 회전 기계의 이상 소리 감지, 창고 로봇의 음성 명령 인터페이스, 그리고 의료 및 은행 업계에서 즉각적인 응답성이 요구되는 대화형 시스템에서 발생하고 있습니다. 음성 워크로드에는 비용 면에서도 장점이 있습니다. 왜냐하면 모델은 동등한 시각 시스템보다 크기가 작은 경우가 많기 때문에 더 간소한 하드웨어 구성으로도 실행할 수 있기 때문입니다. 이로 인해, 대규모 엔드포인트 기기군에 이미 MCU급 장치를 도입한 산업용 OEM 제조업체의 경우, 도입 장벽이 낮아집니다. 앞으로 엣지 AI 소프트웨어 업계에서는 시각적 추론에 종종 필요한 대규모 연산 자원을 요구하지 않으면서도 실질적인 성능 향상을 가져다주기 때문에 음성 및 멀티모달 이용 사례의 중요성이 점점 더 커질 것으로 보입니다.

지역별 분석

2025년, 북미는 엣지 AI 소프트웨어 시장 점유율의 34.78%를 차지하며 여전히 최대 지역 기여자로서의 위상을 유지했습니다. 이 지역은 하이퍼스케일러의 플랫폼과 산업용 기술 공급업체가 밀집해 있다는 장점을 가지고 있어, 덕분에 기업 구매자들은 다른 대부분의 지역보다 더 빨리 풀스택 도입 옵션을 이용할 수 있게 되었습니다. 또한, 북미의 엣지 AI 소프트웨어 시장은 성숙한 기업 소프트웨어의 조달 주기로부터도 혜택을 받고 있습니다. 이 지역에서는 대규모 조직들이 시범 검증을 거친 후, 여러 거점으로 사업을 확대하는 데 자금을 투자하려는 의지가 높아지고 있습니다. 2026년 3월 HPE의 ‘AI Grid’ 출시와 Comcast의 분산형 엣지 추론 현장 시험은 관련 활동이 공장을 넘어 통신 인프라 및 소비자 대상 서비스 제공 네트워크로 확대되고 있음을 보여주었습니다. 또한, 2026년 5월 IBM이 ‘Sovereign Core’를 출시한 것은 디지털 주권과 운영 관리가 정부 및 규제 대상 기업 수요 모두에 영향을 미치고 있는 조달 환경을 반영하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 26.71%로 확대될 것으로 예상되며, 엣지 AI 소프트웨어 시장에서 가장 빠르게 성장하는 지역 부문이 될 것입니다. 이러한 기세는 중국의 제조 규모, 일본의 로봇 공학 및 자동차 관련 프로그램, 인도의 엔지니어링 기반, 그리고 한국의 반도체 생태계에 의해 뒷받침되고 있습니다. 닛케이 신문은 2026년 3월, 후지 키메라 종합연구소의 조사 결과를 인용하여, 2026년 이후 일본 시장에서는 AI 에이전트와 엣지 기반의 물리적 AI 추론이 시장 성장을 주도할 것이라고 보도했습니다. 개인정보 보호와 AI 에이전트의 상용화라는 두 가지 측면에서 엣지 환경의 중요성이 높아지고 있다고 합니다. 이러한 성장 추세가 중요하게 여겨지는 이유는 아시아태평양의 엣지 AI 소프트웨어 시장이 대규모 산업 도입 규모와 AI 기능을 디바이스 계층에 더 가깝게 통합할 수 있는 현지 설계 생태계, 이 두 가지 요인과 모두 밀접하게 연관되어 있기 때문입니다. 또한, 이는 지역 벤더와 전 세계 공급업체들이 소프트웨어 기능뿐만 아니라 비용 효율성, 현지화, 하드웨어와의 호환성 등이 중요하게 여겨지는 환경에서 경쟁하고 있음을 의미합니다.

유럽은 견고한 산업 기반과 구매자 주도의 AI 도입 모델을 장려하는 규제 환경을 모두 갖추고 있어, 엣지 AI 소프트웨어 시장에서 계속해서 중요한 점유율을 유지하고 있습니다. 도이치 텔레콤의 ‘European Edge Continuum’은 2025년에 라이브 랩 및 사전 생산 단계로 전환될 예정이며, 2026년에는 상용화를 향해 추진되고 있습니다. 이는 연합형이며 상호 운용 가능한 엣지 인프라 계층을 통해 유럽의 디지털 주권 의제를 지원하는 것입니다. 시스코는 또한 2025년 3월 볼링거 호페 공장에서 지멘스와 공동으로 진행한 아우디의 ‘Edge Cloud 4 Production’ 도입 사례를 강조했습니다. 이를 통해 가상화된 소프트웨어 정의 자동화 및 AI 기반 공정 제어 기술이 유럽 자동차 제조 업계에 도입되었습니다. 이러한 사례들은 유럽의 엣지 AI 소프트웨어 시장이 산업 현대화, 데이터 관리, 그리고 주권적 인프라 구축이라는 우선순위와 밀접하게 연결되어 있는 이유를 보여줍니다. 남미, 중동 및 아프리카 및 튀르키예는 현재 규모는 작지만, 농업, 금융 포용, 스마트 시티, 물류, 에너지 관리 분야에 대한 투자가 해당 지역 내 AI 도입에 대한 선택적 수요를 창출하고 있기 때문에 여전히 중요한 시장입니다. 이러한 지역에서는 도입이 광범위한 기업 표준화라기보다는 모바일 우선의 연결성이나 국가 차원의 디지털 인프라 프로그램에 의해 형성되는 경우가 많습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the edge AI software market size is projected to be USD 1.82 billion in 2025, USD 2.25 billion in 2026, and reach USD 6.82 billion by 2031, growing at a CAGR of 24.83% from 2026 to 2031.

This report is Segmented by Offering (Solutions, and Services), Data Modality (Visual Data, Auditory Data, Text and Language Data, Environmental and Location Data, and Multimodal Data), Deployment Mode (Cloud, On-Premise, and More), End-User Industry (Manufacturing, Healthcare, Retail and Consumer Goods, Energy and Utilities, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Edge AI Software Market Trends and Insights

Proliferation Of Internet Of Things Endpoint Data

The edge AI software market is gaining momentum because the amount of machine-generated data at industrial and enterprise endpoints has become too large for cloud-relay architectures to handle efficiently. Research on the ELARA framework, published in Discover Computing in May 2026, showed end-to-end latency of 39-52 milliseconds, bandwidth savings of up to 48%, and task completion rates of 93-98% across large-scale IoT networks, which directly supports local processing for time-sensitive workloads. That result matters because industrial systems can emit sensor streams at 1 Hz or higher across thousands of nodes, and the cost of transmitting raw telemetry into centralized infrastructure rises quickly as deployments scale. Cisco's State of Wireless Report 2026 also found that IoT growth ranked as the top driver of enterprise wireless investment, ahead of user mobility and high-bandwidth application adoption, which shows that network spending is now being shaped by endpoint intelligence rather than simple connectivity expansion. In this setting, the edge AI software market benefits because enterprises need software that can filter, contextualize, and act on data locally before deciding what should move upstream, and raw network capacity alone does not solve that requirement.

Demand For Low-Latency Decisioning At The Edge

The edge AI software market is also being pushed forward by use cases that require decisions in real time across manufacturing, autonomous systems, utilities, and public safety environments. Once latency budgets fall below 50 milliseconds, or site telemetry rises to 1 terabyte per day, local inference becomes a practical requirement rather than a design preference. NVIDIA and T-Mobile announced in March 2026 that they were integrating physical AI applications over distributed 5G edge networks with the NVIDIA Metropolis platform, including smart city operations, automated utility inspection, and industrial safety workloads where response speed is operationally critical. Hewlett Packard Enterprise also launched HPE AI Grid in March 2026 to deliver predictable low-latency performance across distributed inference sites, and Comcast began field trials for real-time edge inferencing on its network using small language models. The edge AI software market is therefore shifting toward platforms that can hold inference performance steady under constrained compute conditions, because average throughput on benchmark hardware matters less than deterministic behavior at the point of use.

Heterogeneous Edge Environment Integration Complexity

The edge AI software market still faces a major operational barrier because most enterprise deployments span different processor types, operating systems, and connectivity conditions. Research published in Sensors in 2026 on the MIGS architecture found that heterogeneous device integration requires protocol-agnostic middleware that can work across Modbus, OPC UA, and MQTT at the same time, which shows how difficult interoperability remains in real industrial settings. ZEDEDA's 2026 survey results also pointed to the same problem, with 41% of enterprises identifying distributed workload management as a primary challenge and 47% reporting the use of hybrid cloud-edge architectures that demand consistent governance across different hardware environments. This creates a split in the edge AI software market because large enterprises with standardized fleets can scale faster, while buyers with legacy operational technology face longer deployment cycles and higher integration costs. Until the sector develops a more universal hardware abstraction layer, interoperability will remain a structural drag on rollout speed and software standardization.

Other drivers and restraints analyzed in the detailed report include:

- Need For Privacy-Preserving On-Device Inference

- 5G-Enabled Distributed Application Architectures

- Model Optimization Limits On Constrained Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions held 62.72% of the edge AI software market share in 2025, which kept them in the leading position as enterprises favored integrated platforms over modular contracting models. That pattern reflects a practical buying preference because manufacturers, telecom operators, and other large users want validated packages that combine inference runtimes, compression tools, and deployment orchestration in one product. Buyers have generally preferred this route because it reduces interoperability uncertainty at the edge and lowers the burden of stitching together tools from different vendors. In the edge AI software market, that preference has given platform providers an early revenue advantage because they can sell a complete operating layer rather than only a narrow point capability. The same trend also shows that the edge AI software market has moved beyond trial deployments, since procurement teams usually standardize on bundled solutions only after internal teams see a clear path toward long-term operations.

Services are projected to expand at a 25.64% CAGR through 2031, and that pace is faster than the overall edge AI software market. That spread signals a change in how deployments are being managed after the initial software stack is installed. Enterprises are increasingly outsourcing edge MLOps, model optimization, lifecycle management, and fleet-wide observability because many do not have the internal engineering teams needed to manage model drift across distributed assets. Siemens made that transition more concrete in April 2026 when it announced broader availability for its Industrial AI Suite on Siemens Industrial Edge, covering model training, deployment, retraining, and AI model management across multiple factory sites. Google's expansion of LiteRT-LM support across iOS Swift, JavaScript, and Android APIs in 2026 showed a similar direction in mobile environments, where the runtime increasingly behaves like an embedded managed layer rather than a stand-alone software purchase.

The edge AI software market is therefore seeing a gradual blending of product and service economics, even if the two categories are still reported separately. Integrated solutions remain the first purchase for many enterprises, but service layers become more important once deployments move from pilots into full operations. That is especially visible among mid-market industrial users that installed edge hardware in 2023 and 2024 but still lack internal AI staffing depth. As a result, the edge AI software industry is developing toward lifecycle platforms that combine packaged software with ongoing operational support, rather than simple license-based software delivery.

Visual data accounted for 29.98% of revenue in 2025, making it the largest modality in the edge AI software market. That lead was built on years of computer vision deployment across factory inspection, security surveillance, and automotive perception systems. The installed global camera base continues to create a large demand reservoir because many endpoints still collect video that is not analyzed in real time. NVIDIA noted in 2026 that more than 1.5 billion cameras were installed globally and that less than 1% was being meaningfully analyzed in real time, which points to a large remaining opportunity for local visual inference frameworks. For the edge AI software market, this means visual workloads still anchor current revenue because they connect directly to established enterprise spending categories such as quality control, safety monitoring, and automated inspection.

Other data modalities are also expanding because end users are broadening the kinds of information they want to process locally. Text and language data support human-machine interfaces and local conversational functions, while environmental and location data are tied to monitoring, routing, and infrastructure use cases. Multimodal AI has become strategically important because enterprises increasingly want a single stack that can interpret several inputs at once without relying on separate models for each data stream. NVIDIA's Nemotron 3 Nano Omni model, released in May 2026, combined vision, language, and audio perception in one compact model designed for agentic edge workloads, which reflected this shift toward more unified inference architectures. The edge AI software market is gaining from this because multimodal models can simplify operational complexity when customers need richer local context but cannot support multiple full software stacks on constrained devices.

Auditory data is projected to grow at a 26.88% CAGR through 2031, which makes it the fastest-growing modality in the edge AI software market. The strongest demand is coming from audio anomaly detection in rotating machinery, voice-command interfaces in warehouse robotics, and conversational systems that need local responsiveness in healthcare and banking settings. Audio workloads also carry a cost advantage because the models are often smaller than comparable visual systems and can therefore run on more modest hardware footprints. That lowers deployment barriers for industrial original equipment manufacturers that already have installed MCU-class devices across large endpoint fleets. Over time, the edge AI software industry is likely to see auditory and multimodal use cases become more important because they offer practical performance gains without requiring the larger compute budgets that visual inference often demands.

Geography Analysis

North America held 34.78% of the edge AI software market share in 2025, which kept it as the largest regional contributor. The region benefits from a dense concentration of hyperscaler platforms and industrial technology vendors, and that gives enterprise buyers earlier access to full-stack deployment options than most other regions. The edge AI software market also gains in North America from mature enterprise software procurement cycles, where large organizations are more willing to fund multi-site deployments after pilot validation. HPE's AI Grid launch in March 2026 and Comcast's field trials for distributed edge inferencing show that deployment activity is spreading beyond factories and into communications infrastructure and consumer service delivery networks. IBM's May 2026 launch of Sovereign Core also reflects a procurement environment where digital sovereignty and operational control are influencing both government and regulated enterprise demand.

Asia-Pacific is projected to expand at a 26.71% CAGR through 2031, which makes it the fastest-growing regional segment in the edge AI software market. That momentum is being supported by China's manufacturing scale, Japan's robotics and automotive programs, India's engineering base, and South Korea's semiconductor ecosystem. Nikkei reported in March 2026, citing Fuji Chimera Sogo Kenkyusho research, that AI agents and edge-based physical AI inference were expected to push market expansion in Japan from 2026 onward, with the edge environment gaining importance for both privacy protection and AI agent commercialization. This growth profile matters because the edge AI software market in Asia-Pacific is tied both to large industrial deployment volumes and to local design ecosystems that can embed AI functions closer to the device layer. It also means regional vendors and global suppliers are competing in a setting where cost efficiency, localization, and hardware alignment matter as much as software features.

Europe continues to hold a meaningful share of the edge AI software market because the region combines a strong industrial base with a regulatory environment that pushes buyers toward more controlled AI deployment models. Deutsche Telekom's European Edge Continuum moved into live lab and pre-production status in 2025 and continued toward commercial rollout in 2026, which supports Europe's digital sovereignty agenda through a federated and interoperable edge infrastructure layer. Cisco also highlighted Audi's Edge Cloud 4 Production deployment with Siemens at the Bollinger Hofe factory in March 2025, bringing virtualized software-defined automation and AI-driven process control into European automotive manufacturing. These examples show why the edge AI software market in Europe remains tied to industrial modernization, data control, and sovereign infrastructure priorities. South America, the Middle East and Africa, and Turkey are smaller in current scale, but they still matter because investment in agriculture, financial inclusion, smart cities, logistics, and energy control is creating selective demand for local AI execution. In those regions, adoption is often shaped by mobile-first connectivity and national digital infrastructure programs rather than by broad enterprise standardization.

- Amazon Web Services, Inc.

- Google LLC

- Microsoft Corporation

- International Business Machines Corporation

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Technologies, Inc.

- Nutanix, Inc.

- Siemens AG

- Synaptics Incorporated

- Hewlett Packard Enterprise Company

- Oracle Corporation

- Edge Impulse, Inc.

- ClearBlade, Inc.

- ZEDEDA, Inc.

- Viso AI AG

- Latent AI, Inc.

- Gorilla Technology Group Inc.

- PTC Inc.

- Renesas Electronics Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Internet of Things Endpoint Data

- 4.2.2 Demand for Low-Latency Decisioning at the Edge

- 4.2.3 Need for Privacy-Preserving On-Device Inference

- 4.2.4 5G-Enabled Distributed Application Architectures

- 4.2.5 Fleet-Scale Edge Model Operations and Orchestration

- 4.2.6 Certification-Ready Stacks for Safety-Critical Deployments

- 4.3 Market Restraints

- 4.3.1 Heterogeneous Edge Environment Integration Complexity

- 4.3.2 Model Optimization Limits on Constrained Devices

- 4.3.3 Certification Gaps for Regulated Deployments

- 4.3.4 Immature Benchmarking for Heterogeneous Software Stacks

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Data Modality

- 5.2.1 Visual Data

- 5.2.2 Auditory Data

- 5.2.3 Text and Language Data

- 5.2.4 Environmental and Location Data

- 5.2.5 Multimodal Data

- 5.3 By Deployment Mode

- 5.3.1 Cloud

- 5.3.2 On-premises

- 5.3.3 Hybrid

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Information Technology and Telecommunications

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Automotive and Transportation

- 5.4.5 Retail and Consumer Goods

- 5.4.6 Energy and Utilities

- 5.4.7 Smart Cities and Public Infrastructure

- 5.4.8 Banking, Financial Services, and Insurance

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 South Africa

- 5.5.5.5 Egypt

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amazon Web Services, Inc.

- 6.4.2 Google LLC

- 6.4.3 Microsoft Corporation

- 6.4.4 International Business Machines Corporation

- 6.4.5 NVIDIA Corporation

- 6.4.6 Intel Corporation

- 6.4.7 Qualcomm Technologies, Inc.

- 6.4.8 Nutanix, Inc.

- 6.4.9 Siemens AG

- 6.4.10 Synaptics Incorporated

- 6.4.11 Hewlett Packard Enterprise Company

- 6.4.12 Oracle Corporation

- 6.4.13 Edge Impulse, Inc.

- 6.4.14 ClearBlade, Inc.

- 6.4.15 ZEDEDA, Inc.

- 6.4.16 Viso AI AG

- 6.4.17 Latent AI, Inc.

- 6.4.18 Gorilla Technology Group Inc.

- 6.4.19 PTC Inc.

- 6.4.20 Renesas Electronics Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment