|

시장보고서

상품코드

2062043

Bluetooth Smart 및 Smart Ready : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bluetooth Smart And Smart Ready - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

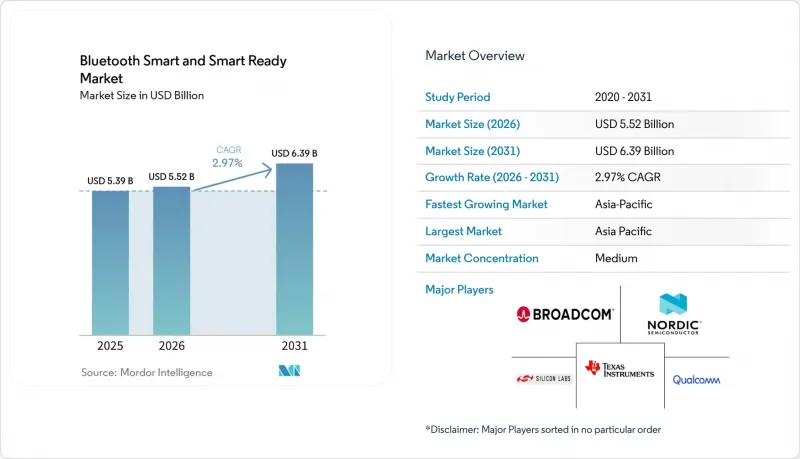

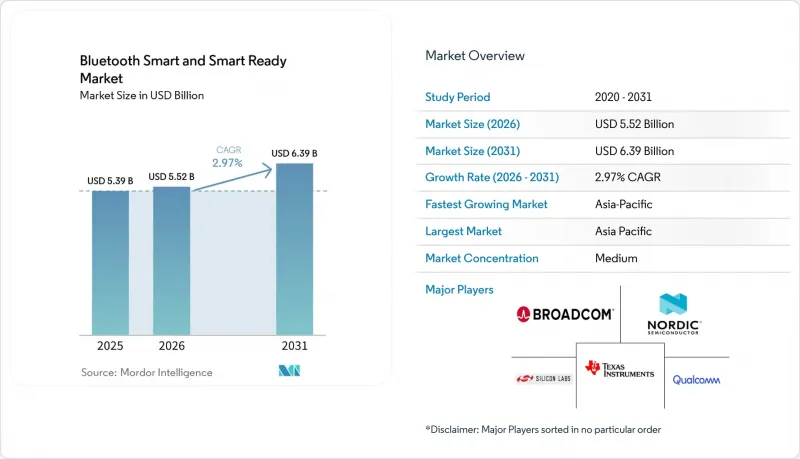

Mordor Intelligence에 의하면, Bluetooth Smart 및 Smart Ready 시장 규모는 2025년 53억 9,000만 달러로 평가되었고, 2026년에는 55억 2,000만 달러로 추정되고, 2026-2031년 CAGR 2.97%로 성장을 지속할 전망이며, 2031년까지 63억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(블루투스 스마트 기기, 블루투스 스마트 레디 기기), 기술별(블루투스 로우 에너지, 블루투스 클래식, 블루투스 메시, 블루투스 5.0, 기타), 용도별(헬스케어, 웨어러블 기기, 스마트 홈, 기타), 최종 사용자 산업별(가전, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 Bluetooth Smart 및 Smart Ready 시장 동향과 인사이트

IoT 노드 도입 대수 증가

블루투스 지원 기기의 출하 대수는 2025년에 53억 대에 달했고, 2029년까지 80억 대에 육박할 것으로 예상되어, 블루투스 스마트(Bluetooth Smart)와 스마트 레디(Smart Ready) 시장을 주도할 만큼 그 규모가 크다는 점이 부각되고 있습니다. 현재 산업, 농업, 빌딩 자동화 프로젝트에서는 온도, 습도, 재실 여부 측정을 위해 메시(Mesh)를 지원하는 블루투스 저에너지(Bluetooth Low Energy) 센서가 채택되고 있으며, 이를 통해 독자 사양의 게이트웨이를 사용하지 않음으로써 부품 비용을 30% 가까이 절감하고 있습니다. 엣지 아키텍처에서는 모든 스마트폰이 필드 프로그래머 역할을 수행하여 도입 및 유지보수를 신속하게 진행할 수 있기 때문에 이 프로토콜이 선호되고 있습니다. 이러한 추세는 코인형 배터리식 센서의 출하량을 직접적으로 끌어올렸으며, 2025년에는 전년 대비 22%의 성장률을 기록했습니다. 향후 10년 동안 1마이크로암페어 이하의 동작 전류가 실현됨에 따라, 이러한 기술의 도입 추세는 더욱 가속화될 것이며, 전력 소비에 민감한 엔드포인트 분야에서 Zigbee나 Z-Wave와의 격차를 더욱 벌려나갈 것으로 예측됩니다.

스마트폰 OEM을 통한 LE Audio 사양 채택

Samsung Electronics는 2025년 1월, 갤럭시 S25 시리즈에 LE Audio를 기본 지원하도록 탑재하여, 게이트 안내 방송이나 음악을 호환되는 이어폰이나 보청기로 스트리밍하는 Auracast 방송을 가능하게 했습니다(samsung.com). 이에 이어 구글은 2026년 2월 미리 공개된 안드로이드 16에 LE 오디오 API의 통합을 의무화함으로써, 향후 출시될 단말기가 멀티스트림 오디오 및 저지연 방송 기능을 제공할 수 있도록 보장했습니다. 공공 장소에서는 이미 Auracast 송신기 설치가 진행 중이며, 2025년 3월에는 시카고 오헤어 공항에서 120개의 비콘이 가동을 시작해 해당 지역 맞춤형 음성 정보를 승객의 기기로 직접 전송하고 있습니다. 이러한 업그레이드 주기로 인해, 스마트폰 제조업체들은 전환 기간 동안 Classic Audio와 LE Audio를 모두 지원해야 하며, 이로 인해 검증 항목이 두 배로 늘어나면서 듀얼 모드 시스템 온 칩(SoC)에 대한 수요가 증가하고 있습니다. LE Audio로의 전환이 진행됨에 따라 싱글 모드 설계가 가속화되고, Bluetooth Smart 및 Smart Ready 시장의 성장세가 더욱 강화될 것으로 보입니다.

Bluetooth Classic 스택의 보안 취약점

National Vulnerability Database(NVD)는 2025-2026년 Classic 스택과 관련된 심각도가 높은 CVE 17건을 기록했습니다. 여기에는 Zephyr, Linux, Airoha 칩셋에 대한 익스플로잇이 포함됩니다. 이와 관련된 리콜 규모는 230만 대에 달했으며, 스마트 홈용 잠금 장치와 의료용 모니터에서는 다운그레이드 공격이 계속되었습니다. 많은 OEM 업체들이 AES-128 기반의 보안 연결을 지원하는 Bluetooth Low Energy로 전환하고 있지만, 약 32억 대의 Classic 전용 기기가 여전히 사용 중이어서 공격의 여지가 남아 있습니다. 이러한 위험 요인은 신뢰를 훼손할 뿐만 아니라, 도입 기반이 갱신될 때까지 블루투스 스마트(Bluetooth Smart) 및 스마트 레디(Smart Ready) 시장의 단기적인 성장을 저해할 것입니다.

부문별 분석

2025년 블루투스 스마트 및 스마트 레디 시장의 매출액 중 블루투스 스마트 기기가 61.32%를 차지했으며, 이러한 우위는 연평균 성장률(CAGR) 3.37%를 기록하며 더욱 확대될 것으로 예측됩니다. 그 매력은 혈당 모니터, 자산 태그, 피트니스 트래커 등이 코인형 배터리로 수년 동안 작동할 수 있는 초저전력 프로파일에 있습니다. 블루투스 스마트(Bluetooth Smart) 및 스마트 레디(Smart Ready) 시장의 스마트 기기 시장 규모는 2031년까지 증가할 출하량의 대부분을 차지할 것으로 예측됩니다.

듀얼 모드 Smart Ready 장치는 자동차 인포테인먼트 및 산업용 게이트웨이 분야에서 여전히 필수적이지만, 구조적인 역풍에 직면해 있습니다. Classic 스택의 작동 전류가 약 30mA인 반면, Bluetooth Low Energy는 5mA 이하이며, 이러한 차이로 인해 하드웨어 설계자들은 싱글 모드 칩을 채택하고 있습니다. 부품 공급업체들도 이러한 변화를 반영하고 있으며, Nordic의 22nm 공정으로 제작된 nRF54L은 Cortex-M33과 RISC-V 코프로세서를 결합하여 수신 전류를 3μA 이하로 낮췄습니다. 한편, Silicon Labs의 BG29는 보청기용으로 2.0mm×2.5mm 크기의 패키지에 1MB의 플래시 메모리를 탑재하고 있습니다. 그 결과, Smart Ready 시장 점유율은 줄어들고 있지만, 프리미엄 스마트폰이나 노트북의 경우 하위 호환성이 필수적인 틈새 시장에서 출하량은 유지될 것으로 보입니다.

2025년에는 Bluetooth Low Energy가 출하 대수의 46.36%를 차지했으나, 소매, 창고, 병원의 자산 관리 분야에서 도착각 측위(AoA)에 대한 수요가 증가함에 따라 Bluetooth 5.1이 3.97%라는 가장 높은 연평균 성장률(CAGR)을 기록했습니다. 블루투스 5.1 태그와 관련된 블루투스 스마트(Bluetooth Smart) 및 스마트 레디(Smart Ready) 시장 규모는 1미터 이내의 정확도라는 장점 덕분에, 비용 효율성을 중시하는 상황에서 고가의 초광대역(UWB) 기술을 대체할 수 있게 해줍니다. 레거시 Classic은 자동차 핸즈프리 프로파일의 지원에 힘입어 28%의 점유율을 유지했으나, LE Audio가 정착함에 따라 성장률은 1.2%로 둔화되었습니다.

블루투스 메시(Bluetooth Mesh)는 12%의 시장 점유율을 기록했으며, 특히 상업용 조명 부문에서 통합된 Matter 펌웨어를 기반으로 점유율을 확대했습니다. 블루투스 5.0은 블루투스 5.4와 6.0에서 도입된 주기적 광고 및 채널 사운딩 기능을 지원하는 새로운 칩셋이 등장함에 따라 그 중요성이 줄어들었습니다. 텍사스 기기(Texas Instruments), NXP, 실리콘 랩(Silicon Labs)은 모두 2025년 1월부터 2026년 4월 사이에 블루투스 6.0 지원 반도체 제품을 출시하고 있으며, 이는 블루투스 스마트(Bluetooth Smart) 및 스마트 레디(Smart Ready) 시장의 성장세를 유지하기 위한 급격한 전환 추세를 시사합니다.

지역별 분석

아시아태평양은 Bluetooth Smart 및 Smart Ready 시장을 주도하며, 2025년에는 매출의 38.83%를 차지했으며, 연평균 성장률(CAGR)은 3.83%를 나타낼 것으로 전망됩니다. 중국은 2025년 1월 이후 판매되는 모든 스마트 홈 가전제품에 블루투스 저에너지(Bluetooth Low Energy) 탑재를 의무화하여, Midea나 Haier 등 OEM 업체들의 도입을 촉진했습니다. 일본의 주요 가전 제조업체들은 2025년형 TV에 LE Audio를 탑재한 반면, 한국의 갤럭시 S25 시리즈는 2026년 1분기에 4,200만 대가 판매되었습니다. 2026년 3월에 발표된 인도의 블루투스 의료기기 관련 규격안은 승인 절차를 효율화하고, 연결형 혈당 측정기의 잠재 시장을 확대할 것입니다.

북미는 28% 시장 점유율과 2.9%의 연평균 성장률(CAGR)을 기록했습니다. FDA의 사이버 보안 지침 강화는 규정 준수 관련 비용을 증가시켰지만, 한편으로는 보험 적용 대상이 되는 원격 환자 모니터링의 길을 열었습니다. 미국의 반도체 정책에 따라 국내 파브에 527억 달러가 투입되고 있지만, 40nm 이하 제조 능력은 2028년까지 가동되지 않을 예정이므로 당분간 대부분의 블루투스 SoC는 대만과 한국에 의존하는 상황이 지속될 것입니다. 캐나다는 전력 제한을 FCC 규정에 부합하도록 조정했으며, 멕시코의 자동차 생산 라인에서는 2025년에 180만 대의 차량에 블루투스 디지털 키가 탑재되었습니다.

유럽은 2025년을 매출 24%, 연평균 성장률(CAGR) 2.7%로 마감했습니다. 2025년 8월에 시행된 무선기기 지침의 사이버 보안 조항은 의료용 센서부터 스마트 홈 허브에 이르기까지, 해당 지역 내에서 판매되는 모든 블루투스 무선 기기에 적용되게 되었습니다. 독일의 자동차 제조업체는 릴레이 공격을 방지하기 위해 블루투스 6.0의 채널 사운딩 기술을 도입했으며, 영국 국민보건서비스(NHS)는 만성 질환 환자 12만 명을 대상으로 블루투스 연결형 모니터의 시범 운영을 실시했습니다. 남미, 중동 및 아프리카의 합계 점유율은 10%, 연평균 성장률(CAGR)은 2.4%였습니다. 브라질의 아나텔(Anatel)은 2025년 4월에 인증 기준을 ETSI EN 300 328에 부합하도록 조정했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the bluetooth smart and Smart Ready market size is expected to grow from USD 5.39 billion in 2025 to USD 5.52 billion in 2026 and is forecast to reach USD 6.39 billion by 2031 at a 2.97% CAGR over 2026-2031.

This report is Segmented by Product Type (Bluetooth Smart Devices, and Bluetooth Smart Ready Devices), Technology (Bluetooth Low Energy, Bluetooth Classic, Bluetooth Mesh, Bluetooth 5. 0, and More), Application (Healthcare, Wearable Devices, Smart Home, and More), End-User Industry (Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Bluetooth Smart And Smart Ready Market Trends and Insights

Growing Installed Base of IoT Nodes

Shipments of Bluetooth-enabled devices climbed to 5.3 billion units in 2025, and forecasts approach 8 billion by 2029, underscoring the scale that is fueling the Bluetooth Smart and Smart Ready market. Industrial, agricultural, and building-automation projects now specify mesh-enabled Bluetooth Low Energy sensors for temperature, humidity, and occupancy, avoiding proprietary gateways and trimming bill-of-materials cost by nearly 30%. Edge architectures favor the protocol because every smartphone can act as a field programmer, accelerating commissioning and maintenance. The trend directly lifts coin-cell sensor volumes, which grew 22% year over year in 2025. The adoption wave strengthens over the next decade as sub-1-microampere active currents arrive, widening the gap with Zigbee and Z-Wave in power-sensitive endpoints.

Smartphone OEM Adoption of LE Audio Specification

Samsung built native LE Audio support into its Galaxy S25 series in January 2025, enabling Auracast broadcasts that stream gate announcements and music to any compatible earbud or hearing aid (samsung.com). Google followed by embedding mandatory LE Audio APIs in Android 16, previewed in February 2026, ensuring that future handsets expose multi-stream audio and low-latency broadcast functions. Public venues are already installing Auracast transmitters; 120 beacons went live at Chicago's O'Hare airport in March 2025, to pipe localized audio directly to passengers' devices. The upgrade cycle obliges smartphone vendors to support both Classic and LE Audio during transition, doubling validation matrices and driving demand for dual-mode system-on-chips. As the installed base flips toward LE Audio, single-mode designs will accelerate, reinforcing volume growth for the Bluetooth Smart and Smart Ready market.

Security Vulnerabilities in Bluetooth Classic Stack

The National Vulnerability Database logged 17 high-severity CVEs tied to the Classic stack in 2025-2026, including exploits in Zephyr, Linux, and Airoha silicon. Associated recalls spanned 2.3 million vehicles, and downgrade attacks persisted in smart-home locks and medical monitors. Although many OEMs are migrating to Bluetooth Low Energy with AES-128 secure connections, roughly 3.2 billion Classic-only devices remain in service, keeping exploit windows open. The risk erodes confidence and clips near-term expansion for the Bluetooth Smart and Smart Ready market until the installed base is refreshed.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Connected-Healthcare Devices

- Rising Demand for Location-Based Retail Analytics

- Chip-Level Supply Constraints for Sub-40 nm Nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bluetooth Smart Devices accounted for 61.32% of 2025 revenue within the Bluetooth Smart and Smart Ready market, a dominance expected to widen under a 3.37% CAGR. Their appeal stems from ultra-low-power profiles that let glucose monitors, asset tags, and fitness trackers operate for years on coin-cell batteries. The Bluetooth Smart and Smart Ready market size for Smart Devices is projected to capture the lion's share of incremental shipments through 2031 as smartphone operating systems phase out Classic profiles.

Dual-mode Smart Ready Devices, while still vital for automotive infotainment and industrial gateways, face structural headwinds. Classic stacks draw roughly 30 mA of active current compared with sub-5 mA for Bluetooth Low Energy, a disparity that pushes hardware designers toward single-mode silicon. Component suppliers signal the shift, Nordic's 22-nanometer nRF54L pairs a Cortex-M33 with a RISC-V coprocessor to cut receive currents below 3 µA, while Silicon Labs' BG29 squeezes 1 MB of Flash into a 2.0 mm X 2.5 mm package for hearing aids. As a result, Smart Ready share recedes, but premium smartphones and laptops will preserve niche volumes where backward compatibility is mandatory.

Bluetooth Low Energy held 46.36% of shipments in 2025, yet Bluetooth 5.1 clocked the fastest CAGR at 3.97% on the strength of angle-of-arrival ranging for retail, warehousing, and hospital asset management. The Bluetooth Smart and Smart Ready market size tied to Bluetooth 5.1 tags benefits from sub-meter accuracy, enabling it to replace costly ultra-wideband in cost-sensitive scenarios. Legacy Classic retained 28% share, buoyed by automotive hands-free profiles, but growth slowed to 1.2% as LE Audio takes hold.

Bluetooth Mesh reached 12% share and improved under converged Matter firmware, especially in commercial lighting. Bluetooth 5.0 slipped in relevance as new chipsets embrace periodic advertising and channel sounding introduced in Bluetooth 5.4 and 6.0. Texas Instruments, NXP, and Silicon Labs all rolled out 6.0-ready silicon between January 2025 and April 2026, signaling a steep migration curve that keeps the Bluetooth Smart and Smart Ready market momentum intact.

Geography Analysis

Asia-Pacific led the Bluetooth Smart and Smart Ready market, accounting for 38.83% of revenue in 2025 and a 3.83% CAGR outlook. China mandated Bluetooth Low Energy in all smart-home appliances sold after January 2025, driving adoption across OEMs such as Midea and Haier. Japanese electronics giants embedded LE Audio in 2025 model-year televisions, while South Korea's Galaxy S25 family moved 42 million units in Q1 2026. India's draft standards for Bluetooth medical devices, released in March 2026, will streamline approvals and widen the addressable base for connected glucose monitors.

North America secured 28% share and a 2.9% CAGR. The FDA's stricter cybersecurity guidance lifted compliance spend but also cleared the path for reimbursable remote patient monitoring. U.S. semiconductor policy channels USD 52.7 billion into domestic fabs, yet sub-40-nanometer capacity will not come online until 2028, keeping most Bluetooth SOCs tied to Taiwan and South Korea in the interim. Canada harmonized power limits with FCC rules, and Mexico's vehicle production line fitted 1.8 million cars with Bluetooth digital keys in 2025.

Europe finished 2025 with 24% revenue and a 2.7% CAGR. The Radio Equipment Directive's August 2025 cyber clause now applies to every Bluetooth radio sold in the bloc, from medical sensors to smart-home hubs. German automakers adopted Bluetooth 6.0 channel sounding to guard against relay attacks, and the NHS piloted Bluetooth-connected monitors for 120,000 chronic-care patients. South America, the Middle East, and Africa combined for 10% share and a 2.4% CAGR, with Brazil's Anatel harmonizing certification to ETSI EN 300 328 in April 2025.

- Qualcomm Inc.

- Nordic Semiconductor ASA

- Texas Instruments Incorporated

- Broadcom Inc.

- Silicon Laboratories Inc.

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Microchip Technology Inc.

- Cypress Semiconductor Corporation

- Realtek Semiconductor Corp.

- Murata Manufacturing Co. Ltd.

- Atmosic Technologies Inc.

- Dialog Semiconductor plc

- Espressif Systems (Shanghai) Co. Ltd.

- MediaTek Inc.

- Toshiba Electronic Devices & Storage Corp.

- Panasonic Holdings Corp.

- ON Semiconductor Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Installed Base of IoT Nodes

- 4.2.2 Smartphone OEM Adoption of LE Audio Specification

- 4.2.3 Regulatory Push for Connected-Healthcare Devices

- 4.2.4 Rising Demand for Location-Based Retail Analytics

- 4.2.5 Convergence of Bluetooth Mesh With Matter Standard

- 4.2.6 Ultra-Low-Power SoC Road-maps From Fabless Vendors

- 4.3 Market Restraints

- 4.3.1 Security Vulnerabilities in Bluetooth Classic Stack

- 4.3.2 Chip-Level Supply Constraints for Sub-40 nm Nodes

- 4.3.3 Inter-Protocol Interference in Dense RF Environments

- 4.3.4 Fragmented Firmware Update Ecosystem for OEMs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Bluetooth Smart Devices

- 5.1.2 Bluetooth Smart Ready Devices

- 5.2 By Robot Type

- 5.2.1 Industrial Robots

- 5.2.2 Collaborative Robots

- 5.2.3 Professional Service Robots

- 5.2.4 Domestic Service Robots

- 5.2.5 Humanoid Robots

- 5.3 By Technology

- 5.3.1 Bluetooth Low Energy

- 5.3.2 Bluetooth Classic

- 5.3.3 Bluetooth Mesh

- 5.3.4 Bluetooth 5.0

- 5.3.5 Bluetooth 5.1

- 5.4 By Application

- 5.4.1 Healthcare

- 5.4.2 Wearable Devices

- 5.4.3 Smart Home

- 5.4.4 Automotive

- 5.4.5 Industrial Automation

- 5.5 By End-User Industry

- 5.5.1 Consumer Electronics

- 5.5.2 Healthcare

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Retail

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Qualcomm Inc.

- 6.4.2 Nordic Semiconductor ASA

- 6.4.3 Texas Instruments Incorporated

- 6.4.4 Broadcom Inc.

- 6.4.5 Silicon Laboratories Inc.

- 6.4.6 NXP Semiconductors N.V.

- 6.4.7 STMicroelectronics N.V.

- 6.4.8 Infineon Technologies AG

- 6.4.9 Renesas Electronics Corporation

- 6.4.10 Microchip Technology Inc.

- 6.4.11 Cypress Semiconductor Corporation

- 6.4.12 Realtek Semiconductor Corp.

- 6.4.13 Murata Manufacturing Co. Ltd.

- 6.4.14 Atmosic Technologies Inc.

- 6.4.15 Dialog Semiconductor plc

- 6.4.16 Espressif Systems (Shanghai) Co. Ltd.

- 6.4.17 MediaTek Inc.

- 6.4.18 Toshiba Electronic Devices & Storage Corp.

- 6.4.19 Panasonic Holdings Corp.

- 6.4.20 ON Semiconductor Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment