|

시장보고서

상품코드

2061963

벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agentic AI Applications In Vector Database - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

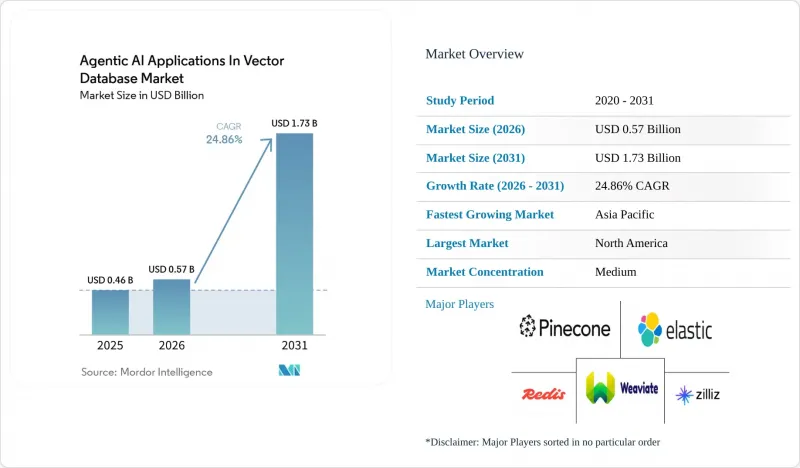

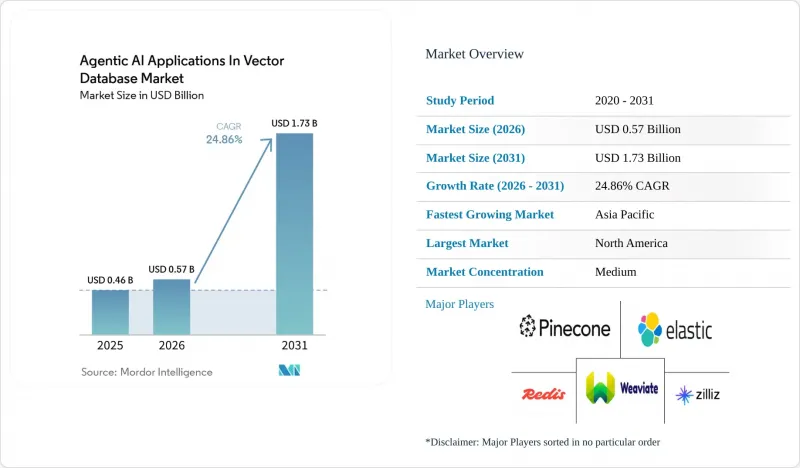

Mordor Intelligence에 의하면, 벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장 규모는 2025년 4억 6,000만 달러로 평가되었습니다. 2026년에는 5억 7,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 24.86%로 성장을 지속하여, 2031년까지 17억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 배포 모드(클라우드 관리형 등), 벡터 DB의 유형(전용 벡터 데이터베이스 등), 용도(대화형 AI 및 검색 확장 생성 등), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 소매 및 전자상거래 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장 동향 및 인사이트

대규모 언어 모델의 보급이 고차원 검색을 주도하고 있습니다.

벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장은 대규모 언어 모델(LLM)이 실험 단계에서 실제 운영 인프라로 전환되고 있는 데 따른 혜택을 누리고 있습니다. LLM의 추론과 내부 실시간 데이터를 결합하는 각 기업의 파이프라인에는 저지연이며 안정적인 검색 성능으로 대량의 임베딩 데이터를 처리할 수 있는 벡터 인덱스가 필요합니다. 많은 조직이 단일 모델로 표준화하는 것을 중단하고, 대신 서로 다른 임베딩 공간에서 작동하는 여러 모델을 지원하게 되면서 이러한 압박은 더욱 커지고 있습니다. 이로 인해 여러 인덱스를 유지할 수밖에 없게 되었으며, 동일한 환경 내에서의 스토리지, 오케스트레이션 및 컴퓨팅 수요가 증가하고 있습니다. MongoDB는 2026년 1월, 동영상 기능을 갖춘 멀티모달 옵션을 포함한 5가지 Voyage 4 임베디드 모델을 출시하고, 외부 임베디드 호출에 대한 의존도를 줄이기 위해 이를 Atlas Vector Search에 통합했습니다. 이러한 통합은 벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장이 단일 검색 패턴에 의존하지 않고, 모델의 다양화와 함께 확대되고 있음을 보여줍니다.

에이전트형 AI 아키텍처의 부상으로 인해 지속적 메모리 저장소의 필요성이 커지고 있습니다.

벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장은 여러 세션에 걸쳐 계획, 검색, 추론, 행동을 수행하는 에이전트형 시스템에 의해서도 주도되고 있습니다. 이러한 워크로드는 하나의 작업에 대해 수천 번의 벡터 검색을 수행할 수 있을 뿐만 아니라, 작업이 활성화된 동안 새로운 메모리를 시스템에 다시 기록할 수도 있기 때문에 정적 RAG와는 다릅니다. Qdrant는 2026년 4월, 프로덕션 환경의 에이전트 루프에서는 워크플로우당 수천 건의 쿼리가 생성되는 반면, 기존의 RAG 워크로드는 여전히 훨씬 더 가볍다고 밝혔습니다. 또한 기업들은 완벽한 가시성, 감사 추적 기능 및 접근 제어를 요구하고 있습니다. 왜냐하면 에이전트의 모든 행동은 사내 거버넌스 팀에 대해 설명 가능해야 하기 때문입니다. Amazon Bedrock AgentCore는 2025년 10월 일반 제공을 시작했으며, 영구 메모리, 시맨틱 검색, 네이티브 OpenTelemetry를 통한 가시성을 도입함으로써 엔터프라이즈 도입의 기준을 한 단계 높였습니다. 그 결과, 벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장에서는 단순한 검색 속도뿐만 아니라 성능과 거버넌스를 모두 갖춘 제공업체가 선호되는 추세입니다.

수십억 규모의 인덱스에서 발생하는 높은 연산 및 스토리지 비용

벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장은 도입 규모가 수백만 벡터에서 수십억 벡터로 확대됨에 따라 현실적인 비용 한계에 직면하고 있습니다. HNSW 인덱스는 여전히 메모리를 대량으로 소비하며, 1,536차원의 10억 개 벡터로 구성된 데이터 세트의 경우, 양자화를 적용하기 전부터도 막대한 양의 RAM이 필요합니다. 이로 인해 매니지드 클라우드 비용이 증가하게 되어, 중견 기업이나 여러 에이전트 워크플로를 동시에 테스트하고 있는 기업의 경우, 사업 타당성이 떨어질 가능성이 있습니다. Qdrant는 리콜률 95% 이상을 유지하면서 메모리 사용량을 32분의 1로 줄이는 바이너리 양자화를 강조하고 있지만, 그 상충 관계는 여전히 워크로드 설계나 검색 결과의 오차에 대한 허용 범위에 따라 달라집니다. 에이전트형 메모리 시스템에 가해지는 압박은 더욱 심각합니다. 정적 검색 시스템과 비교했을 때, 빈번한 쓰기 작업으로 인해 재구축 빈도와 인프라 부하가 증가하기 때문입니다. Tencent Cloud에 따르면, 이 회사의 엔터프라이즈 벡터 데이터베이스는 2025년, Tencent의 전체 사내 사업에서 하루 평균 8,500억 건 이상의 검색 요청을 처리했다고 합니다. 이는 규모의 경제 효과가 여전히 최대 사업자들을 중심으로 집중되어 있음을 보여줍니다.

부문별 분석

벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장에서 2025년에는 클라우드 관리형 배포가 62.31%의 점유율을 차지했습니다. 이는 구매자가 유연성, 통제된 가용성, 그리고 낮은 인프라 오버헤드를 중시했기 때문입니다. 클라우드 관리형 서비스는 플랫폼 내에서 인덱싱, 확장, 장애 조치 및 정기 유지보수를 처리함으로써 AI 팀의 도입 기간을 단축합니다. 또한, 벡터 검색이 별도의 시스템으로 구매되는 것이 아니라 보다 광범위한 AI 구독 서비스에 포함되는 경향이 강해지고 있기 때문에 이 모델은 기업의 구매 행태와도 부합합니다. Amazon Bedrock AgentCore는 관리형 서비스 스택 내에서 영구 메모리와 시맨틱 검색을 통합함으로써 2025년에 이러한 추세를 더욱 공고히 했습니다.

벡터 데이터베이스 기반 에이전트형 AI 애플리케이션 시장에서 자체 호스팅 방식의 배포는 데이터의 저장 위치와 관리가 여전히 중요하게 여겨지는 의료, 정부 및 규제가 엄격한 기업 환경에서 여전히 중요한 위치를 차지하고 있습니다. 조직이 실행 환경에 대한 관리 권한을 잃지 않으면서도 클라우드와 같은 운영을 추구하는 가운데, 하이브리드형 배포는 2031년까지 연평균 성장률(CAGR) 24.81%로 확대될 것으로 예측됩니다. Zilliz는 BYOC-I 및 BYOC Azure 옵션을 통해 이러한 수요에 직접 대응했습니다. 이러한 옵션을 통해 고객은 엔진을 자사의 테넌트 내에 유지하면서, 공급업체의 지원과 관리형 업데이트를 계속 이용할 수 있습니다. 이에 따라, 다지역 기업을 대상으로 하는 벡터 데이터베이스 시장의 대리형 AI 애플리케이션 분야에서 하이브리드 아키텍처는 타협안이라기보다는 기본 아키텍처로서의 입지가 더욱 공고해지고 있습니다.

벡터 데이터베이스 시장에서 전용으로 설계된 벡터 데이터베이스는 고차원 유사성 검색을 위해 처음부터 설계되었기 때문에 2025년에는 에이전트형 AI 애플리케이션 시장의 55.73%를 차지했습니다. 그 가치는 지연 시간 요구 사항이 까다롭고, 인덱스 크기가 크며, 실제 운영 환경의 부하 하에서도 검색 품질을 안정적으로 유지해야 하는 상황에서 가장 잘 드러납니다. Qdrant는 768차원에서 100만 개의 벡터에 대한 p50 쿼리 지연 시간이 3밀리초, p99 지연 시간이 14밀리초라고 보고하고 있으며, 이는 핵심 워크로드에서 전용 엔진이 여전히 매력적인 이유를 보여줍니다. 벡터 지원 관계형 및 문서 저장소 역시 여전히 중요한데, 이는 기업이 새로운 인프라 계층을 도입하지 않고도 기존 용도 데이터베이스에 시맨틱 검색 기능을 추가할 수 있게 해주기 때문입니다.

벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장에서 AI 추론이 액션이 발생하는 지점에 가까워짐에 따라 임베디드형 및 엣지형 벡터 스토어는 2031년까지 연평균 성장률(CAGR) 28.33%로 성장할 것으로 전망됩니다. Qdrant는 2025년 7월, 모바일 기기, 로봇, 리소스가 제한된 하드웨어를 위한 인프로세스 벡터 라이브러리인 ‘Qdrant Edge’를 출시했습니다. 이에 이어 Actian은 2026년 4월, Raspberry Pi 시스템부터 엔터프라이즈 엣지 서버에 이르는 환경을 대상으로 한 ‘VectorAI DB’를 발표했습니다. 로컬 검색을 통해 지연 시간이 단축되고, 오프라인 실행이 가능해지며, 데이터 최소화 요건도 충족되기 때문에 이 부문은 벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장에서 성장세를 보이고 있습니다.

지역별 분석

벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장에서 북미는 2025년에 41.11%의 점유율을 차지하며, 계속해서 지역별 매출 규모에서 가장 큰 비중을 차지했습니다. 이는 기업의 AI 도입이 다른 대부분의 지역보다 빠르게本番 환경에 적용되었기 때문입니다. 미국은 금융 서비스, 의료, 기업 소프트웨어 분야의 대규모 확장을 통해 지역 내 지출을 견인한 반면, 캐나다는 연구 클러스터와 스타트업 생태계를 통해 지원을 강화했습니다. 멕시코 역시 니어쇼어 기술 서비스의 확대와 지역 배송 센터에서의 AI 기반 고객 참여 플랫폼 보급을 통해 기여했습니다. 또한, 해당 지역의 규제 요건도 제품 설계에 영향을 미치고 있으며, 관리형 벤더들은 이미 미국 내 도입을 지원하기 위해 의료 분야에 특화된 규정 준수 기능을 추가하고 있습니다.

벡터 데이터베이스 기반 에이전트형 AI 애플리케이션 시장에서 아시아태평양은 가장 빠르게 성장하고 있는 지역이며, 이 지역 시장 규모는 2031년까지 연평균 성장률(CAGR) 23.97%로 확대될 것으로 전망됩니다. 중국은 주요 수요 거점으로 자리 잡고 있으며, 국내 AI 인프라 투자가 확대되고 있기 때문입니다. Tencent Cloud는 자사의 엔터프라이즈용 벡터 데이터베이스가 2025년, Tencent 내 전체 사업에서 하루 평균 8,500억 건 이상의 검색 요청을 처리했다고 발표했습니다. 일본은 도입 건수는 적지만 계약 규모가 큰 대기업의 지식 관리나 규정 준수 대응을 위한 검색과 같은 이용 사례를 통해 수요를 창출하고 있습니다. 인도는 대규모 개발자 기반과 IT 서비스 부문에 힘입어 성장을 이어가고 있으며, 공공 및 기업의 RAG 프로그램을 위한 벡터 플랫폼 평가가 진행되고 있습니다. 한국에서는 제조업체들이 품질 관리 및 공급망 워크플로우에 에이전트형 AI를 활용하고 있으며, 이러한 시스템이 현지 벡터 스토어에 의존하고 있기 때문에 임베디드형 도입에 있어 해당 지역의 역할이 강화되고 있습니다.

유럽은 벡터 데이터베이스 분야 에이전트형 AI 애플리케이션 시장에서 독자적인 역할을 담당하고 있습니다. 이는 GDPR(EU 개인정보보호규정) 및 EU AI법에 따라 구매자들이 On-Premise형 인프라와 보다 강력한 거버넌스 기능을 중시하게 되었기 때문입니다. Zilliz는 2026년 3월, 고객이 관리하는 암호화 키를 사용하는 BYOC Azure를 정식 출시하여, 고객이 관리하는 환경 내의 주권 요건을 직접 충족시켰습니다. 남미는 여전히 규모가 작은 편이지만, 지역 전체적으로 클라우드 투자가 확대되는 가운데 브라질이 주요 거점으로 부상하고 있습니다. 중동 및 아프리카에서는 주권 AI 프로그램을 통해 탄력을 받고 있으며, 아부다비의 ‘Stargate UAE’ 프로젝트에서는 1기가와트 규모의 컴퓨팅 인프라를 구축 중이며, 초기 단계인 200MW 규모는 2026년 2분기에 가동을 시작했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the agentic AI applications market size in the vector database market is expected to grow from USD 0.46 billion in 2025 to USD 0.57 billion in 2026, and is forecast to reach USD 1.73 billion by 2031 at a 24.86% CAGR over 2026-2031.

This report is Segmented by Deployment Mode (Cloud-Managed, and More), Vector DB Type (Purpose-Built Vector Databases, and More), Application (Conversational AI and Retrieval-Augmented Generation, and More), End-User Industry (IT and Telecom, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI Applications In Vector Database Market Trends and Insights

Proliferation Of Large Language Models Driving High-Dimensional Retrieval

Agentic AI applications in the vector database market are benefiting from the shift of large language models from experimentation to production infrastructure. Each enterprise pipeline that combines LLM inference with live internal data requires a vector index that can handle large embedding volumes with low, stable retrieval latency. The pressure is increasing because many organizations are no longer standardizing on a single model and are instead supporting several models that operate in different embedding spaces. That forces them to maintain multiple indexes and raises storage, orchestration, and compute demand inside the same environment. MongoDB introduced 5 Voyage 4 embedding models in January 2026, including a multimodal option with video capability, and integrated them into Atlas Vector Search to reduce dependence on external embedding calls. That kind of integration shows how the agentic AI applications in the vector database market are expanding alongside model diversity rather than around a single retrieval pattern.

Rise of Agentic AI Architectures Necessitating Persistent Memory Stores

The agentic AI applications in the vector database market are also being pushed forward by agentic systems that plan, retrieve, reason, and act across multiple sessions. These workloads differ from static RAG because they can execute thousands of vector lookups for one task and also write new memory back into the system while the task is still active. Qdrant stated in April 2026 that production agent loops generate multi-thousand queries per workflow, while traditional RAG workloads remain much lighter. Enterprises also expect full observability, audit trails, and access controls because every agent action must be explainable to internal governance teams. Amazon Bedrock AgentCore reached general availability in October 2025, introducing persistent memory, semantic retrieval, and native OpenTelemetry observability, raising the baseline for enterprise deployments. As a result, the agentic AI applications in the vector database market are favoring providers that combine performance with governance rather than solely on retrieval speed.

High Compute And Storage Costs For Billion-Scale Indexes

Agentic AI applications in the vector database market face a real cost ceiling as deployments move from millions of vectors to billions. HNSW indexes remain memory-intensive, and a 1-billion-vector dataset with 1,536 dimensions requires substantial RAM before quantization is even applied. That pushes managed cloud spending to levels that can weaken the business case for mid-market users and for enterprises testing multiple agent workflows simultaneously. Qdrant highlights binary quantization that cuts memory use by 32x while preserving more than 95% recall, but the tradeoff still depends on workload design and tolerance for retrieval drift. The pressure is sharper for agent memory systems because frequent writes increase rebuild frequency and infrastructure load compared with static retrieval systems. Tencent Cloud said its enterprise vector database handled more than 850 billion daily retrieval requests across internal Tencent businesses in 2025, which shows how scale efficiency remains concentrated among the largest operators.

Other drivers and restraints analyzed in the detailed report include:

- Cloud Providers Embedding Native Vector Capabilities Into AI Stacks

- Open-Source Vector Engines Lowering Total Cost of Ownership

- Lack of Standardized Benchmarks And Interoperability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Within the agentic AI applications market for vector databases, cloud-managed deployments held a 62.31% share in 2025, as buyers favored elasticity, managed availability, and low infrastructure overhead. Cloud-managed services shorten deployment time for AI teams by handling indexing, scaling, failover, and routine maintenance within the platform. The model also fits enterprise buying behavior because vector retrieval is increasingly bundled into broader AI subscriptions rather than purchased as a separate system. Amazon Bedrock AgentCore reinforced that pattern in 2025 by combining persistent memory and semantic retrieval inside a managed service stack.

In the agentic AI applications market for vector databases, self-hosted deployments remain relevant in healthcare, government, and heavily regulated enterprise environments where residency and control remain central. Hybrid deployments are projected to expand at a 24.81% CAGR through 2031 as organizations seek cloud-like operations without losing control of the execution environment. Zilliz positioned directly into that demand with BYOC-I and BYOC Azure options that let customers keep the engine inside their own tenant while retaining vendor support and managed updates. That makes hybrid less of a compromise and more of a default architecture for the agentic AI applications in the vector database market across multi-region enterprises.

Within the vector database market, purpose-built vector databases captured 55.73% of the agentic AI applications share in 2025 because they are designed from the ground up for high-dimensional similarity search. Their value is strongest where latency targets are tight, index sizes are large, and retrieval quality must remain stable under production load. Qdrant reported p50 query latency of 3 milliseconds and p99 latency of 14 milliseconds for 1 million vectors at 768 dimensions, which illustrates why purpose-built engines remain attractive for core workloads. Vector-enabled relational and document stores still matter because they let enterprises add semantic retrieval to existing application databases without introducing another infrastructure layer.

In the agentic AI applications market for vector databases, embedded and edge vector stores are forecast to grow at a 28.33% CAGR through 2031 as AI inference moves closer to the point of action. Qdrant launched Qdrant Edge in July 2025 as an in-process vector library for mobile devices, robots, and resource-constrained hardware. Actian followed in April 2026 with VectorAI DB, aimed at environments ranging from Raspberry Pi systems to enterprise edge servers. This segment is gaining ground in the agentic AI applications market for the vector databases because local search reduces latency, supports offline execution, and meets data minimization requirements.

Geography Analysis

Within the agentic AI applications market for vector databases, North America held a 41.11% share in 2025 and remained the leading regional revenue base, as enterprise AI deployments moved into production earlier than in most other regions. The United States led regional spending through large rollouts across financial services, healthcare, and enterprise software, while Canada added support through its research clusters and startup ecosystem. Mexico also contributed through the expansion of nearshore technology services and the wider use of AI-enabled customer engagement platforms in regional delivery centers. The region's regulatory demands are also shaping product design, and managed vendors have already added healthcare-focused compliance features to support U.S. adoption.

Within the agentic AI applications in the vector database market, Asia-Pacific is the fastest-growing region, and the market size in the region is projected to grow at a 23.97% CAGR through 2031. China is a major demand center because domestic AI infrastructure investment is growing, and Tencent Cloud said its enterprise vector database handled more than 850 billion daily retrieval requests across internal Tencent businesses in 2025. Japan is building demand through large-enterprise knowledge management and compliance retrieval use cases that carry high contract value even when deployment counts remain lower. India is supporting growth through its large developer base and IT services sector, which is increasingly evaluating vector platforms for public and enterprise RAG programs. South Korea is strengthening the region's role in embedded deployment because manufacturers are using agentic AI for quality control and supply chain workflows that depend on local vector stores.

Europe has a distinct role in the agentic AI applications market for vector databases because GDPR and the EU AI Act are pushing buyers toward resident infrastructure and stronger governance features. Zilliz made BYOC Azure with customer-managed encryption keys generally available in March 2026, directly addressing those sovereignty requirements within customer-controlled environments. South America remains smaller, with Brazil as the main node, as cloud investment expands across the region. Th Middle East and Africa are gaining momentum through sovereign AI programs, and the Stargate UAE project in Abu Dhabi is building a 1-gigawatt compute base,e with an initial 200 MW phase expected to be operational in Q2 2026.

- Pinecone Systems Inc.

- Zilliz Inc.

- Semi Technologies B.V. (Weaviate)

- Elastic N.V.

- Redis Ltd.

- Chroma Inc.

- Qdrant GmbH

- Oracle Corporation

- MongoDB Inc.

- Neo4j, Inc.

- Microsoft Corporation

- Amazon Web Services, Inc.

- Google LLC

- IBM Corporation

- Databricks Inc.

- Snowflake Inc.

- Couchbase, Inc.

- Alibaba Cloud (Alibaba Group)

- Tencent Cloud

- Vespa.ai

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Large Language Models Driving High-Dimensional Retrieval

- 4.2.2 Rise of Agentic AI Architectures Necessitating Persistent Memory Stores

- 4.2.3 Cloud Providers Embedding Native Vector Capabilities into AI Stacks

- 4.2.4 Open-Source Vector Engines Lowering Total Cost of Ownership

- 4.2.5 Edge AI Adoption Spurring Demand for Embedded Vector Stores

- 4.2.6 Venture Capital Influx Accelerating Product Innovation

- 4.3 Market Restraints

- 4.3.1 Lack of Standardized Benchmarks and Interoperability

- 4.3.2 High Compute and Storage Costs for Billion-Scale Indexes

- 4.3.3 Data-Sovereignty Regulations Restricting Cross-Border Vector Sharing

- 4.3.4 Scarcity of Skilled Vector Similarity Engineers

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intenssity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Managed

- 5.1.2 Self-Hosted

- 5.1.3 Hybrid

- 5.2 By Vector Database Type

- 5.2.1 Purpose-Built Vector Databases

- 5.2.2 Vector-Enabled Relational/Document Stores

- 5.2.3 Embedded/Edge Vector Stores

- 5.3 By Application

- 5.3.1 Conversational AI and Retrieval-Augmented Generation

- 5.3.2 Autonomous Agents and Workflow Orchestration

- 5.3.3 Semantic Search and Recommendation

- 5.3.4 Fraud Detection and Anomaly Analytics

- 5.3.5 Bioinformatics and Scientific Computing

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-Commerce

- 5.4.5 Media and Entertainment

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Pinecone Systems Inc.

- 6.4.2 Zilliz Inc.

- 6.4.3 Semi Technologies B.V. (Weaviate)

- 6.4.4 Elastic N.V.

- 6.4.5 Redis Ltd.

- 6.4.6 Chroma Inc.

- 6.4.7 Qdrant GmbH

- 6.4.8 Oracle Corporation

- 6.4.9 MongoDB Inc.

- 6.4.10 Neo4j, Inc.

- 6.4.11 Microsoft Corporation

- 6.4.12 Amazon Web Services, Inc.

- 6.4.13 Google LLC

- 6.4.14 IBM Corporation

- 6.4.15 Databricks Inc.

- 6.4.16 Snowflake Inc.

- 6.4.17 Couchbase, Inc.

- 6.4.18 Alibaba Cloud (Alibaba Group)

- 6.4.19 Tencent Cloud

- 6.4.20 Vespa.ai

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment