|

시장보고서

상품코드

2061994

특권 액세스 관리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Privileged Access Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

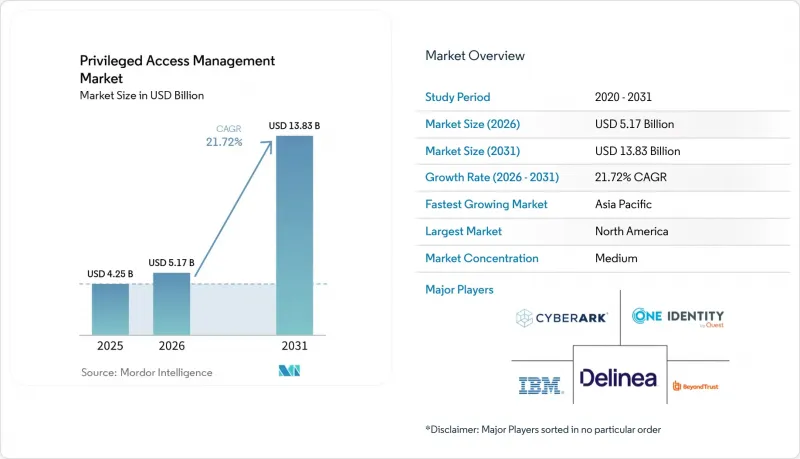

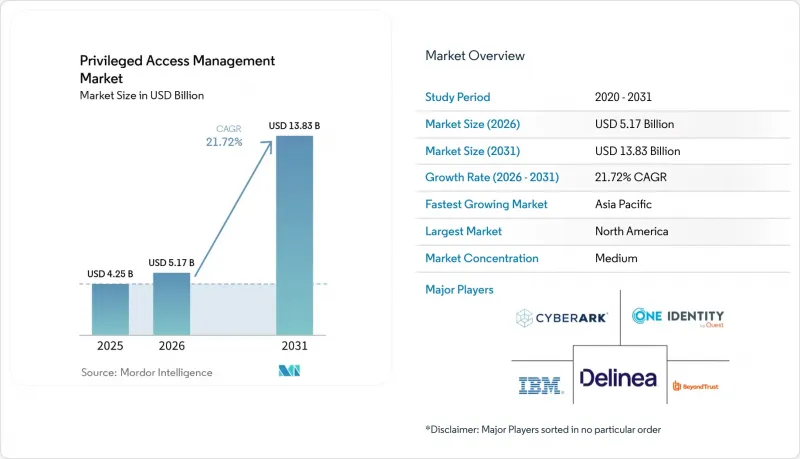

Mordor Intelligence에 의하면, 특권 액세스 관리 시장 규모는 2025년 42억 5,000만 달러에서 2026년에는 51억 7,000만 달러로 확대되어 2031년까지 138억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 21.72%로 성장할 전망입니다.

본 보고서는 구성 요소(솔루션 및 서비스), 도입 형태(On-Premise 등), 조직 규모(대기업 및 중소기업), 최종 사용자 산업(BFSI 등), 액세스 제어 유형(공유/특권 계정 관리, 용도 간 비밀번호 관리 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 특권 액세스 관리 시장 동향 및 인사이트

기기 ID의 급격한 증가와 비밀 정보 관리의 복잡화

마이크로서비스, 컨테이너, 이벤트 주도형 아키텍처를 운영하는 조직에서는 현재 매일 수천 개의 단기 서비스 계정이 생성되고 있어, 기존의 비밀번호 관리 시스템으로는 감당하기 어려운 인증 정보의 확산 문제가 발생하고 있습니다. CyberArk의 조사에 따르면, 사람 1명당 40개의 머신 ID가 존재하는 것으로 나타났으며, 기업의 87%가 관리되지 않는 여러 곳에 비밀 정보를 저장하고 있음을 인정했습니다. 각 벤더사는 비인간 계정에 특화된 자동 감지, 로테이션, 행동 분석 등의 기능을 통해 이에 대응하고 있으며, Saviynt사의 조사에서는 머신 ID 고유의 라이프사이클 정책의 필요성이 강조되고 있습니다.

특권 세션 분리를 가속화하는 제로 트러스트 아키텍처

미국 국방부의 ‘제로 트러스트 실행 로드맵’과 같은 정부 프레임워크에서는 2027년까지 특권 액세스 관리(PAM)를 의무화하고 있으며, 이는 제로 트러스트 청사진에서 적시 프로비저닝과 지속적인 세션 검증이 필수적임을 뒷받침하고 있습니다. 금융 및 의료 분야의 기업들도 이와 유사한 요건을 반영하고 있으며, 그 결과 PAM 벤더들은 컨텍스트상 위험이 높아졌을 때 권한을 취소하는 기능, ID 페더레이션, 마이크로 세분화 게이트웨이, 행동 위험 엔진과의 통합을 추진하고 있습니다.

PAM 도입 및 라이프사이클 거버넌스 분야의 역량 부족

ID 보안 프로그램에는 암호화 기술, 디렉터리 서비스, API 통합에 걸친 전문 지식이 요구되지만, 이러한 기술 인력은 전 세계적으로 만성적인 부족 상태에 있습니다. 기업들은 종종 기존의 아이덴티티 거버넌스에 정통한 직원들조차도, 머신러닝 모델에 의존하는 클라우드 네이티브 분석 모듈의 운영에 어려움을 겪고 있음을 깨닫게 됩니다. 대형 은행이나 의료 네트워크는 장기 관리형 서비스 계약을 통해 이러한 격차를 해소하고 있지만, 많은 중소기업은 외부 컨설턴트를 확보할 때까지 프로젝트를 연기하고 있습니다. 벤더 측의 대응 방안으로는 로우코드 정책 빌더나 설정 시간을 단축해 주는 표준 도입 템플릿 등이 있지만, 이러한 조치만으로는 숙련된 실무자의 필요성을 완전히 없앨 수는 없습니다.

부문별 분석

솔루션 부문은 특권 액세스 관리 시장을 주도하며 2025년에는 매출 점유율의 64.10%를 차지한 반면, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 24.40%로 성장할 것으로 전망됩니다. 기업들이 단일 콘솔 내에서 제공되는 통합 저장소, 세션 분리 및 권한 분석 기능을 선호하기 때문에 플랫폼 통합은 여전히 주요 구매 기준으로 남아 있습니다. 솔루션 분야의 특권 액세스 관리 시장 규모는 2025년에 27억 2,000만 달러에 달하고, 2031년까지 82억 달러를 넘어설 것으로 전망됩니다. 한편, 서비스 분야는 같은 기간 동안 15억 3,000만 달러에서 56억 5,000만 달러로 확대될 전망입니다. CyberArk가 Venafi를 15억 4,000만 달러에 인수한 것은 머신 ID 관리와 인적 권한 워크플로를 통합하려는 해당 벤더의 전략을 보여줍니다. 구매자들은 포인트 제품이 아닌 올인원 플랫폼을 선택할 때, 통합 비용 절감과 감사 대응의 신속화를 결정적인 요인으로 꼽고 있습니다.

서비스의 성장은 세 가지 요인에 의해 주도되고 있습니다. 즉, ID 보안 전문가의 만성적인 부족, 하이브리드 환경의 복잡성 심화, 그리고 도구 라이선싱과 연중무휴 24시간 모니터링을 결합한 성과 기반 관리형 서비스로의 전환입니다. 매니지드 서비스 제공업체는 특히 중소기업을 대상으로, 운영 비용(OpEx)을 중시하는 보안 예산에 부합하는 예측 가능한 구독형 가격을 강조하고 있습니다. 지속적인 자문 서비스 또한 기업이 분기별 규정 준수 갱신이나 새롭게 등장한 포스트 양자암호화 관련 지침에 대응하는 데 도움이 되고 있으며, 이를 통해 서비스 파트너는 향후 10년 동안 두 자릿수 성장을 유지할 수 있을 것으로 전망됩니다.

2025년에는 클라우드 도입이 특권 액세스 관리 시장의 57.05%를 차지했습니다. 이는 구매자들이 On-Premise형 하드웨어 대신 SaaS 방식으로 제공되는 저장소나 정책 엔진을 선호하는 경향을 반영한 것입니다. 클라우드 도입에 따른 특권 액세스 관리 시장 규모는 2025년에 24억 2,000만 달러에 달해, 2031년까지 77억 5,000만 달러에 이를 것으로 전망됩니다. 반면, 하이브리드 도입은 24.10%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 이는 기업이 On-Premise 메인프레임이나 에어갭이 적용된 OT 네트워크를 클라우드의 제어 평면을 통해 연결해 주기 때문입니다. SSH Communications Security의 PrivX는 비밀번호 저장소와 인증서 기반 브로커 기능을 동시에 제공하여, 중단 없는 단계적 전환을 가능하게 합니다.

방위, 유틸리티, 결제 처리 분야의 지속적인 규제 요건으로 인해 On-Premise 구축의 중요성은 여전히 높으며, 특히 데이터 주권 관련 법령에 따라 외부 키 스토어 사용이 금지된 경우 그 중요성이 두드러집니다. 각 벤더사는 프라이빗 클라우드 내에서 가동하면서도 메타데이터를 SaaS 분석 클러스터로 복제하는 컨테이너화된 스토리지 어플라이언스를 통해 마이그레이션 리스크를 완화하고 있으며, 로컬 관리와 클라우드 규모의 인사이트 간의 균형을 실현하고 있습니다. 예측 기간 동안 레거시 시스템이 널리 보급된 업계에서는 하이브리드 도입이 순수 클라우드 도입을 앞지를 것으로 예상되는 반면, 신규 진입한 디지털 네이티브 기업들은 계속해서 완전한 SaaS 형태를 유지할 것으로 보입니다.

지역별 분석

2025년 북미는 특권 액세스 관리 시장에서 38.10%의 점유율을 유지했습니다. 이는 연방 정부의 제로 트러스트 의무화 규제 압력과 정보 유출로 인한 막대한 비용에 대한 인식이 높아지고 있음을 반영합니다. 미국 재무부가 랜섬웨어를 이용한 자금 세탁 단속을 강화함에 따라, 은행과 보험사는 특권 접근을 최우선 통제 수단으로 삼아야 할 압박을 받고 있습니다. 캐나다 역시 PIPEDA 지침 개정을 통해 유사한 추세를 보이고 있는 반면, 멕시코 금융 당국은 국경을 넘는 결제 서비스 제공업체에 대해 데이터 보관(볼팅) 요건을 부과하고 있습니다. 시장의 기존 기업들은 광범위한 파트너 생태계를 유지하고 있으며, 이를 통해 관리형 PAM의 소비 모델이 빠르게 확대되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 23.60%를 기록하며 세계에서 가장 빠른 성장세를 보일 것입니다. 싱가포르 금융청의 지침은 은행 인프라 전반에 걸쳐 특권 액세스 제어를 의무화하고 있으며, 이 기준은 아세안(ASEAN) 회원국 전체로 확산되고 있습니다. 일본의 성숙한 사이버 보안 문화가 플랫폼의 업데이트 주기를 촉진하고 있습니다. Zoho Japan은 자사의 ‘Password Manager Pro’를 통해 2023년 46.2%의 출하 점유율을 확보했으며, 한편 NTT 테크노크로스는 국내 PAM 분야에서의 리더십이 인정받아 업계상을 연속으로 수상했습니다. 중국과 인도의 성장은 스마트 제조 프로그램과, 관리자의 운영에 대해 강력한 감사 추적을 의무화하는 데이터 현지화 법규에 기인합니다.

유럽에서는 불충분한 특권 계정 보호에 대해 제재를 가하는 GDPR(EU 개인정보보호규정) 및 EU 네트워크·정보 보안 지침에 따라, 체계적인 도입이 진행되고 있습니다. 독일과 영국이 이 지역 내 지출을 주도하고 있는데, 이는 자동차, 금융, 통신 사업자들이 국가안보법에 명시된 특권적 접근 권한에 관한 조항에 직면해 있기 때문입니다. 영국의 통신 보안법은 통신 사업자들에게 2024년 네트워크 업그레이드 전에 특권 세션 제어 기능을 도입할 것을 의무화하고 있어, 해당 솔루션에 대한 우선순위가 높아지고 있습니다. 남유럽 및 북유럽 국가들에서는 정부의 디지털 전환(DX) 기금과 의료 시스템의 랜섬웨어 노출 위험 증가를 배경으로 수요가 점차 나타나고 있습니다.

중동 및 아프리카에서는 석유 및 가스 분야의 OT(운영 기술) 현대화, 주권 클라우드 도입, 국가 차원의 사이버 보안 전략을 배경으로 수요가 초기 단계임에도 불구하고 급속히 확대되고 있습니다. 걸프협력회의(GCC) 회원국의 은행 및 유틸리티체들은 입찰 서류에서 PAM(특권 액세스 관리) 인증을 점점 더 요구하고 있으며, 이로 인해 국제적인 공급업체들은 현지 데이터센터 설립 및 아랍어 지원 제공을 강요받고 있습니다. 사하라 이남 아프리카에서는 모바일 머니 생태계의 성장으로 인해 인증 정보 악용 위험이 높아지고 있어, 남아프리카공화국과 케냐가 도입을 주도하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 동향

JHS 26.06.19According to Mordor Intelligence, the privileged access management market size is expected to increase from USD 4.25 billion in 2025 to USD 5.17 billion in 2026 and reach USD 13.83 billion by 2031, growing at a CAGR of 21.72% over 2026-2031.

This report is Segmented by Component (Solutions & Services), Deployment Mode (On-Premises and More), Organization Size (Large Enterprises and Small & Medium Enterprises), End-User Industry (BFSI & More), Type of Access Control (Shared/Privileged Account Management, Application To Application Password Management, & More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Privileged Access Management Market Trends and Insights

Rapid Proliferation of Machine Identities and Secrets Management Complexity

Organisations running microservices, containers, and event-driven architectures now generate thousands of short-lived service accounts every day, creating a credential-sprawl problem that legacy vaults cannot absorb. CyberArk observes ratios of 40 machine identities for every human identity, and 87% of enterprises admit to storing secrets in multiple, unmanaged locations. Vendor roadmaps respond with automated discovery, rotation, and behavioural analytics tuned to non-human accounts, a capability highlighted by Saviynt's research that calls for machine-identity-specific lifecycle policies.

Zero-Trust Architectures Accelerating Privileged Session Isolation

Government frameworks such as the United States Department of Defense Zero Trust Execution Roadmap require privileged access management controls by FY 2027, confirming that just-in-time provisioning and continuous session validation are mandatory inside zero-trust blueprints. Enterprises in finance and healthcare mirror these mandates, causing PAM vendors to integrate with identity federations, micro-segmentation gateways, and behavioural risk engines that revoke privileges when contextual risk rises.

Skills Scarcity for PAM Deployment and Lifecycle Governance

Identity-security programmes demand expertise across cryptography, directory services, and API integration-skills in chronic short supply worldwide. Enterprises often discover that staff versed in traditional identity governance struggle to operate cloud-native analytics modules that rely on machine-learning models. Large banks and healthcare networks offset the gap through long-term managed service contracts, while many SMEs postpone projects until external consultants become available. Vendor response includes low-code policy builders and prescriptive deployment templates that reduce configuration time but cannot fully eliminate the need for skilled practitioners.

Other drivers and restraints analyzed in the detailed report include:

- Cloud-Native PAM Demand from DevSecOps Tool-Chain Integration

- AI-Driven Attack-Surface Discovery Boosting PAM Adoption in OT and IoT

- Brownfield Integration Complexity Across Hybrid Legacy Estates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The solutions category dominated the privileged access management market, accounting for 64.10% revenue share in 2025, while the services category is projected to grow at 24.40% CAGR through 2031. Platform consolidation remains the primary buying criterion as enterprises favour unified vaulting, session isolation, and entitlement analytics delivered within a single console. The privileged access management market size for solutions reached USD 2.72 billion in 2025 and is forecast to exceed USD 8.2 billion by 2031, whereas services will climb from USD 1.53 billion to USD 5.65 billion during the same horizon. CyberArk's USD 1.54 billion acquisition of Venafi illustrates a vendor playbook that merges machine-identity management with human-privilege workflows. Buyers cite lower integration costs and faster audit readiness as decisive factors when selecting all-in-one platforms over point products.

Services growth is propelled by three factors: a chronic shortage of identity-security experts, rising complexity in hybrid estates, and the shift toward outcome-based managed services that bundle tool licensing with 24X7 monitoring. Managed service providers advertise predictable subscription pricing that aligns with OpEx-oriented security budgets, particularly among SMEs. Continuous advisory services also help enterprises keep pace with quarterly compliance updates and emerging post-quantum cryptography guidelines, allowing service partners to maintain double-digit expansion throughout the decade.

Cloud deployments captured 57.05% of privileged access management market share in 2025, reflecting buyer preference for SaaS-delivered vaults and policy engines that avoid on-premises hardware. The privileged access management market size for cloud deployments reached USD 2.42 billion in 2025, with a projected USD 7.75 billion valuation by 2031. Hybrid implementations, however, post the fastest 24.10% CAGR as enterprises bridge on-premises mainframes and air-gapped OT networks with cloud control planes. SSH Communications Security's PrivX offers side-by-side password vaulting and certificate-based brokerage, enabling phased migration without downtime.

Persistent regulatory requirements in defence, utilities, and payment processing keep on-premises deployments relevant, especially where data sovereignty statutes forbid external key stores. Vendors mitigate migration risk through containerised vault appliances that run inside private clouds yet replicate metadata to SaaS analytics clusters, offering a compromise between local control and cloud-scale insights. Over the forecast period, hybrid adoption will outpace pure cloud in verticals with significant legacy footprints, while green-field digital natives will remain fully SaaS.

Geography Analysis

North America retained 38.10% privileged access management market share in 2025, reflecting regulatory impetus from federal zero-trust mandates and high breach-cost awareness. The United States Treasury's crackdown on ransomware-facilitated money laundering compels banks and insurers to treat privileged access as a control of first resort. Canada follows similar patterns through updated PIPEDA guidelines, while Mexico's financial authorities impose vaulting requirements on cross-border payment service providers. Market incumbents maintain extensive partner ecosystems, enabling rapid scaling of managed PAM consumption models.

Asia-Pacific will rise at a 23.60% CAGR through 2031, the fastest worldwide trajectory. Singapore's Monetary Authority guidelines require privileged access controls across banking infrastructures, setting a benchmark that ripples across ASEAN member states. Japan's mature cyber-security culture drives platform refresh cycles; Zoho Japan secured 46.2% shipment share in 2023 via its Password Manager Pro offering, while NTT TechnoCross captured consecutive industry awards for domestic PAM leadership. Growth in China and India stems from smart-manufacturing programmes and data-localisation statutes that require strong audit trails for administrator actions.

Europe notes steady adoption due to GDPR and the EU Network and Information Security Directive that penalise inadequate privileged-account protection. Germany and the United Kingdom head regional spending because automotive, financial, and telecom operators face explicit privileged-access clauses within national security legislation. The UK Telecommunications Security Act obliges carriers to implement privileged session controls before 2024 network upgrades, reinforcing the solution priority. Southern Europe and the Nordics exhibit emerging demand, spurred by government digital-transformation funds and heightened ransomware exposure in healthcare systems.

Middle East and Africa display nascent yet accelerating demand, driven by oil-and-gas OT modernisation, sovereign cloud rollouts, and national-level cyber-security strategies. Gulf Cooperation Council banks and utilities increasingly require PAM certification in tender documents, pushing international vendors to establish local data centres and Arabic language support. South Africa and Kenya lead sub-Saharan adoption because of mobile-money ecosystem growth that raises credential-abuse risks.

- CyberArk Software Ltd.

- BeyondTrust Corporation

- Delinea Inc.

- One Identity LLC

- IBM Corporation

- Broadcom Inc.

- ARCON TechSolutions Pvt. Ltd.

- WALLIX Group SA

- Micro Focus International plc

- ManageEngine - Zoho Corporation Pvt. Ltd.

- Hitachi ID Systems Inc.

- Senhasegura - MT4 Tecnologia Ltda.

- Keeper Security Inc.

- Thales Group (Gemalto NV)

- Fudo Security Sp. z o.o.

- Ekran System Inc.

- Saviynt Inc.

- Ericom Software Ltd.

- Quest Software Inc.

- Bravura Security Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid proliferation of machine identities and secrets management complexity

- 4.2.2 Zero-trust architectures accelerating privileged session isolation

- 4.2.3 Cloud-native PAM demand from DevSecOps tool-chain integration

- 4.2.4 AI-driven attack surface discovery boosting PAM adoption in OT and IoT

- 4.2.5 Stringent cyber-insurance underwriting requirements

- 4.2.6 Post-quantum crypto transition pressure on credential vaulting

- 4.3 Market Restraints

- 4.3.1 Skills scarcity for PAM deployment and lifecycle governance

- 4.3.2 Brownfield integration complexity across hybrid legacy estates

- 4.3.3 Shadow-IT proliferation undermining policy enforcement

- 4.3.4 High TCO for SMEs amid subscription sprawl

- 4.4 Value/Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premises

- 5.2.2 Cloud

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Government and Public Sector

- 5.4.4 Healthcare

- 5.4.5 Retail and E-commerce

- 5.4.6 Manufacturing

- 5.4.7 Energy and Utilities

- 5.4.8 Other End-user Industries

- 5.5 By Type of Access Control

- 5.5.1 Shared/Privileged Account Management

- 5.5.2 Application to Application Password Management (AAPM)

- 5.5.3 Endpoint Privilege Management (EPM)

- 5.5.4 Cloud and SaaS Privilege Management

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Malaysia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CyberArk Software Ltd.

- 6.4.2 BeyondTrust Corporation

- 6.4.3 Delinea Inc.

- 6.4.4 One Identity LLC

- 6.4.5 IBM Corporation

- 6.4.6 Broadcom Inc.

- 6.4.7 ARCON TechSolutions Pvt. Ltd.

- 6.4.8 WALLIX Group SA

- 6.4.9 Micro Focus International plc

- 6.4.10 ManageEngine - Zoho Corporation Pvt. Ltd.

- 6.4.11 Hitachi ID Systems Inc.

- 6.4.12 Senhasegura - MT4 Tecnologia Ltda.

- 6.4.13 Keeper Security Inc.

- 6.4.14 Thales Group (Gemalto NV)

- 6.4.15 Fudo Security Sp. z o.o.

- 6.4.16 Ekran System Inc.

- 6.4.17 Saviynt Inc.

- 6.4.18 Ericom Software Ltd.

- 6.4.19 Quest Software Inc.

- 6.4.20 Bravura Security Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment