|

시장보고서

상품코드

2061990

항공기 브레이크 시스템 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Aircraft Braking Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

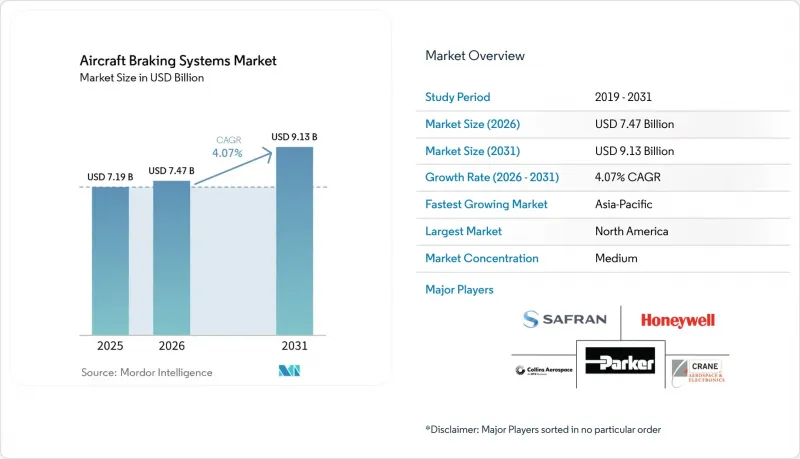

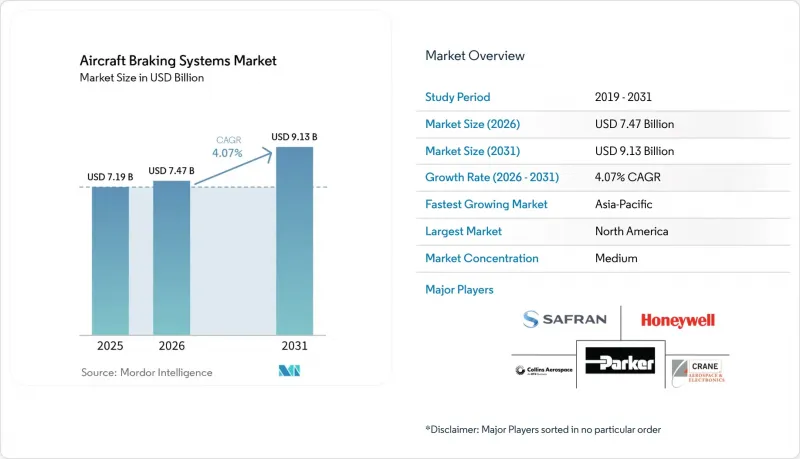

Mordor Intelligence에 의하면, 항공기 브레이크 시스템 시장 규모는 2025년 71억 9,000만 달러에서 2026년에는 74억 7,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 4.07%로 성장을 지속하여, 2031년에는 91억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(카본 브레이크, 스틸 브레이크, 카본 세라믹 브레이크), 작동 방식(유압식, 전기유압식, 전전기식), 최종 사용자(민간 항공, 군용 항공 등), 구성품(휠, 브레이크 디스크, 브레이크 하우징 등), 지역(북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 항공기 브레이크 시스템 시장 동향 및 분석

단통로형 항공기 생산 증가

항공기 브레이크 시스템 시장은 협폭기(narrow-body)의 생산 주기와 직접적으로 연동되어 있습니다. 이는 단일 통로 항공기의 도입이 1대 늘어날 때마다 당장의 브레이크 장치 수요와 향후 정비 대상 항공기 수가 증가하기 때문입니다. 보잉은 2025년에 B737 MAX 447대를 인도할 예정이며, 이는 2024년의 260대보다 증가한 수치입니다. 또한, 4,800대 이상의 미인도 물량을 안고 있는 가운데, 2026년 여름까지월생산량을 47대로, 연말까지 53대로 늘리는 것을 목표로 하고 있습니다. 에어버스는 2025년에 A320 계열 항공기 607대를 인도할 예정이며, 2027년까지월75대 생산을 목표로 하고 있습니다. 카본 브레이크 생산 공장의 가동 개시와 인증에는 수년이 소요되므로, 이러한 일정으로는 연간 브레이크 세트 수요가 신규 인증 소성 및 마감 생산 능력을 증강할 수 있는 속도를 앞지르는 속도로 증가하게 될 것입니다. 따라서 항공기 브레이크 시스템 시장에서는 이미 인증을 받은 생산 거점, OEM 승인, 그리고 확립된 항공사 지원 네트워크를 보유한 기존 기업들이 계속해서 유리한 입지를 점하고 있습니다.

연료 소비 절감 및 중량 감소를 위한 카본 브레이크로의 전환 의무화

항공기 브레이크 시스템 시장은 브레이크 장치의 중량, 정비 주기, 배기가스 목표를 개별 조달 항목이 아닌 상호 연관된 결정 사항으로 다루게 된 항공사의 기체 운영 방침으로부터 지지를 얻고 있습니다. 카본 브레이크는 스틸 제품에 비해 가볍고 수명이 길어, 장기적으로 운영 비용을 절감할 수 있다는 점에서 여전히 매력적입니다. 사프란(Safran)에 따르면, A320neo용 카본 브레이크 ‘SepCarb IV Long Life’는 정비 주기가 2,500회 착륙에 달하며, 단거리 노선을 빈번하게 운항하는 항공사에게 가동 중단 시간과 예비 부품 재고를 줄일 수 있다고 합니다. 이러한 성능은 운항 중인 협폭기 기단의 개조 수요를 뒷받침하며, 신조기 인도에만 의존하지 않는 수요 흐름을 창출하고 있습니다. 따라서 항공기 브레이크 시스템 시장은 공장 출고 시 장착 및 애프터마켓 교체 프로그램 모두에 힘입어 성장하고 있으며, 광범위한 OEM 및 MRO 네트워크를 보유한 공급업체들에게 이익을 가져다주고 있습니다.

탄소 복합재료의 가격 변동

항공기 브레이크 시스템 시장은 카본-카본 브레이크의 생산이 신속한 대체가 어려운 특수 전구체 및 가공 재료에 의존하고 있기 때문에 여전히 원자재 비용 변동의 영향을 받기 쉬운 상황입니다. 공급업체가 가장 큰 압박을 받는 경우는 OEM이나 항공사와 체결한 고정 가격 계약이 원자재 비용과 맞지 않을 때입니다. 또한, 대규모 신규 시설 건설의 경우 투자 승인 전에 수년까지 재료 경제성에 대한 확신이 필요하기 때문에 생산 능력 결정에도 영향을 미칩니다. 사프란사가 리옹 근교에 계획 중인 네 번째 카본 브레이크 공장은 4억 5,000만 유로(5억 2,390만 달러)의 투자액이 소요되며, 이는 해당 분야에서 인증 생산 능력을 확충하는 데 얼마나 막대한 비용이 드는지 여실히 보여주고 있습니다. 따라서 탄소 복합재의 비용 전망이 불투명한 상황이 지속된다면, 항공기 브레이크 시스템 시장에서는 단기적인 이익률 압박과 생산 능력 확대 속도의 둔화가 예상됩니다.

부문별 분석

2025년 기준, 카본 브레이크는 항공기 브레이크 시스템 시장의 52.62%를 차지하며 전체 제품 카테고리에서 1위를 유지했습니다. 사프란은 2025년까지 전 세계 A320 계열 항공기의 70% 이상, 즉 약 5,100대에 자사 제품을 공급할 것이라고 발표했습니다. 한편, 콜린스사는 자사의 DURACARB 기술이 3만 대 이상의 민간 및 군용기에 탑재되어 있다고 밝혔습니다. 이러한 도입 실적을 바탕으로, 대규모 항공사 기단에서 카본 시스템을 중심으로 한 교체, 정비 및 지원 수요가 지속적으로 유지되고 있습니다. 강철 브레이크는 일반 항공기, 지역 터보프롭기, 그리고 초기 도입 비용이 수명 주기 비용보다 중요한 구매 요인이 되는 특정 군용 플랫폼에서 여전히 일정한 역할을 하고 있습니다.

카본 세라믹 브레이크는 항공기 브레이크 시스템 시장에서 가장 빠르게 성장하고 있는 제품 카테고리입니다. 이는 신형 항공기 등급이나 특정 방위용도에서 경량성과 안정적인 마찰 특성이 중요시되기 때문입니다. 임무의 난이도는 매우 다양하지만, 젖은 활주로에서의 성능과 열적 안정성 덕분에 이 소재 세트에 대한 관심은 여전히 지속되고 있습니다. 또한, E-LISA 프로그램에서는 차세대 전동식 랜딩 기어 및 브레이크 시스템을 위한 탄소계 브레이크 소재에 대한 연구도 진행되고 있으며, 이를 통해 개발은 보다 광범위한 전동화 노력과 일관성을 유지하고 있습니다. 따라서 항공기 브레이크 시스템 시장은 현재도 기존의 카본 제품이 주류를 이루고 있지만, 신흥 플랫폼들이 서로 다른 중량, 패키징 및 운용 요건을 요구함에 따라 제품 로드맵은 분명히 확대되고 있습니다.

2025년에는 유압 시스템이 구동 관련 매출의 72.69%를 차지해, 이는 전 세계 항공기 기단의 도입 실적을 반영한 것입니다. 따라서 항공기 브레이크 시스템 시장은 새로운 프로그램의 아키텍처가 다른 방향으로 나아가고 있음에도 불구하고, 현행 기체군에서는 여전히 유압식에 의존하고 있습니다. 완전 전동식 브레이크 시스템은 2026년부터 2031년 사이에 연평균 성장률(CAGR) 8.29%를 나타낼 것으로 예측되며, 이는 항공기 브레이크 시스템 시장의 구동 방식 중 가장 빠른 성장 속도입니다. 파커 에어로스페이스에 따르면, 이 회사의 A220 탑재 Ebrake 시스템은 시속 200마일을 초과하는 속도로 비행하는 60톤 이상의 항공기를 3,280피트 이내에서 감속시킬 수 있으며, 또한 2,000°C에 달하는 고온에도 견딜 수 있습니다.

전기유압 시스템은 그 전환 과정의 중간 단계에 위치하고 있습니다. 이는 OEM이 항공기 시스템을 완전히 재설계할 필요 없이 유압 시스템에 대한 의존도를 낮출 수 있기 때문이며, 전기화의 이점을 어느 정도 누리면서도 여전히 익숙한 백업 로직과 유지보수 방식을 선호하는 프로그램에게 실용적인 선택지가 되고 있기 때문입니다. 클린 스카이 2 ‘모어 일렉트릭 윙(More Electric Wing)’ 프로젝트에서 리프헬 에어로스페이스의 역할은 고출력 모터 컨트롤러와 열 관리 모듈이 여전히 전동식 랜딩 기어 시스템 분야에서 활발히 개발되고 있음을 보여줍니다. 따라서 항공기 브레이크 시스템 시장은 더 광범위한 항공기 등급에서 완전 전기식 구성이 주류가 되기 전에, 다층형 및 하이브리드형 아키텍처를 거쳐갈 가능성이 높다고 볼 수 있습니다.

지역별 분석

2025년, 북미는 항공기 브레이크 시스템 시장 점유율의 36.89%를 차지하며 지역별로는 가장 큰 기여를 한 지역이 되었습니다. 이러한 입지는 주요 OEM 공급 프로그램의 집중, 대규모 방산 조달 기반, 그리고 세계 최대 규모의 민간 항공기 기단을 뒷받침하는 촘촘한 MRO 네트워크에 힘입은 것입니다. 보잉은 2025년에 B737 MAX 447대를 인도하고, 2026년 말까지월53대 생산을 목표로 함으로써, 브레이크 세트에 대한 수요를 지역 공급망에 지속적으로 집중시키고 있습니다. 사프란의 켄튀르키예주 월턴 공장에서는 연간 9,500세트 이상의 휠 브레이크 세트를 생산하고 있으며, 한편 콜린스사는 민간 및 군사 수요를 모두 충족하기 위해 스포캔에서 카본 브레이크 생산 능력을 확대했습니다. 북미 항공기 브레이크 시스템 시장은 Joby와 Archer가 FAA 주도의 승인 절차와 긴밀히 협력하고 있어, 첨단 eVTOL 인증 활동의 수혜를 입고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 5.84%를 기록하며 성장할 것으로 예상되며, 항공기 브레이크 시스템 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 이러한 환경에서 항공기 이용률이 상승하면, 신규 도입분이 추가되기 전부터 브레이크 마모가 가속화되어 정비 수요가 늘어납니다. 중국 역시 C919용 브레이크 디스크의 현지 생산과 AVIC 시안 항공 브레이킹(AVIC Xi'an Aviation Braking)이 보잉, 에어버스, 봄바르디아의 각 플랫폼에서 전개하는 정비 협력을 통해 현지 생산 능력을 확대하고 있으며, 이를 통해 지역 수요에 경쟁력 있는 제조 측면의 강점이 더해지고 있습니다.

유럽은 2025년에 상당한 시장 점유율을 차지하고 있으며, 이는 에어버스의 납품 활동과 항공기 브레이크 시스템 분야의 사프란(Safran)의 프랑스 내 생산 거점에 힘입은 바 큽니다. 브라질에서는 2026년 3월 국내 RPK가 10.8% 증가하여 남미 지역의 협폭기 수요가 점차 확대되고 있음을 시사하고 있지만, 해당 지역은 여전히 수입 브레이크 부품에 대한 의존도가 높은 상황입니다. 아프리카에서는 2026년 3월 RPK가 20.6% 증가했으며, 보유 기체 수는 여전히 적은 편이지만 대륙 내 교통량 증가가 장기적인 MRO 기회를 뒷받침하고 있습니다. 중동에서는 공역 혼란으로 인해 2026년 3월 RPK가 58.6% 감소했습니다. 그러나 사우디아라비아 항공 산업의 성장과 사프란(Safran)사의 전동 카본 브레이크를 장착한 B787-9 기종을 리야드 에어(Riyadh Air)가 도입할 계획에 따라, 중기적인 수요는 유지될 전망입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the aircraft braking systems market size is expected to grow from USD 7.19 billion in 2025 to USD 7.47 billion in 2026 and is forecast to reach USD 9.13 billion by 2031 at 4.07% CAGR over 2026-2031.

This report is Segmented by Product Type (Carbon Brakes, Steel Brakes, and Carbon-Ceramic Brakes), Actuation Method (Hydraulic, Electro-Hydraulic, and Fully-Electric), End User (Commercial Aviation, Military Aviation, and More), Component (Wheels, Brake Discs, Brake Housing, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aircraft Braking Systems Market Trends and Insights

Rising Production of Single-Aisle Aircraft

The aircraft braking systems market is responding directly to the narrowbody production cycle, as each additional single-aisle delivery increases both immediate brake demand and the future overhaul base. Boeing delivered 447 B737 MAX aircraft in 2025, up from 260 in 2024, and it targeted a production rate of 47 aircraft per month by summer 2026 with plans to move toward 53 by year's end against a backlog of more than 4,800 orders. Airbus delivered 607 A320-family aircraft in 2025 and continued to target 75 aircraft per month by 2027. Those schedules lift annual brake-set requirements faster than new qualified furnace and finishing capacity can be added, because carbon-brake production plants take years to commission and certify. The aircraft braking systems market, therefore, continues to favor incumbents that already have qualified production footprints, OEM approvals, and established airline support networks.

Mandatory Shift to Carbon Brakes for Fuel and Weight Savings

The aircraft braking systems market is gaining support from airline fleet policies that now treat brake weight, maintenance intervals, and emissions goals as linked decisions rather than separate procurement items. Carbon brakes remain attractive because they improve operating economics over time through lower weight and longer service life when compared with steel alternatives. Safran states that its SepCarb IV Long Life carbon brake for the A320neo reaches 2,500 landings between overhauls, reducing downtime and spare parts inventory for airlines running dense short-haul schedules. That performance supports retrofit demand on in-service narrowbody fleets and creates a demand stream that does not depend only on new aircraft deliveries. The aircraft braking systems market is therefore being strengthened by both factory-fit positions and aftermarket replacement programs that reward suppliers with broad OEM and MRO reach.

Price Volatility of Carbon-Composite Materials

The aircraft braking systems market remains exposed to raw-material cost swings because carbon-carbon brake production depends on specialized precursor and processing inputs that are difficult to replace quickly. Suppliers face the most pressure when fixed-price agreements with OEMs and airlines do not align with input costs. Capacity decisions are also affected because large new facilities require multi-year confidence in material economics before investment is approved. Safran's planned fourth carbon-brake plant near Lyon carries an investment value of EUR 450 million (USD 523.90 million), underscoring how expensive it is to add qualified output in this segment. The aircraft braking systems market can therefore see short-term margin pressure and slower capacity additions when carbon-composite cost visibility remains weak.

Other drivers and restraints analyzed in the detailed report include:

- Surge in eVTOL/Urban Air Mobility Programs

- Predictive-Maintenance Adoption for Landing Gear

- Lengthy Certification Cycles for New Brake Tech

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Carbon brakes held 52.62% of the aircraft braking systems market in 2025, maintaining their lead across product categories. Safran stated in 2025 that it equips over 70% of the global A320 family fleet, or around 5,100 aircraft, while Collins said its DURACARB technology is installed across more than 30,000 commercial and military aircraft. That installed base keeps replacement, overhaul, and support demand centered on carbon systems across large airline fleets. Steel brakes still retain a role in general aviation, regional turboprops, and selected military platforms where upfront acquisition cost remains a stronger buying factor than lifetime economics.

Carbon-ceramic brakes are the fastest-growing product category in the aircraft braking systems market because newer aircraft classes and selected defense applications value low mass and stable friction behavior. Wet-runway performance and thermal consistency continue to support interest in this material set, despite wide variations in mission intensity. The E-LISA program is also examining carbon-based brake materials for next-generation electrically actuated landing gear and braking systems, thereby keeping development aligned with broader electrification efforts. The aircraft braking systems market, therefore, remains anchored in conventional carbon products today, but the product roadmap is clearly widening as emerging platforms push different weight, packaging, and operating requirements.

Hydraulic systems accounted for 72.69% of actuation revenue in 2025, reflecting the installed-base reality of the global fleet. The aircraft braking systems market, therefore, continues to rely on hydraulic support across current fleets even as new program architecture moves in a different direction. Fully-electric braking systems are projected to grow at an 8.29% CAGR between 2026 and 2031, the fastest pace among actuation methods in the aircraft braking systems market. Parker Aerospace states that its Ebrake system on the A220 can decelerate an aircraft weighing more than 60 tons at speeds above 200 mph within 3,280 feet while handling temperatures up to 2,000°C.

Electro-hydraulic systems sit in the middle of that transition because they allow OEMs to lower hydraulic dependence without requiring a complete redesign of aircraft systems, making them a practical option for programs that want some electrification benefits but still prefer familiar backup logic and maintenance practices. Liebherr Aerospace's role in the Clean Sky 2 More Electric Wing project shows that high-power motor controllers and thermal management modules remain active areas of development for electric landing gear systems. The aircraft braking systems market is therefore likely to move through layered and hybrid architectures before fully-electric layouts become dominant across a wider range of aircraft classes.

Geography Analysis

North America accounted for 36.89% of the aircraft braking systems market share in 2025, making it the leading regional contributor. That position rests on the concentration of major OEM delivery programs, a large defense procurement base, and a dense MRO network serving the world's largest commercial fleet. Boeing delivered 447 B737 MAX aircraft in 2025 and aimed to reach a rate of 53 aircraft per month by the end of 2026, keeping brake-set demand concentrated in the regional supply chain. Safran's Walton, Kentucky, site produces more than 9,500 wheel and brake sets per year, while Collins expanded carbon-brake capacity in Spokane to support both commercial and military demand. The aircraft braking systems market in North America also benefits from advanced eVTOL certification activity, as Joby and Archer remain closely tied to FAA-led approval pathways.

Asia-Pacific is projected to grow at a 5.84% CAGR through 2031, making it the fastest-growing regional segment in the aircraft braking systems market. Higher aircraft utilization in that environment raises brake wear and accelerates overhaul demand even before new deliveries are counted. China is also expanding local capability through C919 brake-disc localization and through AVIC Xi'an Aviation Braking's maintenance cooperation across Boeing, Airbus, and Bombardier platforms, which adds a competitive manufacturing dimension to regional demand.

Europe held a significant share in 2025, supported by Airbus's delivery activity and Safran's French manufacturing base in aircraft braking systems. Brazil recorded 10.8% domestic RPK growth in March 2026, suggesting incremental narrowbody demand in South America, even though the region still relies heavily on imported brake components. Africa posted 20.6% RPK growth in March 2026 and remains small in fleet size, but rising intra-continental traffic still supports a longer-term MRO opportunity. The Middle East saw a 58.6% drop in RPK in March 2026 due to airspace disruptions. Yet, Saudi Arabia's aviation expansion and Riyadh Air's planned B787-9 fleet with Safran electric carbon brakes preserve medium-term demand.

- Safran SA

- Honeywell International Inc.

- Collins Aerospace (RTX Corporation)

- Parker-Hannifin Corporation

- Crane Aerospace & Electronics (Crane Co.)

- BERINGER AERO

- Grove Aircraft Landing Gear Systems Inc.

- Dunlop Aircraft Tyres Limited

- Matco Aircraft Landing Systems

- Aero Brake & Spares, Inc.

- Jay-Em Aerospace, Inc.

- JAMCO Corporation

- Alaska Gear Company

- Tactair

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising production of single-aisle aircraft

- 4.2.2 Mandatory shift to carbon brakes for fuel and weight savings

- 4.2.3 Surge in eVTOL/Urban Air Mobility programs

- 4.2.4 Passenger-traffic growth in emerging economies

- 4.2.5 Defense carrier-aircraft upgrade cycles

- 4.2.6 Predictive-maintenance adoption for landing gear

- 4.3 Market Restraints

- 4.3.1 Price volatility of carbon-composite materials

- 4.3.2 Lengthy certification cycles for new brake tech

- 4.3.3 Supply-chain fragility in niche friction materials

- 4.3.4 Additive-manufactured substitutes eroding aftermarket

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Carbon Brakes

- 5.1.2 Steel Brakes

- 5.1.3 Carbon-Ceramic Brakes

- 5.2 By Actuation Method

- 5.2.1 Hydraulic

- 5.2.2 Electro-Hydraulic

- 5.2.3 Fully-Electric

- 5.3 By End User

- 5.3.1 Commercial Aviation

- 5.3.2 Military Aviation

- 5.3.3 General Aviation

- 5.3.4 Unmanned Aerial Vehicles (UAVs)

- 5.3.5 eVTOL/Urban Air Mobility

- 5.4 By Component

- 5.4.1 Wheels

- 5.4.2 Brake Discs

- 5.4.3 Brake Housing

- 5.4.4 Valves

- 5.4.5 Actuators

- 5.4.6 Accumulators

- 5.4.7 Electronics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Safran SA

- 6.4.2 Honeywell International Inc.

- 6.4.3 Collins Aerospace (RTX Corporation)

- 6.4.4 Parker-Hannifin Corporation

- 6.4.5 Crane Aerospace & Electronics (Crane Co.)

- 6.4.6 BERINGER AERO

- 6.4.7 Grove Aircraft Landing Gear Systems Inc.

- 6.4.8 Dunlop Aircraft Tyres Limited

- 6.4.9 Matco Aircraft Landing Systems

- 6.4.10 Aero Brake & Spares, Inc.

- 6.4.11 Jay-Em Aerospace, Inc.

- 6.4.12 JAMCO Corporation

- 6.4.13 Alaska Gear Company

- 6.4.14 Tactair

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment