|

시장보고서

상품코드

2062034

사료용 메티오닌 첨가제 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Feed Methionine Additive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

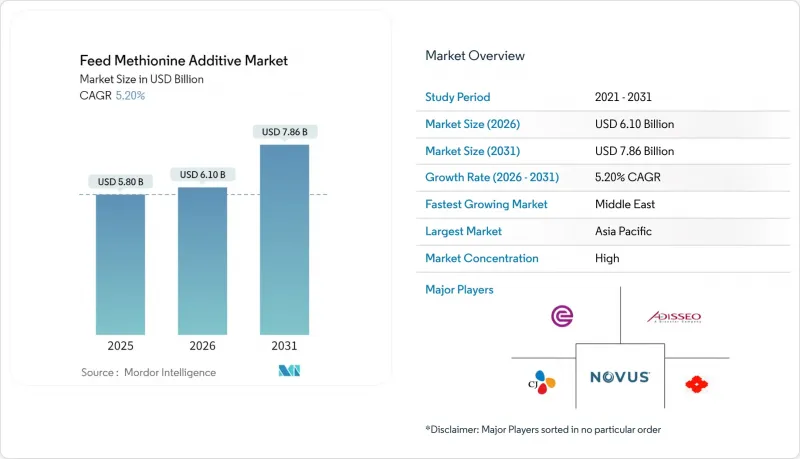

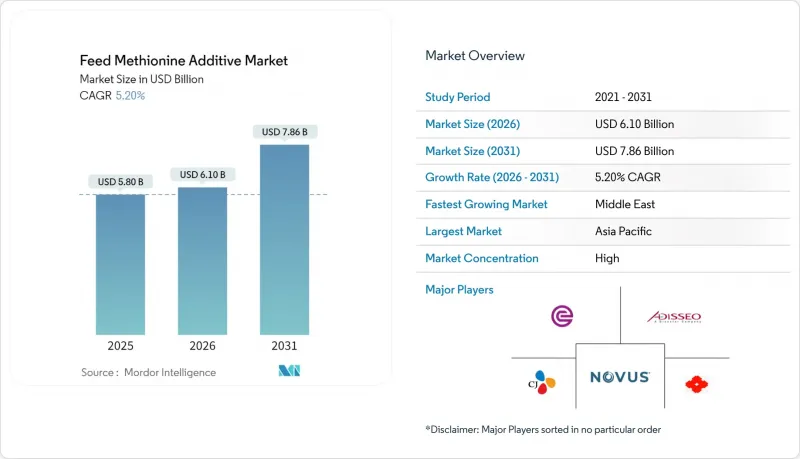

Mordor Intelligence에 의하면, 사료용 메티오닌 첨가제 시장 규모는 2025년 58억 달러로 평가되었고, 2026년에는 61억 달러로 추정되고, 2031년까지 78억 6,000만 달러에 이를 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 5.2%를 나타낼 전망입니다.

본 보고서는 제품 유형별(DL-메티오닌, L-메티오닌, 메티오닌 하이드록시 아날로그(MHA) 등), 형태별(분말 및 과립, 액체), 원료별(석유화학 유래, 바이오 유래), 대상 동물별(가금류, 돼지, 반추동물, 수산 양식 등), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 사료용 메티오닌 첨가제 시장 동향 및 분석

세계 가금육 생산의 확대

도시 소비자들의 합리적인 가격의 동물성 단백질에 대한 수요에 힘입어, 전 세계 닭고기 생산량은 계속 증가하고 있습니다. 유엔 식량농업기구(FAO)는 아시아태평양 지역과 남미에서 꾸준한 성장이 예상된다고 전망하며, 이는 육계 사육 시설의 확장과 메티오닌 사용량 증가와 관련이 있다고 보고 있습니다. 사료 원료 개선 과정에서 유황 함유 아미노산이 적은 비용 효율적인 식물성 단백질이 우선적으로 채택되고 있으며, 이에 따라 사료 요구율을 유지하기 위한 메티오닌 첨가량이 증가하고 있습니다. 2024년, 에보닉 오퍼레이션즈는 싱가포르에 연간 4만 톤 규모의 DL-메티오닌 생산 라인을 가동했습니다. 통합형 양계업자들은 매일의 메티오닌 목표치를 달성하기 위해 실시간 소프트웨어를 활용하고 있습니다.

수산물 양식 산업의 집약화 진전

생선이나 새우 양식장에서는 어분을 대두나 유채로 대체하는 움직임이 확산되고 있으며, 이에 따라 발생하는 메티오닌 부족 문제를 해결해야 합니다. 2022-2023년 실시된 태평양 흰새우에 관한 연구에 따르면, 사료 내 메티오닌 함량을 0.69-0.82%로 늘림으로써 생산성에 악영향을 주지 않으면서 어분 사용률을 18%에서 6%로 줄일 수 있었으며, 33.2%의 투자 수익률(ROI)을 달성한 것으로 나타났습니다. 현재 베트남의 새우 양식장이나 노르웨이의 연어 양식 케이지에서는 용출을 방지하기 위해 코팅 처리된 메티오닌이나 액상 메티오닌이 사용되고 있습니다. 각 공급업체들은 섭취 시 용해되는 마이크로캡슐화 제품을 공급하고 있으며, 이에 따라 사료용 메티오닌 첨가제 시장은 고밀도 순환식 양식 시스템으로 확대되고 있습니다.

변동이 심한 석유화학 원료 가격

2025년 초, 홍해에서의 수송 차질로 인해 유황과 아크롤레인의 가격이 상승했습니다. 계약 조건에는 원자재 가격 변동이 시차를 두고 반영되기 때문에 메티오닌의 이익률에 영향을 미쳤습니다. 황산암모늄으로 인한 비료 수입이 이러한 영향을 상쇄하는 데 도움이 되고 있습니다. 그러나 유황과 메티오닌의 가격이 동시에 하락할 경우, 소규모 생산자들은 어려움을 겪게 됩니다. Bluestar Adisseo Company와 같은 대형 통합 기업들은 생산 수준을 유지하기 위해 원료 리스크를 사내에서 관리하고 있지만, 독립 가공업체들은 종종 설비 유지보수를 연기하거나 가동률을 낮추는 경우가 많아 사료용 메티오닌 첨가제 시장으로의 신규 공급 증가가 제한되고 있습니다.

부문별 분석

2025년까지 DL-메티오닌은 사료용 메티오닌 첨가제 시장의 46%를 차지한 것으로 평가되었습니다. 메티오닌 하이드록시 아날로그(MHA) 시장 규모는 고밀도 육계 및 새우 양식 시스템에서의 투여를 용이하게 하는 액상 등급의 도입에 힘입어, 2026-2031년 연평균 성장률(CAGR) 7.8%로 확대될 것으로 전망됩니다. L-메티오닌은 소화율을 높이는 천연 이성체를 함유하고 있어, 특히 특수 양식용 사료에 효과적입니다. 그러나 높은 생산 비용이 시장 점유율 확대를 제한하고 있습니다.

자동화가 확대됨에 따라, 수요는 감시 제어 소프트웨어와 연동되는 액체 제품으로 이동하고 있습니다. 블루스타 아디세오(Bluestar Adisseo)는 이러한 추세를 반영하여 난징에 위치한 액체 생산 라인의 생산 능력을 확대했습니다. DL-메티오닌은 액체 인프라가 갖춰지지 않은 지역에서는 여전히 필수적입니다. 이는 다른 사료 첨가제와 함께 혼합 화물로, 자루나 빅백에 담아 운송할 수 있기 때문입니다. 그러나 연간 생산량이 많은 사료 공장에서는 액상 시스템의 높은 투자 대비 효과가 도입을 촉진하고 있으며, 사료용 메티오닌 첨가제 시장에서 MHA의 보급률을 높이고 있습니다. 캡슐화되거나 코팅된 제품은 영양소의 서방형 방출이 필요한 수생 생물에게 여전히 중요하며, 입자 형태를 맞춤 제작할 수 있는 제조업체에게는 틈새 시장이지만 안정적인 수익 기회를 제공합니다.

2025년 사료용 메티오닌 첨가제 시장 규모에서 분말 및 과립 제품이 64%로 가장 큰 점유율을 차지했습니다. 그러나 자동화 공장의 도입을 배경으로, 액상 메티오닌 시장 규모는 2026-2031년 연평균 성장률(CAGR) 7.5%로 가장 빠르게 성장할 것으로 전망됩니다. 이러한 제분 공장에서는 생산을 중단하지 않고도 마이크론 단위의 정확한 양을 공급할 수 있는 인라인 펌프가 선호됩니다. 액상 메티오닌은 미국 및 유럽연합(EU)의 산업안전 감사에서 중요한 요소인 흡입성 분진을 최소화하기 위한 수단으로서, 규정 준수 대책으로서의 매력이 높아지고 있습니다.

인프라가 미비한 지역에서는 사료 트럭이 여러 소규모 농장에 공급을 하기 때문에 분말 사료가 여전히 주류를 이루고 있습니다. 포장된 분말의 경우, 제분소는 유통기한이나 펌프 유지보수를 걱정할 필요 없이 수요 변동에 맞추어 배치 크기를 조정할 수 있습니다. 장거리 해상 운송의 경우, 특정 액체 형태에 필요한 냉장 드럼에 비해 유효 성분 1kg당 운임이 저렴하기 때문에 분말 형태가 선호됩니다. 그러나 업계 재편으로 생산이 대규모 공장으로 이전됨에 따라 운영상의 이점은 점점 더 액상 제품 쪽으로 기울고 있으며, 전 세계 사료용 메티오닌 첨가제 시장에서 액상 제품의 점유율은 점차 확대되고 있습니다.

지역별 분석

2025년, 아시아태평양은 사료용 메티오닌 첨가제 시장에서 38%라는 가장 높은 시장 점유율을 차지했습니다. 저장 NHU와 시노펙은 2023년 액체 메티오닌 관련 합작 사업을 발표하며, 아크롤레인공급을 확보하는 한편, 반덤핑 문제가 있음에도 불구하고 장기적인 자신감을 나타냈습니다. 태국에서는 새우 사료 공장의 급속한 자동화가 진행되었고, 인도에서는 복합 유우 사료로의 전환이 확대됨에 따라 고객 기반이 확대되었습니다. 환경 규제는 점점 더 엄격해지고 있지만, 지방 자치 단체들은 생명공학 산업에 세제 혜택을 제공하고 있으며, 이를 통해 규정 준수 비용을 상쇄함으로써 아시아태평양이 사료용 메티오닌 첨가제 제조 거점으로서의 입지를 공고히 하고 있습니다.

중동은 걸프협력회의(GCC) 회원국들이 식량 안보 이니셔티브에 정부 펀드를 투자하고 있어, 2026-2031년 연평균 성장률(CAGR) 8.1%로 가장 빠른 성장을 이룰 것으로 전망됩니다. 사우디아라비아의 대규모 수직 통합형 가금 복합 시설이나 아랍에미리트의 완전 순환식 양식 시스템의 경우, 공장 건설 전에 판매 계약을 체결함으로써 메티오닌 공급업체의 위험을 줄이고 있습니다. 2025년 홍해 항로 혼란으로 인한 운임 급등은 긴 공급망의 취약성을 여실히 드러냈으며, 지역별 메티오닌 혼합 거점 설립에 대한 논의를 가속화했습니다.

북미와 유럽에서는 가축 사육 두수가 성숙기에 접어들어 성장세가 완만하지만, 프리미엄 부문과 항생제 무사용 의무화가 안정적인 수요를 지속적으로 뒷받침하고 있습니다. 2026년, 미국 상무부가 스페인과 중국산 메티오닌 수입에 대해 실시한 조사가 불확실성을 초래함에 따라, 일부 사료 통합 기업들은 관세 위험을 완화하기 위해 고정 스프레드가 적용된 다년 국내 계약을 체결하기 시작했습니다. 유럽에서는 토지 이용 제약과 엄격한 황 배출 규제로 인해 생산자들은 신규 그린필드 프로젝트보다는 단계적인 병목 현상 해소에 주력하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the feed methionine additive market size is projected to grow from USD 5.80 billion in 2025 to USD 6.10 billion in 2026, reaching USD 7.86 billion by 2031, with a CAGR of 5.2% during 2026-2031.

This report is Segmented by Product Type (DL-Methionine, L-Methionine, Methionine Hydroxy Analog (MHA), and More), by Form (Powder and Granules, and Liquid), by Source (Petrochemical-Based, and Bio-Based), by Animal Type (Poultry, Swine, Ruminants, Aquaculture, and More), and by Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Feed Methionine Additive Market Trends and Insights

Escalating Global Poultry Meat Production

Global chicken production continues to rise, driven by urban consumers' demand for affordable animal protein. The Food and Agriculture Organization (FAO) forecasts steady growth in Asia-Pacific and South America, linking broiler facility expansion to higher methionine usage. Facility upgrades prioritize cost-effective plant proteins low in sulfur amino acids, prompting increased methionine supplementation to maintain feed-conversion ratios. In 2024, Evonik Operations GmbH commissioned a 40,000 metric ton per annum DL-Methionine line in Singapore. Integrators rely on real-time software to meet daily methionine targets.

Growth in Aquaculture Intensification

Fish and shrimp farms are replacing fishmeal with soy and rapeseed, creating methionine deficits that must be addressed. A 2022-2023 study on Pacific white shrimp showed that 0.69-0.82% dietary methionine reduced fishmeal from 18% to 6% without affecting performance, yielding a 33.2% ROI. Shrimp ponds in Vietnam and salmon cages in Norway now use coated or liquid methionine variants to resist leaching. Suppliers are offering micro-encapsulated grades that dissolve upon ingestion, helping the feed methionine additive market expand into high-density recirculating systems.

Volatile Petrochemical Feedstock Prices

Sulfur and acrolein increase in early 2025 due to shipping disruptions in the Red Sea. Methionine margins were affected as contract formulas incorporate raw material price changes with a delay. Fertilizer revenue from ammonium sulfate helps offset such impacts. However, when both sulfur and methionine prices decline simultaneously, smaller producers encounter difficulties. Large integrated companies, such as Bluestar Adisseo Company, manage feedstock risks internally to sustain production levels, whereas independent processors often postpone maintenance or lower operating rates, restricting new supply additions to the feed methionine additive market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Premium Pet Food

- Regulatory Push for Reduced Antibiotic Usage in Feed

- Strict Regulations Impact Sulfur Emissions in Production

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DL-Methionine is accounted for 46% of the feed methionine additive market by 2025. The Methionine Hydroxy Analog (MHA) market size is projected to grow at a CAGR of 7.8% from 2026 to 2031, driven by the adoption of liquid grades that facilitate dosing in high-density broiler and shrimp systems. L-Methionine is particularly effective in specialty aquaculture diets due to its natural isomer, which enhances digestibility. However, its high production cost limits its market share.

As automation continues to expand, the demand is shifting toward liquid products that integrate with supervisory control software. Bluestar Adisseo Company has increased the capacity of its Nanjing liquid production line to align with this trend. DL-Methionine remains essential in regions without liquid infrastructure, as it can be transported in sacks and big bags alongside other feed additives via mixed freight. However, for feed mills with higher annual output, the return on investment for a liquid system encourages adoption and increases MHA penetration in the feed methionine additive market. Encapsulated or coated variants remain significant for aquatic species requiring slow nutrient release, creating niche but stable revenue opportunities for producers capable of customizing particle morphology.

Powder and granules accounted for the largest share, 64%, of the feed methionine additive market size in 2025. However, liquid methionine market size is projected to grow at the fastest rate, with a CAGR of 7.5% from 2026 to 2031, driven by its adoption in automated mills. These mills favor inline pumps that deliver precise micron-level volumes without interrupting production. Liquid methionine minimizes respirable dust, a critical factor in occupational safety audits in the United States and European Union, enhancing its appeal as a compliance solution.

Powders remain prevalent in regions with fragmented infrastructure, where feed trucks supply multiple small farms. Bagged powders enable mills to align batch sizes with demand fluctuations without concerns about shelf life or pump maintenance. Long-haul maritime transport favors powders due to lower freight costs per active kilogram compared to the refrigerated drums required for certain liquid forms. However, as industry consolidation shifts more production to large-scale mills, the operational advantages increasingly favor liquids, gradually increasing their share in the global feed methionine additive market.

Geography Analysis

Asia-Pacific accounted for the largest 38% market share of the feed methionine additive market in 2025. Zhejiang NHU Co., Ltd. and Sinopec announced a joint venture for liquid methionine in 2023, ensuring acrolein supply and reflecting long-term confidence despite anti-dumping challenges. In Thailand, rapid automation in shrimp feed mills and India's shift toward compound dairy rations have expanded the customer base. While environmental regulations are becoming stricter, local governments are offering tax incentives to biotechnology, helping offset compliance costs and reinforcing Asia-Pacific's position as the manufacturing hub for feed methionine additives.

The Middle East is projected to achieve the fastest growth, with a CAGR of 8.1% from 2026 to 2031, as Gulf Cooperation Council countries invest sovereign funds in food-security initiatives. Large vertically integrated poultry complexes in Saudi Arabia and full-recirculation aquaculture systems in the United Arab Emirates are securing offtake agreements before plant construction, reducing risks for methionine suppliers. Freight cost spikes during the 2025 Red Sea disruptions highlighted the vulnerability of long supply chains, accelerating discussions on establishing regional methionine formulation hubs.

In North America and Europe, growth remains moderate due to mature livestock inventories, but premium segments and antibiotic-free mandates continue to support consistent demand. In 2026, the United States Department of Commerce's investigation into Spanish and Chinese methionine imports created uncertainty, prompting some feed integrators to secure multi-year domestic contracts with fixed spreads to mitigate tariff risks. In Europe, producers are focusing on incremental debottlenecking rather than new greenfield projects, constrained by land-use limitations and stringent sulfur regulations.

- Evonik Industries AG

- Adisseo Animal Nutrition Private Limited

- Novus International, Inc.

- CJ CheilJedang Corporation

- Sumitomo Chemical Co., Ltd.

- Zhejiang NHU Co., Ltd.

- Sichuan Hebang Biotechnology Co., Ltd.

- Chongqing Unisplendour Chemical Co., Ltd.

- Ningxia Eppen Biotech Co., Ltd.

- Volzhsky Orgsynthese, JSC

- Ajinomoto Co., Inc.

- Kemin Industries, Inc.

- Phibro Animal Health Corporation

- Archer Daniels Midland Company

- Prinova Group LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating global poultry meat production

- 4.2.2 Growth in aquaculture intensification

- 4.2.3 Rising demand for premium pet food

- 4.2.4 Regulatory push for reduced antibiotic usage in feed

- 4.2.5 Single-step fermentation reduces capital expenditure

- 4.2.6 AI-driven algorithms optimize methionine-to-lysine ratios

- 4.3 Market Restraints

- 4.3.1 Volatile petrochemical feedstock prices

- 4.3.2 Strict regulations impact sulfur emissions in production

- 4.3.3 Global supply chains increase exposure to anti-dumping penalties

- 4.3.4 Electrolytic oxidation waste management adds significant costs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 DL-Methionine

- 5.1.2 L-Methionine

- 5.1.3 Methionine Hydroxy Analog (MHA)

- 5.1.4 Other Product Types

- 5.2 By Form

- 5.2.1 Powder and Granules

- 5.2.2 Liquid

- 5.3 By Source

- 5.3.1 Petrochemical-based

- 5.3.2 Bio-based

- 5.4 By Animal Type

- 5.4.1 Poultry

- 5.4.2 Swine

- 5.4.3 Ruminants

- 5.4.4 Aquaculture

- 5.4.5 Pet Food

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Spain

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Indonesia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Evonik Industries AG

- 6.4.2 Adisseo Animal Nutrition Private Limited

- 6.4.3 Novus International, Inc.

- 6.4.4 CJ CheilJedang Corporation

- 6.4.5 Sumitomo Chemical Co., Ltd.

- 6.4.6 Zhejiang NHU Co., Ltd.

- 6.4.7 Sichuan Hebang Biotechnology Co., Ltd.

- 6.4.8 Chongqing Unisplendour Chemical Co., Ltd.

- 6.4.9 Ningxia Eppen Biotech Co., Ltd.

- 6.4.10 Volzhsky Orgsynthese, JSC

- 6.4.11 Ajinomoto Co., Inc.

- 6.4.12 Kemin Industries, Inc.

- 6.4.13 Phibro Animal Health Corporation

- 6.4.14 Archer Daniels Midland Company

- 6.4.15 Prinova Group LLC