|

시장보고서

상품코드

2062008

응집제 및 응고제 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Flocculant And Coagulant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

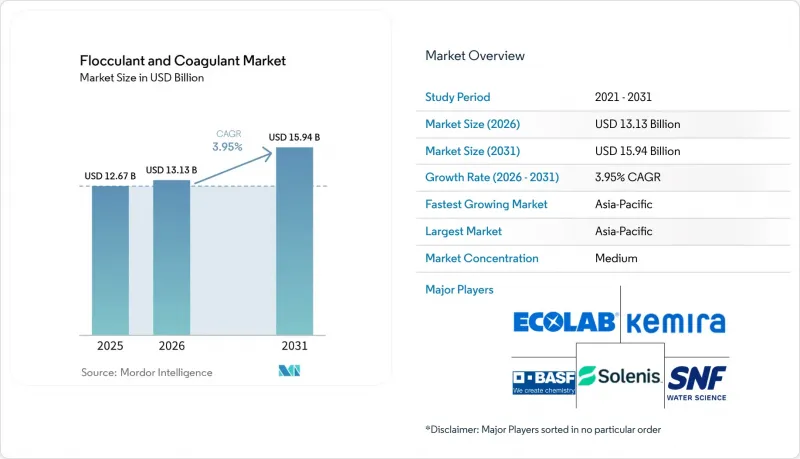

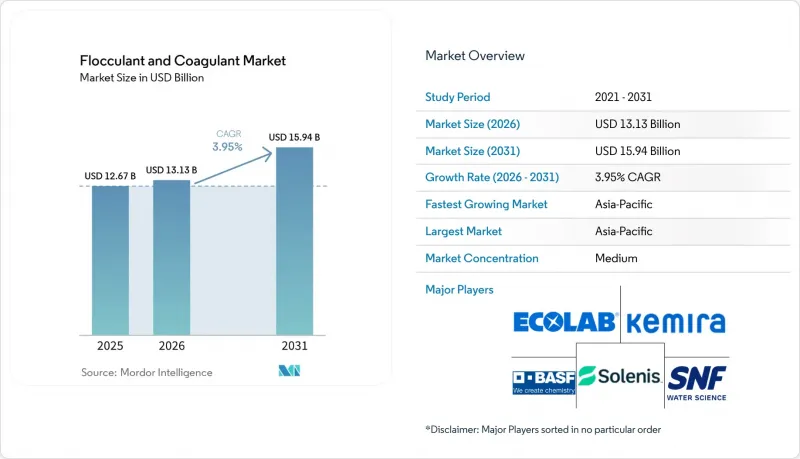

Mordor Intelligence에 의하면, 응집제 및 응고제 시장 규모는 2025년 126억 7,000만 달러로 평가되었습니다. 2026년에는 131억 3,000만 달러로 확대되어 2031년까지 159억 4,000만 달러에 이르고 2026-2031년 CAGR은 3.95%를 나타낼 전망입니다.

본 보고서는 유형(응고제 : 무기, 유기/합성, 천연/바이오 유래; 응집제 : 양이온성, 음이온성, 비이온성), 용도(상수도 처리, 산업 폐수 처리(펄프·제지, 석유 및 가스 등)), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 응집제 및 응고제 시장 동향 및 인사이트

신흥 시장의 산업 클러스터에서 배출 기준 강화

동남아시아 및 남아시아에서는 새로운 규제로 인해 공장들이 화학적 산소 요구량(COD) 및 부유 물질에 관한 더 엄격한 제한을 준수하기 위해 화학약품 처리량을 대폭 늘릴 수밖에 없는 상황입니다. 2025년 1월부터 베트남의 QCVN 40 : 2025 규정에 따라 섬유 및 식품 가공 산업에서 배출되는 폐수에 대한 COD 허용치가 50 mg/L로 하향 조정되었습니다. 한편, 인도네시아의 2024년 가정용 폐수 규정에 따르면 고형물의 80%를 제거해야 할 의무가 부과되어 있으며, 자카르타, 수라바야, 반둥 등의 지자체에서는 설비 업그레이드가 필요하게 되었습니다. 튀르키예, 한국, 인도에서도 규제가 강화되면서 조달 기간이 단축되고, 현지 재고를 보유한 공급업체가 우대받게 됨에 따라, 이들 지역에서 전체 연평균 성장률(CAGR)을 상회하는 수요 급증이 발생하고 있습니다.

제로 리퀴드 디차지(ZLD) 발전소 및 석유화학 플랜트의 급속한 건설 확대

제로 리퀴드 디차지(ZLD) 시스템은 응집, 역삼투, 결정화 기술을 활용하여 거의 완벽한 물 회수를 실현합니다. 막을 보호하기 위해 응고제 사용은 필수적인 전처리 공정으로 포함되어 있습니다. 베올리아는 쉘사의 펄 GTL 공장에 시스템을 도입하여, 하루 1만 2,000m³의 블로우다운수를 99.5%의 회수율로 처리하는 데 성공했습니다. 중국의 산시성과 내몽골 자치구의 석탄 화학 프로젝트, 그리고 2025년 인도의 섬유 산업 클러스터에서는 제로 방류를 목표로 하고 있습니다. 이러한 긴급성으로 인해, 이러한 프로젝트들은 장기 화학약품 서비스 계약으로 이어지고 있으며, 많은 경우 높은 가격에 계약이 체결되고 있습니다.

규제상 독성 : 아크릴아미드 단량체 잔류물에 대한 관심

2024년, 미국 환경보호청(EPA)은 아크릴아마이드를 ‘오염물질 후보 목록’에 추가했습니다. WHO는 음용수 내 아크릴아마이드 잔류량의 상한선을 0.5 mg/kg으로 설정했으며, 일본은 식품 접촉 재료의 기준치를 0.05 mg/kg으로 낮췄습니다. EU는 잔류 모노머 함량이 0.1%를 초과하는 배합물의 사용을 제한할 계획입니다. 제조업체들은 1kg당 0.10-0.30달러의 정제 비용을 부담하고 있습니다. 잔류량이 적은 인증 등급을 제공하는 것은 제조업체가 시장에서 경쟁력을 유지하는 데 도움이 될 수 있습니다.

부문별 분석

2025년, 응고제는 매출의 57.89%를 차지했으며, 이 부문은 2031년까지 연평균 성장률(CAGR) 4.56%를 나타낼 것으로 전망됩니다. 응고제 부문에서는 PAC, 황산알루미늄, 염화제2철 등의 무기계 제품이 생산량 측면에서 주도적인 위치를 차지하고 있습니다. 이러한 우위는 2025년 중국의 PAC 생산량이 231만 2,300톤에 달했고, 국내 평균 가격이 톤당 1,636위안(약 230달러)이었던 사실로도 입증됩니다. 폴리DADMAC이나 EPI-DMDA와 같은 유기 응고제는 15-30%의 가격 프리미엄이 붙어 있습니다. 이러한 유기계 제품은 고알칼리성 수역에서 뛰어난 성능을 발휘하며, 슬러지 발생량을 줄이는 능력 덕분에 높은 비용도 정당화되고 있습니다. 키토산이나 모링가 추출물과 같은 생물 유래 대체 물질은 실험실 시험에서 85-95%의 탁도 제거율을 보였습니다. 그러나 공급망 및 품질 안정성 측면에서 발생하는 문제들로 인해, 그 시장 점유율은 제한적인 수준에 머물고 있습니다.

응집제는 슬러지 탈수 및 광물 처리 과정에서 매우 중요한 역할을 합니다. 양이온성 폴리아크릴아미드는 도시 슬러지나 광산 폐석에서 수분을 배출시키기 위해 고전하 고분자가 필요하기 때문에 응집제 매출의 대부분을 차지하고 있습니다. 음이온성 유형은 펄프·제지 업계에서 유지 보조제로 사용되며, 비이온성 등급은 석탄 세정에 사용됩니다. 음용수 용도에서 잔류 모노머 함량을 0.5 mg/kg 미만으로 제한하기 위한 규제 조치로 인해 생산 비용이 상승하고 있습니다. 그러나 동시에, 이러한 제품들은 프리미엄 가격으로 판매할 수 있는 초저모노머 제품에 대한 기회도 창출하고 있습니다.

지역별 분석

2025년, 아시아태평양은 응집제 및 응고제 시장에서 31.20%의 매출 점유율을 차지했으며, 2031년까지 연평균 성장률(CAGR) 4.98%를 나타낼 것으로 예측됩니다. 주요 시장 참여자인 중국의 PAC(폴리염화알루미늄) 시장은 지역 내 섬유, 제지, 석탄 화학 공장에 제품을 공급하고 있습니다. 한편, 베트남, 인도네시아, 인도에서 배출 기준이 강화됨에 따라 특정 지역 클러스터에서는 화학물질 처리량이 3배로 증가했습니다. 일본과 한국은 최전선에 서서 0.2 mg/L라는 인 규제 기준을 준수하기 위해 AI를 활용한 투여 시스템을 도입하고 있습니다. 아세안(ASEAN) 국가들은 다자간 기구의 지원을 받아 상하수도 시스템을 현대화하고 있지만, 조달 동향은 비용 효율성이 뛰어난 중국 및 인도의 생산 업체들로 쏠리고 있습니다.

북미에서는 처리량 증가세가 완만하지만, 특수 응고제 및 클라우드 기반 제어 플랫폼에 대한 톤당 지출은 증가하고 있습니다. 캘리포니아주의 2025년 직접 음용수 재이용 계획이나 애리조나주의 12억 달러 규모의 물 재이용 프로그램과 같은 주요 사업이 수요를 뒷받침하고 있습니다. 또한, 뉴멕시코주의 2024년 법에 따라 페르미안 분지에서는 생산수를 관개용으로 재활용하고 있습니다. 캐나다에서는 하수 슬러지 매립 처리 비용의 급등에 대응하기 위해 상수도 유틸리티자들이 저용량 PAC 전략을 채택하고 있으며, 처리량은 완만하게 증가하고 있지만 안정적인 수익을 확보하고 있습니다.

유럽 수요는 안정적이며, 특히 독일, 영국, 프랑스, 북유럽 국가들에서 두드러집니다. 에너지 가격 변동으로 인해 저용량 혼합으로의 전환이 진행되고 있습니다. 프랑스에서는 소규모 상수도 유틸리티자를 대상으로 5억 유로(약 5억 8,506만 달러) 규모의 보조금 계획을 통해 이러한 전환을 장려하고 있으며, 특히 ISO 9001 및 NSF 60 인증을 취득한 사업자에게 우대 조치를 제공합니다. 스페인의 새로운 관개용 재이용 규제로 인해 무르시아와 알메리아에서는 응고제 사용이 증가하고 있지만, 러시아에서는 예산 제약으로 인해 성장률이 연간 1-2%에 그치고 있습니다. 남미, 중동 및 아프리카에서는 브라질의 배수 규제 강화, 칠레의 구리 광미 처리, 사우디아라비아의 대규모 해수 담수화 프로젝트를 배경으로, 광업, 해수 담수화 및 지방자치단체의 제로 리퀴드 디차지(ZLD) 프로젝트 분야에서 틈새 기회가 창출되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the flocculant and coagulant market size is expected to increase from USD 12.67 billion in 2025 to USD 13.13 billion in 2026 and reach USD 15.94 billion by 2031, growing at a CAGR of 3.95% over 2026-2031.

This report is Segmented by Type (Coagulants: Inorganic, Organic/Synthetic, Natural/Bio-based; Flocculants: Cationic, Anionic, Non-Ionic), Application (Municipal Water Treatment, Industrial Wastewater Treatment: Pulp and Paper, Oil and Gas, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Flocculant And Coagulant Market Trends and Insights

Stricter Discharge Norms for Emerging-Market Industrial Clusters

In Southeast and South Asia, new regulations compel factories to significantly boost their chemical throughput to comply with stricter limits on Chemical Oxygen Demand (COD) and suspended solids. Starting January 2025, Vietnam's QCVN 40:2025 regulation reduced COD allowances for effluents from textile and food-processing industries to 50 mg/L. Meanwhile, Indonesia's 2024 rule on domestic wastewater mandates an 80% removal of solids, leading to necessary upgrades in municipalities like Jakarta, Surabaya, and Bandung. Turkey, South Korea, and India have also tightened regulations, shortening procurement windows, favoring suppliers with local stock, and creating demand spikes that exceed the headline CAGR in these regions.

Rapid Build-Out of Zero-Liquid-Discharge (ZLD) Power and Petrochem Plants

Zero Liquid Discharge (ZLD) systems utilize coagulation, reverse osmosis, and crystallization techniques to achieve near-total water recovery. Coagulants are embedded as a mandatory pretreatment step to safeguard the membranes. Veolia has implemented a system at Shell's Pearl GTL plant, successfully treating 12,000 m3/day of blowdown with a 99.5% recovery rate. China's coal-chemical initiatives in Shaanxi and Inner Mongolia, along with textile clusters in India in 2025, are aimed at zero discharge. This urgency is steering them towards long-term chemical service contracts, often at a premium price.

Regulatory Toxicity Spotlight on Acrylamide Monomer Residues

In 2024, the U.S. EPA added acrylamide to its Contaminant Candidate List. WHO set a cap of 0.5 mg/kg for residual acrylamide in drinking water and Japan reduced food-contact limits to 0.05 mg/kg. The EU plans to restrict formulations with over 0.1 percent residual monomer. Producers face purification costs of USD 0.10 to 0.30 per kg. Offering certified low-residue grades may assist producers in maintaining a competitive position within the market.

Other drivers and restraints analyzed in the detailed report include:

- Re-Use Mandates in Water-Scarce Regions

- Mature Utility Spending Cycles in North America and Europe

- Growing Preference for Membrane and Electro-Coagulation Hybrids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, coagulants captured a 57.89% share of the revenue pie, and projections indicate this segment will grow at a 4.56% CAGR through 2031. Within the coagulant segment, inorganic variants like PAC, aluminum sulfate, and ferric chloride lead in tonnage. This dominance is supported by China's 2025 output of 2.3123 million tons of PAC, fetching an average domestic price of CNY 1,636/ton (approximately USD 230/ton). Organic coagulants, such as polyDADMAC and EPI-DMDA, have a price premium of 15-30%. These organic variants perform well in high-alkalinity waters, where their ability to reduce sludge volume justifies the elevated costs. Bio-based alternatives like chitosan and Moringa extracts have shown 85-95% turbidity removal in lab tests. However, challenges in the supply chain and consistency have limited their market share.

Flocculants play a critical role in sludge dewatering and mineral processing. Cationic polyacrylamides account for the majority of flocculant revenue, driven by the need for high-charge polymers in municipal sludge and mining tailings to facilitate water release. Anionic variants are used as retention aids in the pulp-and-paper industry, while non-ionic grades are applied in coal washing. Regulatory initiatives aiming to limit residual monomer content to below 0.5 mg/kg in potable applications have increased production costs. However, they also create opportunities for ultra-low-monomer products, which can be marketed at a premium price point.

Geography Analysis

In 2025, Asia-Pacific commands the flocculant and coagulant market with a 31.20% revenue share and is expected to grow at a 4.98% CAGR through 2031. China's PAC base, a dominant player, caters to regional textile, paper, and coal-chemical plants. Meanwhile, tighter discharge norms in Vietnam, Indonesia, and India have led to a threefold increase in chemical throughput in specific clusters. Japan and South Korea are at the forefront, employing AI-driven dosing to adhere to phosphorus caps of 0.2 mg/L. ASEAN nations, with backing from multilaterals, are upgrading municipal systems, yet procurement trends lean towards cost-effective producers from China and India.

North America may be expanding its volume at a slower pace, but it's spending more per ton on specialty coagulants and cloud-connected control platforms. Key initiatives like California's 2025 direct-potable-reuse rollout and Arizona's USD 1.2 billion water-reuse program are bolstering demand. Additionally, under New Mexico's 2024 act, the Permian Basin is reclaiming produced water for irrigation. In Canada, utilities are adopting low-dose PAC strategies to counter rising landfill fees for sludge, ensuring steady revenue despite only modest volume increases.

Europe's demand remains stable, particularly in Germany, the United Kingdom, France, and the Nordic countries. Energy price fluctuations are pushing a shift towards low-dose blends. France is incentivizing this shift with a EUR 500 million (~USD 585.06 million) subsidy plan for small utilities, especially rewarding those with ISO 9001 and NSF 60 certifications. While Spain's new irrigation reuse regulations boost coagulant use in Murcia and Almeria, budget limitations in Russia are restraining growth to a modest 1-2% annually. In South America and the Middle-East and Africa, niche opportunities arise in mining, desalination, and municipal zero liquid discharge (ZLD) projects, spurred by tightening effluent regulations in Brazil, copper tailings in Chile, and grand desalination initiatives in Saudi Arabia.

- Ashland Global Holdings Inc.

- BASF

- Buckman

- Chemtrade Logistics

- Dow

- Ecolab Inc.

- Feralco AB

- Grasim Industries Ltd.

- IXOM

- Kemira

- Kurita Water Industries Ltd.

- Nouryon

- SNF

- Solenis

- Solvay

- USALCO LLC

- Veolia Water Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter discharge norms for emerging-market industrial clusters

- 4.2.2 Rapid build-out of zero-liquid-discharge (ZLD) power and petrochem plants

- 4.2.3 Re-use mandates in water-scarce regions

- 4.2.4 Mature utility spending cycles in North America and Europe

- 4.2.5 AI-enabled dosing control platforms boosting chemical efficiency

- 4.3 Market Restraints

- 4.3.1 Regulatory toxicity spotlight on acrylamide monomer residues

- 4.3.2 Input price spikes for aluminium and ferric salts

- 4.3.3 Growing preference for membrane and electro-coagulation hybrids

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Coagulants

- 5.1.1.1 Inorganic Coagulants

- 5.1.1.2 Organic/Synthetic Coagulants

- 5.1.1.3 Natural/Bio-based Coagulants

- 5.1.2 Flocculants

- 5.1.2.1 Cationic Flocculants

- 5.1.2.2 Anionic Flocculants

- 5.1.2.3 Non-ionic Flocculants

- 5.1.1 Coagulants

- 5.2 By Application

- 5.2.1 Municipal Water Treatment

- 5.2.2 Industrial Wastewater Treatment

- 5.2.2.1 Pulp and Paper

- 5.2.2.2 Mining and Mineral Processing

- 5.2.2.3 Oil and Gas

- 5.2.2.4 Power Generation

- 5.2.2.5 Construction and Infrastructure

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Nordics

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Ashland Global Holdings Inc.

- 6.4.2 BASF

- 6.4.3 Buckman

- 6.4.4 Chemtrade Logistics

- 6.4.5 Dow

- 6.4.6 Ecolab Inc.

- 6.4.7 Feralco AB

- 6.4.8 Grasim Industries Ltd.

- 6.4.9 IXOM

- 6.4.10 Kemira

- 6.4.11 Kurita Water Industries Ltd.

- 6.4.12 Nouryon

- 6.4.13 SNF

- 6.4.14 Solenis

- 6.4.15 Solvay

- 6.4.16 USALCO LLC

- 6.4.17 Veolia Water Technologies

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Rise of fully bio-based coagulants for hypersaline wastewater